Amazon’s Q3 2024

Where’s the ceiling?

Hi reader,

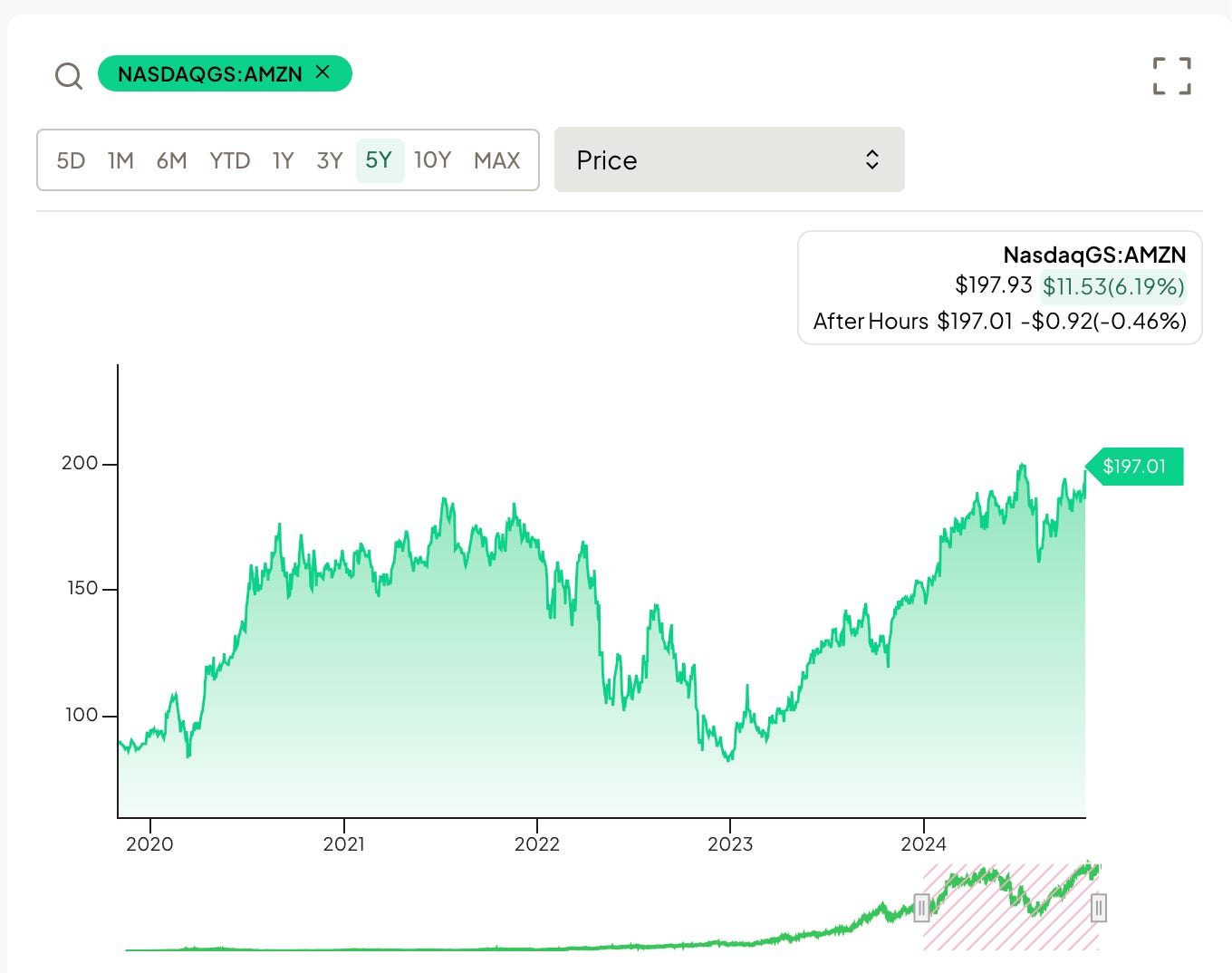

Amazon reported outstanding earnings last week; this time, the market liked them. The stock soared more than 6% the following day and is now hovering around all-time highs, but $200 is proving to be a “psychological” barrier for the market:

The summary table and some comments

This quarter again demonstrated the company's operating leverage. Revenue grew at a good pace across all areas but was clearly outpaced by profit growth:

Some brief comments on these numbers…

Amazon’s top line keeps surprising me. The company grew by double digits for the sixth consecutive quarter at a $620 billion revenue run rate. Management guided for revenue growth between 7% and 11% next quarter, which might become the seventh consecutive quarter of double-digit revenue growth. I think growth across Mega Cap Tech is something people typically take for granted, but they shouldn’t. A quick screener helps us see that Amazon is the only company of its size growing at this pace. Only four companies are growing their revenue double-digits at a +$300 billion revenue run rate: Alphabet, Amazon, Berkshire, and McKesson Corporation:

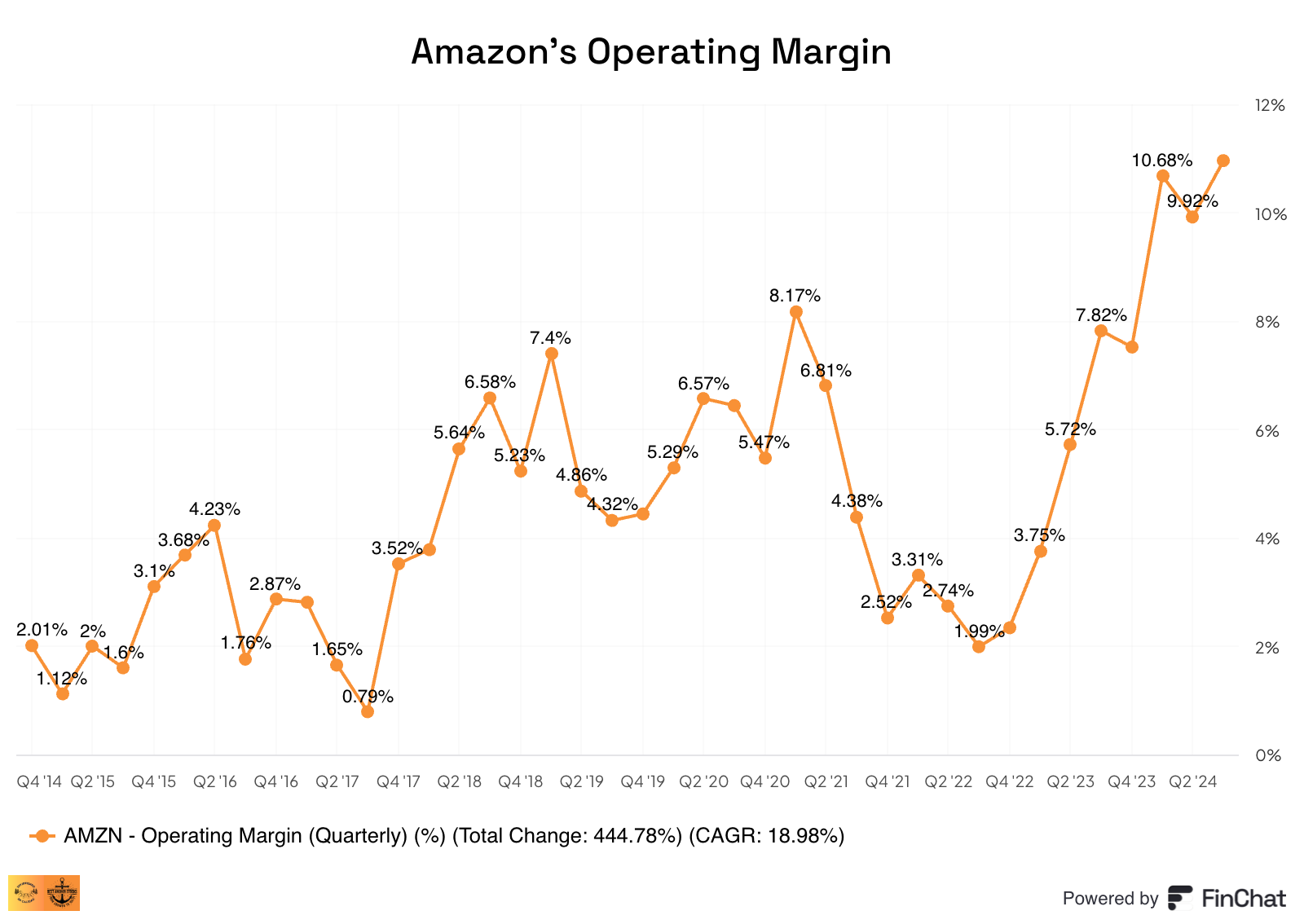

The highlight of Amazon’s quarter was profitability (again). The market has been behind the curve on the profitability front for quite a while, and in the meantime, Amazon has demonstrated that its operating leverage is outstanding. Its operating margin has steadily trended in the right direction and set a new quarterly record at almost 11% this quarter. Since reaching a bottom in Q3 2022, Amazon’s operating margin has expanded by 900 basis points. Andy Jassy once said that the margin reached during the pandemic should not be a ceiling for Amazon, and time has proven him right:

Cash flows grew slower than accounting profits, caused by significantly lower cash conversion. Lower cash conversion can be attributed to movements in working capital and an accounting change management made in 2024 related to the useful life of AWS servers (this also makes accounting margin comparisons a tad misleading). Cash flows can be lumpy from quarter to quarter, but the LTM (Last Twelve Months) figure shows that Amazon has turned on the cash flow machine. LTM Operating Cash Flow has increased 57% to $112 billion, an 18% OCF margin.

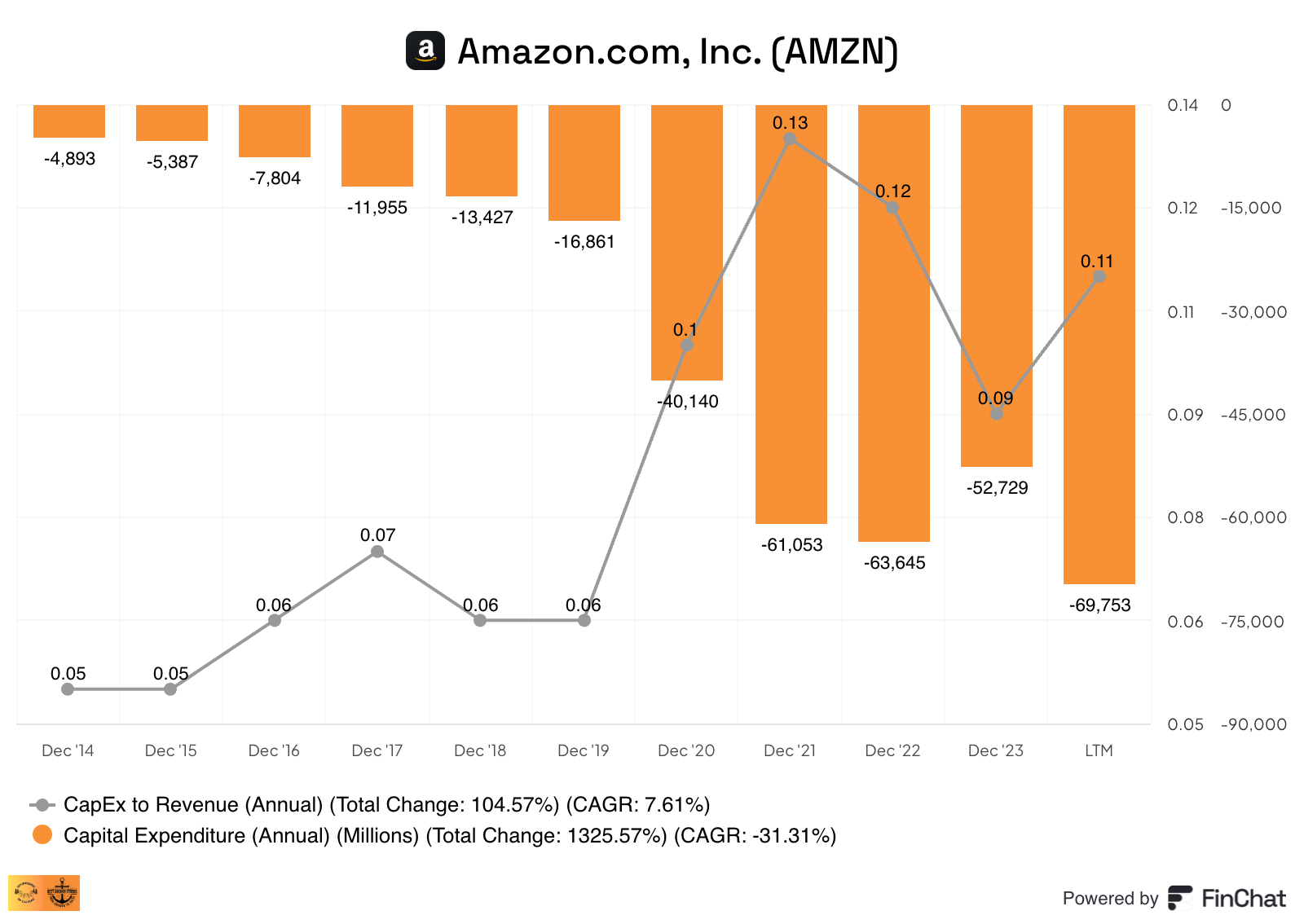

Operating cash flow is not the end of the story for Amazon, though. The company continued investing significantly into Capex, so free cash flow decreased this quarter. Again, it’s best to look at the LTM figure, which keeps going in the right direction. Amazon continues investing into capacity, but it now does so while generating positive free cash flow:

Last quarter, I wrote down the following… “I don’t know the exact number, but I don’t think it’s crazy to believe that Amazon could be generating north of $100 billion in free cash flow in a normalized state (that would be a 17% FCF margin).” While I still believe this is possible, I think it’ll take some time to play out, judging by management’s commentary on Capex investments (I’ll discuss this in more detail later).

It’s tough to find a weak spot across the different segments. North America, International, and AWS kept growing at a good pace. There were two main highlights. The first one was profitability in international, which is getting pretty close to North America’s margins despite being much more immature. The second one was AWS profitability. AWS’s operating margin is getting close to 40%, although management did mention that 200 bps of margin came directly from the accounting change they made some quarters ago that extended the useful life of the servers. Even after correcting for this accounting change, AWS's operating margin expanded by 580 bps year over year. This accounting change is also one of the reasons behind the worsening cash conversion (accounting profits went up, whereas cash profits did not due to depreciation being a non-cash charge).

Another highlight can be found in SBC (Stock-based compensation). Many Big Tech companies have been criticized for letting SBC run loose, but they seem to be focusing much more on this expense. First, Amazon has gone back to a policy of work at the office, claiming that those who do not want to comply can leave the company. Amazon seems to be using this tactic to shave off headcount without incurring significant severance costs. Secondly, we can already see it in the numbers: Amazon’s SBC expense as a percentage of revenue has significantly moderated since peaking last year and is trending in the right direction (albeit it still remains high):

Guidance was also a highlight, in my opinion. Many people will focus on the revenue miss, but for me, the highlight is operating income. Amazon’s management tends to be very conservative with its profitability expectations and is guiding for operating income growth of 40% at the midpoint. For context, this quarter's operating income guidance was $12.3 billion at the midpoint, but the reported number was $17.4 billion, 40% above the midpoint of the guidance. The real “tough” comps will come next year when the change in the useful life of AWS servers is behind us. We should see operating leverage moderate significantly from then on.

All in all, it was another outstanding quarter for Amazon both on the growth side and profitability-wise. The company continued to outperform profitability expectations, and management mentioned they still see ample opportunities to continue making the eCommerce network more efficient, which bodes well for continued margin expansion.

Qualitative highlights and lowlights

Retail operations

Management mentioned some kind of downtrading across retail: “Unit growth continues to be strong and outpaced even our revenue growth.” This is something we’ve seen across many retailers so it’s not surprising and demonstrates that the Amazon customer continues to be engaged with Amazon. This is also a result of Amazon increasingly being used for everyday essentials by its customers. Management believes this is something that Amazon can afford, unlike many others: “It’s easy to lower prices, but it’s much harder to be able to afford to lower prices.” Amazon’s ability to go down the price spectrum has come from improvements in cost to serve, which are expected to continue going forward.

There are still margin expansion opportunities for outbound operations and inbound operations: “We’re in the process of significantly changing the way we inbound items into our fulfillment network.” Andy Jassy mentioned when he got the CEO job that he was re-envisioning every part of Amazon’s supply chain, and he seems pretty serious about it.

Robotics was also a pleasant highlight. The company rolled out a modern fulfillment center design in Louisiana with its most advanced robotics innovations. The results were outstanding: “This new design reduces fulfillment processing time by up to 25%, increases the number of items we can offer for same day or next day delivery, and is expected to drive a 25% improvement in our cost to serve during peak within this next generation facility.” As this design gets rolled out to the entire supply chain, we should see pretty outstanding efficiency gains (albeit it will take some time).

Amazon Web Services

AI is accelerating AWS’ growth: “It’s much harder to be successful and competitive in generative AI if your data is not in the cloud.” Amazon’s AI business continued growing at triple digits year over year at a multibillion-dollar run rate, and interestingly… “Is growing more than 3 times faster at this stage of its evolution as AWS itself grew.” This is obviously great, but I would attribute some of this faster growth to the infrastructure being more prepared today than when AWS was starting out. In short, any cloud innovation can be rolled out much faster today than 10 years ago.

Management mentioned that demand continued to outpace supply. This will lead to increased investment in capacity going forward, which will obviously lead to higher Capex and reduced Free Cash Flow (more on this in the next section).

More Capex: should investors be worried?

Capex has been the buzzword at Amazon for quite some time, and deservedly so. During the pandemic, the company undertook a massive capacity investment plan to service the increasing demand for eCommerce and AWS. This, together with an inefficient supply chain, led to depressed free cash flow. The company has since scaled back investments in the eCommerce network and has made it more efficient, but Capex remains high due to accelerated investments in AWS now to service AI demand. Management expects to invest around $75 billion in Capex this year and more than that in 2025…

We expect to spend approximately $75 billion in Capex in 2024. The majority of the spend is to support the growing need for technology infrastructure. This primarily related to AWS as we invest to support demand for our AI services. I suspect we’ll spend more than that in 2025.

Amazon’s Free Cash Flow has improved markedly over the past two years, but this free cash flow generation has come more from improvements in efficiency and growth rather than lower Capex. While 2023 did enjoy significant Capex leverage, we should consider that to be over now that generative AI is in play:

Amazon might invest almost $90 billion next year in Capex (making this number up), a sum very few companies can afford. This is one of Amazon’s advantages to fence off potential competitors: capital intensity. It’s not a coincidence that management searches for capital-intensive businesses where the economics are attractive, as not many people can compete in these.

Management believes these investments will play out well over the long term despite investor concerns:

We can drive enough operating income and free cash flow to make this a very successful return on invested capital business. And we expect the same thing will happen here with generative AI.

I honestly believe that what Amazon is experiencing here is the holy grail for long-term shareholders. The company is still finding avenues to reinvest significant sums into the business, but it’s now doing so while generating positive free cash flow. As a company gets large, one of the most challenging things is finding reinvestment opportunities, but it still seems to be day 1 at Amazon. Of course, what matters is the returns these investments will achieve, and this is where trust in the management team should come in. I trust management’s capital allocation decisions. Many would prefer a capital returns program to see the stock pop over the short term, but I don’t think that should be a long-term investor’s wish:

And I think our customers, the business and our shareholders will feel good about this long term that we’re aggressively pursuing it. As the market matures over time, they’re going to be very healthy margins here in the generative AI space.

If generative AI would not exist today, we would most likely see Amazon generate significant amounts of cash and institute a capital returns program. However, this new Capex cycle portrays one of the company’s main advantages: optionality.

Andy Jassy is demonstrating to be a great CEO (unpopular opinion?)

Many investors are criticizing Andy Jassy because Amazon’s stock has significantly lagged behind the indices and its Mega Cap tech peers since he got the CEO job (2021). While this is evidently true if we look at the graph below, I don’t think it should be what investors should be focused on right now:

Andy Jassy’s execution has been exceptional both in AWS (where many people expected him to succeed) and the retail operations (where many people expected him to fail). He inherited a business swamped with inefficiencies undergoing a massive capacity expansion plan, but he has managed to turn the ship. Of course, the impact of his changes has not been immediate as large ships like this one take some time to move, but the operating margin is already at an all-time high (albeit aided by an accounting change) and the company is growing double digits. Besides all of these feats, it still seems early in the company’s margin expansion story.

Has the stock price lagged the indices and its peers? Yes. Does this mean that Andy Jassy is a bad CEO? Not at all. Execution has been good, and it’s only a matter of time before the market truly recognizes it. A stock can do poorly over 2-3 years (or even more) without this meaning the CEO is doing a bad job because timing matters. In the words of Jeff Bezos…

Those quarterly results were fully baked three years ago. So today I'm working on a quarter that will happen in 2020, not next quarter. Next quarter is done already and it's probably been done for a couple years.

Take, for example, Microsoft. Everyone praises Satya Nadella (and rightly so) for what he has done. These same people tend to criticize how terrible Steve Ballmer was as a CEO, and while he was no Satya Nadella, the company did okay during his tenure, achieving a 9% EPS CAGR. The stock did terribly, though, because Ballmer inherited a stock trading at 70x earnings and with high expectations baked in. Something similar (albeit not to the same extent) likely happened to Andy Jassy. Andy Jassy inherited a business at pandemic heights that had overbuilt capacity to protect its competitive position. This came at the expense of margins and efficiency, which was a short-term pain that is already behind the company. The only thing we can judge him on over the past 3 years are company numbers, and those have improved markedly.

The cheapest among Big Tech?

One of the questions many people are trying to answer is…is Amazon the cheapest among the Big Tech companies? While I don’t have the answer to this question because I have not studied all the big tech companies, I want to quickly revisit Amazon’s valuation. Amazon is currently trading at a trailing EV/EBIT of 34x and a forward EV/EBIT of 29x:

The company has seen its multiple contract pretty significantly since 2023, (despite the higher stock price) because it started to show its true operating leverage by making its operations more efficient. Still, we must not forget that a portion of this multiple contraction has also come from the accounting change the company made to the useful life of its servers (so we are not really comparing apples to apples). The operating cash flow multiple (which bypasses this accounting change) has also contracted, but not to the same extent…

Amazon’s OCF multiple has contracted from 26.5x in June 2023 to 19x today, a 30% contraction. On the other hand, the company’s EBIT multiple has contracted from 99x in June 2023 to 36x today, a 60% multiple contraction. There’s no denying that Amazon’s multiples have contracted thanks to better fundamental performance, but not all of the contraction can be attributed to this.

I don’t believe Amazon is particularly expensive here (paid subscribers know my purchase price), considering the next reinvestment cycle is already upon us. The stock is trading under 29x next year’s operating earnings despite margin expansion and growth being far from over.

In the meantime, keep growing!