Starbucks software crusade, worth it? (NOTW#99)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

You’ll also get access to the 30+ page detailed report on the robotics industry.

The in-depth reports of Stevanato and Deere are also free to read to gauge the quality of the research.

Join today:

The markets were flat in a relatively boring week, although I discuss one topic that got me particularly interested this week: is AI eating software at large enterprises?

Without further ado, let’s get on with it.

A new in-depth report next week

The day (or better said, week) has come! I’ll publish a new in-depth report next week, exclusive for paid subscribers. The company is a relatively unknown software business that owns proprietary data to fence off the AI “threat.” I believe it’s deeply misunderstood by the market as it has fallen “prey” to two misleading narratives.

You can read all the in-depth reports here and the last 5 by clicking any of the links below:

All of these in-depth reports contain a great amount of detail on the businesses and their investment thesis (when applicable, as not all end up making it into the portfolio). Not in-depth reports per se (at least to my standards), but I’ve also published work lately on Rosebank Industries (LON:ROSE) and Sabre (SABR).

Articles of the week

I published one article this week: the sixth edition of “On the radar.”

I profile four (it’s normally three) companies this week:

An HVAC/Refrigeration provider (hardware, software, and services) that’s family-owned, well-run, and that it’s exposed to the industry in an interesting way

A company with vast proprietary data and competitive advantages in which management is highly aligned with shareholders

A medtech company that has gone from loved to hated in the space of one year without fundamentals budging much

A single-product medtech in the early scaling phases that looks interesting (yes, you read that right “a single product medtech”, yikes?)

I’ve already profiled 19 companies in this series and expect to profile many more in the future.

Without further ado, let’s see what the markets did this week.

Market Overview

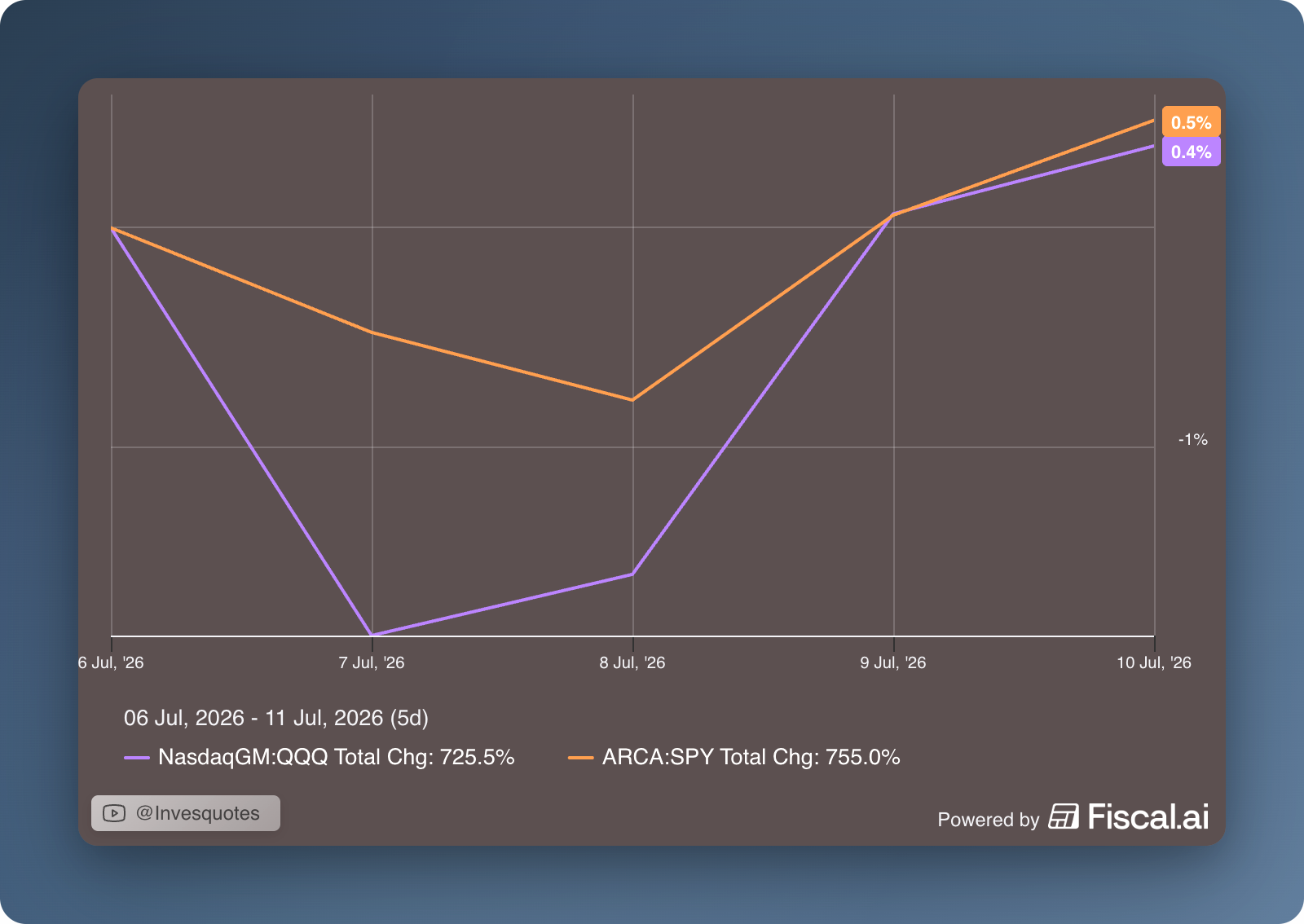

Both indices were relatively flat this week after recovering from a weak start:

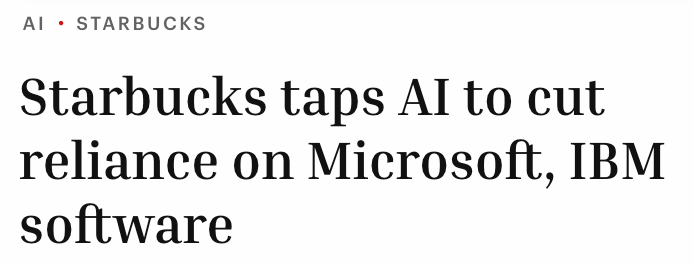

There was one thing I found particularly interesting in an otherwise “boring” week: this Starbuck’s headline:

Source: Fortune

One would’ve imagined that such a headline should’ve destroyed the IGV (the software ETF) because it could be understood as the AI bear case for software becoming a reality. The IGV was indeed down 2.5% this week, but likely far from what one (at least myself) would’ve expected if the market would’ve taken this seriously. The headline portrays one reality, but there’s a different reality hidden in the article. I suspect that not many people who shared the headline have actually read the article, so let’s take a look.

The headline claims that Starbucks is increasing its reliance on AI to cut the software tools of companies like Microsoft (inventory management) and IBM (maintenance). Starbucks’ CTO sent in an internal memo to employees claiming that the company spends around $400 million in software every year and that “there’s clear opportunities to reduce the spend in software.” One thing I believe this misses is how much the internal software development is going to cost in terms of labor and maintenance (software does not maintain itself), but that’s a topic for another day.

The article then goes on to claim that Starbucks has been working for several years on building a POS system to replace Oracle Symphony. This means that after several years of hard work, the efforts have been futile (which, surprise, means that software is not as simple to solve as many believe, even in the AI era).

But several other things in the article seem to indicate that stripping out software from third-party vendors might not be worth it. First, Starbucks has already failed once:

There’s skepticism about how much, or how quickly, AI can speed up and automate work. Starbucks recently pulled an AI-powered system to track inventory at stores, reverting to manual counting. It also continues to use software from third-party vendors, including from companies such as Microsoft.

Okay, I get it, doing this is tough (no surprises here) but the returns must be worth it, right? Well, it turns out they might not be! Starbucks expects to save $10 million from these efforts…

The Starbucks enterprise technology team is on track to reduce its budget by about $30 million in the fiscal year ending in late September, according to the internal presentation. That includes cutting about $10 million in software spending.

…which should be contextualized in the context of the company’s $20 billion opex. This results in savings of 0.05%, which doesn’t seem extremely enticing considering that the company will (and is already) risking business continuity with no measurable results to show thus far. The company expects to “roll out” these features by the end of next year (2027), meaning that we are not even going to see measurable results for a long time. I honestly think that, while the headline looked very bearish for software, the reality portrays that it’s actually not that easy to replace software and that it doesn’t seem like the risk/reward is worth it! If it’s not worth it in enterprise SaaS, it might be even less worth it in SMB SaaS, which is where most of my exposure to software lies.

The industry map was mixed this week, with semis picking up some of the ground they lost last week:

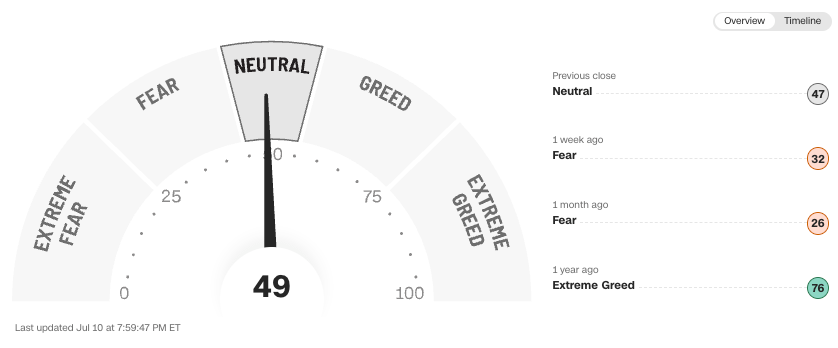

The fear and greed index improved materially and is now in neutral territory: