Shift4: Was it THAT bad?

Q4 earnings digest

You can read this article for free. Shift4 is a company I have profiled at Best Anchor Stocks. The full in-depth report is reserved for paid subscribers. You can read it here.

If you like what you read, consider becoming a paid subscriber. A paid subscription gives you access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Enjoy!

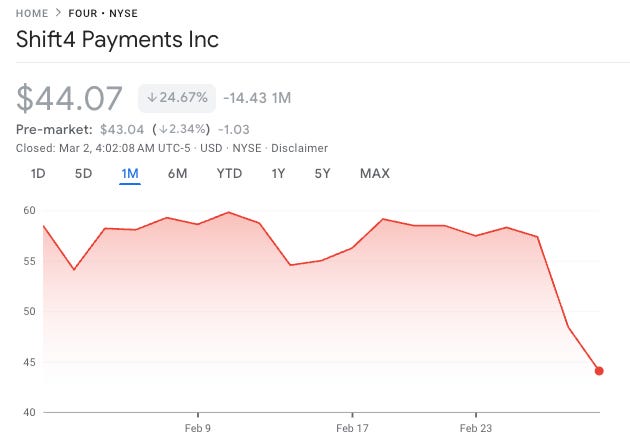

Shift4 reported earnings last week and…let’s just say the market did not like them much. The stock dropped double digits the day of the report and dropped an additional 8% the following day (why not?). The result? A stock that is today trading at $44 when it was trading close to $58 before reporting earnings barely a few days ago:

It doesn’t take a genius to guess that earnings were not outstanding, but were they this bad? I believe a lot of people got caught in thinking they were just purely based on the market’s reaction. When a stock drops 18% after reporting earnings, it’s natural to think that these were terrible (and most of the time we might be even right). What’s pretty amazing is how one can guess what a stock is doing after reporting earnings just by taking a look at X. It’s pretty simple, on X:

If the stock is down = bad earnings

If the stock is up = good earnings

The reality is that the numbers are the same no matter if the stock is up or down.

Let’s dig deeper.

Shift4’s quarter

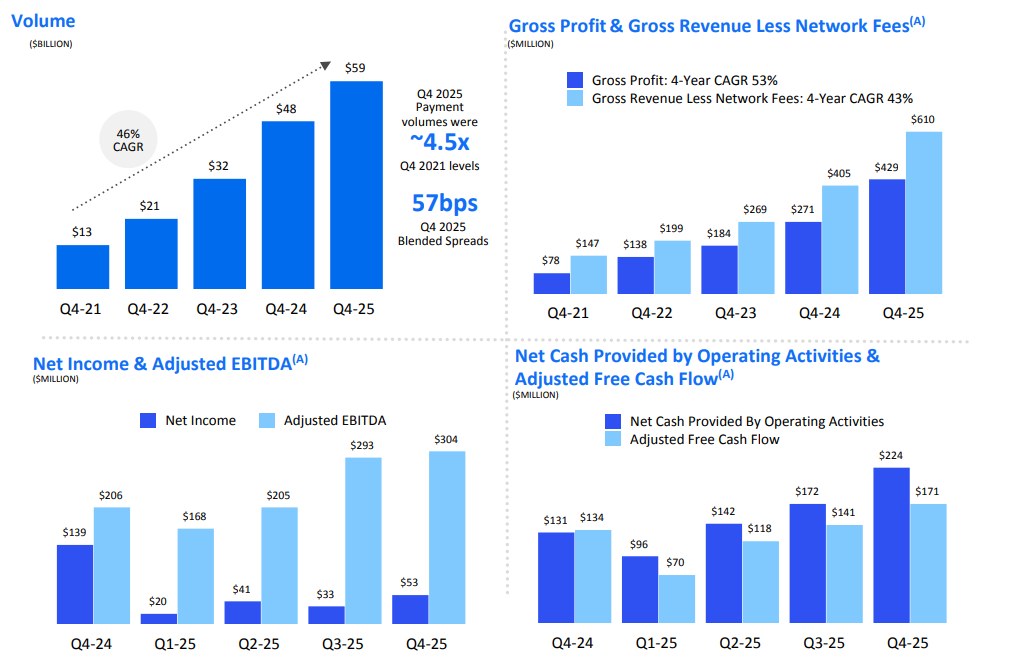

Shift4 delivered decent numbers in Q4 2025. Payment volume grew 23%, GRLNW (Gross Revenue Less Network Fees) grew 51%, Gross Profit grew 58%, and Adjusted EBITDA grew 48%:

This growth was evidently not all organic (due to the acquisitions of Global Blue and Smart Pay), and here’s where (imho) the “problems” start.

Management disclosed last quarter an organic growth figure. Even though this was well received by shareholders, they did not provide one this quarter (at least not a “clean” one). This should’ve (and it did) raised some eyebrows because lower disclosure is evidently not great (and a terrible misstep in communication in my view). Management, however, improved disclosure through other means. For example, they provided disclosure across revenue sources. Management now views the business across three segments:

Payments-based Revenue Less Network Fees: $340 million or 56% of the total

Tax-Free Shopping (i.e., Global Blue): $125 million or 20% of the total

Subscription and Other: $145 million, or 24% of the total

I welcome this disclosure, especially since it somewhat allows us to understand where organic growth lies. I must say (in fairness to management) that they did provide a proxy for organic growth during the call:

When you exclude the contribution of Global Blue and Smartpay, we delivered roughly 23% year over year growth in gross revenue less network fees during 2025.

Even though the word “organic” was not mentioned, the above seems to be a close proxy. Still, there’s a significant caveat we must be aware of. We must not forget that a good chunk of this “organic” growth stems from cross-selling to “acquired” customers. What this ultimately means is that Shift4’s organic growth story is, to an extent, dependent on ongoing M&A activity (albeit the runway is long if M&A were to completely stop today).

So, ultimately, no, 23% is not even close to Shift4’s terminal organic growth rate. The company’s true terminal organic growth rate is likely much much lower (LSD-MSD maybe?) and is indexed to global consumption. Management mentioned that they saw strength in enterprise but a continuation of weak Q3 SSS (same store sales) among SMEs in the Americas. This is ultimately the underlying organic growth that the business would enjoy absent M&A and the cross-selling pipeline. Now, it remains interesting that some people believe that true organic growth should not include cross-sell and should be equivalent to growth in perpetuity. Were this the case, I suspect that organic growth across many businesses would be lower than reported.

Management’s growth guidance disclosure for 2026, together with the new revenue sources, should help somewhat approximate organic growth (or at a minimum understand that it’s not 0% like many people claim). Management guided for the following in terms of payment-based revenue less network fees:

Mid-teens percentage growth in the Americas market with “minimal” contribution from M&A

High 20s percentage growth in Worldwide payments-based revenue, which does include synergies from Global Blue and SmartPay

Even if we assume that all growth in Worldwide Payment Revenue Less Network Fees is inorganic (which it is not the case whatsoever considering that synergies with Global Blue are not expected to bear fruit until H2 2026), arguing that organic payments growth is 0% (or even below HSD) becomes a challenge.

As for the remaining segments, management guided for the following:

Tax Free Shopping: mid-single digit organic growth

Subscription and other: low single digit growth

I mean there’s no denying that Shift4’s core organic growth (excluding cross-sell) is not spectacular, but I suspect the company has a long runway ahead before this “terminal” organic growth becomes the headline organic growth.

Now, I do understand where the market concerns come from. Why call it…

The Americas market, this is our most mature region where all of our market leading experience, economy, commerce, solutions are present and is a market where in 2026 there will be minimal impact from prior year M&A annualization, we expect payments based revenue less network fees to deliver mid-teens percentage growth. We view this growth rate as being more than three times the baseline growth of the comparable market.

…when you can just call it organic growth? One thing even the most enthusiastic Shift4 shareholders can’t deny is that communication was poor. One could definitely argue that with $500 million outstanding in the repurchase program and a new CFO there’s probably no reason to be an optimist, but this shouldn’t prevent management from communicating well.

The Global Blue concerns

The mid-single digit growth expected for TFS (which is almost exclusively Global Blue) also raised some concerns. Concerns came along the lines of…

What a dud acquisition. Decelerating growth and no significant synergies.

Let’s address both. First, yes, Global Blue is expected to decelerate next year (this is a mathematical fact). Management attributed the deceleration to exchange rates and rising tensions in Asia (between China and Japan). Now, MSD for the standalone Global Blue is not catastrophic. Before being acquired by Shift4, Global Blue guided for an organic growth CAGR between 8-12%. Shift4’s management argued that the business grew low double digits in 2025 and that growth will normalize in 2026. Adding both years together we probably get to a 7%-8% CAGR for the 2025-2026 period. Not great, but not catastrophic either.

I believe that many viewed this as terrible due to the lack of synergies. This POV is (in my view) a bit flawed because…(1) it assumes synergies will be realized through TFS and not payment-based revenue less network fees (it’s likely here where we would see synergies as Shift4 cross-sells payments to the TFS customer base) and (2) we are still barely 6 months into the acquisition period.

Shift4’s strategy here is to cross-sell payments to TFS customers by offering them an all-in-one terminal that includes payments, TFS capabilities, and DCC (Dynamic Currency Conversion). Only Shift4 is able to deliver this, but the main bottleneck is getting the product out there.

They expect these cross-selling opportunities to start materializing this year, but it’ll probably be more back-ended. Shift4 currently has around 80,000 merchants in international geographies (to which TFS can also be cross-sold to) and they believe the addition of Global Blue could potentially accelerate net adds in international geographies:

To give you a sense of how we view success internally, it’s the ability to add several thousand merchants a month towards the back half of this year. We see a lot of that data internally, and we know that several thousand merchants a month is a very reasonable outcome.

So, I mean, not outstanding, not catastrophic either (at least not yet).

Is the market worried about the balance sheet?

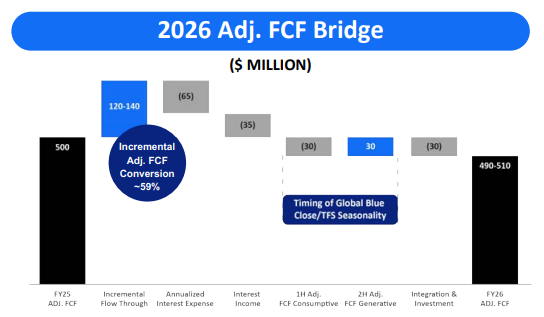

Global Blue comes with an additional “problem” in 2026 (besides lower organic headline growth): Free Cash Flow conversion. Free Cash Flow conversion is expected to drop to 42% in 2026 driven by three things:

Annualization of higher interest payments

Lower interest income due to lower cash balances

The impact of Global Blue seasonality

I must say that I don’t know if I truly understand the last point (don’t think it was explained well during the call), although I’ll give it a go. This is what Shift4 shared in the shareholder letter:

GB Timing of Close / TFS Seasonality: The Global Blue acquisition closed on July 3, 2025 resulting in 2H25 consolidation of operating results. The Tax-Free Shopping business has seasonality with Adj. FCF consumption in CY1H due to NWC growth in the seasonally high shopping periods and Adj. FCF generation in CY2H. On a YoY basis, given the timing of the transaction close, 1H26 will fully absorb the Adj. FCF consumption period while the 2H26 Adj. FCF generation only reflects the incremental Adj. FCF over 2H25 Adj. FCF generated.

What I believe they are ultimately saying with this is that Free Cash Flow generation was inflated in FY 2025 because Global Blue did not consume working capital (i.e., Shift4 only enjoyed the working capital tailwind). In 2026, this tailwind goes away and becomes a $30 million headwind to conversion. The company is also incurring $30 million in additional expenses related to the integration of Global Blue and AI infrastructure which they don’t expect to recur over the long-term:

Note that cash generation will actually be lower than guided because the TRA payment has been excluded from Adjusted FCF. Taylor Lauber (Shift4’s CEO) told me that it should be adjusted out because it’s one-time and comes with future cash benefits (some could argue it’s an investment). While I do agree with his POV here, it’s nevertheless something to consider when looking at pure cash generation in 2026. Instead of $500 in Adjusted Free Cash Flow, Shift4 will most likely generate somewhere close to $361 million (the above minus the $138.8 million cash payment related to the TRA).

Weak cash generation is some kind of a concern. It shouldn’t surprise anyone that the market sees Shift4 as a levered company ($3.5 billion in net debt) that is seeing FCF conversion drop while the core business (excluding cross-sell) slows down somewhat and while management continues to plow money into buybacks:

As we looked at our capital allocation options in Q4, we found the most attractive risk adjusted return was repurchasing our own stock between Q4 and year to date, we have repurchased 7.7 million shares and now have a remaining $500 million.

With the Adjusted Free Cash Flow guide calling for $500 million in 2026 (excluding the TRA payment), Shift4 has several options:

Lever up more to continue repurchasing shares: cash generation in 2026 is unlikely going to be enough to fund the remaining repurchase so they might have to draw down the cash position or issue more debt

Stop repurchasing shares to start paying debt down: this seems to be the preferred option for the market

Regardless of which one you think is the most appropriate option, what the market is likely worried about here is potential bankruptcy. When debt significantly surpasses equity, the latter can be whipped out quite fast if problems arise. It’s not unusual to see significant volatility in highly-levered companies (more so when around 30% is in the hands of its owner) and this is what we might be seeing play out for Shift4. So, what is the market worried about? The perfect storm:

Recession: lower growth and lower cash flow

Shift4 needs to refinance (if they can) at unfavorable terms

The equity becomes permanently impaired

Can this happen? Yes, of course, but I attribute it a low (albeit non-zero) probability. There’s no denying that Shift4 is indexed to global consumption patterns. This means that a recession would put pressure on SSS and, therefore, on payment volume. One could also think there could be some pressure on the take rate as the market becomes more competitive, although the market is already pretty competitive and take rates are stable (so there must be something more than just price playing a role).

During the Global Financial Crisis (the most “recent” crisis that impacted consumption the most), PCE (Personal Consumption Expenditures) fell by 3.4%. It’s true, though, that the non-discretionary segments to which Shift4 is more exposed did see considerable declines from peak to trough, roughly of about 10%. I don’t want to call it a worse case scenario but it would be pretty close to one. A 10% decline would probably come with some kind of operating deleverage, so Shift4 could potentially face the situation where FCF drops 20%-30% in a given year.

From the 2026 guide of $500 million in Adjusted FCF we would end up with around $400 million in FCF (which already assumes interest has been paid). With no relevant maturities until 2032-3022, I’d say that the risk of bankruptcy is low, but seeing the market worry about the balance sheet should not be surprising either.

The company is currently trading at a FCF multiple (on its market cap) of around 9x times, which does seem pretty cheap for a company growing at a mid teens rate (“organic”). If we use EV we also have to use unlevered FCF (which is around $670 million), meaning that Shift4 is trading at an EV/FCF unlevered multiple of around 14x. I will most likely add to my position at current levels because (acknowledging all the negatives), the opportunity does seem quite asymmetric.

One more thing…

Just as I was writing this I saw that Jared Isaacman, Shift4’s founder, made an open market purchase worth around $13 million after the post earnings drop:

Some will point out that he did the same thing a while ago and that he is 50% down on his previous purchase. While this evidently correct, I believe there’s no denying that the LT chart portrays that he is somewhat opportunistic with his purchases:

Regardless of whether you view the stock as cheap or not, one thing that’s clear is that this is what you’d like to see as a shareholder when the company is using cash to aggressively repurchase shares.

Have a great day,

Leandro

Great post — Shift 4 is a really interesting one. I also just published a deep dive on the company if anyone wants another perspective on it! https://substack.com/@stonemountainresearch/note/p-189720240?r=1ml5j6&utm_source=notes-share-action&utm_medium=web

Horrible communication, but overall not much changed. I'm super tempted to add slightly as well, but I'm also not really looking to increase payments exposure further