Why I am (still) adding to Nintendo

In-depth valuation analysis

Nintendo is currently my second-largest position, so I thought it would be a good idea to write a detailed article discussing the valuation now that it has run up a bit from my cost basis. I must say that writing an article on valuation during a week when volatility has been through the roof has been a real challenge. I’ve had to modify the article a couple of times, and what I am about to share here might become obsolete in no time if volatility continues. The good news is that I also share my model at the end so you can tweak it as you like.

When I started writing this article, the stock had run up “significantly” from my cost basis, but I imagine you know how things have changed lately in financial markets; Nintendo has not been immune to the selloff. That said, I believe Nintendo is a good example of how equity returns don’t tend to come in a straight line.

I added the ADR ($NTDOY) to my portfolio around 2 years ago (February 2023) at a price of $10.16. The stock remained basically flat for a good part of 2023 (while equity markets were booming), only to run up at the end of the year (I took advantage to build my position). 2024 started on a good note for the stock, which continued running up until reaching $14, only to remain flat all throughout the remainder of 2024. The stock, however, has skyrocketed in 2025 and, believe it or not, it’s still up 19% YTD despite the broad market selloff:

The above is just a reminder of how tough long-term investing can be. When stocks go sideways, there will always be an urge to “do something,” but if the company remains attractively valued, the best thing one can do is either add to their position (I guess this constitutes “doing something”) over time or simply wait until the market portrays its true value. Note that Nintendo has only been flat for a couple of months, but some stocks can go sideways for years, and that’s when the pressure to do something really kicks in.

Since my first purchase two years ago, Nintendo is up around 70%, and it got close to 100% at some point. Note that the market is up around 30% over the same period, which begs the question:

Is Nintendo’s stock expensive today?

This article aims to answer this question and explain why I will continue adding to my position. To what is (in my view) an attractive valuation, we must add the fact that Nintendo might be well isolated from the current macro environment (I discussed why here, but also share some thoughts at the end of the article).

Before jumping right into it, I want to explain its structure. The article will have three main sections:

Nintendo’s (hidden and not so hidden) assets: In this part of the article, I’ll explain the value the market ascribes to Nintendo’s core business. The company has some significant hidden (and not so hidden) assets that must be valued separately to get to an adjusted valuation figure (i.e., the value of its core video game franchise)

How much is Nintendo’s core business worth? The outcome of the first part will be the valuation that the market believes Nintendo’s core business deserves. With this number, we’ll work through the different KPIs to get to a reasonable forecast of Nintendo's revenue and gross profit. I’ll divide this section into three sub-sections, which will be discussed later in the article.

The remaining P&L and the DCF: with the outcomes of the first two sections, I will build the remaining parts of Nintendo’s P&L and build a DCF model to understand the potential returns the stock could offer going forward from the current price.

Before jumping right into the exercise, I want to make an important disclaimer: this is a valuation exercise, and therefore, it’s pretty subjective. There are not many certain things in life, but one certainty that I can share with you is that the numbers shared here will be wrong. The good news is that the goal of the exercise is to be roughly right and to understand where the valuation lies today, being conservative and acknowledging that we’ll be wrong (hopefully the mistake is being too conservative and not too optimistic).

Let’s start with the company’s assets.

1. Nintendo’s hidden (and not-so-hidden) assets

Firm in its tradition as a Japanese corporation, Nintendo has significant investments in other companies with which it has a commercial relationship (the famous Japanese cross-shareholdings), an investment in the Seattle Mariners (weird, I know), and a significant cash position. All of these must be stripped out of the current valuation to estimate the value the market is giving to the core videogame business. It’s a good idea to start with the assets that are apparent to everyone: those assets that Nintendo openly discloses.

Nintendo discloses a series of participations in other companies in its annual report, some of which are disclosed at book value rather than at current value (due to their values not being readily available). The value of some of these investments is easy to calculate because some are publicly traded corporations. Let’s go with the most significant two: BANDAI NAMCO and DeNA. Nintendo holds shares in these two companies because of their relevant commercial relationship. BANDAI is a software developer, and DeNA is responsible for developing some of Nintendo’s mobile games. The company owns around 11.5 million shares of the former and 15.1 million shares of the latter. This translates into (roughly) the following stakes at current valuations (note that shares recovered today, but I decided not to change the valuations here as it just makes the exercise more conservative):

BANDAI NAMCO: $342 million stake. The value that figures in Nintendo’s annual report is $216 million, which is close enough. BANDAI NAMCO’s shares have risen significantly since Nintendo filed its 2024 annual report

DeNA Co., Ltd: $300 million stake. The value that figures in Nintendo’s 2024 report is $151 million. DeNa’s stock has roughly doubled since the closing date of the annual report in 2024. The rise has been partly due to the successful launch of The Pokémon Card Game for mobile (this was a terrible mistake of omission on my side because there was plenty of time to get onboard, and it was obvious it would be very successful)

This means that Nintendo owns around $650 million worth of stock in both BANDAI and DeNA. Note that these stocks have also fallen significantly lately due to the tariff drama (despite selling software). As the remainder of the investment shares are not as significant in the equation, I’ll simply ignore them (it’s more conservative this way).

To the above, we must add a couple of other (private and not readily apparent) assets. This is where we have to start to make some assumptions. The first and strangest one is Nintendo’s stake in the Seattle Mariners, a Major League Baseball team. Baseball is pretty huge in Japan, and the story between Nintendo and the Seattle Mariners is an interesting one:

The Mariners principal owner before that was Nintendo's 3rd president Hiroshi Yamauchi who was the one who purchased the team in 1992. Yamauchi helped keep the Mariners in Seattle when he stepped in to purchase the team at the time from former owner Jeff Smulyan, who was looking to move the club to Tampa Bay.

This was done as favor to the Seattle area & team, since Yamauchi got involved as his home was in Redmond, Washington, next to Nintendo of America HQ.

Although he retired as chairman of Nintendo in 2002, he served as head owner of the team until his passing in 2013.

Nintendo of America sold most of its shares in 2016 but retained a 10% stake, probably to continue enjoying the historically good commercial relationship with the team. According to several sources, the Seattle Mariners are worth around $2.2 billion. If we were to add a 20% illiquidity discount, Nintendo’s stake in the team would be worth around $176 million.

Another relevant asset is Nintendo’s stake in Niantic, a developer of augmented reality mobile games.

(Note: Niantic recently sold its gaming division to Scopely, but as Nintendo has not reported receiving the money yet, I decided to leave this section as is. If anything, the recent sale should help us confirm the numbers here)

Nintendo and The Pokémon Company invested $30 million in Niantic in 2015 when it was valued at $100 million. This means that Nintendo’s stake should be somewhere around 30%. The problem is that we don’t know if Nintendo has participated in further financing rounds to retain its stake or if it has been diluted. To be conservative, I’ll assume Nintendo’s stake in Niantic is around 20%. Niantic raised at a $9 billion market valuation in 2021 (the peak of the bubble and the Pokémon Go craze), so I think it’s reasonable to drop this valuation number to somewhere around $5 billion. This would make Nintendo’s stake worth around $1 billion. Note that Niantic recently sold its gaming division to Scopely for $3.5 billion (not $5 billion), but Nintendo invested in the entire company, not just the gaming division.

So, just to recap, adding Nintendo’s stake in DeNa, BANDAI, Niantic, and the Seattle Mariners, we would arrive at a figure around $2 billion.

These, however, are not as hidden as the next asset is: The Pokémon Company. According to its annual report, Nintendo owns 32% of The Pokémon Company:

The Pokémon Company is a private company, so the book value that Nintendo reports is laughable: the investment in TPC is reported at $2.44 million!

So, the problem with the information shared by Nintendo is that it’s missing considerable relevant data. The first missing data point is that Nintendo also owns stakes in the two other owners of The Pokémon Company: Game Freak and Creatures. These are not disclosed in the annual report because they fall under the 20% threshold. Assuming both GameFreak and Creatures own equal amounts of The Pokémon Company (which we don’t know), and that Nintendo owns 10% stakes in both (for example), Nintendo’s actual ownership of the Pokémon Company would be closer to 40% (rather than the reported 32%).

The thing is that Nintendo does not need to have a majority stake to have control over The Pokémon Company. The reason is that Nintendo owns all of the Pokémon trademarks, so nothing happens at The Pokémon Company without Nintendo’s permission because the company basically owns the brand. The Pokémon Company solely acts as a publisher and distributor.

So, how much is The Pokémon Company worth? According to several sources, The Pokémon Company generated $1.9 billion in revenue and $402 million in net profit in its fiscal year ending February 2024. If we assume that a royalty-like business like this one would be valued at 30x earnings (probably conservative), TPC would be worth somewhere around $12 billion, making Nintendo’s stake worth around $5 billion. So, adding all of the above, we would end up with around $7 billion in hidden (and not-so-hidden) assets.

It’s worth noting, though, that besides Nintendo’s stake in the Seattle Mariners, all of these stakes are, in one way or another, related to the company’s core business, so it’s not like they can easily be stripped out of the company and sold.

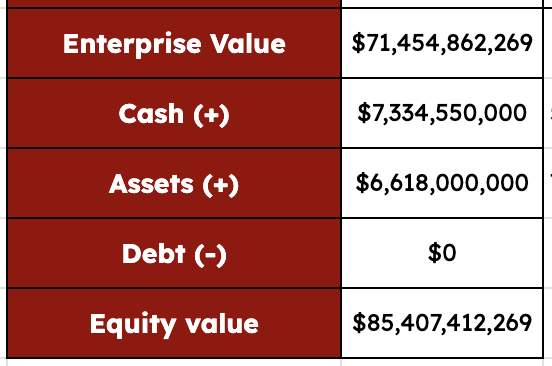

In comes the elephant in the room: cash. Nintendo, like any true Japanese company, holds no debt and a substantial amount of cash. As of the end of Q3, Nintendo had around $14 billion in cash and short-term investments. This amounts to around 20% of its current market cap.

Nintendo’s cash position has historically been controversial among investors. Management has openly shared that it carries such a hefty cash position in case the next system is a flop and/or the company has to weather a cyclical downturn. This also applies to any macro-induced black swan event. Nintendo is also reluctant to fire anyone, so the company must resist as-is an unsuccessful launch or a challenging period. Many claimed that this meant that this cash was not available to shareholders, which, to an extent, was true.

With cyclicality risk significantly diminishing with the announcement of an iteration of the Switch, many wonder if Nintendo’s cash position is available for shareholders today. While we will only know if this is the case in hindsight, I believe that at least considering that 50% of this amount belongs to shareholders is sensible. This means that, to understand what Nintendo’s core business is worth, we must start by deducting $14 billion from Nintendo’s current market cap:

Note that there’s always the option that the market is writing down the value of these assets to zero, which would, to an extent, make sense. Some of these assets are illiquid; for the others, it might be tough to foresee a scenario in which Nintendo makes them liquid and returns them to shareholders (i.e., these seem like strategic investments that are unlikely to be wound down).

2. What’s the core business worth?

Nintendo has three main ways to make money at its core: selling hardware, selling software, and through other related IP ventures (merchandise, movies, mobile games…). While the company has historically made most of its money through the first two, I think the third revenue source will play a more relevant role going forward due to the company’s commitment to publishing a movie every year and the impact this can have not only on revenue but also on marketing leverage. This said, as I don’t think it’s a good idea for me to forecast the impact it will have on revenue (too many unknowns), I will leave it out of the equation, and it will serve us yet another layer of conservativeness. This means I am valuing the company’s “nascent” IP venture-related business at $0. The article will focus on the company’s video game platform.

So, my objective in this section is to forecast three parts of Nintendo’s video game business:

The ongoing business of the Switch 1

The nascent business of the Switch 2

The development of the NSO (Nintendo Switch Online) subscription