(NEW) On The Radar #1

A retail turnaround, a stable healthcare business, and a tricky aerospace business

Welcome to the first issue of On The Radar, a new Best Anchor Stocks recurring section! The initial idea is to publish an “On The Radar” article once every two weeks, probably at or around the end of the week (Thursday/Friday). Even though I’ll share more information below, the goal of “On The Radar” is to openly share much more of my investment process in a way that’s useful to you. Let me explain a bit further.

What exactly is “On The Radar”?

The idea of this new recurring section is to share three companies/investment ideas which I believe are interesting, explaining why I believe this to be the case. The goal ISN’T to share an in-depth report on each, but simply a small text explaining why I am considering researching these businesses in more depth after having conducted some initial (and thorough) filters (both quantitative and qualitative). This is what you should expect for each idea:

A brief description of the business

Why it caught my attention

What I like

What gives me pause

What I am watching/looking to analyze further or why I ended up discarding the business (most will fall in the former category, but I also consider some discarded companies interesting)

But… “Why” On The Radar? If you are used to doing your own analysis, you’ll know that the journey between getting initially interested in an idea and making a portfolio inclusion is not typically fast. The reality is that one can’t (or better said: “shouldn’t”) force a portfolio inclusion, which doesn’t mean one should simply sit down without doing any work. I take a look/analyse at A LOT of companies each week, and these tend to end in several buckets:

Immediately discarded after a quick look

Discarded after some more work

Watchlisted to do more work in the future as I deem there are more interesting things out there or there’s something I don’t feel quite comfortable with yet

Immediately start doing more in-depth work

Discarded after more in-depth work (sucks, but it happens pretty often)

Portfolio inclusion

As you’d imagine, the last of these is the least likely outcome. I tend to view any investment process like a funnel. A lot of companies go in at the top, but only a few make it down the bottom (portfolio inclusion):

This doesn’t mean that there are no interesting companies within the funnel. On the Radar focuses primarily on the third and four stages described above: “Watchlisted to do more work in the future” and “immediately start doing more in-depth work.” Each “On The Radar” issue will bring three ideas that primarily belong to these two buckets and which have the potential (over time) to make it to the last stage: portfolio inclusion.

So what’s the value add for you? You’ll get a constant stream of potential ideas that have already been significantly filtered by me. This is work that I was already conducting either way, but I also get some value: writing down these ideas will help me structure my process more clearly.

As to what kind of companies you can expect here…the answer is pretty much anything. I take a look at a lot of situations every week and try to stay open minded as to where there might be interesting investment opportunities. This week’s issue is a good example as I’ll be profiling three very different businesses and situations:

A European retail turnaround

A very stable and interesting healthcare business (with an appealing growth profile)

An interesting aerospace business with some messy accounting

Every “On The Radar” issue will openly share one of the companies, with the remaining being reserved for paid subscribers.

If you want to have exclusive access to On The Radar Issues and…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

(The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.)

Consider becoming a paid subscriber:

So, without further ado, let’s jump with today’s issue!

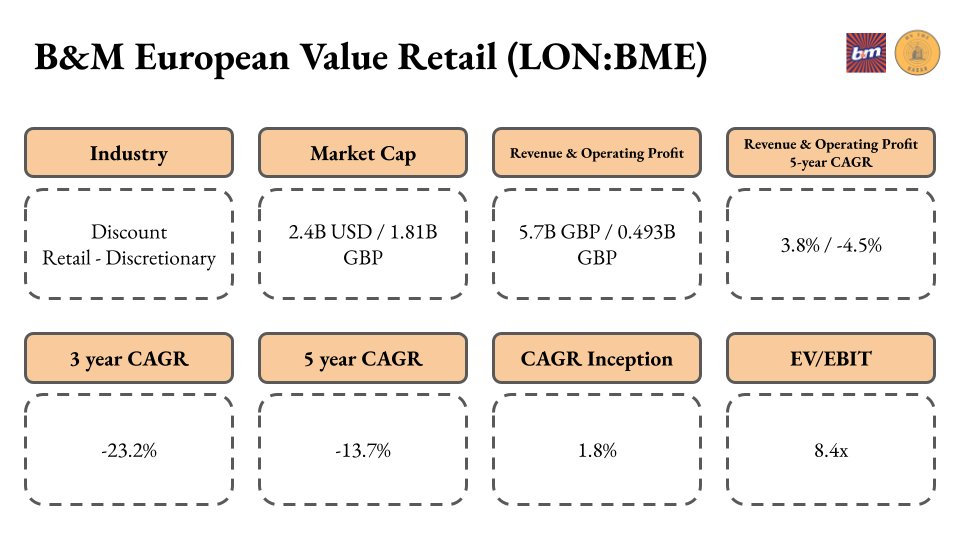

1) B&M European Value Retail (LON:BME)

Brief description of the business

B&M is a UK-based discount retailer that operates in the UK and France. The company owns more than 1,000 stores which carry FMCG (Fast-Moving Consumer Goods) and General Merchandise items, almost in exact proportions (50/50).

The company’s operations can be divided into three segments (1) B&M UK (786 stores), (2) B&M France (135 stores), and (3) Heron Foods (343 stores). The model is straightforward: open as many stores as possible at attractive returns (typically less than 1 year payback) while pursuing sustainable LFL (like for like) growth. The value proposition rests on remaining an attractive place for value-conscious consumers to find great deals.

Why it caught my attention

The valuation was the main reason why B&M caught my attention. I had looked into the company before but had not fallen “in love” with the business. That said, everything (or pretty much everything) has a price, and B&M seems to be trading pretty cheap considering its risks/drawbacks. But, why?

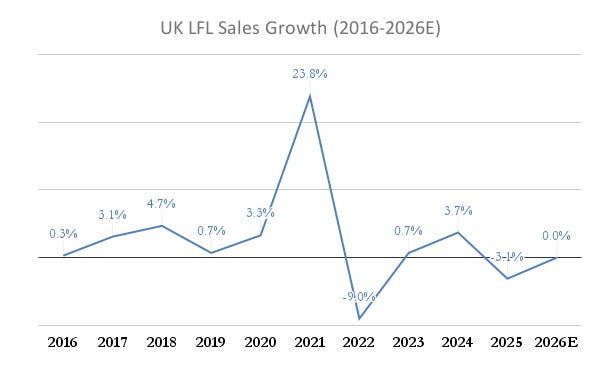

After a pandemic boom (B&M stores were considered “essential” during the pandemic), UK LFL growth weakened quite considerably.

Source: Made by Best Anchor Stocks

It seemed a bit harsh for the stock to be down so much in the face of such deceleration (some of which could be considered a return to normal). This said, it’s also true that the company seemed to have been run for margins during Alex Russo’s (former CEO) tenure. This resulted in significant execution issues and an unsustainable margin level.

The company is now a turnaround play and has a new management team that is implementing an improved operating model (Back to Basics). Should the management team manage to turn the ship around (namely LFL sales growth in the UK), the shares should significantly rerate higher. To this, I must add that the company remains cash generative and is in the process of redomiciling to Jersey (from Luxembourg), which should allow management to conduct buybacks, a tool that has historically been absent from the capital allocation framework.

What I like

There are a couple of things I like about B&M, namely the following:

Discount retail is secularly gaining share and is more insulated from macro pressures than traditional retail

Despite the troubles one can see in the financials, the customer perception of B&M’s value proposition does not seem to have changed materially (very relevant in any retail turnaround)

The new management team has openly discussed the areas of underperformance and is working on solving these

The stock is cheap IF the model is not broken

The opportunity in France seems to be significant and early signs are encouraging (i.e., the model seems to be exportable, even though it failed in Germany)

It bears some resemblance with Five Below’s (FIVE) turnaround, a business I know well

What gives me pause

There are two things that give me pause. First, the fact that the underlying business doesn’t appear to be great even in a normalized environment. I’ve calculated the LFL sales CAGR in the UK over the past decade (so considering the post pandemic boom and posterior bust) and the result is a 2.5% CAGR. I am pretty sure this signals that there’s been no real growth over the last decade. It’s true, though, that the UK economy has seen better days and it’s not entirely B&M’s “fault.”

The second thing that gives me pause is that retail is very hard and most turnaround promises end up terribly. Will this time be different? I don’t know, but if it is, the shares will most likely do well as the market seems to have priced in a not-ideal outcome (the market, though, has been right thus far). Note that retail concepts can spiral out of control, both to the upside and the downside: if the model works it’s a money making machine, if it doesn’t, it can quickly go bankrupt (many such cases).

Lastly, I would say that after analysing a discount retailer that ended up making it into the portfolio, the bar is very high. Why would I buy B&M when I can simply add to a much healthier and more defensible business that’s “similar”? (it also has its drawbacks, of course). This is a question that I continue to think about.

(You can read the in-depth report of the other company that did make it into the portfolio here.)

What I am watching

I have not yet discarded B&M entirely, but I must say that I have grown increasingly concerned with the underlying business. How much is a business that has not delivered real growth over the last decade worth? Probably more than it’s worth today, but maybe not a return to historical norms. I will continue to watch the company closely in case there’s further evidence of a turnaround, but staying on the sidelines for now.

Let’s jump to the second company.