Earnings volatility, “specialists”, 13Fs, Amazon’s earnings, and positive news for ASML (NOTW#56)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

The indices were up again this week, and while I did not follow markets closely, I discussed three relevant topics in the market commentary:

Positioning and earnings season volatility

Specialists

13Fs

In the news section (reserved for paid subscribers), I also go over Amazon’s Q2 and some incrementally positive news for ASML.

Without further ado, let’s get on with it.

Articles of the week

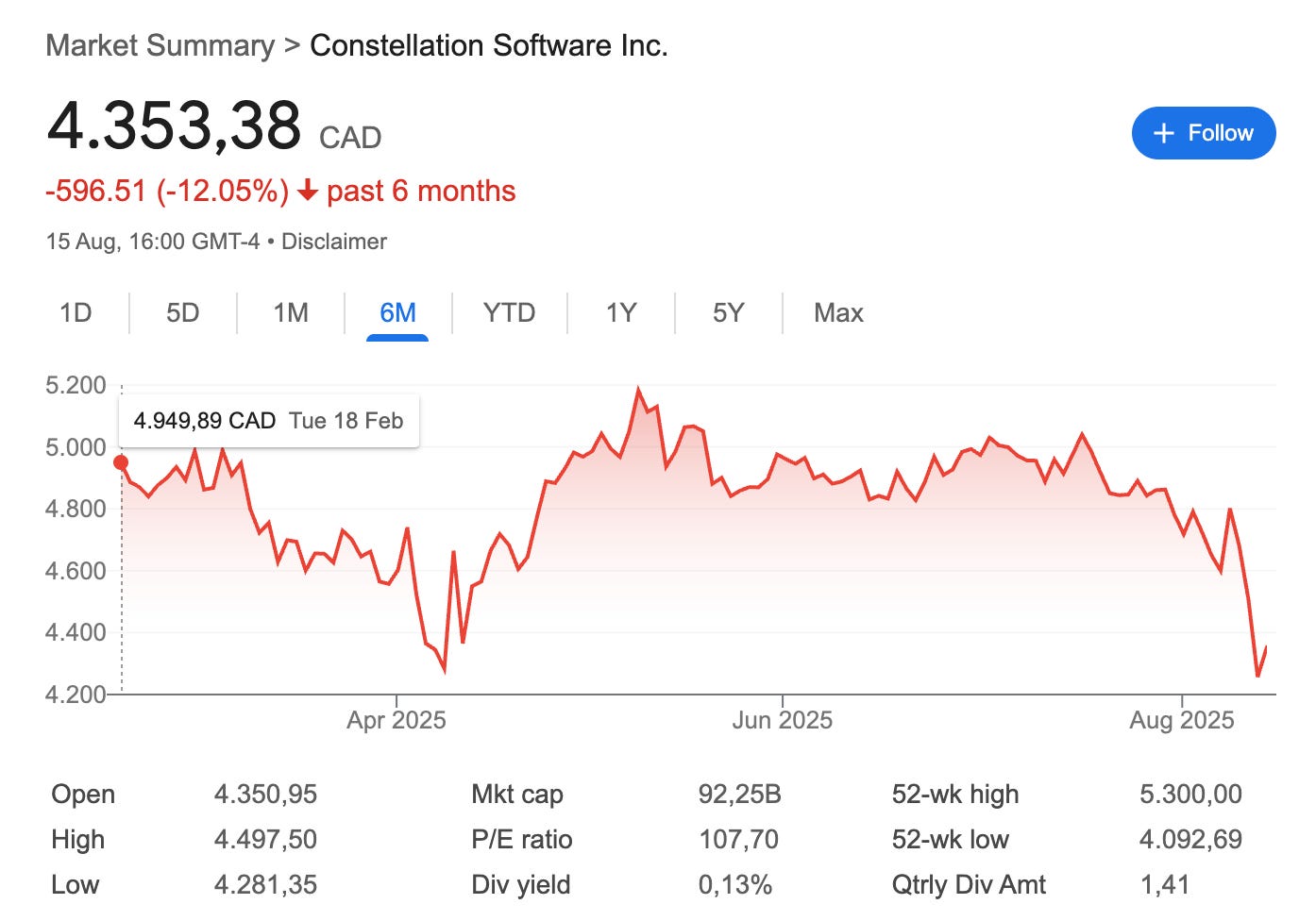

I published two articles this week, both earnings digests. The first one was Constellation’s Q2 earnings.

Hidden Value in a Liability

(Note that this article was written before the rise in Constellation’s stock today. This means that the valuation numbers might be a bit outdated although it should not change much of the big picture.)

The company reported solid earnings, both in organic growth and capital deployment (but especially the former). What might have happened here is that the narrative of “SaaS is dead due to AI” might have gotten hold of the stock. Constellation’s stock retested its April lows and was down almost 20% from its highs, something that doesn’t tend to happen often:

I think the narrative that AI will kill software vendors because everyone will insource software development makes little sense for HMS (Horizontal Market Software), but it makes even less sense for Vertical Market Software. I am not far from getting to a price that I would be willing to add to my position, but I am still not there yet.

The second article of the week was Deere’s earnings digest.

The Reason Behind the Drop

Deere reported earnings this week, but the market did not like them much. Despite a beat-beat quarter, Deere’s stock dropped significantly, maybe because the midpoint of the guide was somewhat lowered and the

The company reported solid earnings, but management sounded cautious about what 2026 might look like due to geopolitical uncertainties. The stock, however, remains close to ATHs.

Last week, I said that I would also bring an earnings digest on Amazon, but I did not. The reason is that quite a long time has passed since the company reported earnings and I don’t have much more to share than what you’ve probably already read. This said, I’ll share some brief thoughts on the earnings in the news of the week (reserved for paid subscribers).

Market Overview

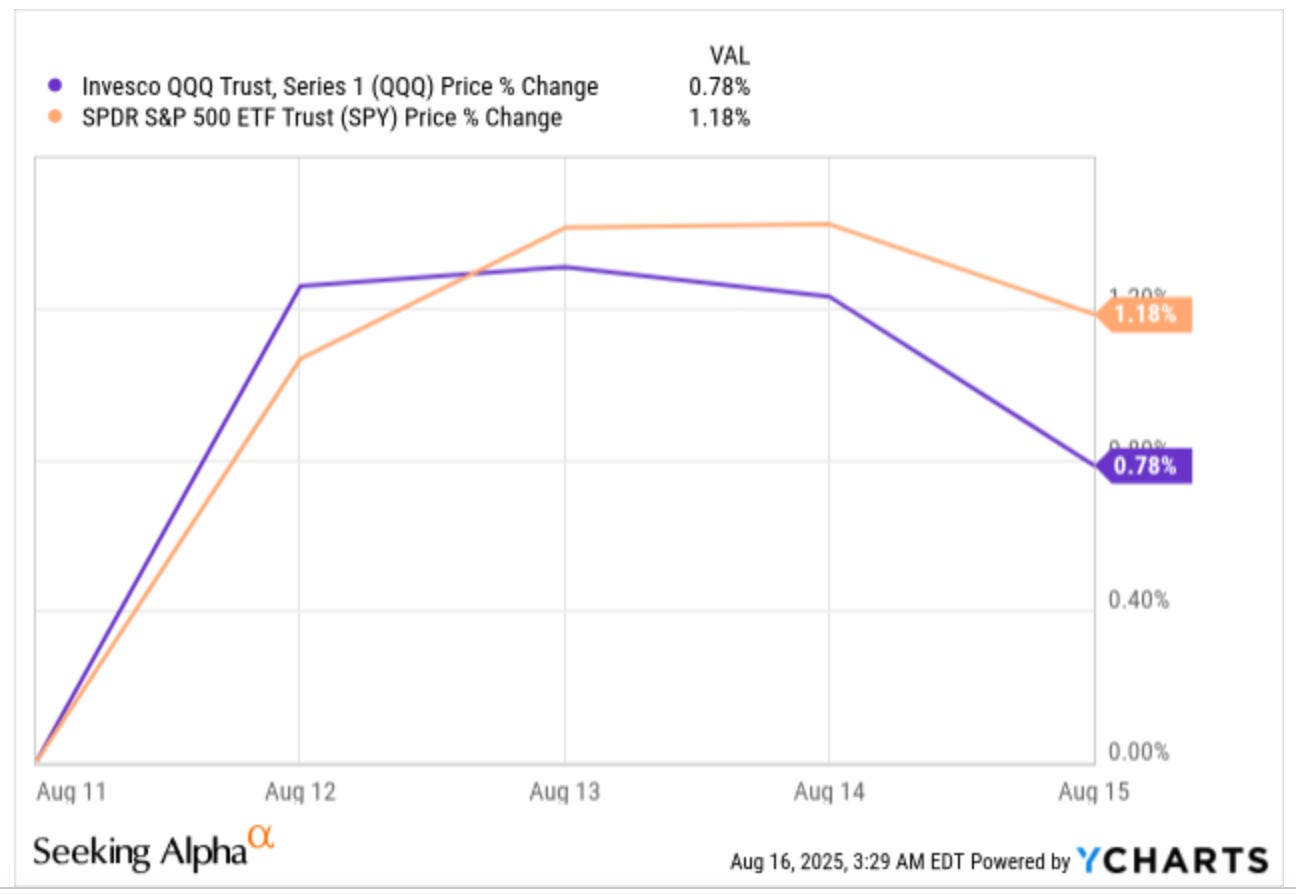

Both indices were up again this week:

I did not follow the markets closely this week because I was travelling with my family, so I might have missed some “relevant” news. This said, I wanted to touch on several topics here. The first one is the current earnings season. Even though I still have some earnings reports to go, I can already say that it has been a pretty hectic earnings season. Even though volatility has always been the norm in financial markets (especially during earnings season), I must say I have seen a notable shift this season. I “jokingly” tweeted the following the other day:

This makes me think that positioning into earnings has gotten to an extreme. What I mean by this is that a lot of money is positioned to “guess” earnings or to quickly jump or leave a position if earnings are not what one expected (purely momentum-based). While speculation around earnings is not new, it does seem to have reached an extreme. Let’s take a look at some examples. First, there’s Medpace (MEDP). A lot of people claimed that “alt data” showed that Medpace would report bad earnings, which is maybe why short interest skyrocketed before earnings. The alt data was a bit faulty because the earnings were better than expected, and the stock rose +50% in the following day. How’s that for an earnings reaction of a +$6 billion company?

Another notable case is AAON (AAON). The stock dropped 18% initially following “bad” earnings. Management later mentioned that most of the drop had been caused by problems around the implementation of a new ERP. After the market considered the bump to be temporary, the stock rose 42% in two days and breached new ATHs! While these moves might not make much sense, I do think they bring some important lessons. The main lesson is that there seems to be a lot of money trying to guess earnings (the famous pod shops). This results in something interesting: when something inflects, it’s going to get repriced very quickly, meaning that it might make sense to be early rather than late. I read this week the Q2 letter of Praetorian Capital, which echoed some similar comments:

Now, I genuinely wonder if the tables have turned. I know that this is very subjective, but I feel like top quality assets now get far cheaper than I could have ever previously imagined, but only when the next few quarters are expected to be poor. Meanwhile, when you look out a few years, you can see nothing but rainbows—except the active capital today does not have a timeline that extends that far.

Back in 2019, I realized that at the first sign of a positive inflection, there would be almost no change in the share price, as investors adopted a heavy dose of skepticism towards what could be a potential inflection—in inflection investing, there are many false dawns. That gave us an opportunity to pay a small premium to the undisturbed price, with the belief that a potential inflection was afoot. As always, the ratio between risk and reward is what drives an investment, and from a practical sense, if I could risk only the small change from the undisturbed price to see if the inflection had legs, spread over many situations, we were bound to prosper.

Now, I increasingly feel that any good news leads to an explosion in the share price, as every computer model is programmed to chase the inflection, and every short has to cover as the negative rate of change has reversed. Instead, I genuinely wonder if it’s time to flip the script and purchase into the depths of despair, rather than chasing after the inflection. This may imply that we are likely to be early in both price and timing, as these securities are likely to go against us early in the process, but when top quality assets get this cheap, I wonder how much downside is really left. This is still an evolving thought-exercise, but I’ve always believed that to prosper at this game, you need to go where the capital isn’t. Trust me, there’s no one looking to buy after bad news, with the expectation that there could be another dose of bad news.

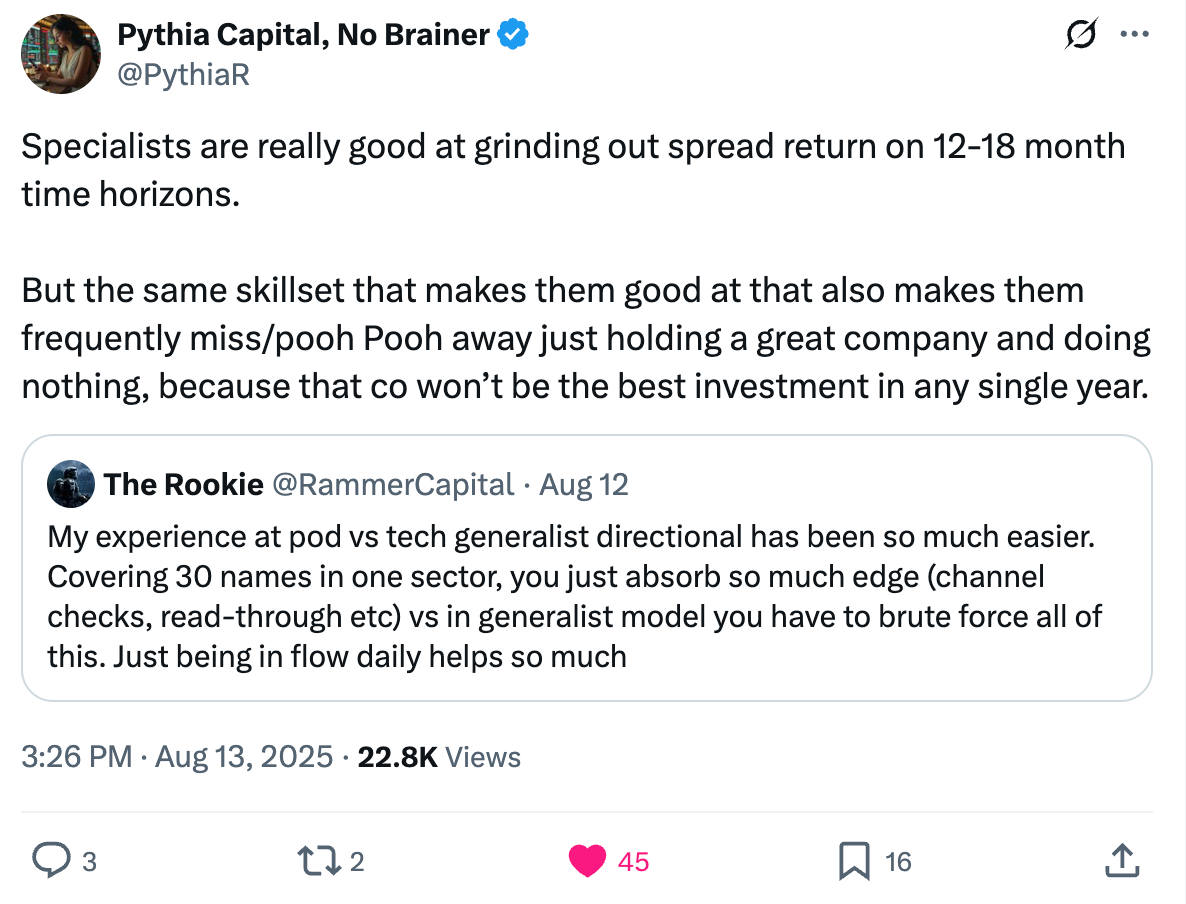

Another topic that I feel is interesting is that of “specialists.” If you are active on X, you probably have come across many specialists on any given topic (everyone is a specialist on geopolitics, by the way). This is somewhat normal because the investment industry is, to a great extent, organized this way. Now, many of these accounts think that, because they are “specialists,” they have a higher probability of forecasting the future. My POV is precisely the opposite. Because they are specialists, they sometimes tend to obsess over short-term topics that might be noise long term. At the same time, they sometimes struggle to focus on what matters long term. Some people think you have to be a specialist on any topic to have a view. While I do believe one needs to know what they are buying, knowing “too much” might give one a false sense of confidence and might be a roadblock to looking at the big picture. I agree entirely with this post:

The last topic I want to touch briefly on is that of 13Fs. Many funds/investors are required to file 13Fs with their US-based positions at the end of every quarter. For many people, this is an excellent source of ideas, but I increasingly feel it has become more of a confirmation bias than a source of ideas. I would be very careful with treating 13Fs as a signal for several reasons:

You don’t know what led the investment manager to make a decision

Investment managers also make mistakes

The data is outdated, and for all you know, they might have already sold their positions when you are getting the 13F

Needless to say, if one’s strategy is to copy these positions blindly, they will probably have a harsh time weathering future downturns, as they would be doing so with borrowed conviction.

The industry map was mixed this week:

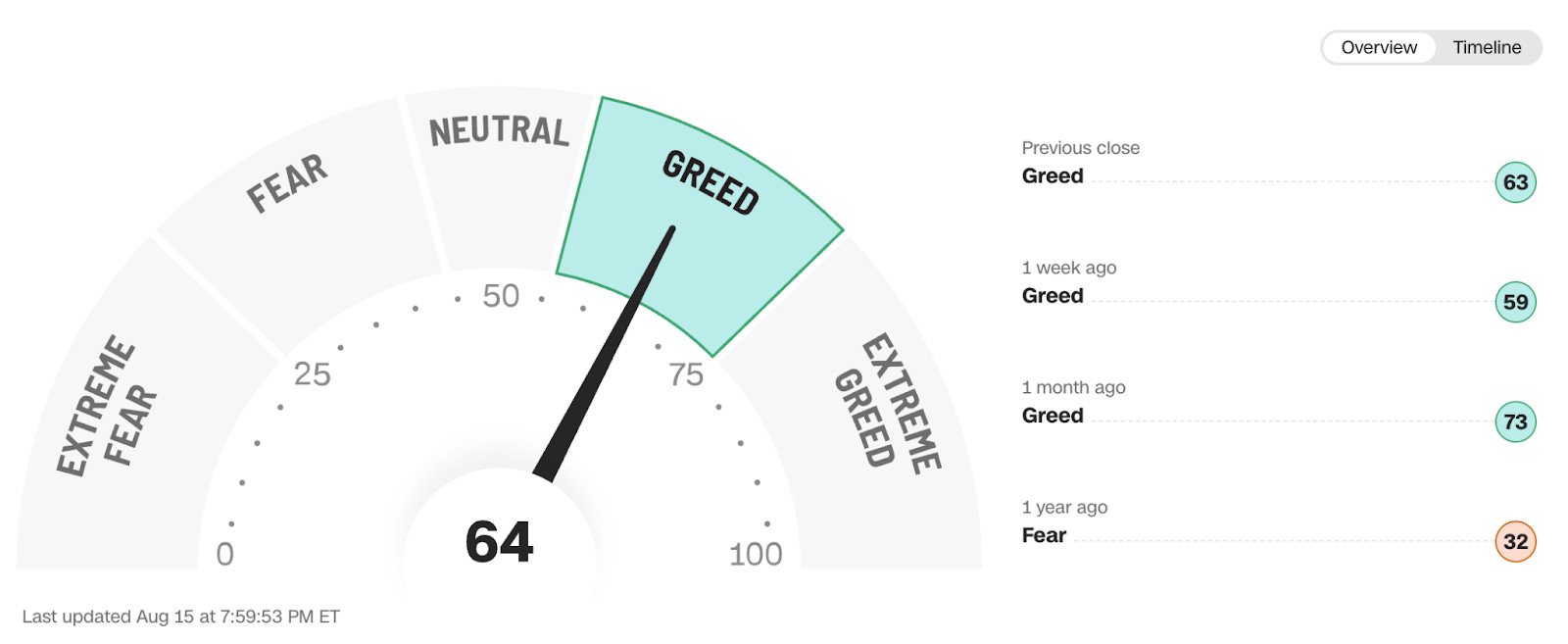

The fear and greed index rose and remains in greed territory: