On The Radar #5

More injectables, a software business with proprietary data, and a distributor with a great track record

Welcome to the fifth issue of “On The Radar.” If you want to know what this series is about, I recommend reading the first issue.

Simply put, the goal is to share interesting companies that I’ve looked at but have not researched in-depth yet. You can think of the “On The Radar” series as a well-curated list of companies that fit my investment philosophy and that might (in the future) make it into the portfolio. So far I’ve only included in my portfolio 1 of the 12 companies I have profiled in this series, with good (but still early) results: +13% in about a month (there’s also an in-depth report available for paid subscribers).

Today’s issue brings yet another three companies (one for free and the remaining reserved for paid subscribers). Here’s what you can expect today:

A company that participates in the injectables supply chain with a pretty solid competitive position and great growth prospects

A software business that acts as the system of record in its industry and that owns proprietary data (I’ve been looking for a similar set-up for a while)

A distributor with a great track record in a secularly-growing industry that has entered other attractive and high-growth markets

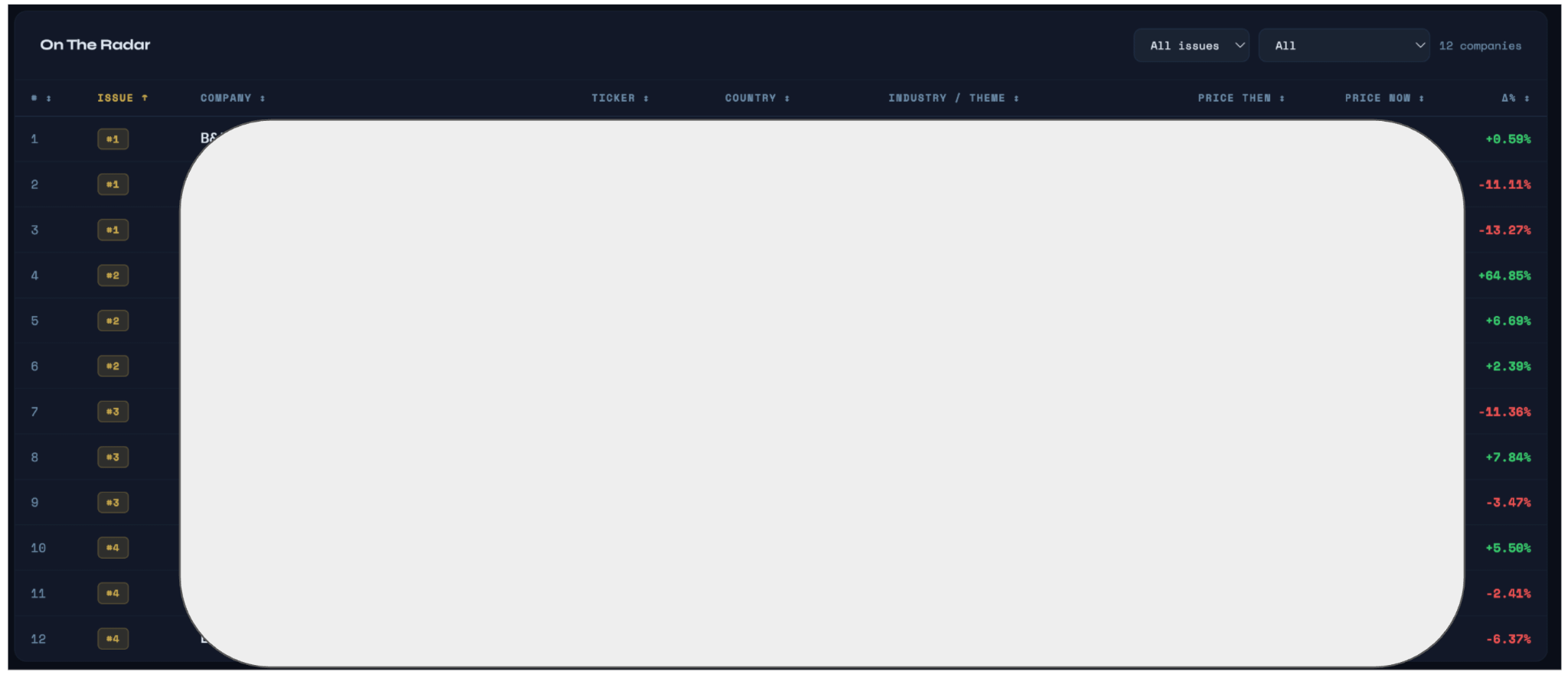

Note that all of these businesses get included in the “On The Radar” tab of the Portfolio Management Tool with their respective price evolution since the issue. These are generally companies that I don’t own but I find interesting so I prefer to see stock prices dropping across the board. Some have unfortunately done very well before I was able to make my mind up:

As this is the fifth issue, free subscribers have had access to 5 companies (one for free per issue) whereas paid subscribers have had access to 15.

So, without further ado, let’s jump into today’s issue which starts (again) with a Swiss company.

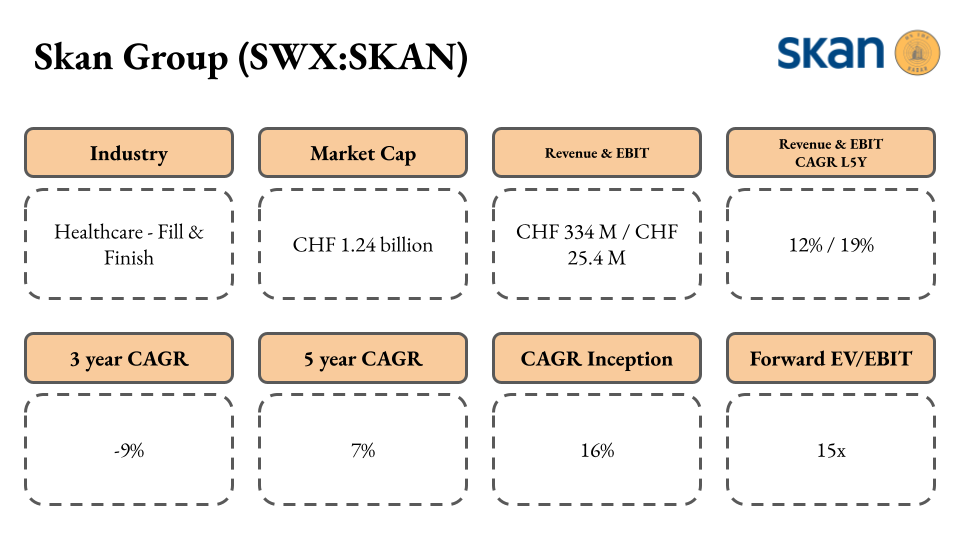

Skan Group (SWX:SKAN)

Brief description of the business

I believe this is the third consecutive issue that starts with a Swiss company. You might think that I have been scouting the Swiss stock market and I’m doing this on purpose, but that’s far from the truth!

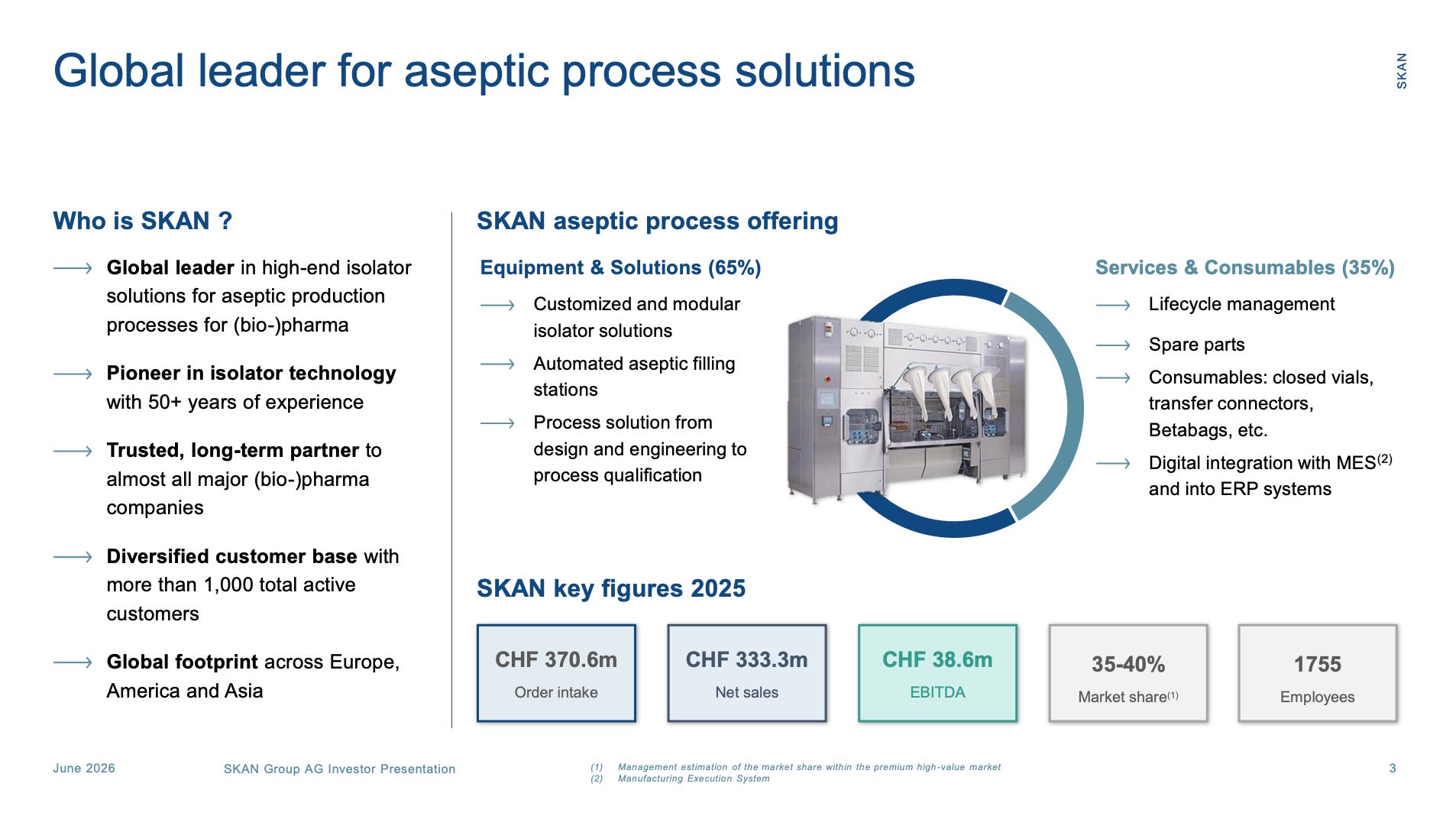

So, what does Skan Group do? Skan Group manufactures equipment relevant to the fill & finish process in the pharmaceutical industry. The company sells (primarily) isolators and automated aseptic filling stations and follows a razor-razorblade business model. Skan sells the equipment at a lowish margin but subsequently monetizes it through high-margin services and consumables:

Source: SKAN Investor Presentation

Injectable and sensitive drugs can’t be sterilized the same way that a pill can because the heat would destroy the compound, so they must be filled into their respective containers in an extremely “clean” environment. Just like with semiconductors, the most relevant threat in this process is the human being so isolators (such as the ones SKAN sells) help avoid any contact whatsoever with a human being:

So, an isolator is ultimately a tool that allows pharmaceutical companies to safeguard the drug’s contamination through the fill & finish process. Skan is the global leader in high-end isolators with a 35-40% market share.

Why it caught my attention

If you’ve been following my work for a while and you have seen my portfolio (paid subscribers know), you’ll know that I am pretty bullish on the secular tailwinds that SKAN can potentially benefit from. The company is poised to enjoy two main tailwinds:

Growth in injectables medicines (well documented and evident in the pipeline due to the rise of biologics)

More stringent regulations stemming from politicians wanting to regulate more and the increased complexity of biologics/ADCs

Pharmaceuticals like biologics, ADCs, cell and gene therapies…will most likely be delivered in an injectable format and will also face very stringent regulations in terms of contamination. This means that the demand for high-end isolators should theoretically grow as complexity rises, and this is precisely where SKAN excels. I think the trend is inevitable (my portfolio surely believes so!) and that many companies that potentially benefit from said trend are trading at attractive valuations. SKAN is undoubtedly a cyclical company exposed to the industry’s capex cycles (it has not been pretty over the past few years) but it’s currently trading at forward EV/sales under 3x despite holding a solid competitive position in a critical part of the value chain.

This doesn’t seem incredibly cheap, but it’s at the low end of what the company has historically traded for. So, three things ultimately caught my attention:

The secular tailwinds of the industry (already knew this)

SKAN’s role in the supply chain and its strong competitive position

The valuation

Companies like Danaher have been claiming for quite a while that the industry has underinvested in capacity after having digested the pandemic overcapacity and that a capex supercycle is “around the corner”:

I think the takeaway here is that, one, equipment investment has been muted here for the last couple of years, despite the fact that demand has been fairly strong, as we see in the consumables demand. There’s probably some catch-up required here over time just to meet the existing demand, and then you add on top of that, the reshoring topic, which continues to advance. There’s no question that is going to happen. It’s just a matter now of bringing that timing together, but we really believe we could be in the early innings of a long-term investment cycle.

The Capex upcycle has been around the corner for a while now, but we have started to see some green shoots. If the cycle is finally upon us, it bodes pretty well for companies like SKAN as they are exposed to a great degree to the capex of its customers. We’ll see.

What I like

I liked several things about SKAN:

It’s a good business with a leading position in its core market and “expanding” into several interesting adjacencies like Pre-Approved Services (other adjacencies do seem less “core”)

The company is preparing to launch a service called Pre-Approved Services that should materially shorten the validation time of its equipment. This should shorten validation timeline and should grant SKAN more pricing power and a better lock-in

It participates in an industry that I believe will enjoy considerable tailwinds going forward

The company is currently in a cyclical trough

The consumables/services mix is increasing. Management believes that services and consumables as a percentage of revenue will increase 800 bps over the medium term, something that promises to be pretty accretive to margins as S&C margins tend to be almost triple those of equipment (not rare in razor-razorblade business models)

Management believes that sales will grow mid to upper teens over the mid term (I imagine they are expecting an upcycle and wouldn’t take this as through-the-cycle growth)

What gives me pause

The main thing that gives me pause is execution and the financials. The future SKAN Group might look a lot better than it looks today (this is what we should care about as investors) but the reality is that profitability has been considerably impacted in FY 2025 and that it’s a cyclical business. All good so long as it’s indeed a cycle and the business eventually recovers. I must say that the guide for FY 2026 sort of confirms that the 2025 figures might have marked the “bottom”: management expects upper teens growth and a strong recovery in EBITDA margins.

The other thing that gives me pause is the “moat.” Even though the company has a head start in terms of high-end isolators, it’s not alone in the market and there are no “drug-master-file” style switching costs.

What I am watching

I am looking to learn more about the company and understanding whether the ancillary services the company is introducing are a game changer or not.

Let’s now jump into the next company which I’d say is the one that excites me the most in this issue.