On The Radar #4

A boring Swiss industrial with AI exposure, cybersecurity, and a boring and unexpected 20%+ compounder

Welcome to the fourth issue of “On The Radar.” If you want to know what this series is all about, I recommend reading the first issue. I have already shared nine companies across the first three issues, and today’s issue brings another three (one for free and the remaining reserved for paid subscribers). Here’s what you can expect today:

A Swiss industrial with a leading position in a key product in the data center buildout

A cybersecurity company with defensible competitive advantages (and that has positive GAAP earnings!)

A rather special serial acquirer (you probably don’t expect it) with a great track record and in a defensible industry

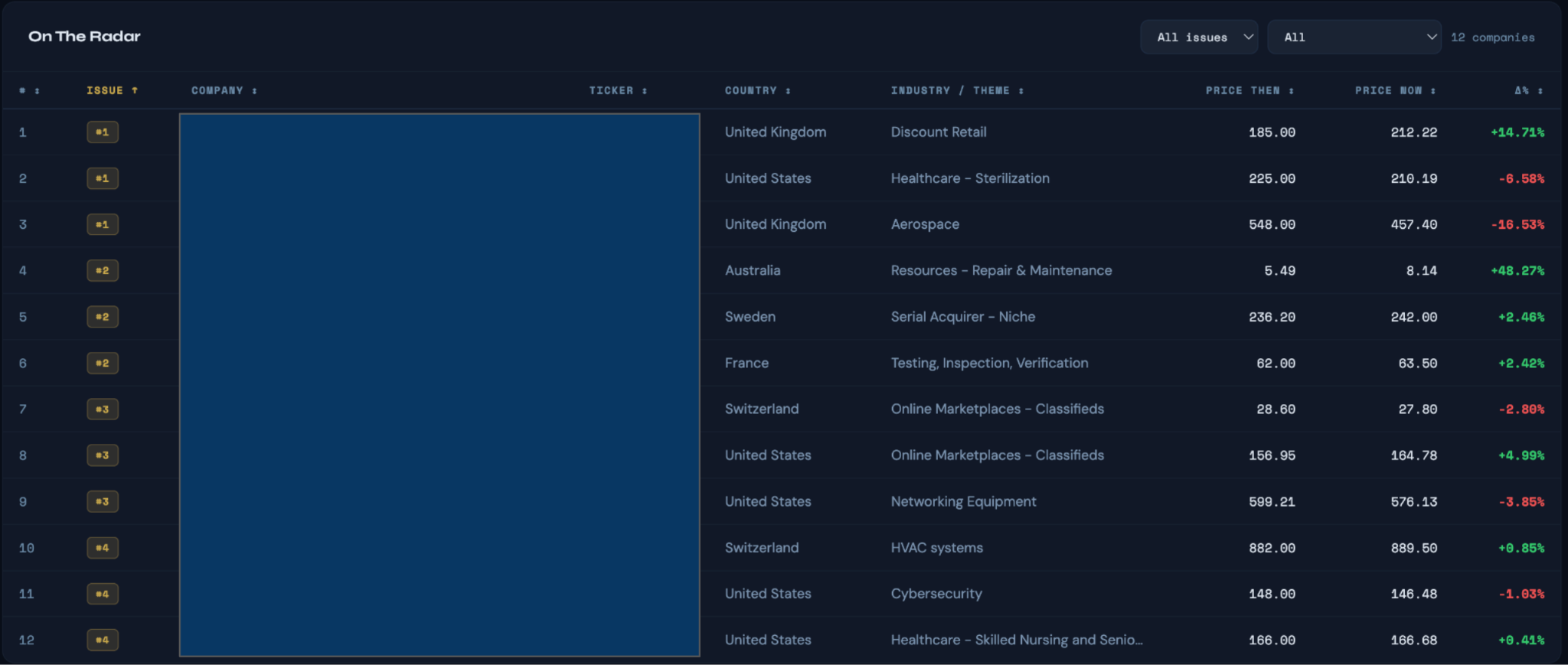

All of these businesses get included in the “On The Radar” tab of the Portfolio Management Tool with their respective price evolution since the issue. These are companies that I don’t own but I find interesting, so in most cases what I want to see is stock prices dropping across the board. Some have unfortunately done very well before I’ve taken action and I’ve included one company in this list to my portfolio so far:

So, without further ado, let’s jump into today’s issue!

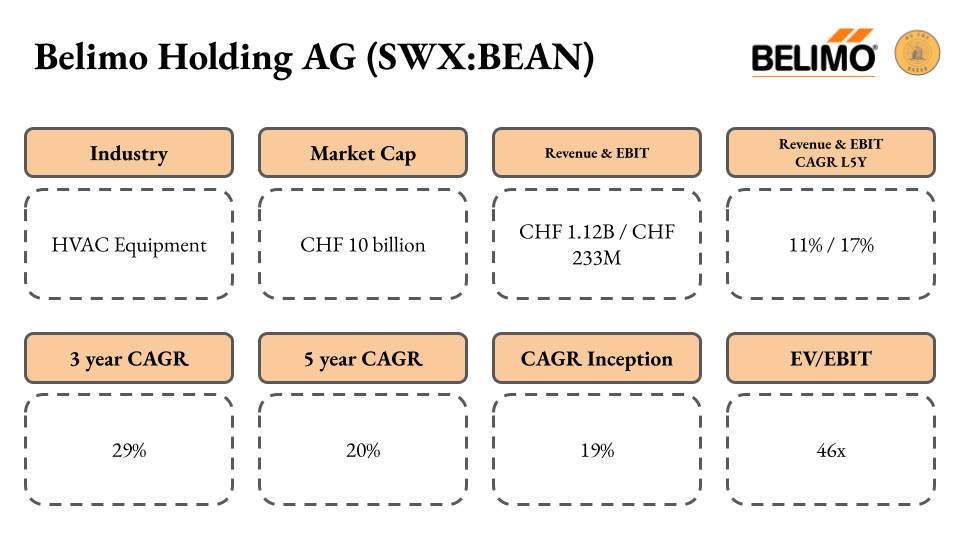

Belimo Holding (SWX:BEAN)

Brief description of the business

This fourth issue starts with a Swiss company, just like the last. Belimo is specialized in HVAC equipment, and even though this might seem quite boring at first glance, digging deeper is advised.

Two products are responsible for the great majority (+90%) of the company’s sales, and they rely on a very similar technology:

Damper actuators: a device that controls the opening and closing of a damper to control the airflow

Control Valves: basically the same as a damper actuator but instead of controlling air they control gas and liquid

Even though the above might not seem like rocket science, Belimo has carved itself a leadership position on both products thanks primarily to its focus. Unlike competitors who typically offer them as part of E2E portfolios, Belimo is specialized only on these two critical products. Why are Belimo’s products so critical? Because ultimately the delivery of the HVAC system is entirely dependent on how the actuators and valves work. This is pretty straightforward if we use the human body as a proxy: there’s little use for the heart beating if there are no valves controlling the blood flow.

Due to its expertise and technological advantage, Belimo boasts global market shares in the 20-30% range. So, it seems like a pretty good business!

Why it caught my attention

The business caught my attention for two main reasons. First, the underlying business is good in its own right. Now, the second (and most important) reason was that it’s exposed to several secular tailwinds that could accelerate the business’ growth profile (we are already seeing this play out). Belimo is exposed to secular tailwinds like…

Liquid cooling in data centers

Semiconductor fabs

Pharma manufacturing

Energy efficient construction (both commercial and residential)

All of these segments have two requirements, which is precisely where Belimo excels: energy efficiency and reliability. Seeing an apparently “boring” company directly exposed to so many long-term secular tailwinds is great news, but it comes with a drawback that I’ll discuss later.

What I like

There are a lot of things I like about Belimo. Namely:

It’s exposed to many long-term secular tailwinds (discussed above)

The founding family still retains a 20% stake

Management has a significant tenure (the CEO has been serving since 2015), which means that long-termism spans the organization

Compensation is based on sales growth, EBIT margin, and ROCE, so it’s unlikely there’s a growth-at-all-costs mentality

The company is currently undertaking a significant capacity expansion plan in the US and Asia, which portrays the believe there’s demand durability

It has a defensible position due to technological leadership and the high cost of failure of its products

The company trades in Swiss francs, which one might think that it can continue its long-term appreciation against the Euro and the Dollar (I’m not in the business of forecasting FX, though)

There are lots of things to like about Belimo, but there’s one thing to dislike: its valuation.

What gives me pause

The only thing that I don’t like much at this point is the company’s valuation. Management has set a LT growth target of 6-9%, but it has grown above this target for two consecutive years and expects to do so for a third year in a row:

2024: +13% YoY

2025: +23% YoY

Expected 2026: mid-teens growth

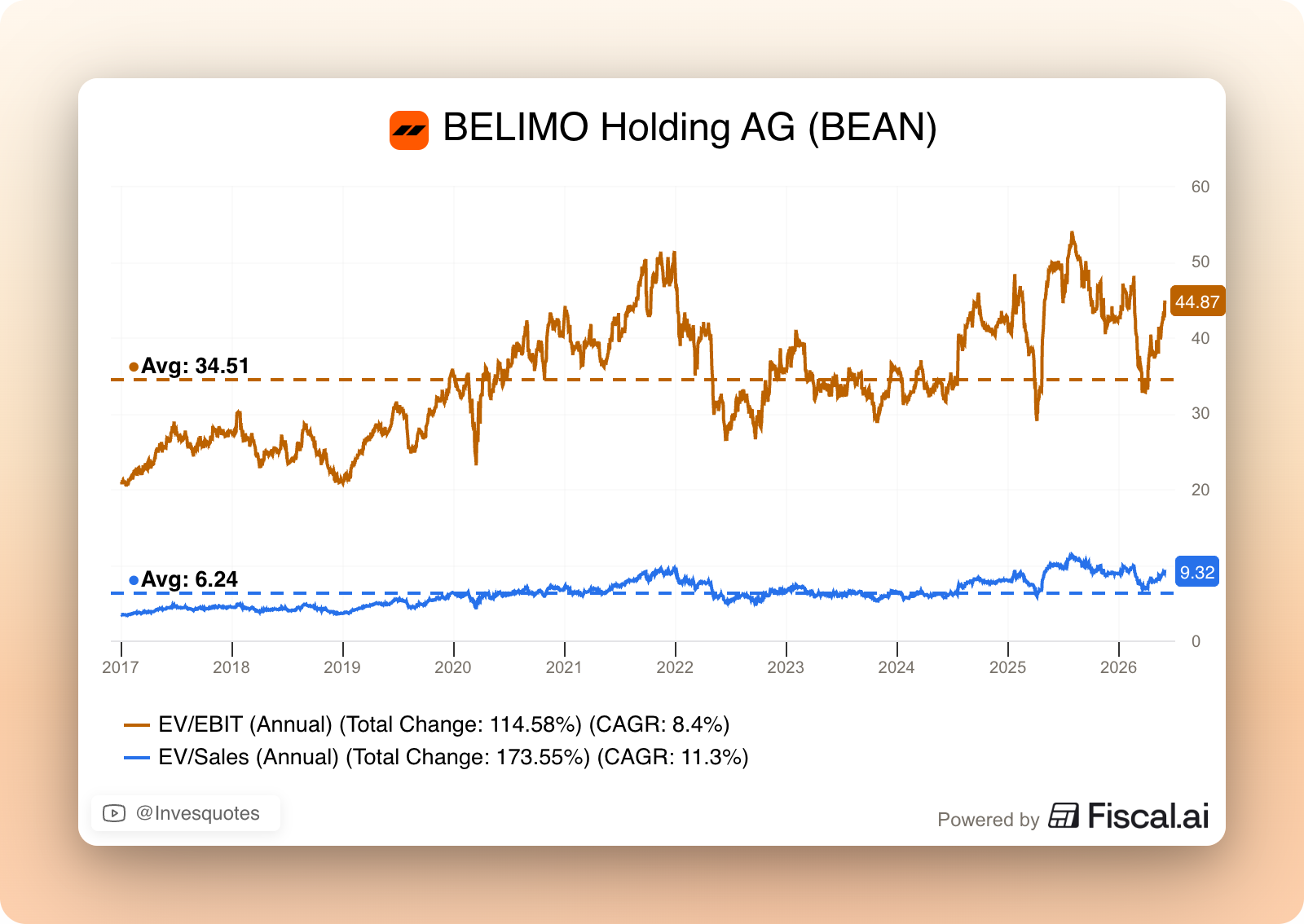

This has evidently resulted in multiple expansion, with Belimo currently trading at 9x sales and 45x EBIT. The company has historically traded at seemingly “rich” multiples (likely due to its defensible competitive position), but this seems a bit on the high side:

If I assume that EBIT growths at a 20% CAGR over the next 5 years (significantly above its LT history) and that I exit at a 30x EBIT multiple (still pretty high), my CAGR would be around 10%. It’s not disastrous, but that’s some heavy assumptions one has to make to get to a double digit return.

What I am watching

I will include the company in my watchlist in case the valuation comes back to more acceptable levels. Things can move fast in this market and you can see this in the graph above: the EBIT multiple was close to 30x just this year! Patience will most likely get rewarded, and if not, we’ll move on to the next one!