Hermes’ strange Q1 2026

Secular or temporary?

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

I’ll publish an ASML update tomorrow and an article about a relatively unknown company early next week.

Join today:

A couple of weeks ago, I published an article about Hermes titled “The Stock is down 40%, the business isn’t” sharing some thoughts around the current state of the luxury industry, Hermes’ main bear case, and the stock’s valuation (you can also read my in-depth report here).

The stock rose somewhat from the price it was trading at when I published that article but is “cratering” today (-9% as of the time of this writing) after reporting relatively weak Q1 2026 earnings. Now, “cratering” might be a strong word when a stock is down less than 10% (I’ve definitely seen worse), but it’s undeniable that this is a very rare occurrence for Hermes: over the last 20 years, the stock has only suffered a comparable one-day drop (the pandemic). The stock price is at a somewhat similar level today than it was when I published that article, so I would refer you back to it if you want to know what I think about the valuation (my thoughts have not really changed).

The goal of this article is to share a brief note about Hermes’ Q1 earnings, sharing the most important details, what I thought about this, and what the market might be worried about.

As you may know, the war in Iran promised to be disruptive for luxury companies, which would be theoretically impacted across two fronts:

Asian tourist flows to Europe: fewer flights and more expensive

The disruption in the Middle East itself: inability to operate normally

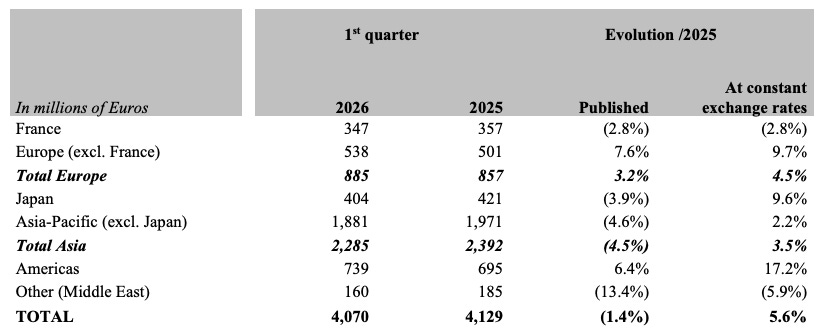

Hermes’ business was disrupted by both this quarter. Despite the group’s organic growth of 6% in Q1 (not bad considering China is also subdued and suffering tough comps), Hermes reported unusual drops in France (-3%) and the Middle East/Other (-6%):

Management shared during the call certain details to help contextualize these drops:

Owned stores’ sales growth was 7% but sales at concession stores (airports/the middle east) dropped 7%. This tells us that the conflict in Iran mainly impacted the Middle East region and tourist flows. France was particularly impacted by the conflict because sales to concession stores and airports are typically bundled in this geography. Sales in France would’ve dropped “only” 1% ignoring these

Sales grew double digits in France outside the main tourist destination (Paris), so management can “confidently” claim that the drop excluding concession store sales was driven by fewer tourists

Sales were growing double digits in January/February in the Middle East but ended up dropping significantly in March. I.e., it does seem that all the weakness was caused by the conflict

Overall, the impact of the war in Iran was estimated by management to be 150 basis points to total group growth. This means that, excluding the conflict, sales would’ve grown more than 7%. This would’ve been pretty acceptable considering the state of the industry and the fact that two other growth levers that should accelerate in the quarters ahead:

Store openings and remodels: Q1 was a particularly soft quarter in this front, but management expects store openings and remodels to pick up in the coming quarters and to end up contributing 1% to total yearly growth

Leather growth: leather grew 9% in Q1 but management maintained its 12% YoY growth guide for 2026. They explicitly claimed that leather should accelerate throughout the year and that it’s lumpy due to its artisanal nature

So, assuming these levers play out and that the impact of the conflict in the Middle East eases somewhat through the remainder of the year (management claimed that April showed improvement due to stores being open again), then we could think that Q1’s 5.6% organic growth might be a trough. Management also claimed that, excluding the Middle East, trends were improving in March, which bodes well for the overall health of the business. Part of me wants to believe this will be the case, but at the same time I can understand why there might be skepticism around how the next few quarters will look like (which was likely represented in the stock price drop).

The conflict in Iran began at the end of February/beginning of March. This means that it “only” impacted one month of Hermes’ Q1. This one month impact created a 3% drop in France, a 6% drop in the Middle East (with the rest of geographies growing at a good/great pace), and an overall headwind to group growth of 150 bps. We are currently only 15 days into Q2, but with the conflict in Iran ongoing, the market is likely worried about what the potential impact for Q2 numbers might be. Now, there are certain caveats to discuss here that should stop us from blindly extrapolating Q1 trends to Q2 (i.e., assuming that the conflict will be a 4.5% headwind to group growth in Q2).

First, it’s highly likely that the conflict in Q1 took management by surprise, leaving little options to react. This will not be the case for Q2 as the conflict is already “advanced” or at a more mature stage. Secondly, it’s likely that the early stages of the conflict are much more disruptive than the later stages, and there are reasons to believe we might be transitioning to the latter (recall that April already showed improvement compared to March). I highly doubt that the conflict in Iran will be as disruptive in Q2 as it was in Q1 (I don’t even expect the conflict to last the entire Q2) so directly extrapolating makes little sense in my view although I can understand why one would be inclined to do it. Now, this doesn’t mean that Hermes is out of the woods in Q2.

Management also gave some context around growth in the APAC region in Q1. The main highlight was that China grew despite facing tough comps (Chinese New Year in Q1 2025) and that trends are somewhat improving. So, what’s my take? Hermes is currently suffering several concurring headwinds:

A strong euro: note that this is excluded from the organic growth number I shared above but ultimately impacts organic growth because it reduces tourist flows (i.e., it becomes more expensive to buy luxury goods in Europe)

A weak China that seems to be recovering but is still not there yet

The conflict in the Middle East that shaved 1.5% off of quarterly growth in one month

Despite all of this, the company still managed to grow 6% organically, which is pretty impressive. I believe there are reasons to expect an acceleration in growth over the coming quarters (discussed above) but that this is also contingent on things outside of the company’s control (like the war in Iran). Do I think earnings were -14% worthy? No, but I shared what I think about the valuation in my most recent article, so I recommend reading that if you are interested.

Before ending the article, I wanted to say that these earnings have implications for Shift4’s Global Blue. Recall that Global Blue makes money when a tourist is eligible for a VAT deduction. Less tourists mean less transactions and therefore less revenue and profits for Global Blue. I don’t think this matters a lot seeing where Shift4 is trading, but worth having it in mind.

Have a great day,

Leandro

Thanks Leandro, another example of how the markets take a short term view of a long term company. A real war is waging - it’s no wonder even great businesses are affected somewhat. The underlying business remains first class. The global rich are getting richer and more numerous and Hermes make something unique and artisan in an otherwise mass production world. I hope for further price drops.

Great company and I'd love to own it.

But a PE in the high 30s with 7% growth is too expensive. Even accounting for their cash.

French budget deficit is unsustainable but they get riots when they try to reduce it. The temporary tax probably becomes permanent.

Until France goes back to a currency they can print.

And the EU has to breakup - 27 nations cannot agree on anything.

All this must happen, but I don't know when.

Theres probably a crisis/opportunity there sometime to buy good shares.