More than a GLP-1 company

Stevanato's Q4 2025

You can read this article for free. Stevanato Group is a company I have profiled at Best Anchor Stocks.

If you like what you read, consider becoming a paid subscriber. A paid subscription gives you access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Enjoy!

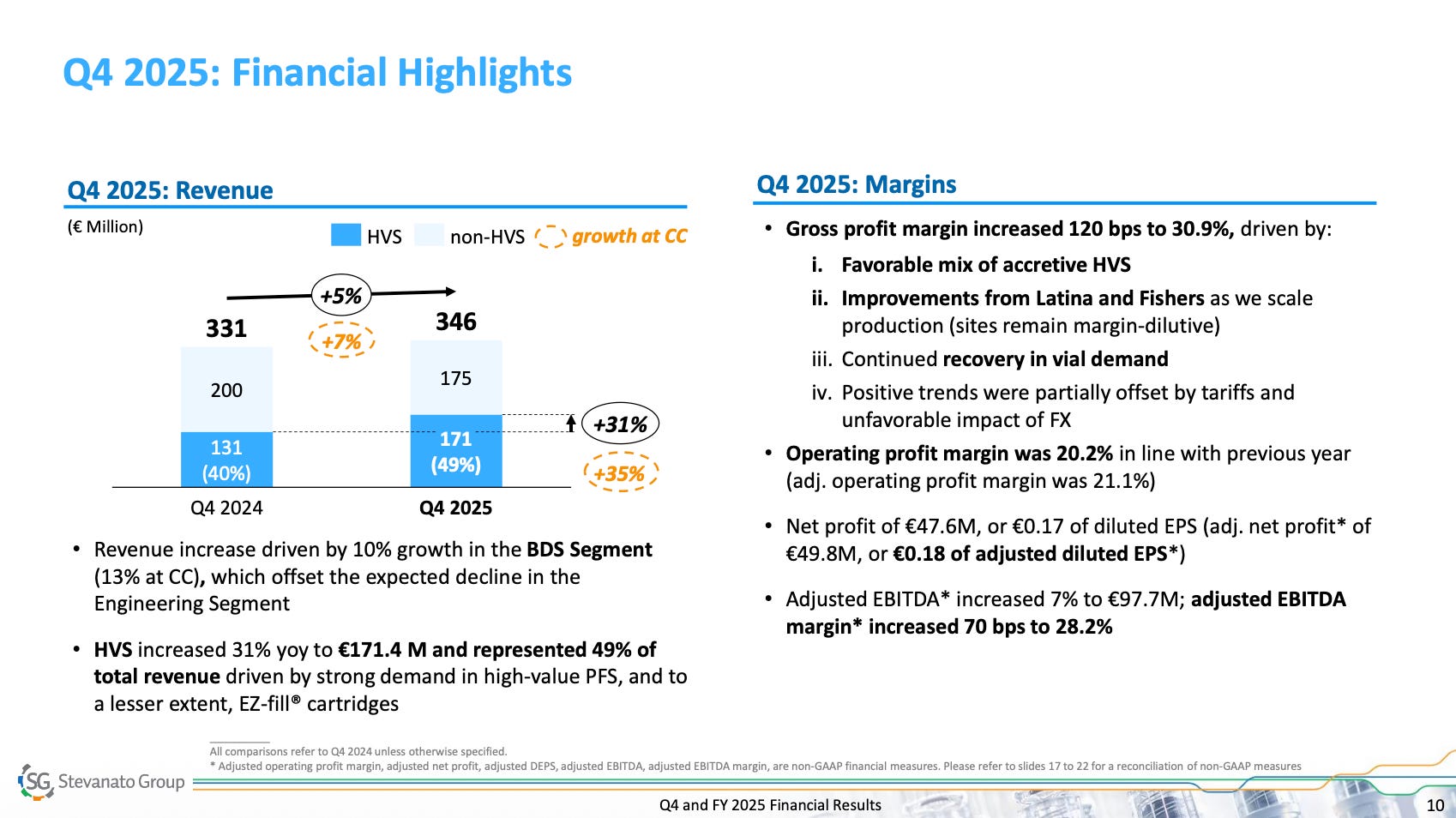

Stevanato Group reported very strong Q4 earnings today. And by very strong…I mean that Q4 significantly beat consensus estimates. And by significantly I mean…

Reported revenue growth was +5% compared to consensus of +0.8%

Organic revenue growth was +7% compared to consensus of LSD (low single digits)

This information should be useful to contextualize 2026 guidance (among other things). Overall, this is how Stevanato performed in Q4: good revenue growth with expanding margins driven by strong HVS growth (like clockwork):

Growth was driven by BDS (+13% in CC) with engineering remaining weak (again). Within BDS, HVS was the main growth driver (again!) with 31% YoY growth. Management, however, took investors by surprise (myself included) by breaking out GLP-1 exposure:

Revenue from GLP1s accounted for approx. 19% to 20% of total Company revenue, growing 50%+ compared to 2024.

This disclosure is great, but it probably includes diabetes and obesity GLP-1 exposure. This is what I wrote in my article ‘The Great Oral GLP-1 Scare’:

Stevanato is the worldwide leader in cartridges (the most common administration form of GLP-1s in diabetes), so even if we are conservative and assume that 80% of biologics revenue is GLP-1 (the rest being other biologics) and that 30% of this revenue is obesity-related (JP Morgan estimates that by 2030 the split of the GLP-1 market between obesity and diabetes will be 50/50), then we get to a “finer” estimate of obesity GLP-1 exposure: 34% * 80% * 30% = 8%.

Even though my obesity-related estimate (8%) was probably too low, I must say that my GLP-1 estimate was definitely too high at 27%. Good news is that Stevanato is less of a GLP-1 company than I previously envisioned, which should make it less exposed to the oral GLP-1 narrative than I thought. The ideal scenario would’ve been to have the disclosure between obesity/diabetes GLP-1s, but the more I think about it, the more I believe that Stevanato is unlikely to have that level of detail.

GLP-1 revenue grew 50% (!) in 2025 and despite the market being worried that the pill would result in a complete drop-off in terms of GLP-1 revenue, management confirmed that guidance includes mid-teens growth for GLP-1 revenue in 2026. This number is important for two reasons. First, it allows us to triangulate how much the non-GLP-1 business is expected to grow in 2026. If GLP-1 revenue is 20% of 2025 total company revenue, that means that it’ll add 340 basis points to Stevanato’s consolidated organic growth (20%*17%). Knowing that Stevanato guided for 9% organic growth (midpoint) for 2026, we can infer that the remaining 80% of the company is expected to grow 7% in 2026. This is despite the expected revenue decrease (MSD to HSD) of the engineering segment. Conclusion? Stevanato is much more than a GLP-1 company.

Management also gave an interesting data point to portray that the future might even be less about GLP-1s:

In 2025, +40% in the number of customers ordering High-Value PFS (pre-filled syringes) for non-GLP biologic applications.

The non-GLP1 biologics pipeline looks pretty strong but it’s not as immediately accretive as the GLP-1 opportunity. The latter is taking the market by storm whereas the former is still in the early stages of the pipeline when volumes are not extremely significant. Despite Stevanato not being “just” a GLP-1 company and despite the non-GLP1 business already growing at a good pace and expected to accelerate in the future, management still expects that obesity GLP-1s will be a long-lasting tailwind for Stevanato:

We currently expect that GLP one will serve as a meaningful tailwind as patient demand continues to grow in the years to come. With the launch of the Wegovy pill. Patients now have more options for GLP treatments. The general consensus among industry experts and our customers is that injectables are expected to be the preferred format for treatments like obesity, while oral gel pills will enable market expansion and support patients with specific needs.

Engineering remains the “wild card.” The segment is still not doing well but management continues working to stabilize it, and management remains convinced that the medium term opportunity is bright. The Engineering segment’s performance has been a bit frustrating as an investor because, at this pace, it’ll be so small when it turns around that it won’t even matter. All in all and despite the continued weakness in engineering, a great quarter.

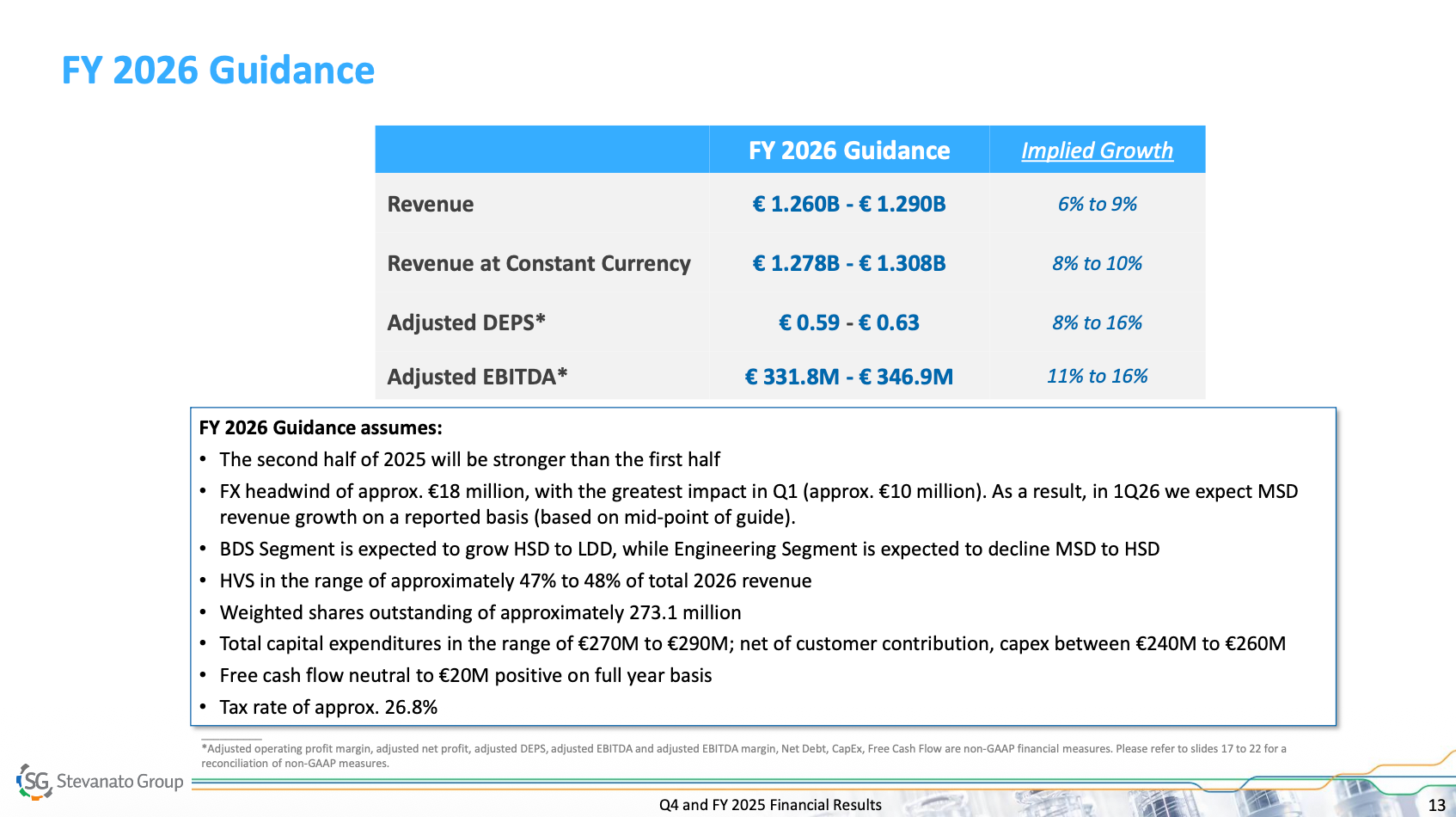

Contextualizing the guide

Stevanato (finally) provided an organic growth guidance for 2026, although that didn’t stop them from also providing a reported revenue growth rate:

Giving organic growth guidance is important for effective communication. Just for context, if Stevanato would’ve provided organic growth guidance last year, management would’ve been able to raise the guide 3 times throughout the year. However, they did not. This said, the reported growth guidance eventually was conservative enough as to absorb a depreciating dollar and tariffs.

Some have pointed out that the guide came in a touch soft compared to consensus. This is true but I believe it requires some context. First, Stevanato massively beat Q4 numbers. If we add the Q4 actual numbers to the 2026 guidance, Stevanato was comfortably ahead of the consensus coming into earnings. The company “indirectly” reported a beat-beat-beat quarter.

Secondly, after several years of being too optimistic and getting wrong-footed with the whole destocking issue, management seems to have convinced itself that it has to provide conservative guidance. Just for context, the company provided 5-8% guidance for FY 2025 in Q4 last year. The end result was 9%. I don’t know if Stevanato will grow ahead of what they’ve disclosed, but there does seem to be a tendency to guide conservatively. This, by the way, is not entirely isolated to Stevanato, as it’s something we are seeing across the management teams of many healthcare companies.

So, even if the guidance fell slightly below expectations, the reality is that it’s probably considerably ahead all things considered.

Fishers, Latina, and future Capex

One thing that surprised me was the 2026 Capex number. I expected it to be considerably lower than it was. Management guided for (before customer contributions) €280 million of Capex at the midpoint. That’s (using the midpoint revenue guidance) a Capex/sales ratio of 21%. Now, several things to consider here.

First, Capex is being built today (and over the past years) to support future revenue growth in HVS. Growth in HVS is pretty strong, so one can’t really claim that Capex is not delivering good growth. Another thing to take into account is that the Capex comes with a significant lag. Stevanato builds the shells, then installs the equipment, validates the production lines, and only then can start ramping up capacity.

If I can give a sort of business angle, in Latina, we have continued the installation of a high-speed line for syringes Nexa, and we are continuing to perform validation to our regional customer, international customers. This year, we’re going to install the first high-speed line for cartridges Ez-fill. The goal is to do the validation this year to start to do commercial revenue at the beginning of 2027.

In Fishers. Right, we continued to perform audits with our big international clients in order to become particular domestic United States. In fact, we have doubled the number of audit validation 2025.

This means that the Capex that is being built today should support strong revenue growth for many years (but not immediately). Management mentioned that 89% of next year’s Capex is growth Capex, implying that around 11% of the €280 million is maintenance Capex (around €30 million).

This means that, even though FCF is expected to remain depressed over the short term, Stevanato’s owner earnings are considerably higher than what we are seeing here. Assuming that Stevanato converts 95% of its Adjusted EBITDA to Operating Cash Flow this would result in 2026 Operating Cash Flow of around €323 million. Subtract maintenance Capex and that’s around €293 million in steady-state Free Cash Flow, or what’s the same…a 6% FCF yield. One could argue that this would be the no-growth Capex, but this would be a bit misleading as well.

With all the Capex that the company has already spent, I’d assume that growth would not suddenly drop to 0% but that the company would continue growing significantly for the coming years as it ramps up existing capacity (i.e., the Capex that it has already spent). This existing capacity would also be higher margin (due to its HVS nature), meaning that earnings could potentially continue growing LDD to mid-teens for a while without needing to invest in much additional capacity.

The ramp-up is ongoing at both plants (Fishers and Latina), but these are still dilutive to consolidated gross margins (primarily led by Fishers):

We see quarter after quarter better financial performances. The operational performance…we are growing quantities and better leverage our fixed expenses. We are very well positioned in Latina where we are getting close to our average gross profit margin. Fishers. We are a little bit behind, but we see steady improvement.

Besides being important for growth and margins, Fishers also carries a strategic importance in a “de-globalized” world:

The plans of Fishers played an important role when we decided in 2020 And we started to develop these plans in 2021. It was really the purpose to build a campus that was going to mirror exactly the same capability that we have in Europe, in particular, for Ez-Fill technology with a different range of syringes or vials to fillers for devices. Today, what we see is that many clients are re-addressing their supply chain states, and the fact that we are present in Fishers with this wider capability does play a role in translating what we can really accelerate additional opportunity for customers wanting the US supply chain.

Note that higher than expected Capex doesn’t come out of thin-air. Management argues that cartridge HVS demand has been higher than previously anticipated, which, together with their intent to satisfy customer’s contract manufacturing needs, has resulted in higher Capex:

As we noted on prior calls, recent demand for cartridges has outpaced our prior expectation. And we are expanding our capacity to satisfy demand. We see this. Trend align with the introduction of new pen injector formats with various treatment plans, as well as the expected growth of biosimilars, especially in APAC.

All in all, good earnings for Stevanato that disprove (again) the oral GLP-1 narrative. In all fairness, this narrative will only be disproven over the mid to long term, but it got postponed for an additional year not only through good GLP-1 growth, but by the fact that more than 60% of the company’s growth guidance this year will be satisfied by the non-GLP-1 business.

Have a great day,

Leandro

Good summary. Price action shows this thing is an unbelievable HF knife fight. Numbers notwithstanding the GLP1 fear prolly sits with the name for a while. And tbf their answer on the 30% market share section was uninspiring. In any event the growth algorithm looks very strong right now and the company is really cheap as the capex rolls off

Stevanato is probably too dependent on a few customers, isn't it?