The Death of Software and (more) Tariffs (NOTW#55)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

The markets somewhat recovered this week after a couple of not-so-great weeks. It was also a week packed with news (tariffs, the death of SaaS…) all of which I’ll discuss in the market overview. In the news section (exclusive for paid subscribers), I also explain why I remain hesitant to invest in pharma companies directly and prefer getting exposed to the sector through picks and shovels (applicable as well to the semiconductor industry).

Without further ado, let’s get on with it.

Articles of the week

I published three articles this week, all of which were earnings digests. The first one was Nintendo’s earnings recap.

A Smashing Debut

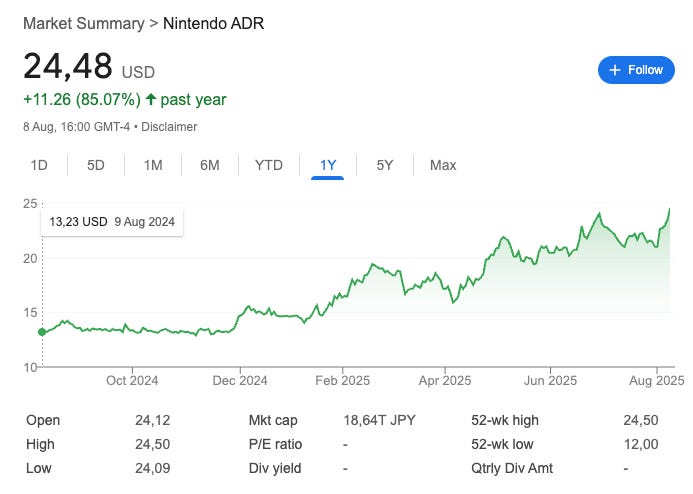

Nintendo reported great Q1 earnings last Friday, where we finally got to see some official numbers around the debut of the Switch 2. Everything called for record numbers, but the truth is that it was better than most (myself included) expected. Before going into the details, let’s take a look at the headline numbers.

Management is on pace to beat its annual estimates after a smashing Switch 2 debut, but they decided to stay put and avoided raising guidance (in pure Nintendo fashion). Investors and the market, however, seem to be updating their own estimates, and the stock climbed to a fresh new all-time high:

Nintendo made it into my portfolio in February 2023 at a price of $10.16, although I have added significantly to my position since. With the benefit of hindsight, I can say that I should’ve added much more (duh!), especially as it was one of the most skewed opportunities I have ever found (i.e., the risk I was taking seemed very low compared to the potential reward).

The second article of the week was Stevanato’s earnings recap.

An Implicit Organic Raise?

(My Stevanato in-depth report is free to read as one of my model reports. You can read it here.)

The company reported strong numbers, but management decided to maintain guidance due to some non-operational headwinds. This demonstrated (as I discussed in a previous article) that guidance had been sandbagged. The market punished the stock significantly the day after earnings, but it recovered some of the drop over the coming days. I also made a significant update to my purchase price because I had made a couple of mistakes in my valuation model. Luckily, the mistake led to a more conservative “buy” price rather than the other way around!

The third article of the week was Zoetis’ Q2 earnings digest.

What is the market worried about?

Zoetis reported a beat-beat-raise quarter this week, but the market portrayed a version of its bipolarity. Zoetis’ stock was up almost 10% in the pre-market, but ended the day 3% down! I’ve been investing for a while, and (outside of meme stocks or stocks with very tight liquidity) I struggle to remember experiencing a 13% fade on a $60 billion+ company. This is one of the things I “love” about the stock market: you never know how it’s going to surprise you.

The company reported good earnings, but the growth drivers left some doubts among investors, and the stock remains close to 5-year lows.

Next week, I plan to bring earnings digests from Amazon and Constellation Software. I am also thinking about starting a new article series, but I’ll give you more details over the coming weeks.

Without further ado, let’s see what the markets did this week.

Market Overview

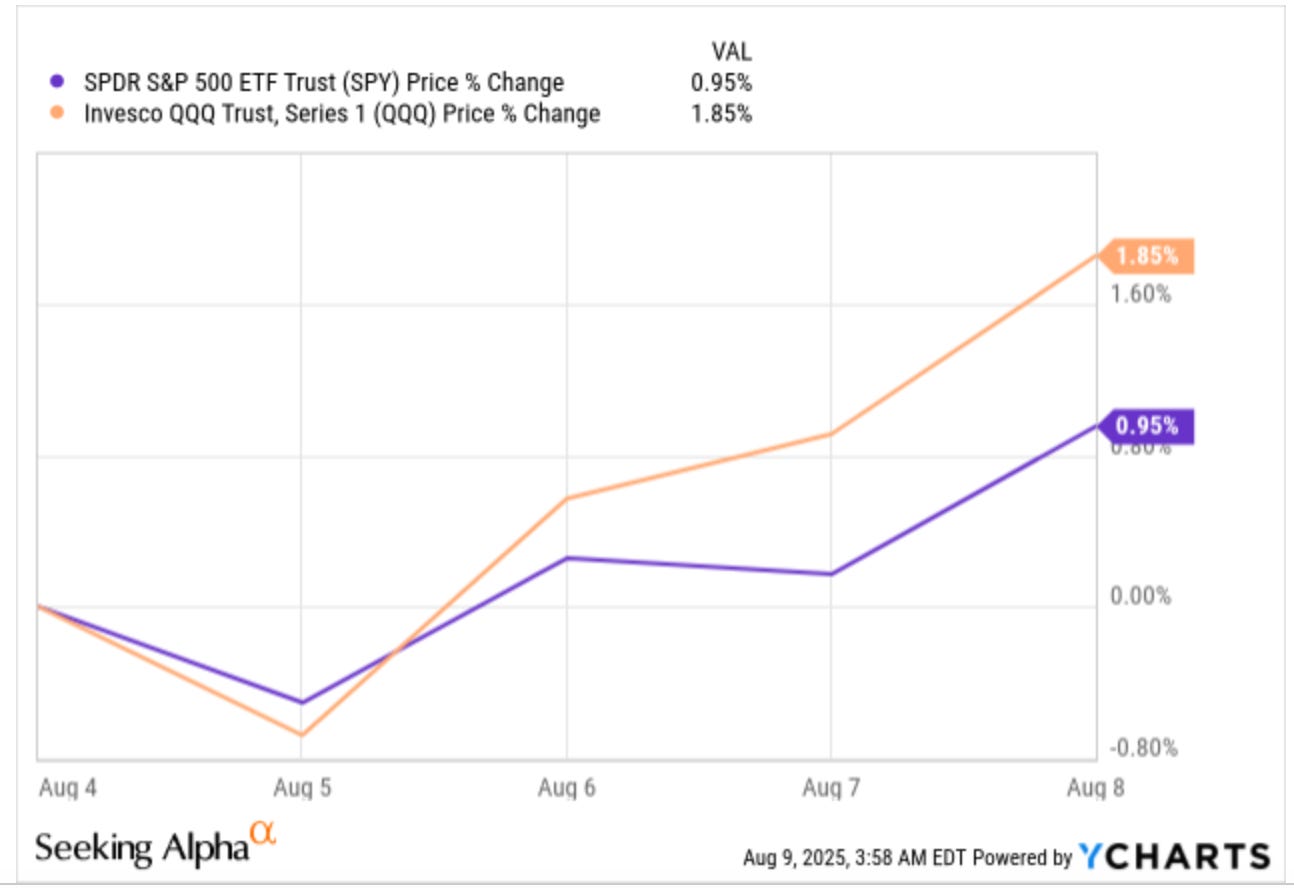

After a couple of weeks of “hesitation”, indices went back to doing what they’ve been doing for a while: climbing to all-time highs. Both the Nasdaq and the S&P rose this week:

There were a couple of interesting “stories” this week. First, Trump announced 100% tariffs on semiconductors. While this might sound worrying at first, the announcement came with a very important caveat: companies that have announced plans to invest in the US would not be subject to said tariffs. With Intel, Samsung, and TSMC all having ongoing plans to invest in the US, the 100% semiconductor tariff suddenly becomes 0%! Semiconductor stocks reacted positively, probably signalling this might be the light at the end of the tunnel that everyone had been waiting for.

Trump also made another announcement that concerns the semiconductor industry: he called for the resignation of Intel’s CEO (Lip Bu Tan), citing his “ties with China.” Some people pointed out that Intel’s real problem is not the CEO but the board, which I honestly don’t know if it’s the case because I don’t follow Intel that closely. As an ASML shareholder, I view both news as positive. The tariff announcement reduces the uncertainty and confirms that fabs must go through with onshoring if they don’t want to suffer competitively in the US. As for the Intel news, it clearly demonstrates that the US government cares about the survival of Intel, and having more than one credible customer for EUV is good for ASML.

There was more tariff-related news. Trump also announced that pharma tariffs could go up as much as triple digits, but that he would give some time to Pharma companies to onshore production. While the outcome of this is still unknown, it definitely benefits two companies in my portfolio (Danaher and Stevanato) as it will most likely create a more inefficient supply chain, resulting in more equipment sales. Stevanato also benefits because the company is way ahead of its peers in building capacity in the US. This means that if tariffs become a consideration for customers, Stevanato becomes more attractive than competitors (both of which manufacture primarily in the EU).

All this said, the topic that took the market by storm was the launch of ChatGPT 5. OpenAI hosted a (not outstanding) demo of its new flagship model, unleashing many people’s imagination. First, it made many people think that AGI/supreme intelligence is actually further away than we thought. The reason is that ChatGPT 5 doesn’t seem exponentially better than its predecessor. Bear with me because this POV is not very consistent with what I am about to share now, but it also surfaced worries about the sustainability of SaaS business models. SaaS stocks plummeted as the market increasingly believes that AI will render their business models obsolete by reducing the cost of developing software to 0.

Software “bears/skeptics” believe that in a utopian world, every business will write their own software and will not rely on software vendors. This seems somewhat of a stretch for several reasons. First, it’s not the core operation of these businesses. Secondly, it seems like enterprises would be taking a huge risk for a pretty small payoff (software doesn’t typically make a huge portion of Opex for many businesses). The judge is still out there as to what will happen with software in an AI-driven world, but I’d say it’s probably more complex than just saying that everyone will develop their own proprietary software because AI lowers development costs. Note that a “similar” argument was made with the advent of the cloud. Many believed that not requiring to have on-premise hardware would lower development costs (which it did), leading to the “death of software.” Turns out that what it did was lower the barriers to software adoption, helping software build the SaaS model that has worked so well over the last decade.

When there’s a significant change in any industry you’ll have a lot of people claiming one of two things:

It’s different this time

It’s not different this time

We will only know which one is right in hindsight, but note that software can still do fine regardless of whether it’s different or not this time. The SaaS revolution meant that “it was different this time,” it’s just that it was not a bad outcome for software. Like in everything in life, I don’t expect things to be black or white. Some business models will get competed away, others will come out stronger (and this is inside the same industry). This said, I am fine if the weakness persists as I have started looking into a software company that in my opinion would benefit from any of the outcomes above.

The industry map was mostly red, with two noticeable exceptions: software and Lilly (for reasons I’ll explain in the news of the week):

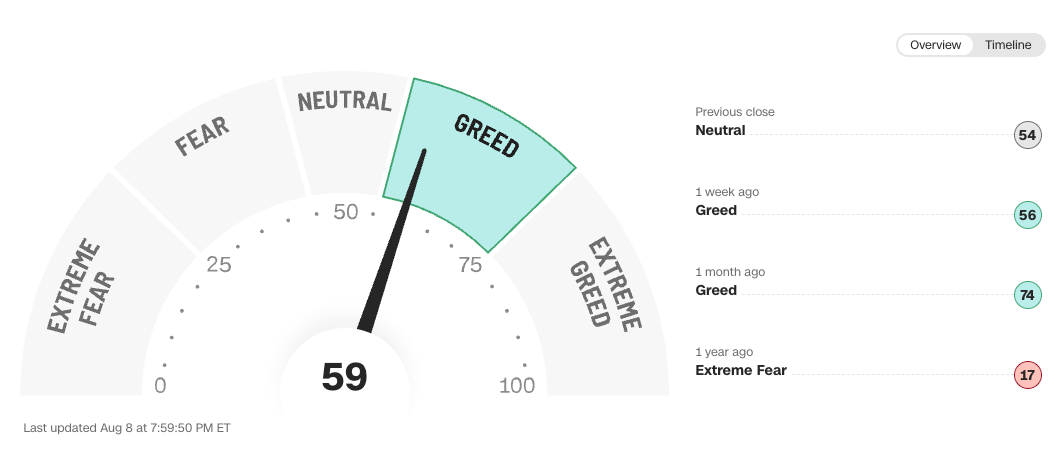

After quickly dropping to neutral from almost extreme greed last week, the fear and greed index went back to greed territory this week:

This is what I bought this week

I added to several positions this week. Here they are: