It's Part of the Plan

Medpace's Q4

(Medpace is a company I profiled in May of 2025. You can read the in-depth report here)

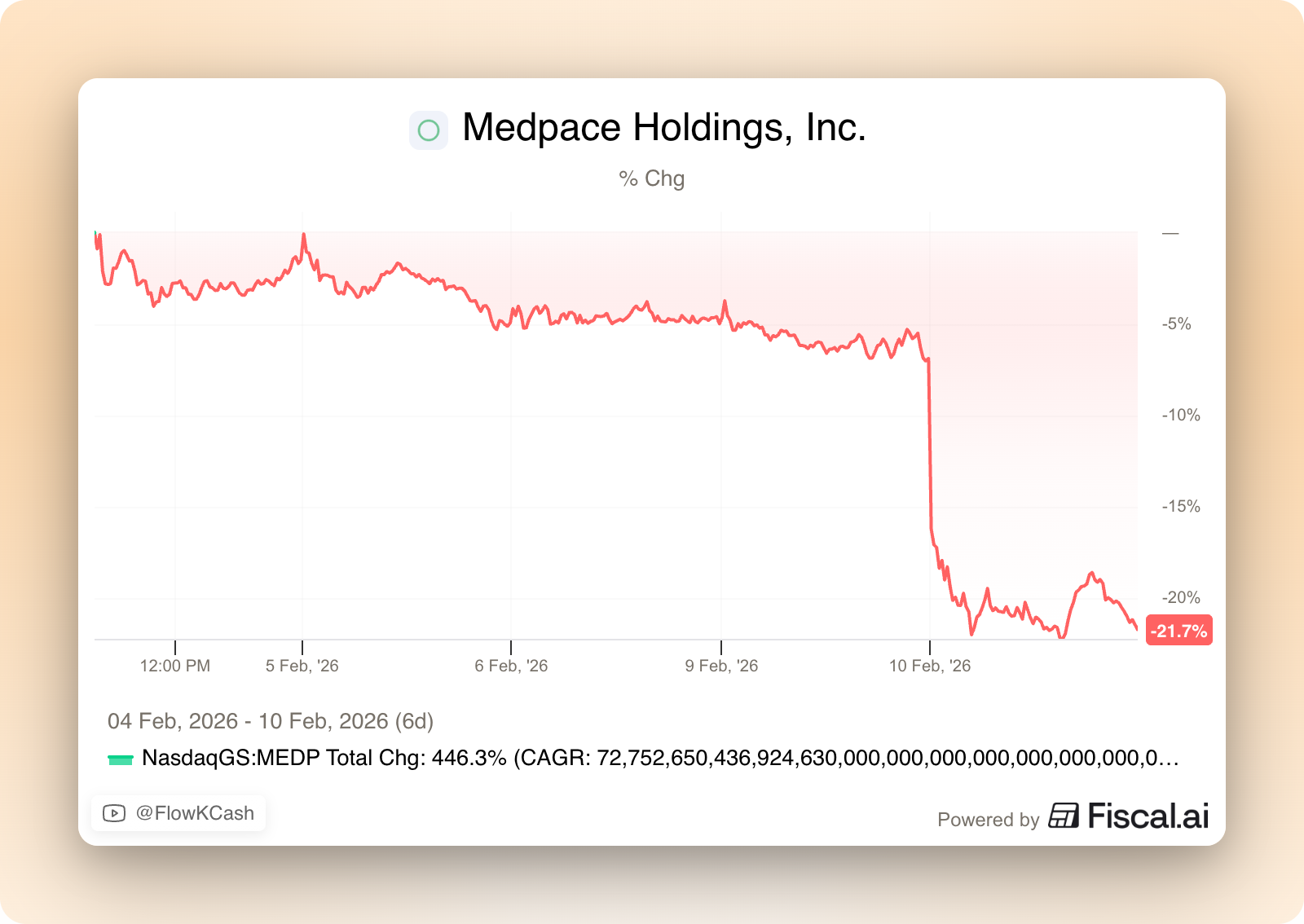

Medpace reported great earnings on Monday, but the market did not appear to like these much:

I can’t entirely blame the market because management significantly downplayed the earnings. I have my theory as to why, but I’ll discuss that later. Before that, let’s take a look at the numbers.

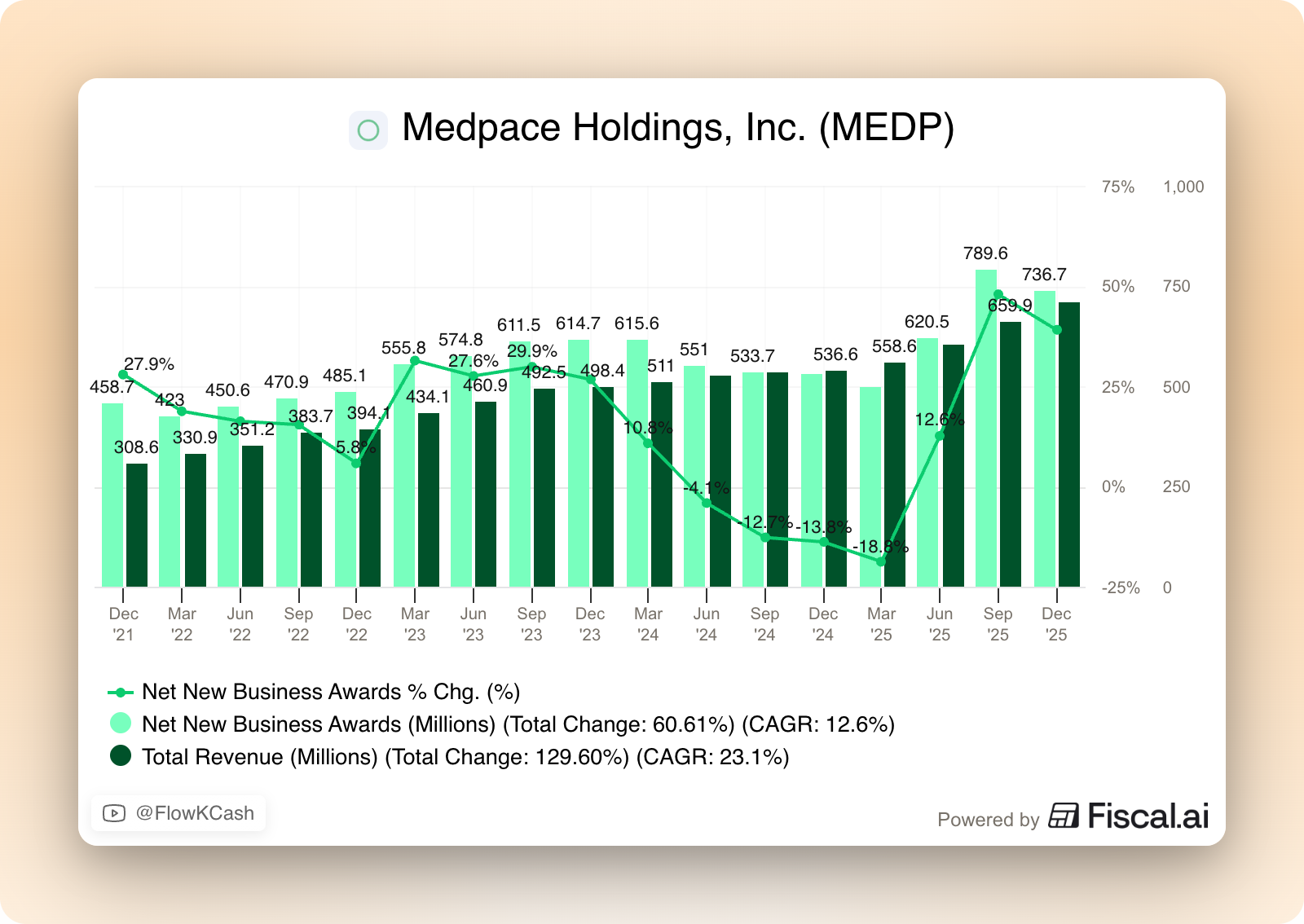

Medpace’s headline growth numbers are simply spectacular and significantly beat the market’s estimates. Despite August claiming (literally in the first quote of the call) that cancellations were “the highest they’ve been in over a year”, net new awards (+39% YoY) grew ahead of revenue (+32% YoY) to result in a slightly positive book to bill. I don’t want to imagine what net new awards growth would’ve been without an elevated level of cancellations (August didn’t want to tell us either!), but I mean, the trajectory here seems pretty healthy after the 2024 “setback:”

August did claim that, besides cancellations taking them by surprise, the business environment is good and he doesn’t expect the current level of cancellations to recurr throughout the year:

I see no reason to expect the higher level of cancellations to continue, but did not anticipate the spike in Q4. Only time will tell. Good opportunities continue to present themselves, and I rate the overall business environment as adequate and headed in the right direction.

Margins compressed in 2025 but not for the reason I would’ve expected. Note that in my Medpace report I wrote that I expected productivity improvements to plateau (i.e., analogous to claiming that margins would compress), but management attributed the margin decline to business mix. They’ve had more metabolic trials in 2025 and these have a higher percentage of pass through costs, and therefore, lower margins.

Full year EBITDA margin was 22% compared to 22.8% in the prior year. EBITDA margins were impacted by higher reimbursable cost activity driven by therapeutic mix.

Surprisingly, there were good news on the productivity front due to higher retention. One of the bear cases that Medpace has typically had is that it’s a “terrible place to work.” I’ve heard opinions from both sides: some people claim that it’s the jungle, whereas others claim that its a place where you can make a lot of money if you work hard. Nothing new considering this is akin to a consulting business. High retention seems to be some kind of narrative violation…

As Jesse mentioned, from a hiring perspective, we expect to be in the mid to high single digits, which is lower than the expectation on revenue growth. And so what’s driving that is just continued expectation that we continue to see good retention throughout 2026, which enables the productivity that we’ve seen throughout 2025 and exiting 2024. And so it enables us to hire higher, but at a slower rate.

This is a tailwind for margins because you don’t need to continuously train people if you are able to retain your existing staff.

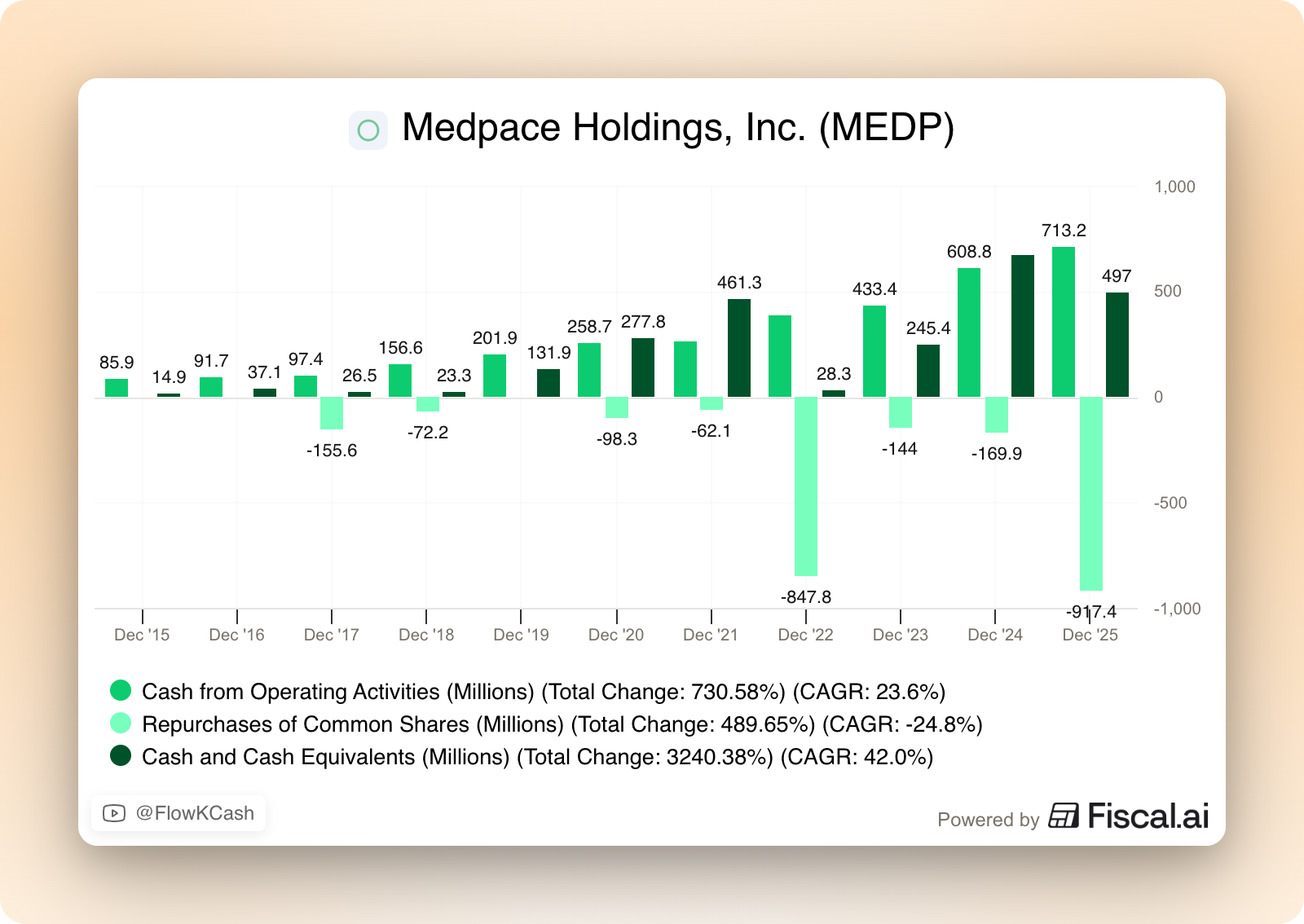

It wasl also a very strong year year in terms of cash flows for Medpace. The company generated more than $700 million in Operating Cash Flow in 2025 which, for context, is around 7% of the market cap the company began with at the start of the year. This cash flow, together with the existing cash position, allowed the company to repurchase $900 million worth of shares (opportunistically) and end the year with around $500 million in cash.

One of the beauties of Medpace’s model is that it enjoys negative working capital (customers pay first and receive the services later). This cash generation capacity married with good and opportunistic capital allocation results in great outcomes over the long term and I don’t expect it to be different in the future.

The outlook and management’s plan (?)

The outlook (together with the comment on cancellations) was likely what the market did not like. Medpace guided for a significant growth deceleration in 2026 (midpoint of 11% growth YoY) and you know what happens in this market when you don’t accelerate your top line, right? EBITDA margins are expected to expand slightly, but why would management be so conservative with top line growth when they exited 2025 growing 30%+ and the business environment is moving “in the right direction”? I believe there are two reasons behind their conservativeness, one inherent to the business, and one that probably is part of management’s plan.

The one that’s inherent to the business is visibility, or the lack thereof. Medpace has no way of knowing if a clinical trial will start in Q3 this year, Q1 next year, or maybe if it will be cancelled (cancellations and timing tend to be the unknown variables). This means that there’s poor visibility early in the year, which evidently funnels into conservativeness. I mean, management began last year (2025) with a revenue growth guidance between 0% and 4.8%. The end result, for context, was 20%. I must say this has not always been the case, but the differential in 2025 was striking and it allowed…

Management to repurchase a significant chunk of shares on the cheap

For the stock to perform well post de-risked expectations

The first of these takes me to the next point: I believe management is willingly downplaying earnings. I mean, who starts an earnings call where they grew revenue 32% and net new awards 39% in the following way? (This is literally August Troendle’s first quote!)

Good day, everyone. Cancellations were elevated again in Q4. Backlog cancellations, in absolute and percent terms, were the highest they’ve been in over a year. This resulted in a lower than anticipated net book-to-bill ratio of 1.04.

I believe that management is well aware that the stock was not cheap (for one, this management team knows when their stock is expensive/cheap) and they need something to do with the cash. Medpace ended the year with around $500 million in cash and no debt. To this we must add the cash that the business will generate throughout the year (last year it generated $700 million), which means that management will have north of $1 billion to allocate this year. So, what can Medpace do with this cash? There’s only one option…

Dividends: Medpace doesn’t pay dividends

M&A: Medpace doesn’t normally acquire other businesses and I highly doubt they would do any transformational acquisition

Repurchase stock: Medpace has done this in the past

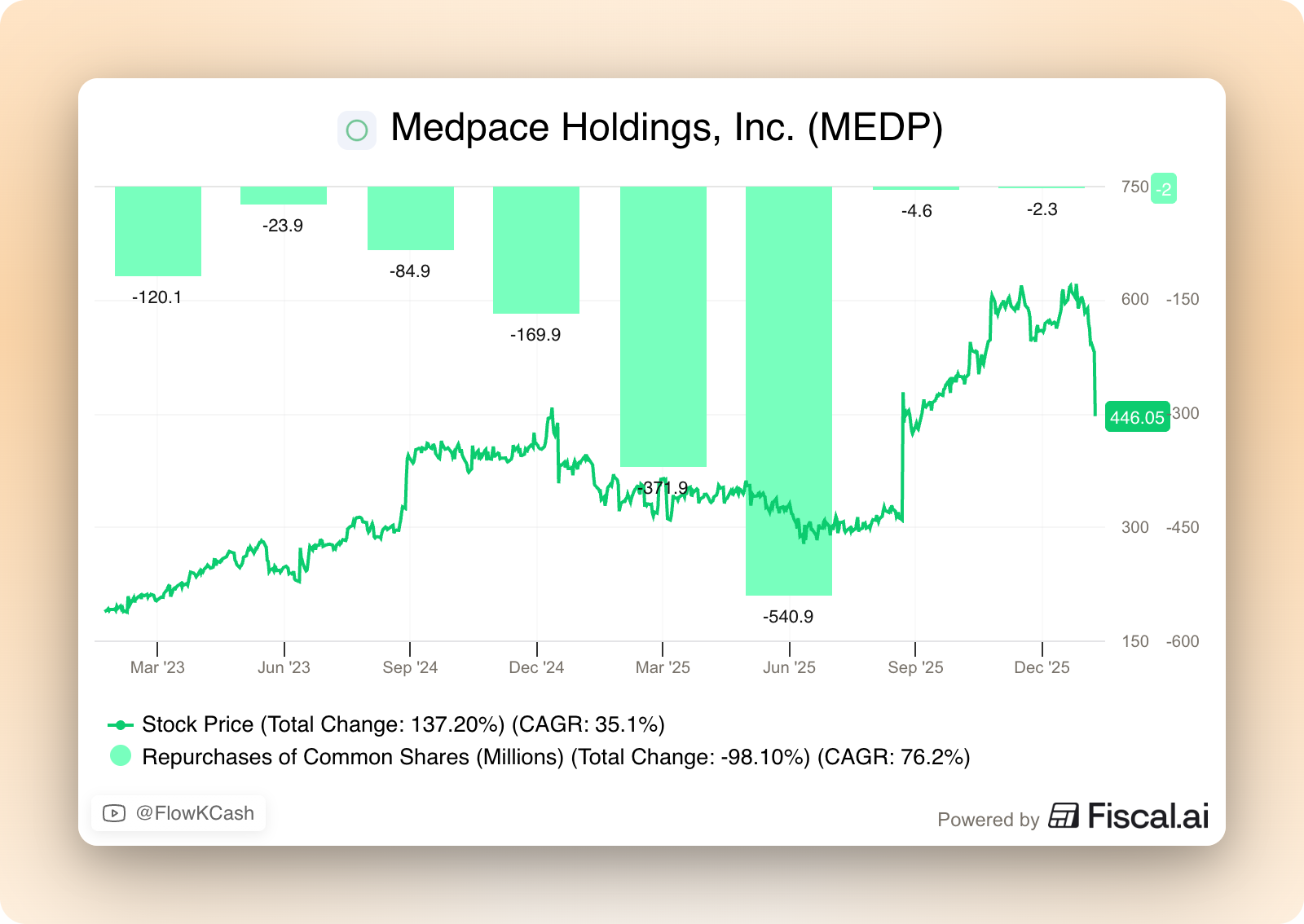

The only virtually available option to Medpace to use its cash is to repurchase stock, but this is not the kind of management team that repurchases stock at any time; they do so opportunistically. In fact, buybacks have completely dried up during the current run (as they should’ve):

My feeling is that August wants a lower stock price to repurchase shares with the available cash. Of course, he took advantage of several excuses to be able to do so. First, the lack of visibility (normal). Secondly, the higher than usual cancellations. And lastly, he got a question on AI to which he answered rather cryptically:

I think it’s too early to know what kind of changes. I do think that they will occur slowly. I would not anticipate really any productivity advantage, overall net advantage to AI applications in 2026. And I think that’s not because we’re not rolling out and doing a lot of things in AI. It’s that I think the investment is going to at least equal the benefits seen in this first year of kind of rolling out applications.

Where this goes in terms of how much productivity enhancement there is in the long term and what that means to us, I mean, I do think that the productivity advances are going to be to the benefit apart, it’s going to be rent to the providers of the models, etc., but are going to be benefits to clients. And what that means in terms of encouraging more development, etc. But overall, you’d think on the surface of it, it’s a net negative to a service company that makes money by providing staff to perform work that is now made more efficient.

But I think that the timing of this, it’s going to take years. Just what that means, what the opportunities for us are, are difficult to see. I don’t really think we have, you’d say, barriers to prevent yeah, I mean, we’re hoping to use AI in a lot of applications. We hope it does improve our productivity. And that means potentially, in the long run, fewer staff than you’d otherwise have. And that means a little bit less revenue than you would have otherwise had, at least net revenue.

If someone would’ve told me this story for any other management team, I would’ve probably called them crazy, but I mean, it’s August Troendle, he already did it last year! Just in case you don’t remember, management used pretty much all the cash available to repurchase shares when they were out of favor. They did this just before telling the market that growth was actually going to be substantially higher. I may be hallucinating (like an LLM) thinking something similar is going to happen this year, but everything adds up.

The last unknown variable is whether the stock is cheap after the post earnings drop. Let’s take a look at the valuation.