Election and Interest Rate Week, Is A Bubble Inflating? (NOTW#20)

Don’t forget that Best Anchor Stocks has a partnership with Finchat (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

Hi reader,

Indices were significantly up this week on the back of two relevant events: the US Presidential Election and the Fed’s interest rate decision. I share my view on both topics and explain what I think about the current market environment. I don’t intend to time the market, but I am human and obviously have a view of where things stand today. I also share the the earnings digest of one of the company’s in my portfolio in the news section (reserved for paid subscribers).

Without further ado, let’s get on with it.

Articles of the week

I published three articles this week (one can tell it’s earnings season), all of them free to read. The first article of the week was Amazon’s earnings digest, where I discussed the numbers and explained why I think Andy Jassy doesn’t get the credit he deserves. The stock has lagged since becoming CEO, but it might be too soon to judge him just based on this metric alone.

The second article of the week was a rather special one. I discussed two industries offering an asymmetric bet on AI; they can enjoy growth opportunities without suffering too many disruption risks. The Best Anchor Stock portfolio (and, therefore, my portfolio) is exposed to both industries.

The third article was Nintendo’s 6-month earnings digest. The company reported what appears to be a poor quarter, but it was actually a pretty good quarter from a long-term investor’s perspective.

I also sent an email to paid subscribers with the earnings digest of the latest addition to my portfolio. I honestly wasn’t expecting such a strong short-term pop, but the stock is up 20% from my cost basis in just one month (it’s very volatile due to its low float). I have not finished building my position so I evidently don’t like it. I’ve thus far published three parts of this company’s article series (three more to go):

If you want to access this article series and the rest of the deep dives, you can do so by subscribing to Best Anchor Stocks:

Market Overview

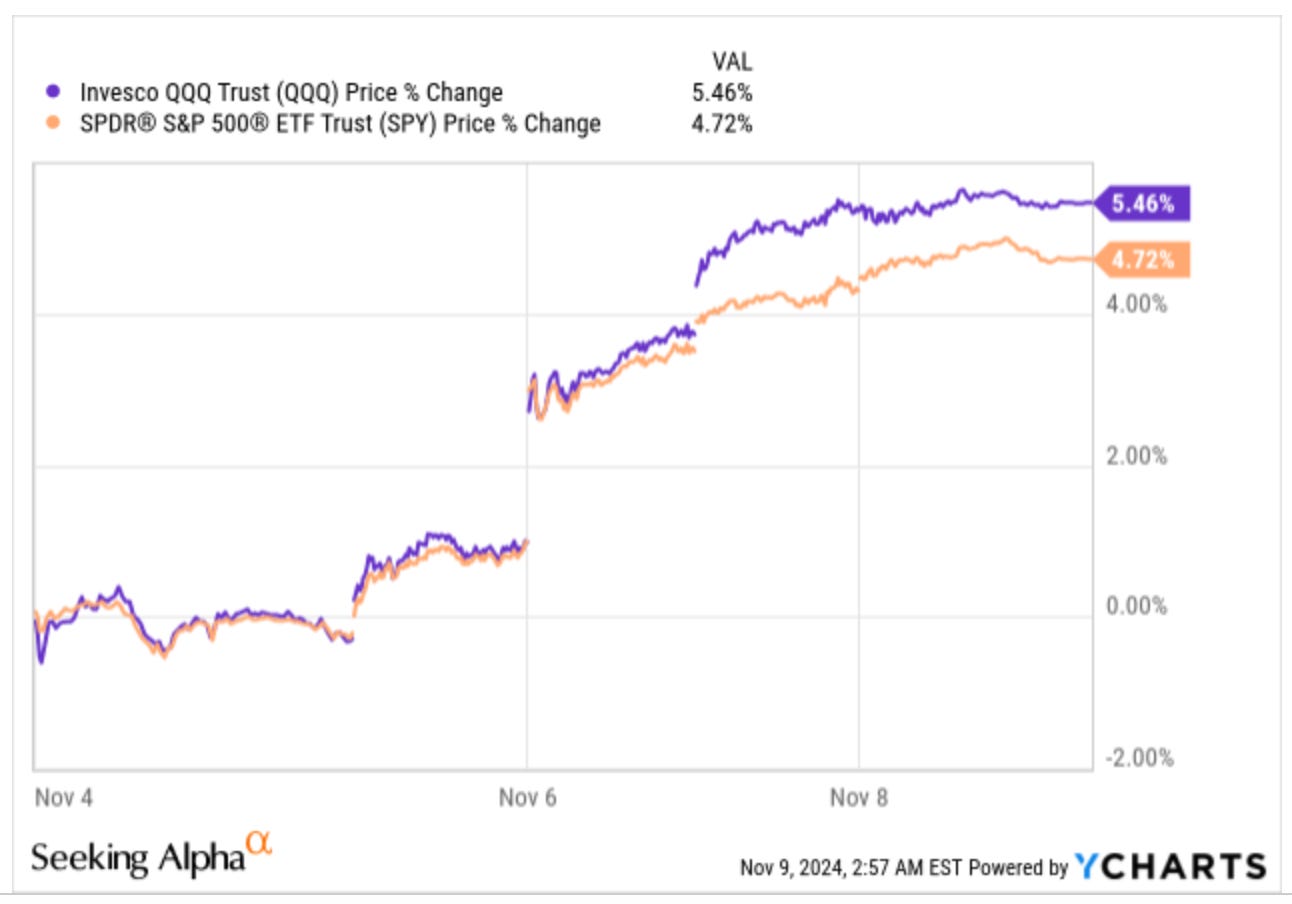

The indices had an outstanding week. The Nasdaq was up more than 5% whereas the S&P 500 was up more than 4%:

What caused this “huge” run? Well, more than how this week’s events per se unfolded, it probably has more to do with the fact that they unfolded and, therefore, significantly reduced uncertainty. It was a pretty relevant week in terms of data for markets as the US held its Presidential election and the Fed announced yet another rate cut. Let me discuss both briefly.

Once the result of the US election was said and done (Trump won, in case you are living under a rock), many people started claiming that the market (or this or that stock) was going up because Trump got elected. While this might be true, it seems to have more to do with the fact that uncertainty is behind us. The market hates uncertainty, and we’ll never know how it would’ve reacted if Kamala Harris won.

Interestingly, people seemed to know what the next 4 years would bring for the companies in their portfolio based on what the stock price was doing the day following the election. Everyone is speculating about what could happen during Trump’s second tenure, primarily by taking at face value everything he’s said during his campaign. You might have seen that I highlighted the word “second” in the preceding sentence; that’s because I want to highlight that this is not Trump’s first mandate, and during the first one the world did not end, and good companies did just fine. What a candidate says during the campaign is typically very different from what they do when they become President. This is a tale as old as time in politics.

Anyways, the market’s rise was also aided by the Fed’s decision to lower interest rates by 25 basis points. This was followed by Jerome Powell’s words claiming that the economy is in a good place. I honestly don’t understand why the Fed would lower rates into a strong economy; there seem to be only downsides to being pro-cyclical. This said, there’s little I can do to change what they do, and I don’t have as much data as they do, so I try to focus on things I can control.

Both events took the indices close to or to all-time highs, something that has people thinking that a potential bubble might be inflating in the US. One of the things they claim to defend their posture is that the P/E ratio of the S&P 500 is reaching the high end of the 10-year historical series. The forward P/E multiple is around 22, which is above the 5-year average of 19.6 and the 10-year average of 18.1:

There’s no denying that 22x forward earnings seems expensive for an index, but it definitely doesn’t look like bubble territory. We should consider that this index is now more concentrated among higher-quality companies than it was in the past, so all things equal, it likely deserves a higher multiple. The question is obviously “to what extent.”

Another thing investors should consider is that Trump said during the electoral race that he would lower corporate taxes from 21% to 15% for companies that made their products in the US. According to Fortune, this would immediately boost S&P 500 earnings by 4% (I don’t know how they calculated this). If this earnings boost is accurate then, all things equal, the S&P 500 is actually trading at a multiple of around 21x, which still seems a bit frothy but less so. Of course, lower taxes also mean that companies have more money to invest in growth, which could potentially lead to higher growth going forward. We still don’t know if this tax cut will come to life or how exactly it will impact S&P 500 earnings, but it seems pretty clear that, if anything, it would benefit earnings on the whole and, therefore, bring the current multiple down.

The S&P 500 is undoubtedly trading at the high end of historical valuations, but it’s a stretch to call it a bubble at this point. While many large companies have enjoyed outstanding performances over the last years, many pockets of the markets have not. The S&P 500 might not perfectly represent what’s going on under the hood. There are undoubtedly companies that seem to be in bubble territory (those trading at 20x+ sales), but that doesn’t mean the market as a whole is in a bubble. The P/E ratio of the largest 10 companies in 2000 (dotcom bubble) was significantly above what we see today despite this misleading chart going viral on Twitter:

I don’t know who gathered the data for this chart, but P/E multiples during the dotcom era were significantly above what we see today:

Everyone will cater the data to their beliefs; it’s human nature. I don’t think we are in a bubble, but I also don’t believe indices will return 15%+ forever. We’ll probably see some sort of relaxation period going forward. This scenario and that of a bubble are markedly different. Another thing that should tame the fears of a bubble is that many people believe that we are in a bubble and in for a rough landing. Rarely do the markets do what everyone expects them to.

The industry map was pretty much what you can expect during a week when markets were up more than 5%:

The fear and greed index went back to greed territory, an improvement that makes sense considering that a good deal of uncertainty is behind us now:

The rest of the content is reserved for paid subscribers.

Have a great weekend!