Understanding Medpace’s business

Q1 Earnings

(Medpace is a company I profiled in May of 2025. You can read the in-depth report here)

Medpace’s fate in Q1 was not too dissimilar to that of Q4. The company reported outstanding earnings but dropped pretty much by the same magnitude as it did three months ago (22%). Medpace’s stock is not for the faint of heart, but it becomes easier to digest when you understand what’s going on:

The drop seems to have been caused by the go-forward looking indicators, to which management added their fair share of skepticism through pessimistic commentary. Just like last quarter, August decided to begin the call on a positive note (I am being ironic, in case you don’t get it):

Quarter one of 2026 saw cancellations rise again, with backlog cancels reaching their highest point in over a year. Net bookings were below the level seen in Q4, but well above those in Q1 2025, with a net book-to-bill ratio of 0.88. RFPs were down in the quarter sequentially and year over year. Initial award notifications and win rate were strong. We continue to view the quality of opportunity flow as good.

I have a theory as to why management (particularly August) turns every data point or qualitative commentary that is nuanced and could be considered “grey” into a black one to downplay the earnings, and I already shared this theory in my Q4 earnings digest (‘It’s all part of the plan’). The theory is pretty simple and doesn’t require a galaxy brain. If we consider the $657 million Medpace has in cash and the +$100 million in OCF (Operating Cash Flow) generation per quarter, together with the fact that Medpace only returns cash to shareholders opportunistically through share repurchases ($800 million left in the authorization), it’s not tough to understand that management has no incentive for the stock to go up right now, no matter how good the results are. There’s also a track record of management using this same strategy in the past, so it’s not like I am completely making this up.

One thing that I believe that this quarter also portrayed is that not many people understand Medpace’s forward-looking indicators. This becomes evident in the fact that most consider the book-to-bill ratio as Medpace’s “north star” and an unequivocal indicator of the company’s future (spoiler: it’s not Medpace’s north star and neither does it portray what will happen next year). The goal of this article is threefold, although I don’t expect to follow a strict guide:

Briefly go over the quarter

Explain Medpace’s forward-looking indicators in a way that they are understandable

Go over Medpace’s valuation (contrary to what many believe, Medpace doesn’t need to grow at 20%+ rates to work from here)

Medpace’s quarter

Medpace’s quarter was exceptional and the company delivered (again) a beat-beat quarter. The beat on the bottom line was pretty significant:

Revenue of $706.6 million beat estimates of $697 million (1.2% beat)

EPS of $4.28 beat estimates of $3.88 (10% beat). Just for context, Medpace has beaten EPS estimates 16/16 quarters, not a bad track record

The company started the year growing revenue 27% YoY, which is significantly ahead of the full year guide provided barely three months ago (9% to 13% YoY growth). Despite this delta, management decided to stay put with the guide and simply reconfirmed it. It was likely this plus a relatively “weak” book to bill ratio (0.88x) that caused the violent downward reaction of the stock. Jesse Geiger (Medpace’s President) announced its intention to retire in May, with August taking the position as they look for a replacement. This might have also worried investors because I believe Jesse was considered the “natural” replacement to August, but August calmed the waters claiming that he remains passionate about Medpace and will be at the reins for long (ofc, if his health allows).

Besides Jesse’s departure, everyone seemed to be hyper focused on two metrics: backlog and book to bill. Many believe that the direction of these two metrics portray that Medpace’s growth is about to decelerate significantly and that revenue is at the verge of a cliff. The former (the deceleration) is a pretty logical assumption to make as I don’t believe anyone believes that Medpace will continue growing at a 25% clip forever. A very different (but key) question is whether 25%+ growth is needed for the current valuation to make sense (something I’ll discuss in the last section).

So, why are both the backlog and (especially) the book to bill ratio ill-suited as Medpace’s go forward indicators? Let’s give it a shot, starting with the book to bill. Medpace reported a sub 1x book to bill ratio in Q1. What this ultimately means is that the company is eating into its backlog because it was not able to replace the entire Q1 revenue with net new awards. Management attributed this to higher cancellations than usual and also to lower than expected gross backlog bookings. They however believe that “initial award notifications and win rate were strong” (more about what this means later on):

Quarter one of 2026 saw cancellations rise again, with backlog cancels reaching their highest point in over a year. Net bookings were below the level seen in Q4, but well above those in Q1 2025, with a net book-to-bill ratio of 0.88. RFPs were down in the quarter sequentially and year over year. Initial award notifications and win rate were strong. We continue to view the quality of opportunity flow as good.

A lot of analyst questions were around the future rate of cancellations, to which management answered that they don’t view these as structural but rather as business as usual:

Cancellations were again just the kind of random stuff you’d expect. You know, product performance, reprioritization, etc. It wasn’t particularly informed by acute financial shortages or anything like that. It was just kind of a usual thing, but higher than we have historically averaged. It put pressure on our book-to-bill. Cancellations in the quarter were the largest. The therapeutic areas are oncology and cardiovascular, which is usual anyway. Really nothing to. It’s really too early to get any kind of read on cancellation rate and whether it’s going to be high again in Q2. I think it’s too early to make any kind of assessment of that.

This is interesting because the current guide is based on the current level of cancellations, but if these were to abate and with Medpace having grown 27% in Q1, the guide seems sandbagged (again, management has no incentive to not sandbag it if they want to repurchase shares).

Management also believes (and I fully agree with them here), that the book to bill needs context and that it’s actually not a great metric. The main reason is that, yes, Medpace delivered a sub 1x book to bill, but it did so in a quarter where it delivered 27% growth. This means that net new awards (the other variable used to calculate the book to bill alongside revenue) were actually up 24%. Not only does this seem sufficient to singlehandedly cover the full year guide, but management also believes that it’ll get better throughout the year. Now, “getting better” has three potential implications:

Revenue growth decelerates

Net new awards accelerates

Both

I don’t know which one will happen, but if the guide is legit (which honestly doesn’t seem so), then it’s logical to think that the book to bill will improve as revenue growth decelerates throughout the year. Will a book to bill over 1x in the face of revenue deceleration make Medpace a better business? I’ll leave this question unanswered and as food for thought in terms of interpreting the importance of the book to bill metric. August somewhat agrees:

First off, you know. Book the bill. I mean you. No, it’s just a horrible measure. I mean, look, I get it. It’s useful to see that the bucket is filling at a rate that’s commensurate with what’s pouring out in the revenue, that you’re either growth or non-growth in future revenue opportunity. But particularly under 606, you know. You don’t model things based on a book-to-bill. You know, we miss book-to-bill because revenue ran up so fast that it made our book-to-bill lower. Even though we exceeded our bookings expectation, you miss on things that are good. You missed that book-to-bill target because our revenue was so high. Oh, is that a bad thing?

I don’t want to talk about book-to-bill, and I’m not going to give a guide to future book-to-bill for us. But we certainly do hope to have improving bookings over time. I would assume that the book-to-bill of 0.88, where things are contracting, is not anything we would expect going forward. The cancellations can drive you to lower levels occasionally.

Let’s now turn to backlog and the famous “revenue cliff.” The market’s bear case claims the following: Medpace’s backlog is growing significantly slower than revenue which means that Medpace will eventually face a revenue cliff. In plain English this means that Medpace’s engine is not being fed enough gas so there will come a time when it abruptly stops. The numbers seem to support this thesis. Medpace’s backlog grew a paltry 2.9% YoY in Q1 to $2.93 billion. While $2.93 billion seems like a large number, the reality is that Medpace’s TTM revenue is around $2.7 billion. This ultimately means that the backlog is not (supposedly) covering more than 1 year’s worth of revenue.

Now, this bear case started getting traction last year, which led management to disclose (opportunistically and has not been since numerically disclosed) its pre-backlog figure. This is what management said back then:

There has been some concern that, you know, our burn rate has gone up quite a bit. You know, our backlog hasn’t grown much this year. So, you know, it’s low single digit. You know, a couple percent up over the past year. But I wanted to let people know that, you know, that the overall pipeline of awarded studies I mean, I’m not just talking about the pipeline of opportunities, awarded studies.

We’ve got a fixed scope of work. We’ve negotiated the price on it. They’ve, you know, you know, given us a written award for that. And it just hasn’t gotten to the first patient in yet. So we may be working on it. Etc.. And it just hasn’t gotten to you know, the first patient enrolled. And that’s in our, you know, this bucket pre backlog. And that is up 30%. And you know this pre-book this pre backlog bucket of awarded you know firm award work is larger than our backlog itself. And is up 30% over the year. So I think that puts us in a good position for refilling our backlog over the next year. And not having you know what a number of people have described as, you know, some sort of air gap in, in, you know, our revenue growth and, you know, things will stall. And we run out of backlog kind of, you know, so we really are. Improving our, our, our opportunities for backlog conversion in 26 and revenue generation.

In Q1 they simply said that the pre-backlog is generally comparable in size to the backlog and that it grew during the quarter (even though they did not quantify it). They remain, however, optimistic in terms of the pipeline that’s flowing into the pre-backlog:

The quarter was good in terms of clients telling us that they’ve now got money or they’ve got plans or they’re going to have money and they want to use us.

This changes the landscape pretty significantly. The bear case is that Medpace’s reported backlog is insufficient (both in terms of size and growth) to cover future revenue (i.e., a revenue cliff is coming). The reality, however, is that Medpace’s actual total backlog is likely closer to $6 billion and likely growing faster than the reported backlog (albeit we don’t know at what pace).

One could ask themselves why Medpace doesn’t simply report this number, and the answer lies in conservativeness. Management is very conservative in terms of what it includes in the backlog due to the risk profile of its customer base. We could argue that projects that are included in the backlog have significantly lower risk than those of pre-backlog as the first patient already needs to be flowing through. This means that things only go into the backlog when Medpace is already generating revenue from the project.

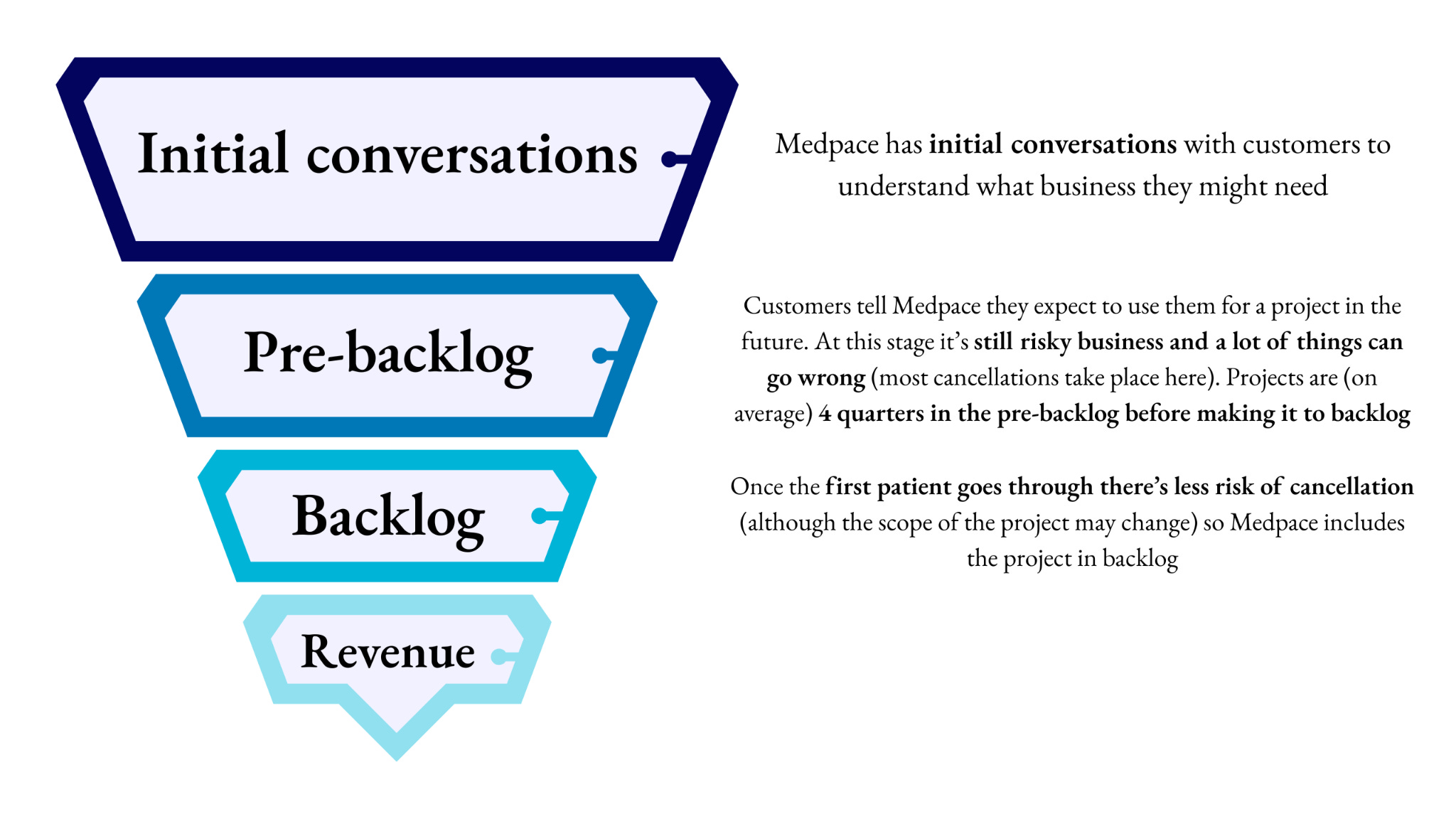

This is very important because I’d imagine that most people believe that the true definition of “backlog” is actually the pre-backlog and not the reported backlog. In fact, I highly doubt that other CROs report backlog as Medpace does (which also makes sense if they are exposed to large pharma). Anyways, just to clarify how this all works, I decided to work on the following chart:

Only the last two stages of this funnel (backlog and revenue) are reported to the market, but Medpace’s qualitative commentary around the first two were positive and somewhat invalidates (or reduces the risk) of the revenue cliff bear thesis. In fact, cancellations in the early stages of the pipeline were lower than in the backlog (which bodes well for future work flowing into the backlog):

Cancellations in that bucket though were not particularly elevated in the quarter in Q1. It was more backlog related cancellations that were problematic for us. I don’t think that impairs our future.

What one needs to understand is that the total opportunity set is pretty large and that it’s simply a matter of timing that makes projects flow to the “reportable” segments:

If you cancel, it’s probably dead. I mean, look. If things don’t generally come back from cancel bucket. But I’m just saying that there are things that didn’t make it into backlog, you know, in a given quarter that might come in in future quarters. You know, we might have expected them to come in one quarter and they get delayed and get pushed into other quarters. Some of the stuff that’s in backlog that gets put on hold, yeah, it could cancel. I mean, we don’t necessarily cancel it because of that. We just hold it in backlog. You know, it remains in backlog. You know, cancel it. It’s just on hold for a period of time. Hopefully it gets started. Or maybe it does cancel in the future.

Management also made a pretty interesting comment about the early stages of the funnel. They mentioned that they are working hard to improve the win rate and that they expect measurable benefits this year:

I’m not going to get into individual things. We’re doing. I think that’s just a little bit too much to push out to our competitors. But I just wanted to really express that, you know, we are focused on this and we do see opportunities. I wanted to just point out, we do believe there’s opportunities to expand our both the pipeline and the win rate on our opportunities. To really combat the higher cancellations should they continue on to get back to a growth rate that we want. It was more to really focus on that in terms of timing. I’m hoping this over the next few quarters we’re going to see. Real improvement. I think we already have even in Q1 a good win rate. I’m hoping it’s sustainable. The things we’ve done and put in place and the enhancements we’re making improve our. Our win rate meaningfully over the immediate term.

So, with all the context behind us, let’s take a look at the valuation.