The Reason Behind the Drop

Deere's Q3

Deere reported earnings this week, but the market did not like them much. Despite a beat-beat quarter, Deere’s stock dropped significantly, maybe because the midpoint of the guide was somewhat lowered and the go-forward commentary was not as positive as many expected:

I expect to be brief with this earnings analysis, which I will conclude with an explanation of my plans for the position. If this is the first time you are reading about Deere in Best Anchor Stocks, don’t forget you can read (for free) my in-depth report here.

Let’s start with the numbers.

The numbers

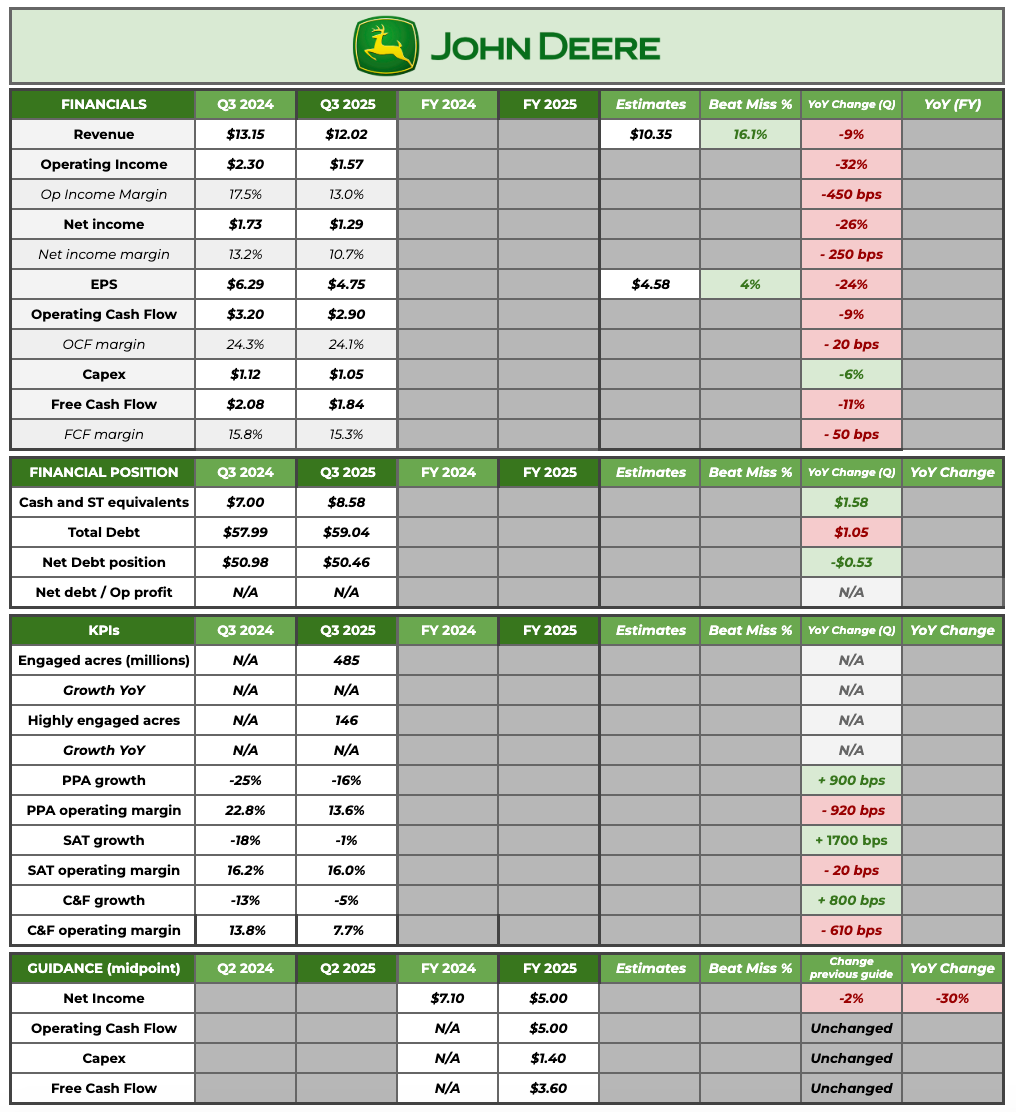

Here is Deere’s summary table:

As has been the norm over the last couple of quarters, Deere beat again on EPS. Note that revenue beats/misses are likely to be misleading because estimates might be for equipment operations (which might be the reason why we typically see such a large beat). Deere continues to outpace profitability expectations, showing early signs that the margin profile of the business is structurally improving.

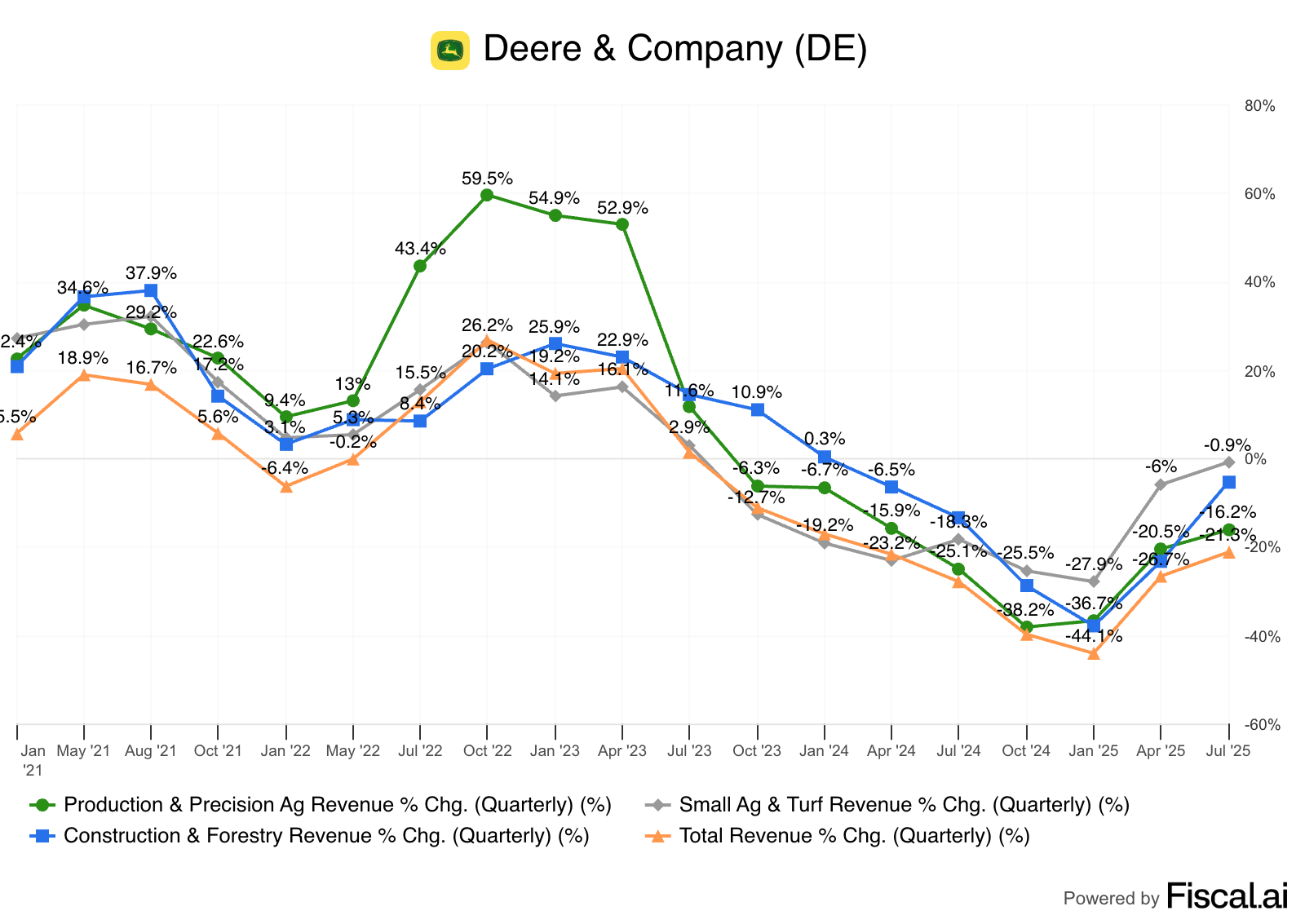

Another thing that stands out from the numbers is that, despite the drop in pretty much every metric, the drops are getting shallower. Deere remains in the agricultural downturn, but things are trending in the right direction. Despite diverging recoveries, the trend is positive for all segments:

I was negatively surprised by the construction segment. Pricing has been under pressure (-5%), and the segment is more competitive than I previously anticipated, especially on earthmoving equipment. The good news is that lower prices did bear fruit:

The price actions that we took in the quarter were reflective of a need to be aggressive on price in the North American earthmoving market. Where competitive pressure has been tougher. Importantly, we saw was a favorable market response to these actions as our retail settlements were up mid-single digits year over year in the third quarter. On top of that, we've seen a pickup in our order book where, on a percentage basis, we're up mid-teens year over year.

At the beginning of the year, management mentioned they expected Q4 to be a growth quarter for equipment operations, but is this still the case? Management did not explicitly confirm this in Q3, but we can calculate it with their full-year expectations and the results of the first 3 quarters:

Production and Precision Ag: management expects a 15%-20% drop in sales for FY 2025. This means that sales end somewhere between $17.7 billion and $16.7 billion. This segment has generated $12.57 billion in sales thus far this year, meaning we can infer Q4 sales of around $4.63 billion. This would translate to 7.5% year-over-year growth in Q4 for PPA.

Small Ag & Turf: management expects a 10% drop in sales for FY 2025. This means that sales end somewhere around $9.9 billion in FY 2025. This segment has generated $7.77 billion in revenue so far this year, implying Q4 revenue of $2.13 billion, which would translate into a sales drop of 7.7%

Construction & Forestry: management expects a drop in sales of 10%-15%, which would translate into FY 2025 revenue between $11.01 billion and $11.66 billion. The segment has generated around $8 billion in revenue so far this year, meaning that it should generate somewhere around $3.3 billion in Q4. This translates into growth of around 25% for Construction.

If we add all of the above, we get to equipment operations revenue of around $10.09 billion in Q4, which translates to growth of around 9% year-over-year. According to Fiscal.ai, market expectations call for a 5% drop, which wouldn’t be consistent with management’s commentary and the numbers above. Now, the question is…if Deere expects to return to growth in Q4, why is the stock bleeding? It likely has something to do with visibility.

Deere has its production booked for 2025 (recall that in PPA and Construction most of it goes to its dealers) and therefore can estimate with some degree of certainty where sales may land this year. That said, visibility into 2026 is not high, and management sounded quite cautious this quarter. An early indicator management looks at when thinking about 2026 is their Early Order Programs or EOPs (mainly for large agriculture). They run three EOPs; one for sprayers, one for planters, and one for combines. The EOP for sprayers is the only one where Deere has some sort of visibility to date because it ended this week (opened in May), whereas the rest are ongoing (planters follow sprayers and combines follow planters, just like the planting season would suggest). The EOP for combines, for example, barely begun two weeks ago. So here comes the “bad” news. Management mentioned that the EOP for sprayers shows a 20% decrease from last year, BUT there’s a relevant caveat: sprayers had been countercyclical in 2024:

Given the timing of the model year 'twenty four EOP, along with the excitement for new technology in the product line, sprayer demand was actually up year over year in fiscal year 2024. While tractors and combines were down over 20% in the same year. Essentially, in 2025, sprayers are in year one of a down cycle versus year two for tractors and combines.

The explanation makes sense. Management was obviously questioned about how the EOPs for planters and combines were evolving, considering that they are in a more normalized cycle, but they did not give many details. They did mention that they were seeing customer cautiosness in both but that EOPs always tend to accelerate towards the end of the period. So, where’s the uncertainty coming from? You guessed it: geopolitics. Management believes that all the tariffs and the volatile geopolitical environment are delaying purchase decisions (just like many other companies have been flagging for a while):

You mentioned uncertainty in your opening comments, and I think that's probably a good place to start. Given challenging industry fundamentals and evolving global trade environment, and ever-changing interest rate expectations, our customers are operating in increasingly dynamic markets. This naturally drives caution as they consider capital purchases.

This doesn’t necessarily mean that 2026 will not be a growth year, though. What it means is that management doesn’t know how 2026 will play out at this point, although they flagged several tailwinds that can play out if uncertainty diminishes:

And we think there's positive tailwinds from both what we see in the trade deals. We think there are positive tailwinds from what we see in tax policy. We think there are positive trade wins or tailwinds from what we see in the RVOs (Renewable Volume Obligations) that are going out there in renewable fuels. So there's good things coming. It's a question of when does that relate to the demand that we see.

If you look at the overall demand for crop, it's continuing to go up. Even with the large expected crop, the demand is going up and it's going to be tight in terms of stocks going forward. So the future is bright. The question is when do we see that turn? What we can do is prepare ourselves for it and get ourselves positioned to respond when it happens.

So, the summary of what I have just discussed is that it’s not a question of “if” but “when” demand comes back. It’s also worth noting that Deere has been reducing inventories across its channels aggressively in 2025. This means that, should end market demand come back in 2026, then Deere will (1) fully benefit from it because it will produce to market in 2026, and (2) can potentially benefit from any inventory stocking should demand be stronger than anticipated in 2026. In short, Deere decided to take a “double hit” in 2025 to prepare for the next upcycle:

I want to take a second to double down on that point. We as an organization have intentionally and proactively responded to this downturn faster and more aggressively than ever before. The results of that work are apparent in reductions that Josh just mentioned. We obviously don't have a crystal ball to know definitively when markets are going to turn. However, we know that when that happens, nobody's better positioned to respond to it and to respond to the demand than Deere.

This is Justin. I agree with Corey's point. On top of that, the underproduction we've done this year in small ag and construction forestry should be a year over year tailwind to our production as we move into 2026. As we're enabling both businesses to build in line with retail demand next year.

Now, with EOPs still being very early and the uncertain environment we are living in, we still don’t know what will happen in 2026 (and the market hates uncertainty). This is interesting because CNH Industrial (one of Deere’s peers) basically called 2025 a trough year in its earnings call a couple of weeks ago. Deere chose to be more cautious:

There's still a fair bit of uncertainty as we look ahead to next year. However, given reduced field inventory levels, our expectation is to build to retail demand across all our businesses will be beneficial. Particularly in areas where we're seeing positive momentum we finish 2025.

We’ll only know who is right in hindsight, but I prefer the conservative stance. Note that Deere still has around $7 billion in the bank (just counting cash from equipment operations), continues to generate significant sums of cash flow (thanks to the countercyclicality of industrial businesses as working capital gets drawn down), and can continue conducting repurchases. The company repurchased an additional $300 million worth of shares in the quarter. The pace of repurchases has somewhat decelerated, but I would love to see it accelerate considering the large cash position and the fact that the stock seems attractively valued (more on this later).

Many were discussing the guide as a point of weakness in the release. Deere “cut” its net income guidance from $5.12 billion to $5 billion but claimed that they expected $100 million additional headwinds related to tariffs, which would mostly explain the entirety of the guidance “cut.” Is it great? No. Is it worrying for the long term? Doesn’t seem so, no. In my opinion, something much more important for the thesis than a 2% guidance cut caused by tariffs is tech penetration. Management shared some interesting highlights here. The first one is that it apparently works and farmers are finding value. As farmers see the value, they use it more and more:

Since its launch, Precision Essentials has brought over 2,400 new customers into the John Deere Operations Center. And for those that were already in op center, we've seen a 35% increase in their engaged acres and a nearly 50% increase in their highly engaged acres since adopting the solution.

On average, 2024 See and Spray units are running the technology on 30% more acres this year.

Additionally, these same customers have added incremental Sea and Spray units to their fleet this season. This is evidence of the value that our customers are seeing in the technology.

The second one is that the R&D in agriculture is “jumping” to Construction:

The road building op center adoption metrics to date are impressive. Over the course of the year, we've more than doubled active role building organizations to nearly 3,000 in the operation center.

Is Deere still cheap?

Deere’s stock dropped quite a bit after reporting earnings, but barely stands today 10% off its highs. The question to answer here is whether it remains attractively valued.