Incentives, incentives, incentives, and some pretty relevant news (NOTW#29)

Best Anchor Stocks has a partnership with Finchat (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

Both indices were significantly up this week after a slow start to the year. There was not too much relevant news on the macro front (besides the fact that inflation came in lower than expected), but there was plenty of relevant (and good) news for many companies in the Best Anchor Stock portfolio.

Without further ado, let’s get on with it.

Articles of the week

I published two articles this week. The first one discussed the (supposedly) terminal decline in the spirits industry. This topic is highly subjective, but I try to shed some light on recent evidence (objective evidence, not anecdotal).

Is Alcohol Consumption in Terminal Decline?

It’s no secret that alcohol-related stocks have seen better days. After strong excitement during the post-pandemic drinking surge, the stocks of well-known spirits and beer brands are significantly o…

The second article of the week listed the books I read in 2024. The objective is to help you expand your library, and I highly encourage you to leave your favorite investment-related book in the comments so that I can expand mine.

Books of 2024

2024 was a productive year from a reading standpoint. I read 18 books last year, less than I would’ve liked (as always) but probably more than I expected to. I never start a year with a specific goal…

Market Overview

After a slow start to the year, both indices performed very well this week. Both the Nasdaq and the S&P 500 were up almost 3%:

We are in a time of annual recaps and I find it interesting how many fund managers are “adjusting” the returns of the leading indices to justify their returns. If you’ve read a couple of these letters, you might have noticed how these fund managers might write something like…”We outperformed the S&P 493” (which excludes the Mag 7). This is an interesting (but not very honest) way of looking at it because the opportunity cost for most people is not the S&P 493 but the S&P 500 (which includes the Mag 7). I wonder how their portfolios would’ve performed when ignoring their best performers. It’s also rather surprising how most of these fund managers despise adjusted metrics when it comes to accounting but use them freely when their performance is at stake.

We should not kid ourselves; most of these managers are perfectly aware that underperforming one year or a couple of years means nothing, so why can’t they simply say this? The answer, like in most investment-related matters, lies in incentives. Most fund managers are incentivized to increase their AUM (Assets Under Management), and they’ll do whatever it takes to do so. Many of their LPs (limited partners) lack the necessary patience, so they might leave if the fund suffers an “unjustifiably” underperforming year (i.e., no bueno).

I think this behavior also, to some extent, portrays quite a bit of ego. Making mistakes is fine in investing, in fact, investing is a place where making mistakes is not only fine but also inevitable and acceptable. Best of all, mistakes don’t kick you out of the game; you can do very well even after making several mistakes per year. The reason lies in the asymmetric nature of stock returns (unlimited upside with a capped downside). So, why continue trying to hide these? Incentives, incentives, incentives. This incentive structure reigns the industry and allows individual investors to have a good chance of faring better than professional managers. This advantage can be encompassed in two words: permanent capital. Many professional managers have to focus on two things: (1) finding a good opportunity, and (2) starting a position at the most optimal time. Individual investors with permanent capital can do very well just focusing on (1).

The industry map was pretty much green with the only two notable exceptions being Apple and some healthcare companies:

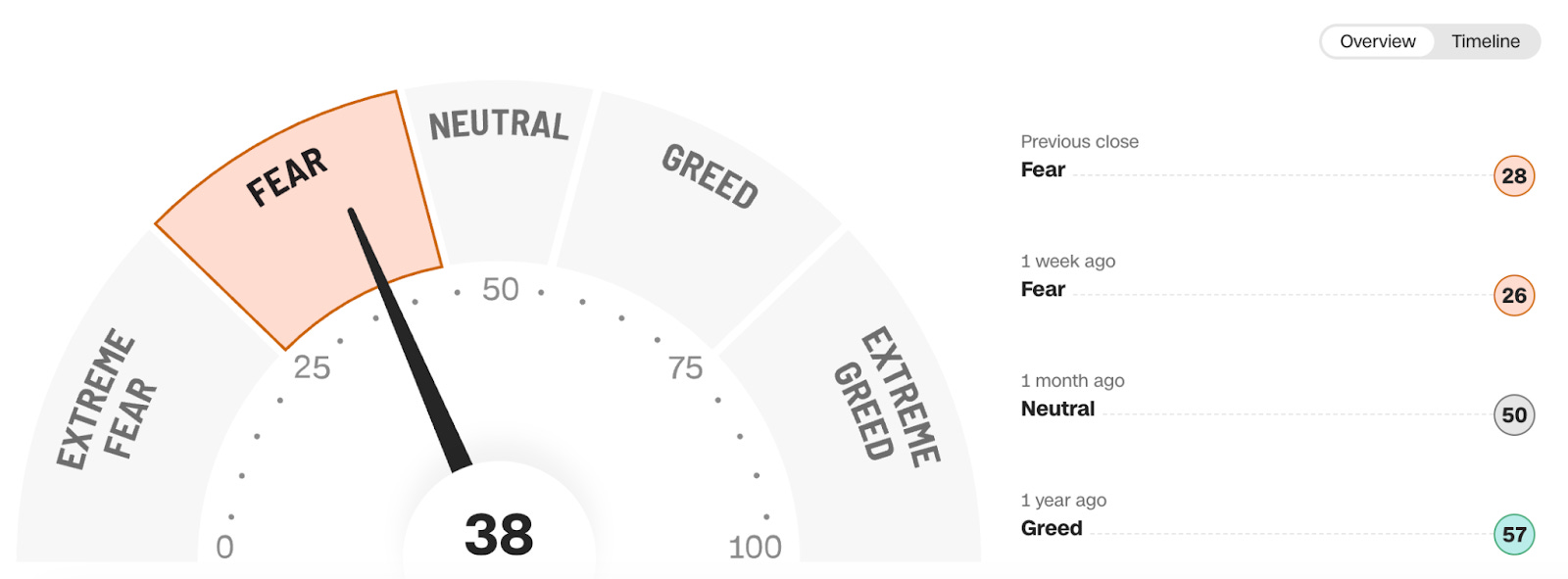

The fear and greed index started the week touching extreme fear but recovered quite significantly during the week:

The free content of this News of the week ends here, in the rest of the article I’ll share my purchases this week and the relevant news for the companies in my portfolio.