The rational long-term strategy (NOTW#88)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

US indices had a great week, driven by (supposedly) positive news flow from Iran. I discuss why remaining fully invested is arguably the more sensible long-term choice and share why it seems like the trend between semiconductors and software seems to have changed somewhat (can both go up at the same time?).

Without further ado, let’s get on with it.

Articles of the week

I published two articles this week. The first one was Hermes’ Q1 2026 earnings digest.

Hermes’ strange Q1 2026

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

The company reported a strange quarter (for Hermes’ standards) that requires significant context. It’s arguably the first time in a while that a quarter was not completely under management’s control.

The second article of the week was ASML’s earnings digest.

Derisking the thesis

Despite the adverse market reaction, ASML reported good earnings on Wednesday. We need, however, some context to understand the market reaction. First, ASML’s performance over the past year has been exceptional and it’s now hovering around ATHs (i.e., the stock’s performance has been very healthy):

The company reported again a very good quarter, not necessarily because quarterly numbers were good (which they were), but because the go-forward indicators look as good as they’ve ever had. I explain what I think about the 2030 guide and what this means for the valuation.

Without further ado, let’s see what the markets did this week.

Market Overview

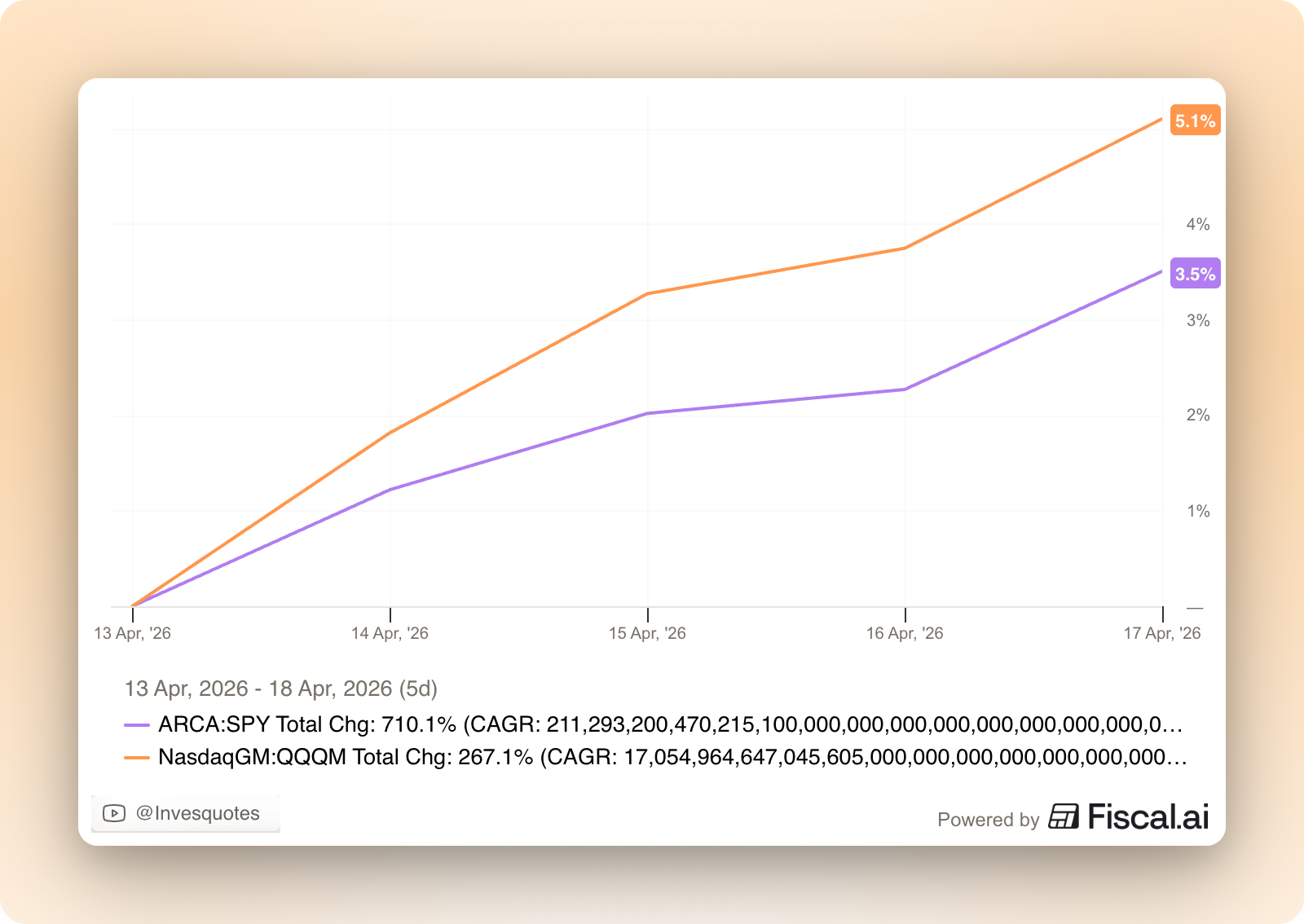

The indices had a great week due to the “positive” news flow from Iran. The S&P 500 was up more than 3% whereas the Nasdaq was up more than 5%:

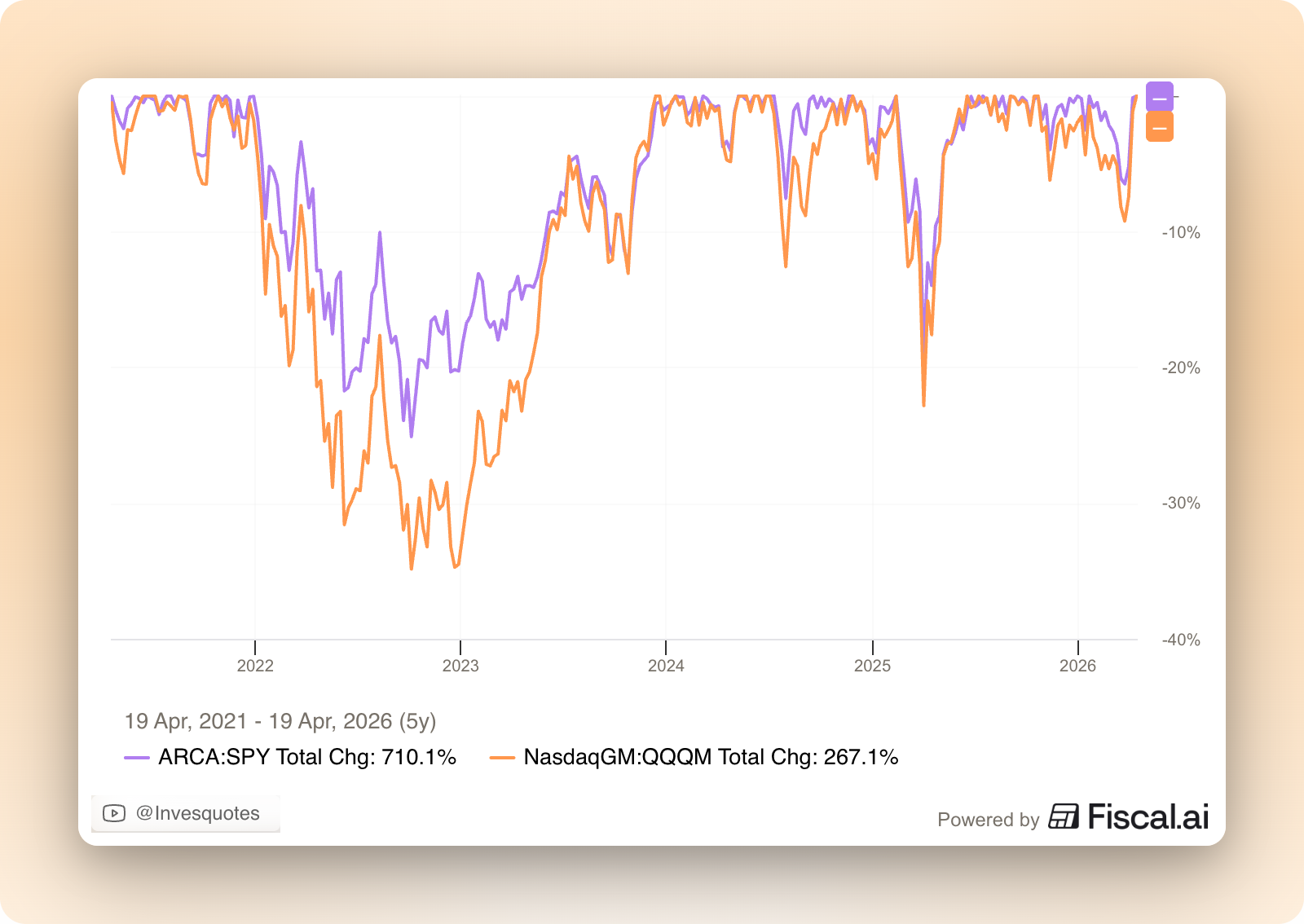

Not long ago, I was discussing in the NOTW how both indices were close to (or even suffering) a correction, but two weeks was all we needed for indices to go climb to ATHs:

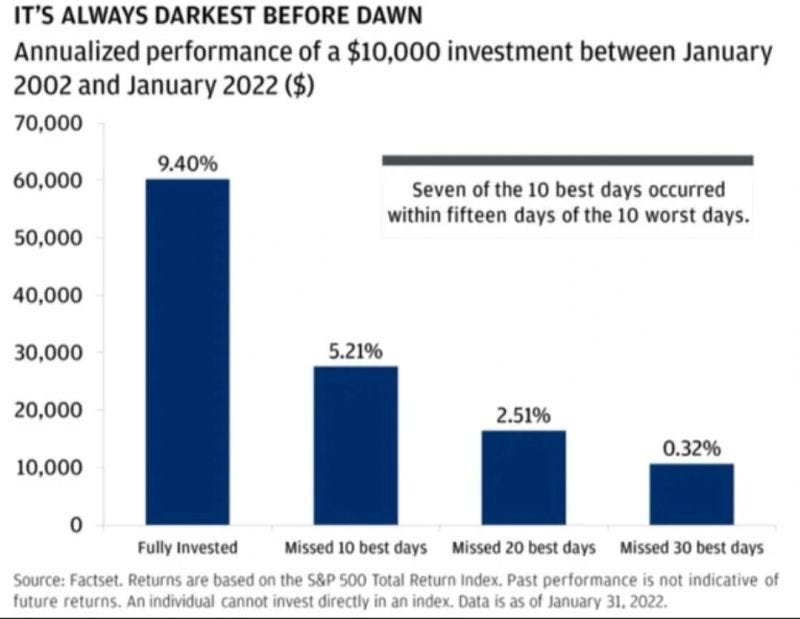

There’s a lesson here somewhere. If one is in full cash waiting to time the market, they might end up losing on quite a bit of the upside just because the upside can happen very fast (markets tend to take the elevator both up and down). There’s a relatively well-known chart which shows that the impact of missing the best days in the market can be terrible over the long term:

Some people will say that missing the worst days would also result in a much better return than remaining fully invested. While this is mathematically true, the only (but not minor) caveat is that remaining fully invested requires no supernatural forecasting ability, while missing only the worst days does require this superpower (it’s something that 99% of the population can’t do accurately and recurringly). So, what I get from this is that:

Missing the best days can be very damaging for long term returns

Being able to forecast the worst days with accuracy many times in a row is pretty much impossible

So what’s the conclusion? Remaining fully invested seems like the rational choice over the long term. If anything we are seeing this is the case time and time again with every drop. Of course, during every market cycle you’ll see people that have forecasted it correctly, but the only “problem” or “flaw” is that these people are rarely the same people that forecasted it right the last time around (weird, right?).

The industry map was coherent with things (supposedly) getting better in the Hormuz Strait, pretty much everything was up except energy and materials:

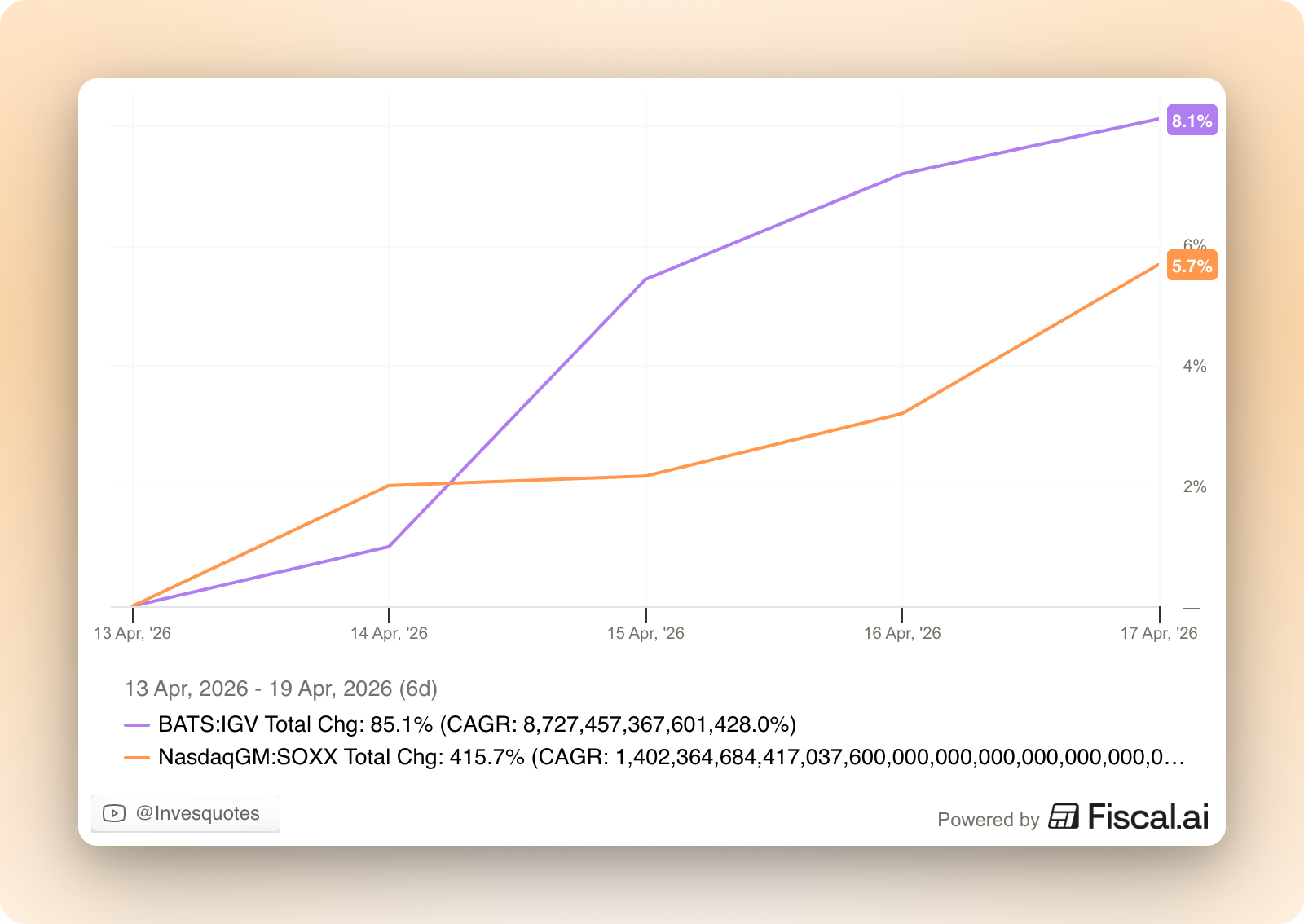

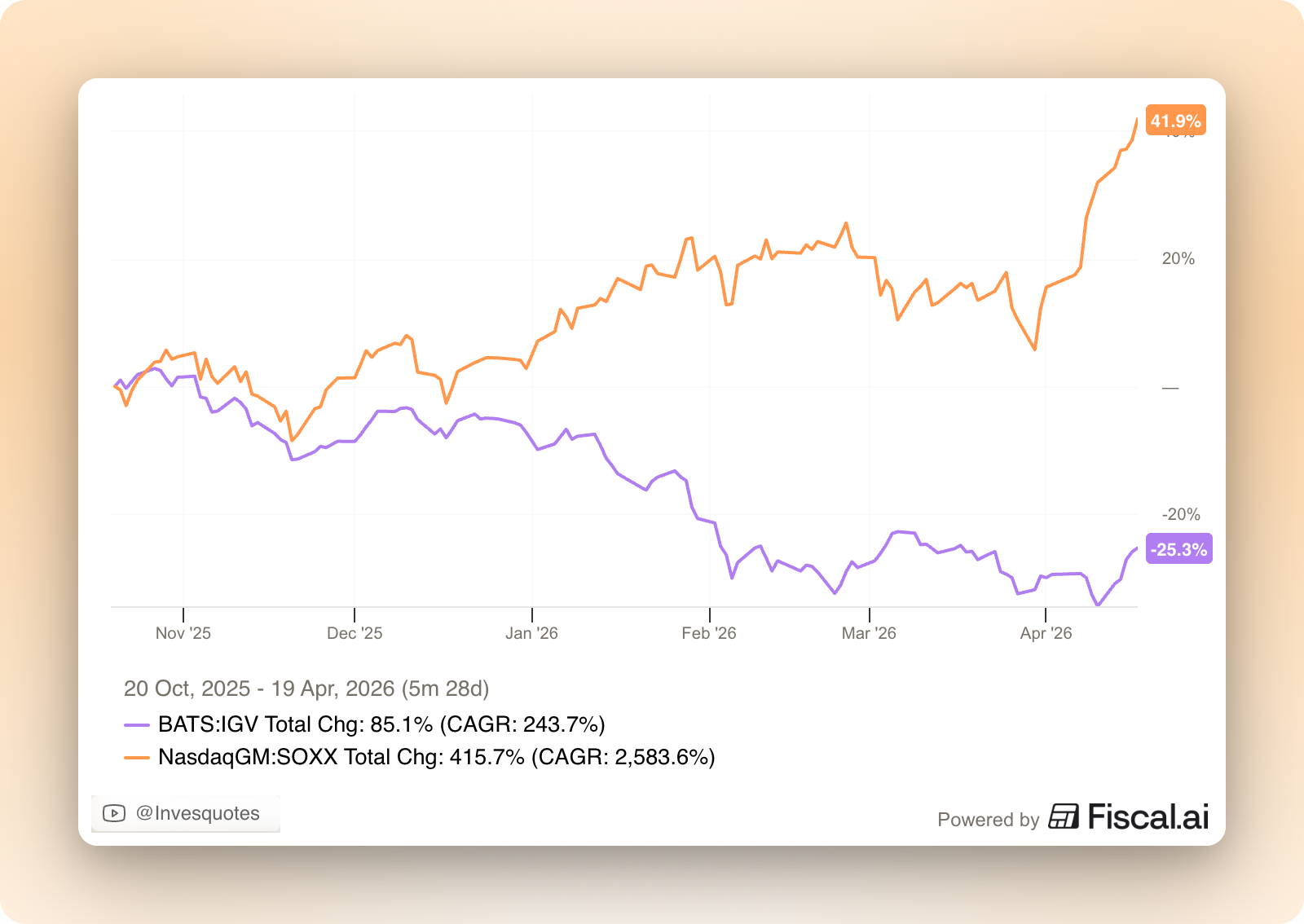

It was a very interesting week because both software and semiconductors were up quite a bit:

I say this is interesting because we’ve become used to seeing these two “factors” move against each other. If the “AI trade” was doing well then you’d see semis up and software down (due to AI-disruption fears). The opposite happened when the “AI trade” took a breather. Both things seem to be moving lately in the same direction (which might or might not have to do with the fact that everything is going up):

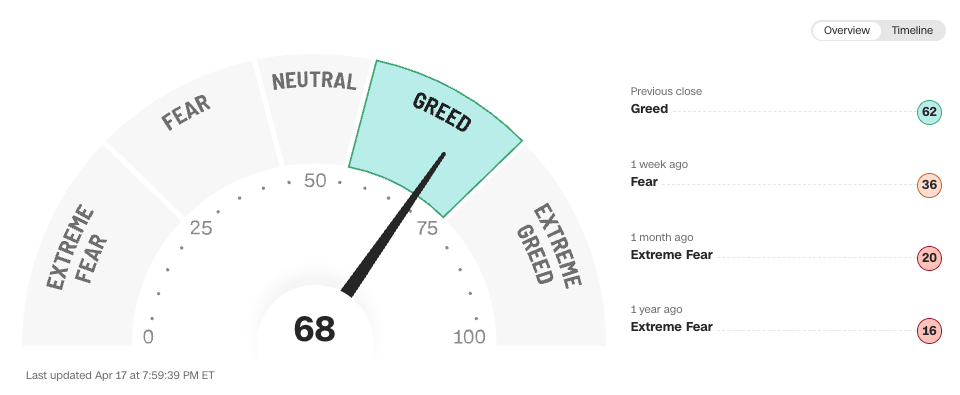

The fear and greed index improved notably and is already in greed territory:

If there’s one thing to take away from this is that sentiment changes very fast and that it’s always darkest before dawn (although I don’t think it got really dark, tbh).