Derisking the thesis

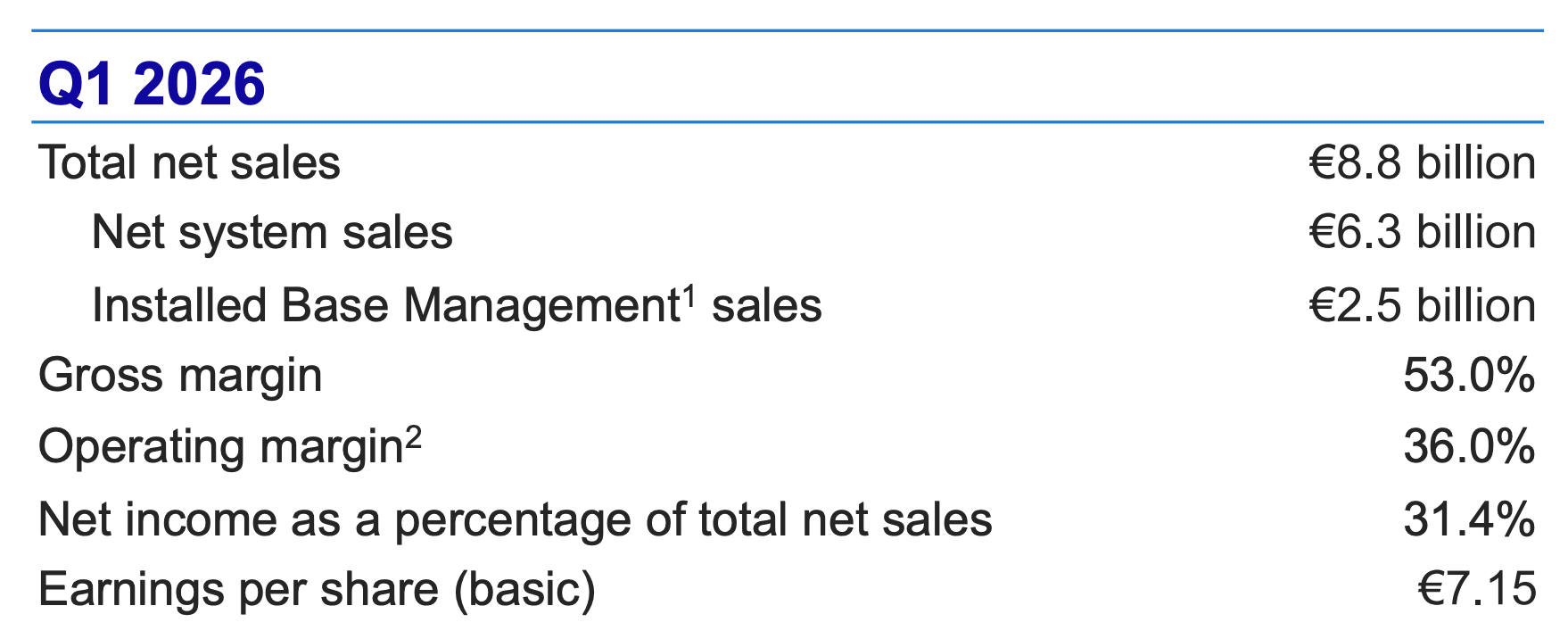

ASML’s Q1 2026

Despite the adverse market reaction, ASML reported good earnings on Wednesday. We need, however, some context to understand the market reaction. First, ASML’s performance over the past year has been exceptional and it’s now hovering around ATHs (i.e., the stock’s performance has been very healthy):

Secondly, ASML typically reports earnings just before its main customers (TSMC, Intel, Samsung, and the memory players) do. Even though ASML shares some context around the demand environment, the market typically waits for its main customers to share their Capex plans. TSMC, for example, reiterated today that they expect Capex to be “significantly higher” in the coming three years than it was over the past three years (around $100 billion). A portion of this money will flow directly to ASML and confirms the company’s qualitative comments.

Customer comments are now more important than ever because ASML has stopped sharing quarterly order numbers (now that they would probably be beating the most optimistic projections, I know).

I’ll not focus much on the quarterly numbers and you should know why if you’ve read my past research on ASML (all of which is available here): quarterly numbers are mostly noise, more so now without leading indicators. The reason is that ASML’s revenue is getting increasingly skewed toward higher ASP products (EUV) so any minor delay/revenue recognition of an EUV order can make the quarterly numbers move significantly without a fundamental meaning. The only highlight I’d make from the quarterly numbers is that (once again) gross margins topped management’s expectations due to (once again) higher than expected IBM sales:

Seeing IBM (Installed Based Management) sales outperform management’s expectations so recurrently has two potential readings, with both probably being true simultaneously:

Management is being conservative with the IBM business: I believe this is true and that it has implications for the 2030 guide

Demand still outpaces supply and therefore customers resort to upgrades to try to meet the heightened demand

Pretty much the entire earnings call was focused across three main topics, namely:

The 2026 and 2030 guides

Capacity to meet future demand

Technology development

Let’s take a brief look at these.

1. The 2026 and 2030 guides

Management raised the midpoint of its 2026 revenue guide (interesting considering it’s just Q1) while leaving the range for gross margin unchanged. ASML now expects 2026 sales of €38 billion (midpoint) which would result in 16% year over year growth. More importantly, this is a 4% guidance raise from the expectations they had just a quarter ago (€36,5 billion midpoint) and is also ahead of the market’s expectations. So, what changed? Management attributed (interestingly) the raised guide to the immersion DUV franchise ex-China. They expected the non-EUV business to be flat this year, but now they expect it to grow.

They also shared some qualitative comments around demand:

In the past months, our customers have increased their expected short and medium-term demand for our products. ASML’s order intake continues to be very strong as a result.

The most interesting part (in my view) of this quote is the “medium-term demand” part. It seems like ASML is increasingly gaining visibility on its 2030 guide and that they might end up closer to the high end. They refused to change the 2030 guide BUT they did argue that when they set these objectives they did not believe DRAM would be so strong. This potentially means they’ll come up with a “raise” guide or maybe more confidence on the high end, but this is something we’ll only know in next year’s CMD.

Seeing ASML raise the 2030 guide in 2027 (3 years in advance) would be great, but I believe that what we should take away from the above is that the current 2030 guide seems pretty achievable and that ASML is likely trending towards its high end (I’ll discuss more about this in the valuation section).

The strong demand is ultimately being driven by the AI infrastructure buildout, where demand remains above capacity. ASML flagged that both logic and memory customers (especially the latter) have told them that they expect the shortage to persist beyond 2026 (which honestly doesn’t bode well for Nintendo but already seems to be discounted to an extent in its stock price). For more context on Nintendo’s memory woes, you can read this article).

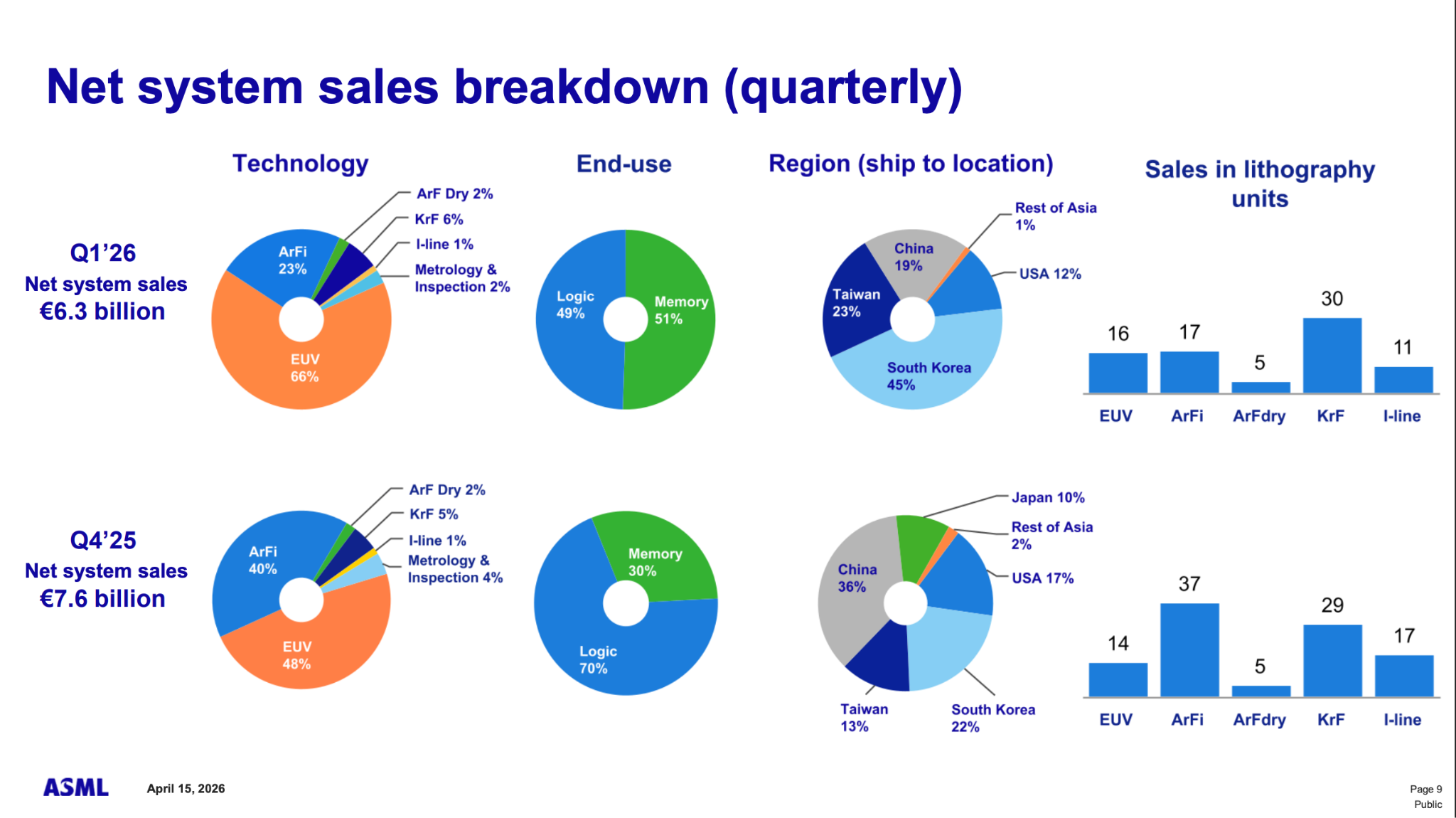

The AI infrastructure buildout and the memory shortage are somewhat shifting ASML’s geographic and product distribution. EUV sales are now account for 2/3rds of total sales, memory for half, and South Korea for a little less than half:

Despite being pretty much sold out, ASML claims that they are not the bottleneck. It seems like the current bottleneck revolves around energy and memory producers, with their stocks reflecting this situation. Note that, at first, many claimed that this time around memory players would not expand capacity and would milk customers to oblivion. Even though this seemed to be the case during the first few months, memory players eventually decided to expand capacity (benefiting semicap players). It’s interesting because even though ASML holds arguably the strongest position in the semi supply chain, the company has a policy of not milking customers:

Now, in our model of pricing, as you know, our model of pricing is not based on the squeeze that our customers find themselves in. That’s not the way we do business. The way we do business is that we look at the value that we provide to our customers, generation on generation, tool on tool, and we take our fair share in that. You might say, in the current climate, can’t you squeeze out a little bit more? I understand that, but it’s also true that when the market goes down a little bit, and the customers are going through more difficult times, that it also pays these fees. Fundamentally, we believe that the model that we have is a fair model.

This, imho, is one of the pillars of the company’s moat. Not only are customers more likely to share the roadmaps with ASML (therefore giving it an “unfair” advantage over competitors) but it also makes them less likely to pursue other alternative technologies (should these present themselves).

2. Capacity to meet future demand

ASML’s management rightly pointed out that capacity should be looked at from two angles: units and productivity/throughput. Customers can meet their increasing wph (wafer per hour) needs either by buying more units, upgrading existing units to gain productivity, or both. ASML is focused on…

Being able to provide an increasing number of units going forward (capacity investments)

Making said units more productive (technology investments)

Let’s start with (a). Management shared that they expect to be able to produce 60 low-NA EUV units this year and at least 80 units next year. ASML shipped around 43-45 low-NA EUV units in 2025, so they expect to increase capacity by 25% in 2026 and an additional 33% in 2027. Recall that when ASML’s stock was at the lows, everyone was worried about demand. With ASML at ATHs, everyone started to worry about the company’s capacity to meet increasing demand (funny how this works). ASML’s developments in terms of its ability to ship units not only makes the company able to potentially meet the increased demand but also derisks somewhat the 2030 guide.

Now let’s turn to point (b) in the following section.

3. Technology development

There was a lot of news regarding technology, but let me kick this section off talking about capacity. Management shared two highlights regarding productivity improvements. First, they increased the output of the NXE:3800 from 220wph to 230 wph. Secondly, they announced that the 1,000 watt source will enable them to extend the use of low-NA EUV for many years as it will be capable of a throughput of 330 wph. These productivity improvements have several implications:

They allow ASML to meet industry capacity without needing to focus too much on units (evidently more productive tools come with a higher price tag and therefore it’s very profitable business for ASML)

They protect ASML from future competition. This business is not about how much an “equivalent” system costs but about what “equivalence” means. It’s not enough to have a system that can do the same, it must need to be able to do the same at a similar pace. Increasing productivity can only done through data, and to do so you need an installed base, so it becomes the chicken and egg problem

We should not forget that ASP (average selling price) correlates strongly with increased throughput, so more productivity means higher prices and higher prices likely translate into improved profitability for ASML.

They also expect high-NA to be a long lasting system:

Also, at the conference, we saw customers presenting several strong papers highlighting their progress with high-NA. These presentations demonstrated use cases in both logic and DRAM, in which a single ion exposure can replace complex multi-patterning processes that today require 3 or 4 low NA exposures. For some critical layers, High NA can reduce the number of process steps by a factor of ten. The progress being made throughout the ecosystem, especially with resist, allows us to target lines and pitches of 80 nanometers for logic and contact pitches below 28 nanometers for DRAM. This means that high-NA can support single exports for at least three nodes in logic and DRAM.

All in all, a very good quarter from ASML, but is it still a good risk/reward?