On The Radar #6

An interesting HVAC company, a great compounder at (finally) a decent valuation, and a double inclusion

Welcome to the sixth issue of “On The Radar.” If you want to know what this series is about, I recommend reading the first issue.

Simply put, the goal is to share interesting companies that I’ve looked at but have not researched in-depth yet (at least not to my standards). You can think of the “On The Radar” series as a well-curated list of companies that fit my investment philosophy and that might (in the future) make it into the portfolio. So far I’ve only included in my portfolio 1 of the 15 companies I have profiled in this series, with good (but still early) results: +13% in about a month (there’s also an in-depth report available for paid subscribers). I have to say that I am close to making the second inclusion of an “On The Radar” company into the portfolio. I’ll publish the in-depth report next week (exclusive for paid subscribers).

Today’s issue brings four companies (one for free and the remaining reserved for paid subscribers) as I’ve decided to make a double-inclusion and I’ll explain why. Here’s what you can expect today:

An HVAC/Refrigeration provider (hardware, software, and services) that’s family-owned, well-run, and that it’s exposed to the industry in an interesting way

A company with vast proprietary data and competitive advantages in which management is highly aligned with shareholders

A medtech company that has gone from loved to hated in the space of one year without fundamentals budging much

A single-product medtech in the early scaling phases that looks interesting (yes, you read that right “a single product medtech”, yikes?)

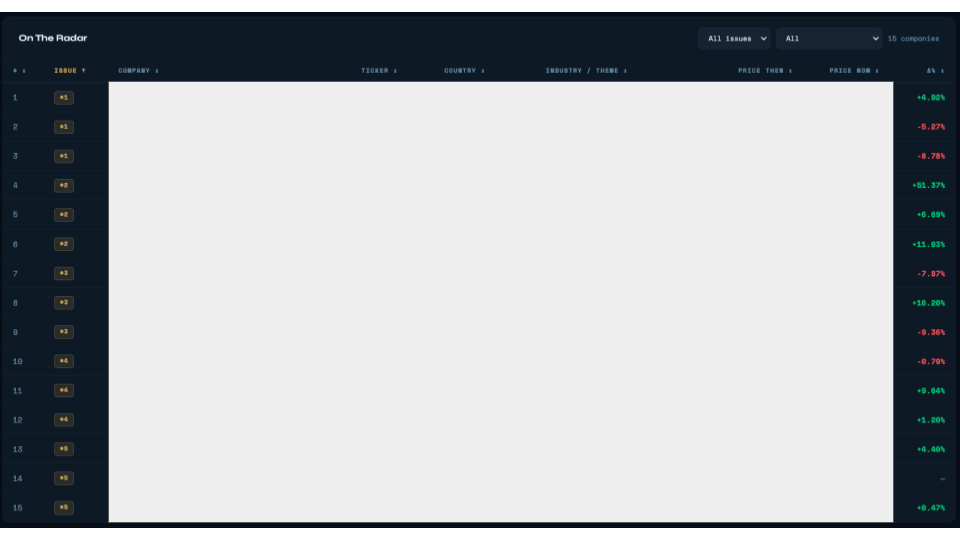

Note that all of these businesses get included in the “On The Radar” tab of the Portfolio Management Tool with their respective price evolution since the issue. These are generally companies that I don’t own but I find interesting so I prefer to see stock prices dropping across the board. This said, I do expect to include good companies here, so even if I don’t include them in the portfolio, I’d expect to see stock prices rise over the LT because that would mean I am fishing in the correct pond:

As this is the sixth issue, free subscribers have had access to 6 companies (one for free per issue) whereas paid subscribers have had access to 19!

So, without further ado, let’s jump into today’s issue which doesn’t start with a Swiss company (surprise).

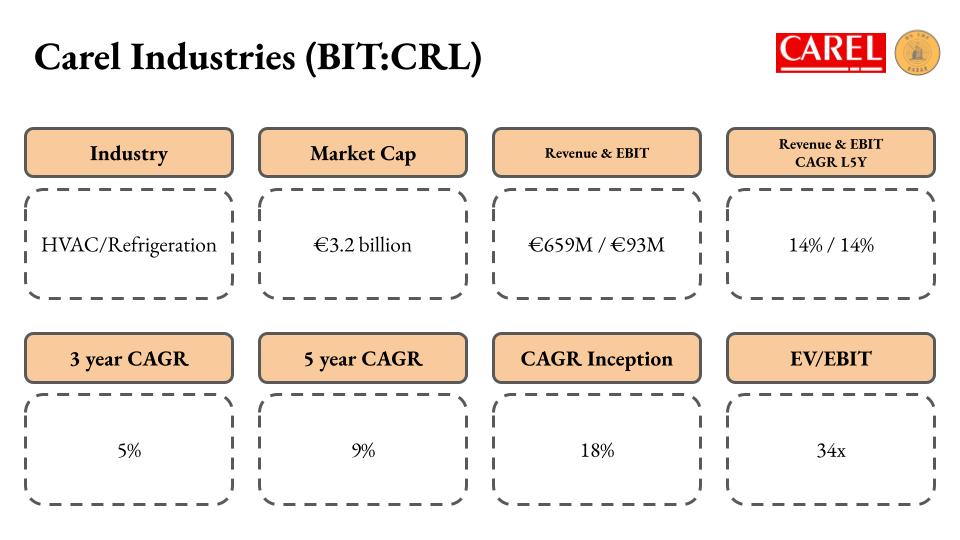

Carel Industries (BIT:CRL)

Brief description of the business

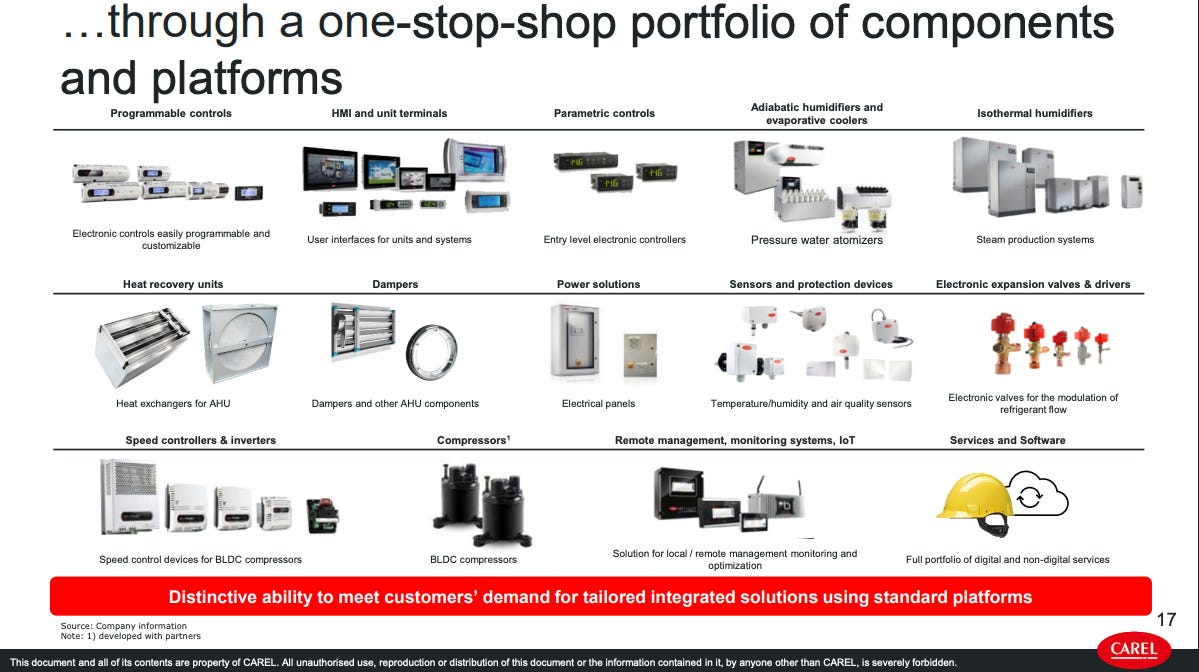

Carel participates in the HVAC and refrigeration markets. The company sells (primarily) control systems to HVAC/refrigeration OEMs. These OEMs install Carel’s products with the goal of making their solutions more energy efficient. Maybe a better way of understanding Carel is thinking that the company provides the brains (both hardware and software) that go into HVAC and refrigeration equipment.

One would think that HVAC and refrigeration equipment OEMs would’ve already in-sourced something like this, but it turns out that it’s tougher than it looks.

Why it caught my attention

Carel caught my attention for two reasons, but it all started with my willingness to look into the HVAC industry. Seeing the heatwaves that Europe has faced over the last couple of years, I thought it would be a good idea to try to look for HVAC beneficiaries. If you live in the US, you’ll know that HVAC penetration is pretty high there, but it’s significantly lower in Europe…

While nearly 90% of US homes have air conditioning, in Europe it’s around 20%.

Source: CNN

The CNN article goes to claim that the trend if shifting:

There are already clear signs uptake is increasing in Europe, as in many parts of the world. An IEA report found the number of air conditioning units in the EU is likely to rise to 275 million by 2050 — more than double the 2019 figure.

Now, there’s an additional roadblock in Europe and it’s exactly the one you’d expect: regulation. The EU is dead serious with their “Climate Neutral” ambitions and they are pushing towards energy efficiency. This means that not only is the European HVAC industry in need of new units, but they’ll also be significant retrofit/renovation demands to adhere to regulations. For these reasons, I tried to look for companies in Europe that might be flying under the radar in the industry, and Carel popped up.

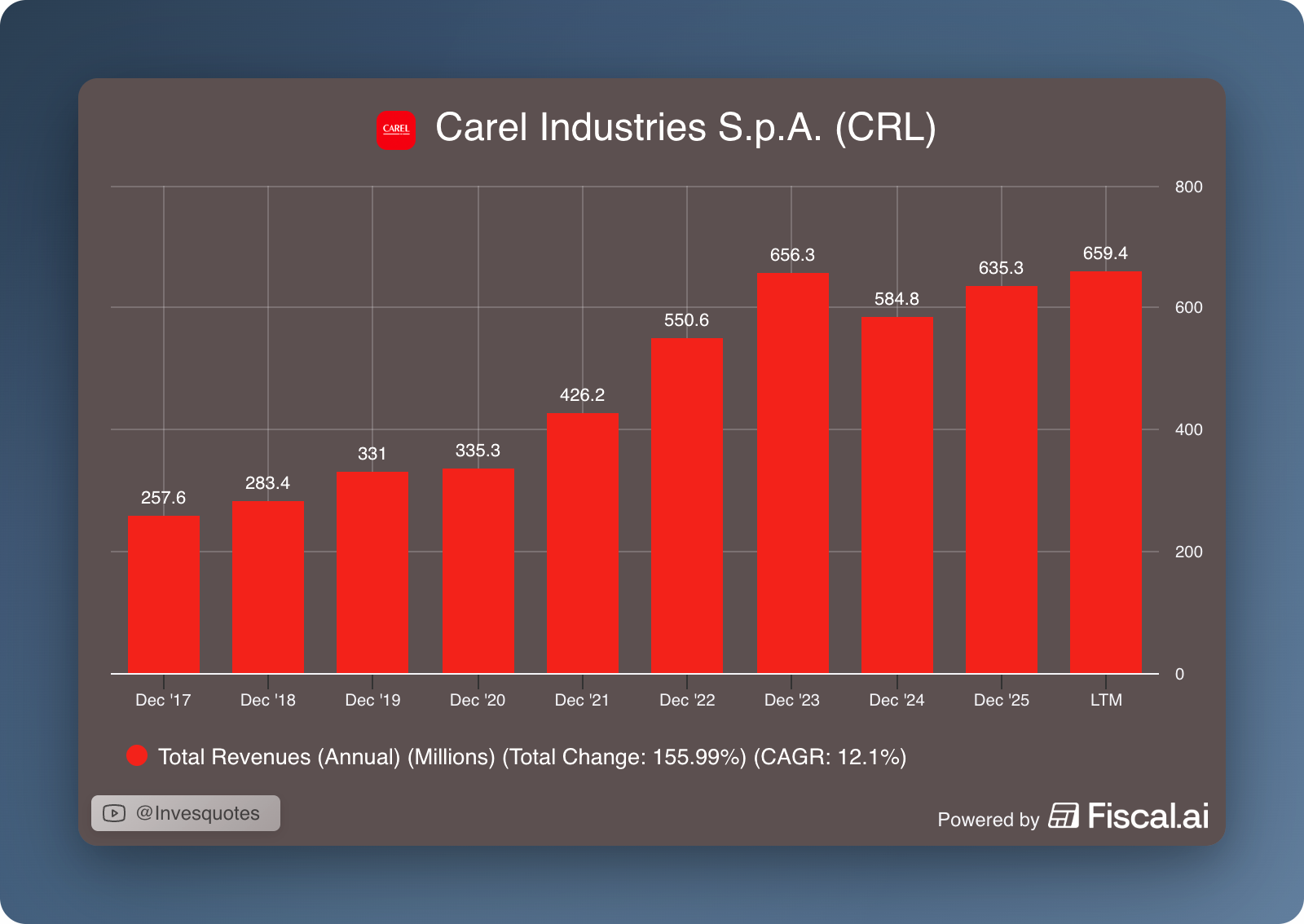

Now, the main reason why I looked into Carel was its track record. When one looks into an HVAC supplier/OEM, one expects to see cyclicality tied to new construction or inventory cycles. While Carel has only been publicly traded since 2018, the organic growth track record is pretty good: only one negative growth year (2024) but higher growth than one would’ve imagined (management strives for HSD organic growth to which one must add tuck-in acquisitions). Since 2017, revenue has CAGRd at a 12% clip:

The other thing that made me want to look into it was the fact that it remains family-owned and run, BUT (very important BUT) with the family striving to improve the liquidity of the stock.

What I like

I liked several things about Carel:

It seems like a pretty well run business in which management knows what they are doing (this is obvious if one reads the earnings calls)

The HVAC industry enjoys secular tailwinds (mainly in Europe) so it seems like an interesting place to fish (this is not only applicable to Carel and I don’t expect to stop looking once I dig into Carel)

The company is exposed in an interesting way to the HVAC industry. It’s not your typical OEM vendor; Carel sells a high quality and mission critical product into the equipment

Carel also made an interesting software-like acquisition in 2023 (Kiona), which grows considerably faster than Carel and enjoys better margins (which have been expanding)

The company is also exposed to the fast-growth data center market which is becoming a pretty strong tailwind. This said, the company does not entirely rely on this industry as less than 50% of its current growth comes from data center (it’s still significant, though)

What gives me pause

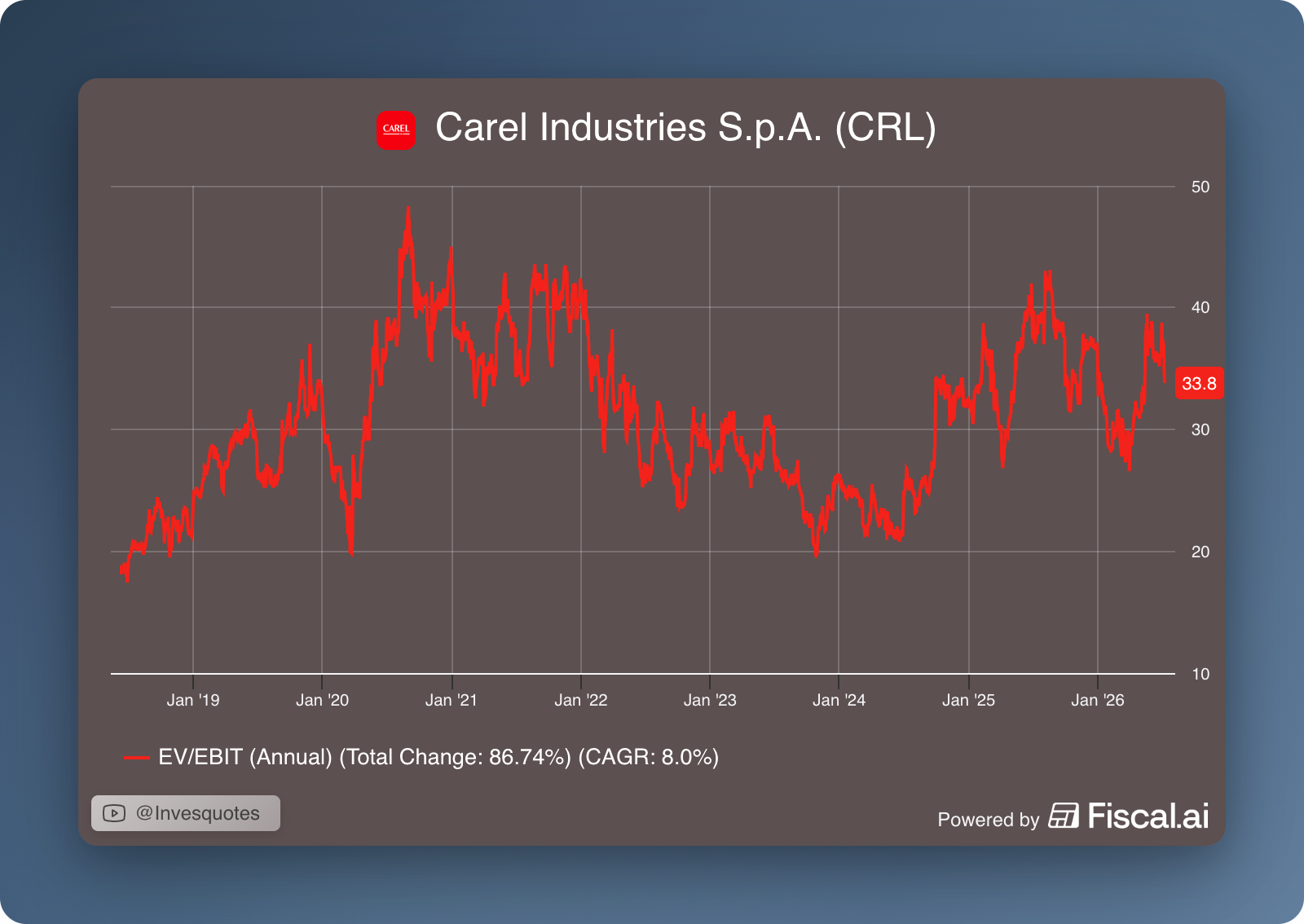

The main thing that gives me pause is that I believe the company has gotten bid up (up 83% over the past year) probably due to its data center exposure. If there’s a market rotation outside of AI, the stock may suffer. I’d say this is pretty apparent in the fact that Carel has moved lately together with the semiconductor industry.

The valuation also seems tight for a HSD (high-single digit) organic grower; it’s currently trading at a 34x EBIT!

What I am watching

I have to do more work but based on what I’ve seen, this seems like a “do-the-homework-today-to-enjoy-it-tomorrow” kind of situation as there seems to be significantly better opportunities across my portfolio.

Let’s now jump into the next company.