Sabre (SABR): To be Or not To be

You might have read somewhere that Constellation Software has done something unusual: the company has built a stake in a publicly-traded software company. Many people argued that software valuations were still not low enough for Constellation to step into public markets post-SaaSmageddon, and while this is definitely true if we consider what CSI typically pays for businesses, the company seems to have found one: Sabre (SABR). The stock price chart is exactly the one you’d expect if Constellation is stepping in:

Nobody ever asked themselves the following…

What does Constellation have in common with LVMH?

…but the manner in which CSI has built its 12.7% stake in Sabre is strikingly similar to how Bernard Arnault tried to acquire Hermès a long time ago. Constellation acquired a direct ownership stake of 4.7% in Sabre throughout 2025. To avoid having to disclose a 5%+ position, CSI built an additional 5%+ stake through derivatives. This meant that Sabre’s management was ultimately not aware that Constellation had built a 10%+ position. Then, in January 2026, Constellation disclosed its entire stake to Sabre’s management and requested two board seats. Sabre’s management was initially hesitant, did not comply with Constellation’s demands, and even enacted a poison-pill at 15% ownership (the poison pill would ultimately dilute CSI’s stake should it go above 15%). Both companies ended up reaching an agreement in early March. Constellation has been granted one board seat (to be occupied by Damian Mckay, CEO of Vela Software) and the ability to acquire up to 15% of Sabre, with Sabre eliminating the poison pill.

Needless to say (and if you are a CSI shareholder this shouldn’t come as a surprise) Sabre is not the perfect company (nothing close to it actually). Constellation, however, doesn’t look for “perfect,” Constellation looks for a good IRR. This is ultimately what Vela Software believes it can get with Sabre (let’s not forget that their bonus is on the line when making these decisions). Just for context (before explaining what Sabre does), Sabre’s main problem can be encapsulated in one word: leverage. Sabre has around $3.7 billion in outstanding debt (at a significant interest rate), an interest coverage ratio below 1x, and interest pretty much makes up 100% of Operating Cash Flow. Yikes.

What Sabre does

If you invest in European equities you might be familiar with Amadeus, historically known as one of Europe’s highest-quality companies/compounders. Well, Sabre is Amadeus, but worse. Both companies do primarily two things.

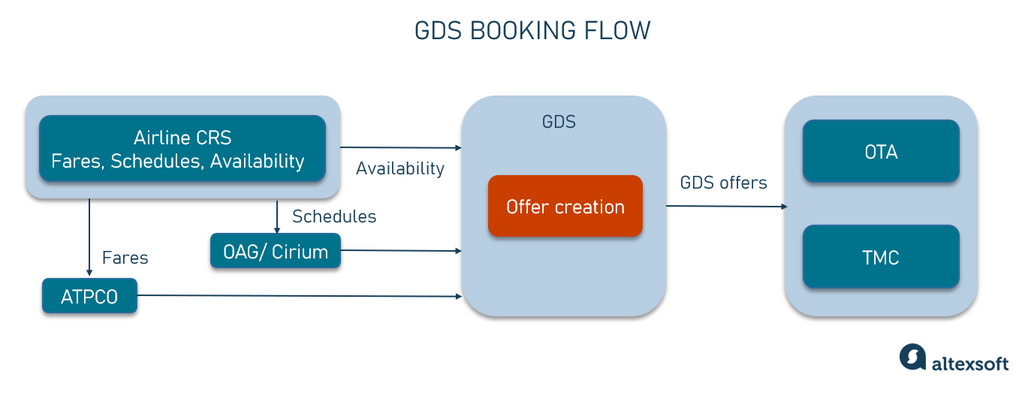

First, Sabre and Amadeus act as the distribution layer between the travel industry (airlines, lodging, car rentals…) and the travel agencies (both OTAs and physical). This is known as GDS (Global Distribution System). What these companies ultimately do is aggregate supply from many different sources (mostly known for aggregating airline ticketing) to make it searchable and bookable for agencies. Instead of having to go to each airline, a travel agency goes to a GDS to get a transversal view of their options.

The revenue model is pretty straightforward: these businesses take a transaction fee for every booking made:

The GDS business model is not free of risks. Airlines are trying to disintermediate GDS, and they are getting help from IATA. NDC stands for New Distribution Capability and it’s an IATA-promoted standard that enables airlines to directly communicate with OTAs. Airlines, on their side, are also trying to drive more direct bookings. The portion of the ticket paid to a GDS doesn’t seem significant, BUT airlines have thin margins and therefore every basis point saved counts.

The way airlines are trying to do this is by taking certain fares out of GDS and only making them available through direct booking and NDC. The long-term trend does seem to favor disintermediation, but short-term disruption doesn’t seem likely. For two reasons…

The GDSs of the world are connecting to airlines through NDC and in some cases are gaining exclusive NDC access (therefore driving differentiation).

This is from Sabre’s February call:

Finally, we extended our leadership position in NDC by adding 15 live integrations during the year, bringing our total to 42, and we are seeing adoption ramp. We exited 2025 with NDC representing approximately 4% of total air distribution bookings, and we expect our rate of NDC bookings to accelerate throughout 2026.

Completely ignoring the GDSs of the world can lead to lost sales. American Airlines pulled 40% of fares from GDS in 2023 but reversed the decision when it lost corporate travel revenue

Interestingly, a Columbia Business School investment research note tried to mathematically demonstrate that disintermediating GDS does not make economic sense:

Mathematically disproving direct connect to TMCs: Each TMC agent earns ~$1.50 per booking from SABR and can book 4 tickets / hour, totaling $6/hour of fees earned from SABR. Through direct connect, the productivity of an agent drops to 1 ticket an hour (15 min x 4) which means the airline will have to pay TMCs $6/booking. Adding 3 additional agents at an hourly wage of $10 each to keep up the pace of 4 tickets an hour implies a break‐even booking fee of $64/hour, an amount that is 16x more than ~$4/booking fee that airlines currently pay to Sabre. This is before taking into consideration the amount of technology costs incurred for direct connections between TMCs and airlines to be possible.

I must note that the above research paper was a “long SABR” thesis at $22 and the stock is trading today at $1.7 (so do with it what you will). The argument of losing corporate travel somewhat makes sense. If a corporate travel manager has to oversee tens or hundreds of programs then he most likely needs an aggregation layer, which is why GDS remains relevant despite the ability to connect directly to the airlines. All this said, the GDS thesis does have some question marks. I’ll later provide an example of why potential synergies with Vela Software might somewhat “eliminate” said fears.

Amadeus and Sabre also offer a VMS platform for airlines. This VMS is typically known as a Passenger Service System or PSS, and it’s basically the software in which an airline runs. Sabre offers SabreSonic, which is bleeding share to Amadeus’ IT solution. The company recently launched SabreMosaic, an AI native solution. It’s still early days, but there have been some early customer wins:

Why Sabre loses share here is pretty straightforward: in addition to Sabre probably having an inferior product, Amadeus uses its GDS dominance to win IT contracts. Just so you grasp a bit of the competitive positioning here…Sabre has a 35% market share in GDS compared to Amadeus’ 40%+. The market is oligopolistic and the three largest players control around 97% of bookings. Interestingly, the battlefield is more balanced in the Asia-Pacific region. This is relevant (more than it seems at first glance) because the APAC region is expected to be the main driver in passenger volume growth going forward. Despite GDS being somewhat challenged as airlines push direct distribution, Sabre’s GDS business grew in 2025, driven by hotel accommodations (which remains small compared to airline ticketing):

Sabre sold its Hospitality Solutions segment in 2025 for $1 billion to pay down debt but critically retained its hotel B2B distribution business, remaining the only global marketplace with Chinese lodging availability (the company acquired Abacus in 2015, Asia-Pacific’s leading GDS).

Just to wrap up this section, I think it’s important to understand that Sabre was already undergoing a financial turnaround before Constellation’s arrival. Several things point to this being the case…

A new management team came in 2022-2023: both the CEO and the CFO came to the company in 2022/2023 and have deep travel experience. They are compensated based on adjusted EBITDA and, to a lesser extent, Free Cash Flow. Both have made open market purchases at significantly higher prices than today’s stock price (not saying this is necessarily a signal)

The numbers are improving and the company is launching new products. Margins have expanded over the past few years and importantly, debt has been pushed further out (refinancing wasn’t cheap, though)

The above doesn’t automatically make Sabre a riskless investment (leverage is still very high and Free Cash Flow generation is poor), but it does portray that current management is swimming in the right direction. FY 2026 doesn’t paint a rosy picture in terms of FCF, but both revenue and margins are expected to continue their improvement:

Now, when you have $3.7 billion in net debt on a $600 million market cap and no Free Cash Flow, you know that the market is not looking at growth, it’s looking at survival (i.e., the balance sheet). Does Sabre trade at 0.2x revenue because the market believes it’s a terrible business? No, it trades there because the market believes that Sabre’s business is being eclipsed by financial problems, which is undoubtedly true.

How Sabre fits into Constellation

The concept of an-okay-business-going-through-a-rough-patch fits directly into Constellation’s playbook. This is, ultimately, the type of situation that Constellation typically buys. As I shared earlier, CSI’s goal is to generate a good IRR, not to hold excellent businesses. I suspect that people who are criticising Constellation for buying a troubled business are not really accustomed to the company’s typical purchases (ehem, Allscripts). We can look at Sabre’s fit within Constellation through two angles:

Constellation’s intentions and the potential outcomes (investment angle)

How Sabre fits within Vela Software (operational angle)

Let’s go in order.