An Implicit Organic Raise?

Stevanato's Q2 earnings

(My Stevanato in-depth report is free to read as one of my model reports. You can read it here.)

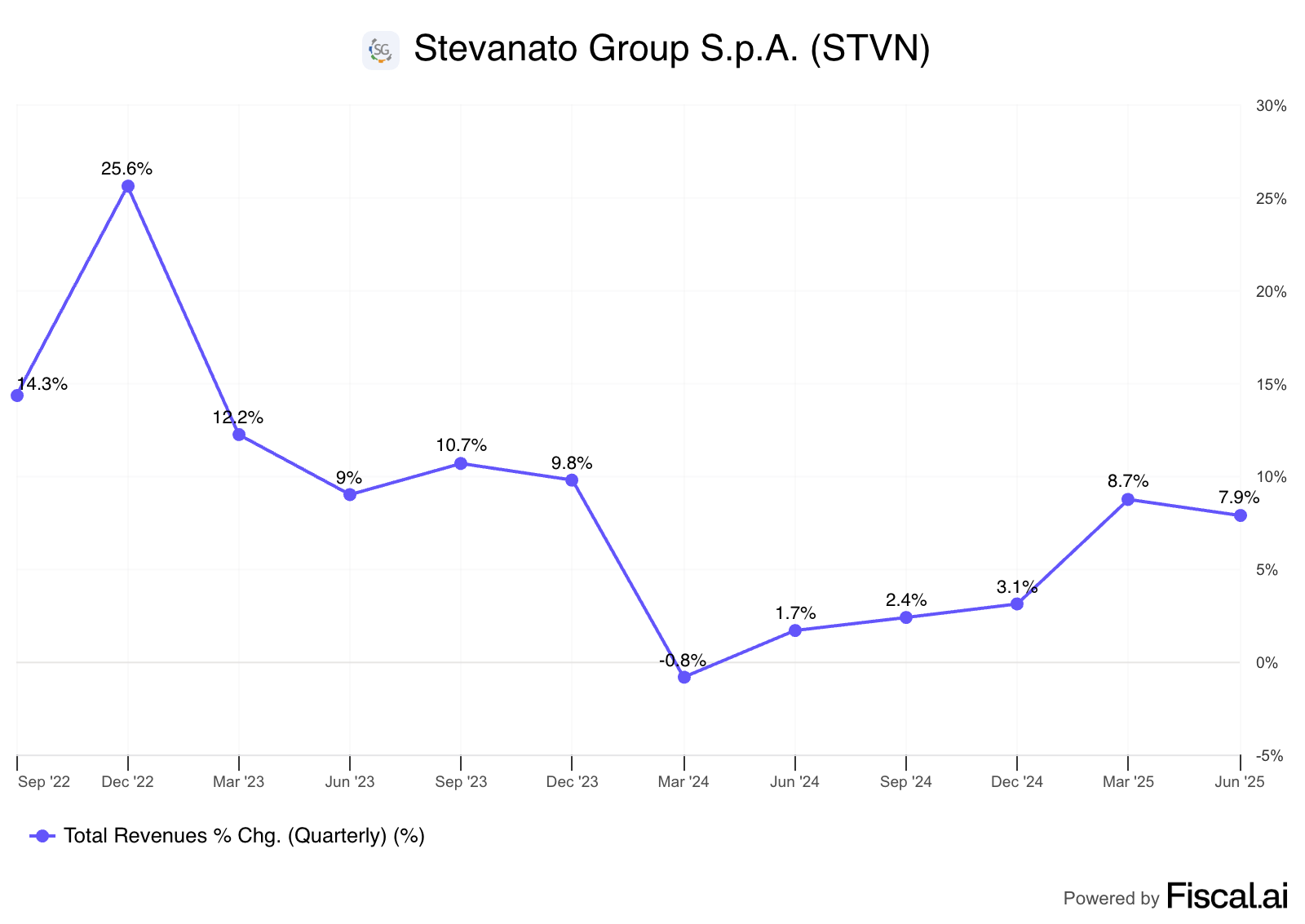

Stevanato reported earnings on Tuesday, and the market did not like these. The stock dropped almost 10% (albeit it recovered somewhat on Wednesday +4%):

Regardless of what the drop might make you think, earnings followed the same path as those in Q1: outstanding numbers coupled with management conservativeness. Q2 also portrayed (once again) the growth and margin potential of the business.

I know this is going to sound strange at first, but it's rare to find a management team that implicitly raises guidance while maintaining guidance. While I am all up for management conservativeness (let the numbers do the talking), there’s no denying that it’s tough to see a stock rise significantly without delivering an explicit beat-beat-raise in a stock market dominated by participants trading around earnings.

Let’s start by looking at the numbers.

The numbers

Stevanato delivered another solid quarter in terms of growth and margin expansion. Revenue came in at €280 million, growing 8% on a reported basis and 10% on an FX-neutral basis. Note that Stevanato reports in Euros, and even though the company hedges some of its currency exposure, a weaker dollar is a headwind. Revenue growth has accelerated materially after a weak 2024 (destocking):

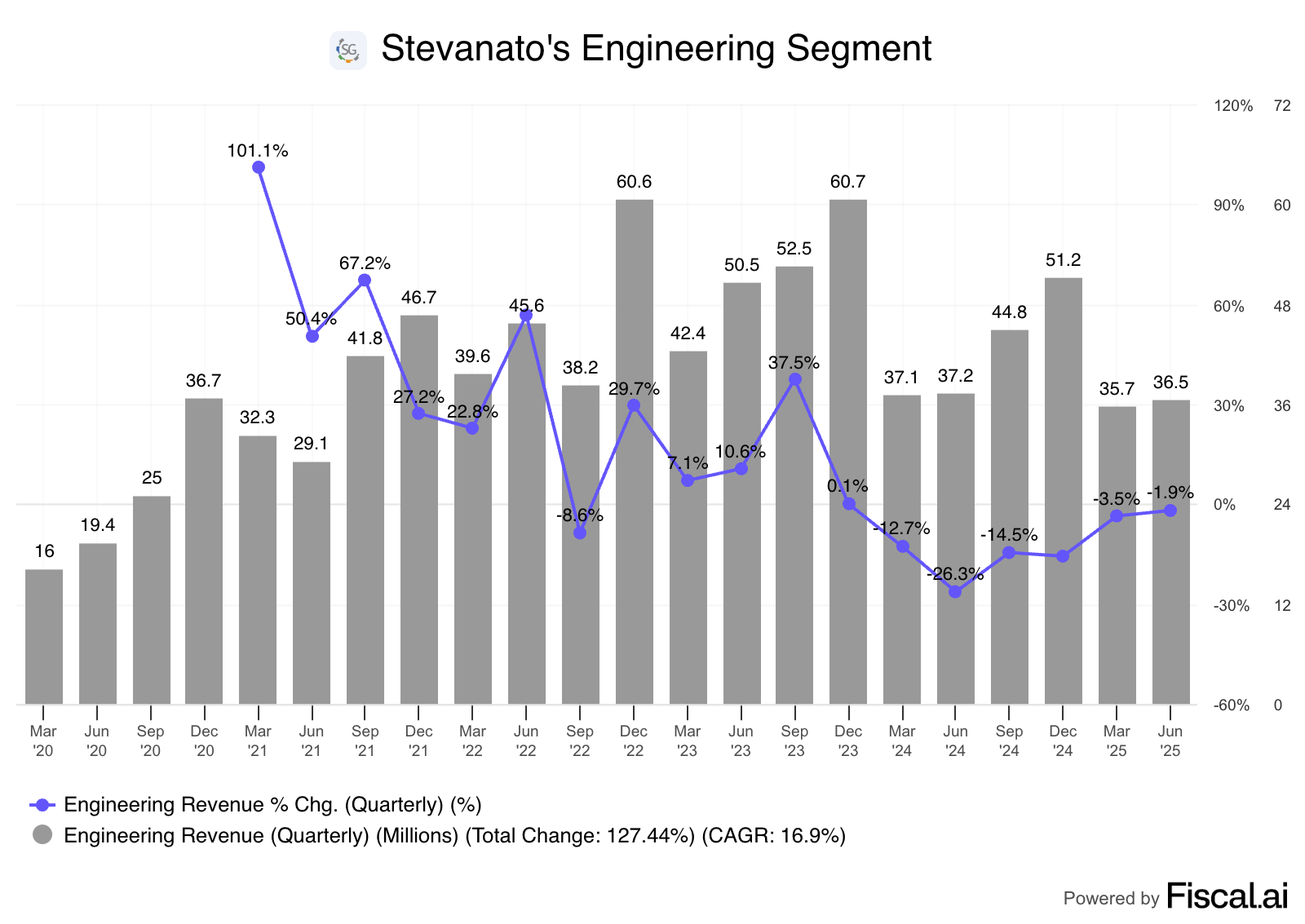

Note that revenue would’ve accelerated sequentially if not for the currency impact. The different segments show more good news. BDS grew 10% year over year (12% at constant currency), and the engineering segment decreased 2%. Within BDS, high-value solutions grew a whopping 13% year over year and already represent 42% of total revenue (and 48% of BDS revenue).

The good news for engineering is that it seems to be bottoming (albeit we’ll see later that this is not the case yet):

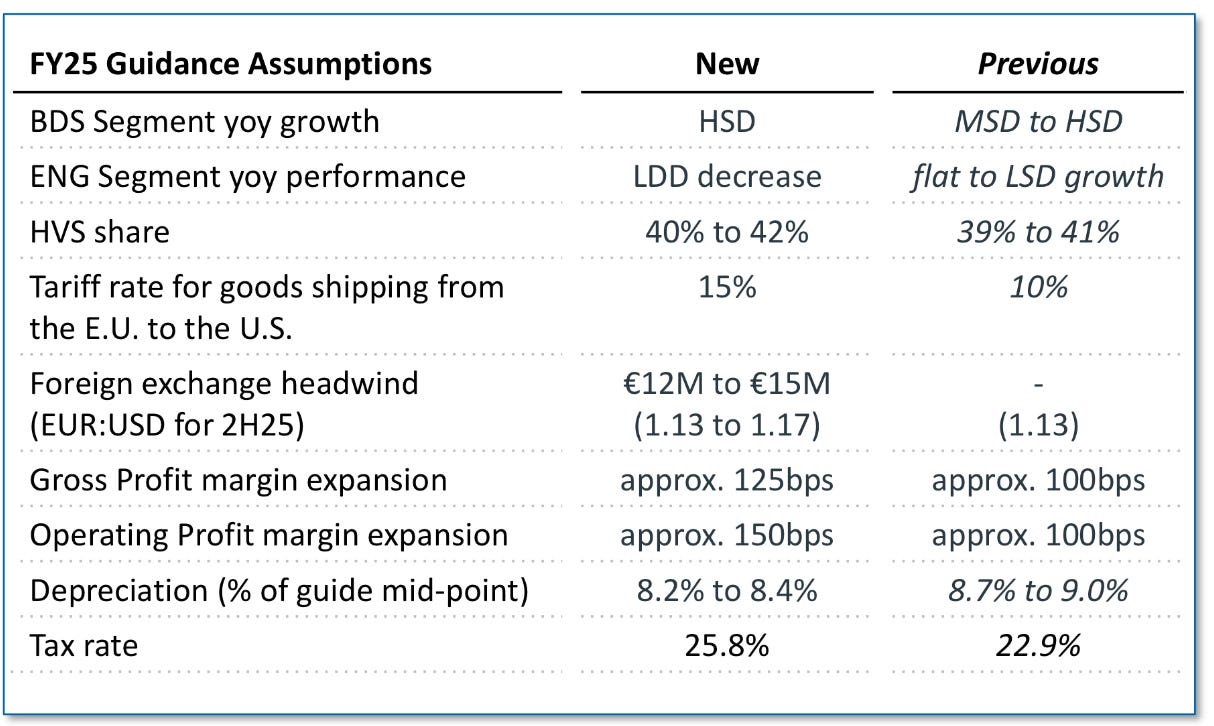

Management pointed out that there was a deferral of engineering orders in Q2, which impacted their profitability and full-year expectations. They now expect to receive these orders in the second half of 2025, but these will probably not be fulfilled until 2026. Therefore, Stevanato now expects a low double-digit decrease in engineering compared to the flat to slight growth that they expected last quarter.

Despite the apparently “low” importance of Engineering, it’s currently a headwind to Stevanato’s consolidated growth and margins. The differential is just too large for it not to have an impact. BDS is growing 12% in constant currency while engineering dropped 2%. The margin gap is even more material, with BDS gross profit margin coming in at 31.2% and engineering gross profit margin coming in at 6.6%. Operating margin in BDS was 19.1% whereas it was negative 0.8% for engineering.

The good news is that management showed optimism. They expect to return to HSD growth (the “historical growth profile” of this segment) in the future and to ultimately match the 2023 margins. For context, engineering delivered 26% EBIT margins in 2023, and the operating margin of the most recent quarter was -0.8%. Management also mentioned onshoring as a tailwind for the segment, something that should bode well for other companies like Danaher (through bioprocessing equipment).

We are starting to see a change in the strategy, in particular, with our big international clients, and also some biosimilars, to review their installation of capacity in the United States.

A closer look at margins

Margins are where things get interesting for Stevanato (even though I wouldn’t call double-digit growth unexciting!). The company managed to expand margins significantly again. The Gross Profit margin expanded 210 bps due to the ramp-up in Latina and Fishers and the higher mix of HVS. Now, despite this good performance, the gross profit margin is still suffering some significant headwinds:

The ramp up of Latina and Fishers: despite this being a tailwind to margins as utilization improves, it’s also sort of a headwind because both plants combined are still dilutive to consolidated gross margins

Engineering gross margins are currently dilutive to consolidated gross margins as well and significantly so (discussed above)

The tailwinds were more substantial than the headwinds (helped by the fact that BDS makes up 85% of total revenue), so Stevanato grew gross profit by 16% on the face of 8% revenue growth. News is even better when we go down the income statement. The operating profit margin expanded 400 bps to 14.8%. This means that operating profit grew 29% in Q2. Note that it’s the second consecutive quarter of +20% operating profit growth for Stevanato, portraying why pretty much all the headline numbers about the company were misleading. The 2024 growth rate was not normalized, and neither were margins.

Note that underlying margins ex-engineering are ramping pretty fast even though Latina and Fishers are not yet fully utilized. BDS gross margins expanded 350 bps to 31.5%! The operating profit margin of the segment rose 460 bps to 19.1%. BDS is single-handedly carrying the margin expansion of the business despite facing some headwinds that slowly but steadily are converting into tailwinds.

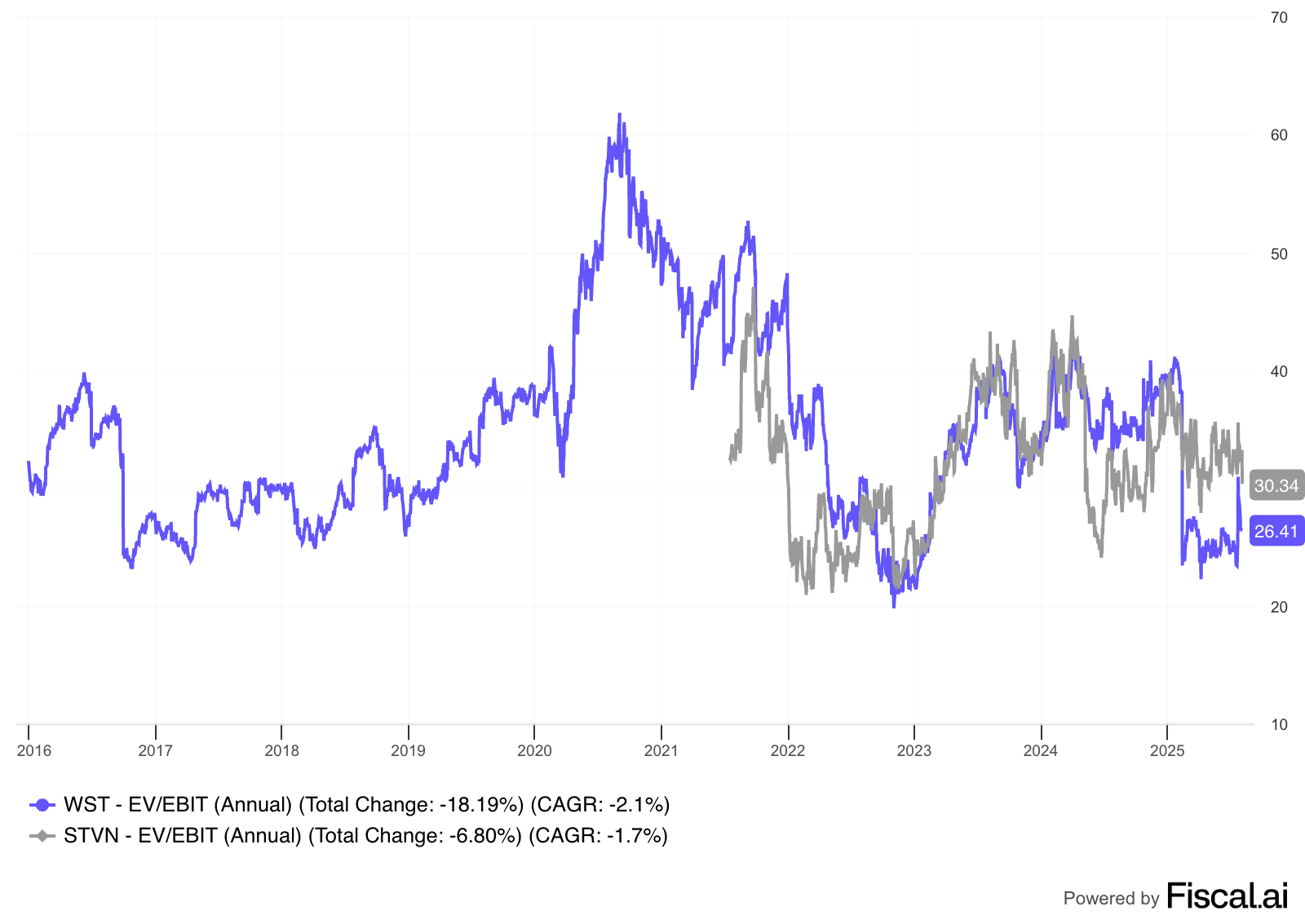

I expect Stevanato’s margins to continue expanding as it grows over the foreseeable future. With management expecting a recovery in engineering and the continued ramp-up of Latina/Fishers + the high-value solutions, we shouldn’t be surprised to see gross margins approaching 40% (or higher) by the end of the decade (I might be a bit conservative here and I’ll later explain why) from a current level of 28%. This would be a 1,200 bps gross margin expansion in under 5 years, while at the same time experiencing top-line growth of HSD/LDDs. The EV/EBIT multiple is optically high, but Stevanato can enjoy strong earnings growth over the next decade+ (especially as margins normalize). Note that West Pharmaceuticals is not trading at a dissimilar EV/EBIT despite having far fewer tailwinds at its disposal:

Management’s ongoing conservativeness

The highlight of the quarter for me was again management’s conservativeness. Last quarter, I titled my article ‘Sandbagging…anyone?’ claiming that the guide was too conservative based on what we were seeing. Now, even though management did not explicitly raise the guide this quarter, they did so implicitly (at least organically speaking). The reason was that they saw two additional headwinds not present in Q1 and still held the guide:

A weaker dollar: they now expect a €12 to €15 million headwind from €0 in Q1

A higher tariff rate, which has risen from 10% to 15% due to the new “agreement” the US and the EU signed earlier this month.

The fact that they maintained the guide despite these two additional headwinds means that they would’ve raised it if these had been absent.

For foreign currency, we now assume a headwind of approximately €12 to €15 million in the top line. The headwind is fully absorbed in the model. An updated tariff rate for imported goods from the European Union to the US of 15% compared with our prior assumption of 10% is also fully absorbed in the guidance.

Note that on an organic basis (i.e., ignoring FX), the midpoint of the guide would be €13.5 million higher, which would’ve resulted in a 1% raise (without considering the additional impacts of tariffs). There was an additional headwind to the guide that demonstrates that profitability had also been grossly sandbagged: the tax rate. Stevanato now expects a tax rate of 25.8% compared to the previous 22.9%. The diluted EPS guidance was maintained despite the higher tax rate. The offset was that they now expect more significant margin expansion due to a more significant share of high-value solutions share within BDS:

To achieve the midpoint of the revenue guide (€1.175 billion or 6.5% growth), growth in the second half of the year would have to decelerate to mid-single digits. Recall that Stevanato grew 8.7% in Q1 and 7.9% in Q2 and is guiding for an H2 deceleration despite no signs that BDS will slow down. Comps indeed become somewhat tougher in H2 than H1, but the slowdown can primarily be attributed to engineering.

This was the only negative revision in the guide, which went from flat/LSD growth to LDD decline. Management claimed that they still expect sequential improvement in Q3 and Q4 for engineering, but this still results in a year-over-year decline as comps get much tougher in the second half. Suppose we assume engineering revenue improves 5% sequentially in Q3 and Q4 (much lower than the step-up the segment typically sees in the second half). In that case, we get to 2025 revenue of around €151 million, which is consistent with a low double-digit decline for the segment. A 10% year-over-year drop would result in engineering revenue of around €153 million.

Now, the BDS guide went up from MSD/HSD to HSD (high single digits). HSD seems conservative considering the segment grew 11% in Q1 and 10% in Q2, and the fact that Latina and Fishers continue their ramp. A 9% growth in BDS for the year means revenue ends up at €1.018 billion. Add both together and we get to around €1.17 billion, the midpoint of the guide. Now, if BDS grows 10% (which is not out of the question), then we get to €1.18 billion, at the high end of the guide (which, in my opinion, is more realistic).

While all of the above demonstrates that the guide given in Q1 (with the information we knew then) was extremely conservative, the timing issues in engineering might have made the guide now somewhat “realistic.” Note that the fact that this is a timing issue means that it’s not really that relevant for the long term, as the engineering orders that got postponed will probably make it into revenue in 2026. There’s also another possibility that management is unsure if they’ll be able to deliver on these orders by year-end, and therefore, they prefer to play it conservatively.

What seems evident to me is that management should come up with an organic revenue metric considering they report in euros and the fact that, with Fishers ramping up, they are expected to generate significant dollar revenue in the future.

Is Stevanato a buy today? A significant change to my price estimate

I made my first purchase of Stevanato in November at $18.23. I’ve added to my position since and my average cost is now $19.23. This means that my position is up around 25% in under a year, but does this make the stock expensive today? I have already discussed above that the fundamentals are all going in the right direction, but do they fully justify the higher price? Let’s take a look.