The Things the Market Might Be Worried About (NOTW#82)

(+ What I Am Worried About)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of subscribers today:

Both indices were down this week, continuing the relative softness exhibited late last week. I discuss what the market might be worried about and what I am a bit worried about in the brief market commentary.

There was also plenty of company-specific news this week (and most of them pretty relevant for their long-term investment theses).

Without further ado, let’s get on with it.

Articles of the week

I published three articles this week. The first one was Shift4’s earnings digest.

Shift4: Was it THAT bad?

You can read this article for free. Shift4 is a company I have profiled at Best Anchor Stocks. The full in-depth report is reserved for paid subscribers. You can read it here.

The company reported an okay quarter although communication during the quarter wasn’t (in my view) the best. This said, communication improved significantly in a recent conference and there was some great news for shareholders (more about this in the company-specific news section).

The second article of the week was Stevanato’s earnings digest.

More than a GLP-1 company

You can read this article for free. Stevanato Group is a company I have profiled at Best Anchor Stocks.

The company reported a stellar quarter, but it required some context to understand why it was really stellar (I provide this in the article, which is free to read). The stock popped almost 20% during the following day but pretty much gave much of this run in the following days (great news for those willing to add). Stevanato remains my strongest conviction.

The third and last article of the week was an article on Sabre (SABR).

Sabre (SABR): To be Or not To be

You might have read somewhere that Constellation Software has done something unusual: the company has built a stake in a publicly-traded software company. Many people argued that software valuations were still not low enough for Constellation to step into public markets post-SaaSmageddon, and while this is definitely true if we consider what CSI typically pays for businesses, the company seems to have found one:

Sabre is Constellation Software’s latest (and unusual) investment. I go over what the company does and why it might fit the Constellation story. I believe some people think that Constellation has to significantly turn the business around operationally, but I don’t think that is what Constellation needs to do to do well from here.

Without further ado, let’s see what the markets did this week.

Market Overview

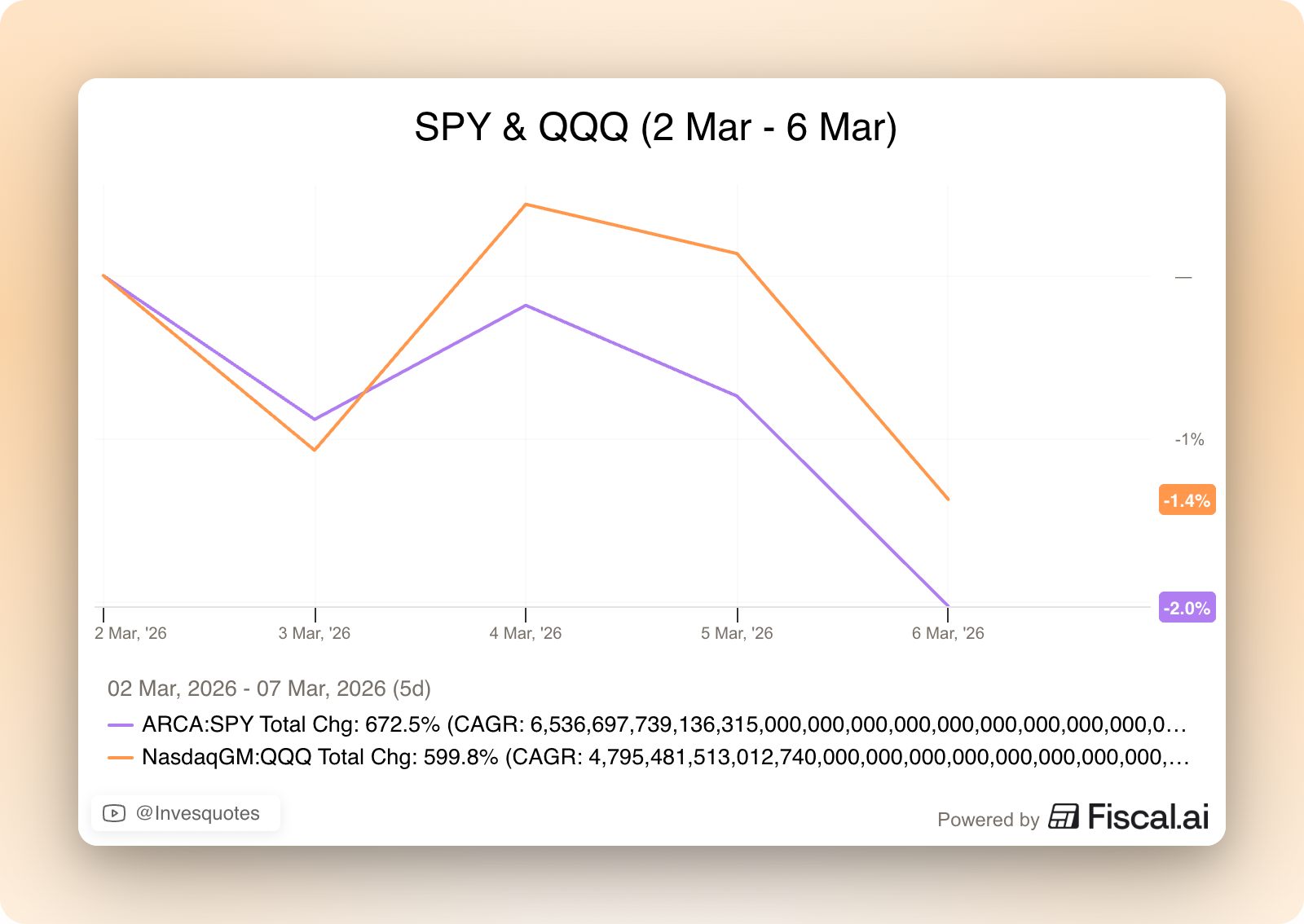

It was yet another entertaining week in financial markets (just in case you were not already entertained). Both indices suffered a “significant” drop this week:

Many reasons have tried to point out why markets have been weak, and all of them are related in some sort of way. I believe the consensus “bear” narrative is that the war with Iran will go on for longer than many expect, which will prolong the closing of the Strait of Hormuz, which will in turn drive oil prices higher, which will in turn feed into accelerating inflation through higher energy prices. All of this is happening while job numbers are disappointing, which is making some people worry about stagflation. Stagflation is one of the trickiest situations for central bankers because they don’t have much room to manoeuvre. The reason is that, if they lower interest rates to stimulate the economy, inflation might go up from an already elevated level. If they raise interest rates to fight inflation, they might end up worsening the economy even more. I.e., no bueno.

I have no clue whether stagflation will play out or not, but I’ll just say that the word stagflation has been around since 2022 and it’s already 2026 and we (or better said, the US) have not suffered from it. There are so many variables that can potentially play into macroeconomic scenarios that I believe that it’s a fool’s game to try to predict it. You might be right from time to time, but you’ll probably have lost significant money in the meantime. Now, this said, there are several things that do worry me personally.

The first one is positioning. I don’t know if the X algo is playing tricks on me or not but sentiment in down days seems to be terrible despite indices being 5% off ATHs. This makes me think that a lot of people are not prepared for a significant drawdown despite it not being an unusual scenario. This is something I have shared before, but the probability of the index suffering a 10% drawdown in any given year is higher than 50% (i.e., much more habitual than people believe). The “super bullish” positioning and the amount of leverage there seems to be in the market makes me think that, if we go into a significant drawdown, things can spiral out of control pretty fast (in reality, it’s always this way!). We’ve seen this play out in certain industries like software this year.

The second thing that worries me (which might be just a bump along the road) is that the AI infra thesis might be starting to show some cracks. OpenAI and Oracle reportedly canceled an existing agreement to expand a data center in Texas. I think it’s a bit too much to say that the AI-infra thesis is showing cracks because this might be an OpenAI-specific decision, but I do think that the market is growing concerned about this topic. I mean, even though the economy is doing well, it is to a great extent being supported by the AI-buildout. This means that if the AI-buildout falters, the economy might be in for a rough surprise (who knows). The neoclouds did not react well to this OpenAI/Oracle announcement. In my opinion, this is due because many of them are seen as the “flexible” data center supply for the hyperscalers. If the AI-buildout falters, these companies are likely going to be the first to suffer from it…

The one thing that bulls will always have on their side is TACO (Trump Always Chickens Out). I believe Trump has demonstrated time and time again during his mandate that he cares deeply about markets. This means that there’s an additional line of defense against drawdowns than in prior administrations. Is this a sign of a healthy market? Probably not, but it is what it is. All the above said, I am humble enough to know I have no clue what will happen from now on; I’m just making an educated guess.

The industry map was pretty much red this week, with some pockets of green. Interestingly software is doing really well just as the market becomes more cautious about AI. Coincidence? I don’t think so, but we’ll have to ask the algos whether this is sustainable or not:

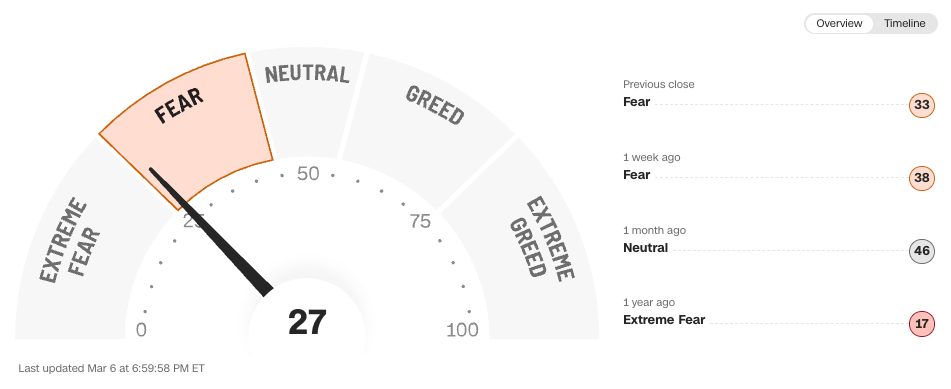

The fear and greed index worsened considerably and is now deep in fear territory:

My buys and sells this week

This week, I partly sold one position after a significant run, added to several existing positions, and started an entirely new position: