Deepseek, Tariffs, the Fed, GDP...choose whatever you want! (NOTW#31)

Best Anchor Stocks has a partnership with Finchat (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

The indices did not have a great week, and this is the first time I've said this in a while (a sign of the times, I guess). The reasons behind this week’s poor performance are varied, and one can choose whatever best fits their narrative. In the market overview, I also discuss the topics of drawdowns and concentration.

I have added a new company to the Watchlist, and there is quite a bit of news this week (reserved for paid subs).

Without further ado, let’s get on with it.

Articles of the week

I published two articles this week. In the first one, I gave my opinion on the implications of the launch of Deepseek for certain industries.

The Potential Implications of Deepseek for Certain Industries

As I shared in the last News of The Week, a Chinese AI start-up called Deepseek recently launched an AI model that was up there in terms of performance with the latest US-based AI models. The catch? …

In the semiconductor industry, lower cost has typically entailed more future investment, not less. So, regardless of what happens over the short to medium term, it seems likely that the semiconductor industry, in general, will benefit over the long term.

The second article of the week was also related to semiconductors, as it was ASML’s earnings digest.

Don't Focus on Quarters

ASML had been on the chopping block since reporting Q3 earnings. The company not only saw these earnings leaked ahead of time but also reported very weak net bookings, something that spooked the market (it always does).

The company reported a strong quarter, surprising especially on orders. If you have been following my work for a while, you should know that ASML’s quarterly numbers are not really meaningful. Interestingly, “bears” or skeptics claim this to be the case only when they were better than expected; I wonder why.

Next week, paid subscribers can expect a detailed article about Danaher’s earnings and the Zoetis deep dive.

Without further ado, let’s see what the markets did this week.

Market Overview

The indices suffered (if I recall correctly) the first negative week of the year. Both were down more than 1.4%, albeit the Nasdaq dropped almost 2%:

As always, pinpointing the exact reason for the drop is pretty much impossible. Before trying, let’s zoom out a bit. Both indices are up more than 2% year to date after enjoying two consecutive +20% return years. In short, this week’s drop means nothing in the grand scheme of things.

People have gotten too accustomed to seeing stocks only go up, but if history is any guide, we should always be prepared for significant intra-year drops. The fact that stocks tend to go up over the long term doesn’t mean that they do so linearly. Look at the probability of suffering a drop of a given magnitude over any given year…

A 20% drawdown or worse happens once every 4 years, and if I am not mistaken, we have not had one since 2022. We should expect a significant drawdown relatively soon if the above is any guide. Of course, this seems impossible today as stocks soar, but it’s when it seems impossible when the likelihood (i.e., the risk) is the highest. This is one of the challenging things about investing: when risk is the highest, it seems the safest!

It also becomes very tough to stay still when such drawdowns occur because stock prices drive narratives (not the other way around). If we add to this the fact that it’s pretty “easy” to come up with a “credible” bear thesis for any of the companies one holds at a given moment, we end up with the perfect formula for long-term underperformance: selling when it makes less sense to do so (despite this time being when it seems the safest course of action).

Anyway, going back to the market this week. The reasons behind this week’s drop are like a buffet (not to be confused with Buffett); you are free to choose. We had…

The Deepseek-driven selloff to start the week: Nvidia dropped like a rock as the market believed that the demand for GPUs would come crashing down under a more efficient AI. Meta sort of reassured investors by confirming its Capex guide

A slower GDP growth than expected

The Fed not lowering rates and claiming that the pace to decrease them will be slower

Trump enacting tariffs on China, Mexico, and Canada

There are literally hundreds of scenarios you can make up to justify this week’s market performance, but I am pretty sure most of them will end up being meaningless noise in 5 to 10 years. Some can significantly impact markets over the short to medium term, though.

Market concentration is also a topic that I’ve talked about before. Something that never changes is that concentration seems great when it’s working, but less so when it doesn’t. People with relatively diversified portfolios will be dunked on when a few players (or a given factor) are carrying markets, but these portfolios tend to remain resilient when the trend reverses. I have always thought that being “irresponsibly” long any given company (and by this, I am saying 50%+ in a given position) is just that: irresponsible. I believe the goal for any investor should be to stay in the game (this is when compounding does its magic), and having such a large portion of your money tied into a single position significantly reduces the chances of one “staying in the game.” No matter how well one knows a company, there are always unknown and unforeseeable risks.

Why am I saying this? Because both indices “suffered” a bit this week from this concentration. Of course, concentration has allowed them to do exceptionally well over the past, so I am not claiming that his concentration is good or bad (neither the Nasdaq nor the S&P 500 have 50%+ of their eggs in one basket). For context, more than 284 companies in the S&P 500 have beaten the index’s YTD return of 2.97%. This means that more than half of its constituents have generated 2.97% or better returns. The index this year is not up more because several of the most significant constituents have done poorly (Nvidia, Broadcom, Apple, Tesla…). Not trying to claim here that this is good/bad, but rather that there’s much more to the S&P 500 than just the headline number.

I’ve chosen the year-to-date industry map this week to portray what I discussed above. The market in general has done better than the indices, but large companies like Nvidia, Microsoft, Tesla, Apple, and Broadcom have not and this has been a headwind:

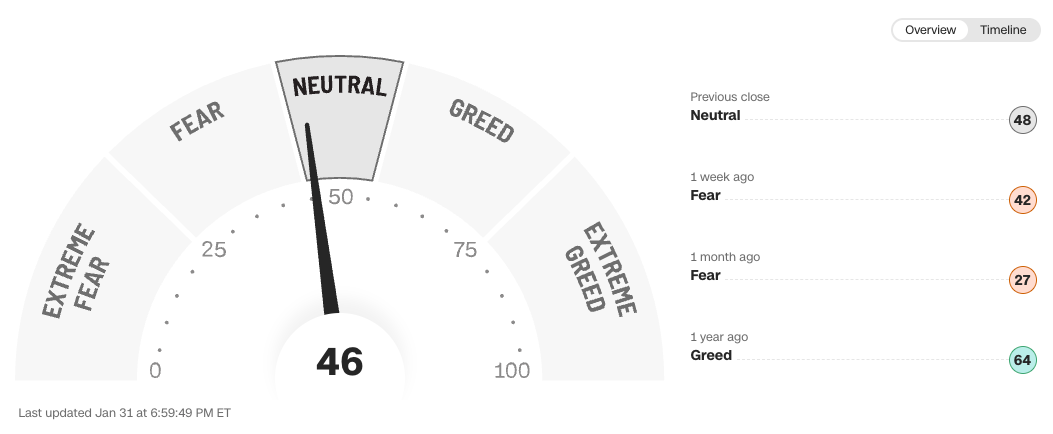

The fear and greed index remained in neutral territory despite all the “negative” news this week:

The rest of the content is reserved for paid subscribers.