On The Radar #3

An amalgamation of monopolies, a marketplace with “AI-risk”, and a true outsider running a cyclical business

Welcome to the third issue of “On The Radar.” If you want to know what this series is all about, I recommend reading the first issue. I have already shared six companies across the first two issues, and today’s issue brings another three (one for free and the remaining reserved for paid subscribers). Here’s what you can expect today:

A company that owns several monopolies that benefit from network effects (no, it’s not Meta)

A platform company currently viewed by the market as an AI loser (I don’t think the market is right on this one)

A network equipment business run by what I would consider a very unconventional outsider

So, without further ado, let’s jump into today’s issue!

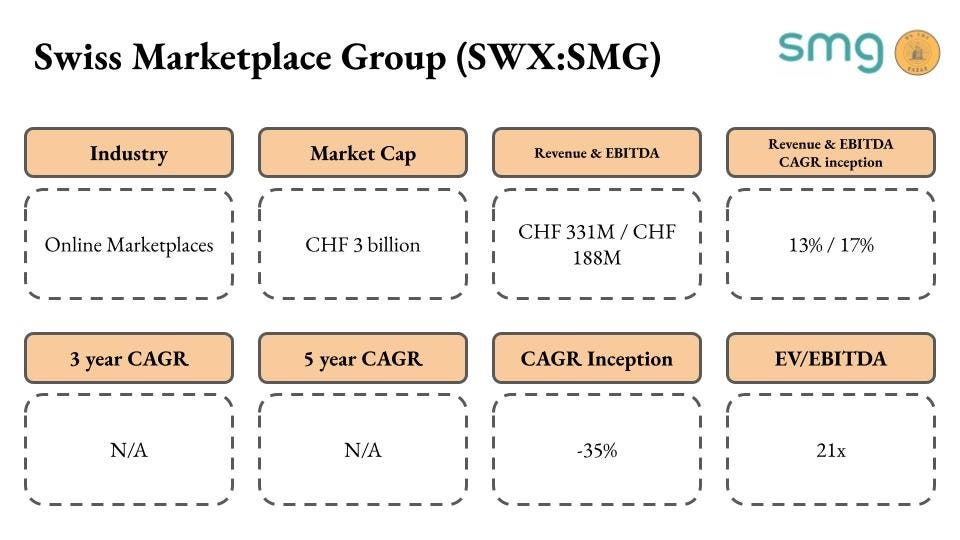

Swiss Marketplace Group (SWX:SMG)

Brief description of the business

SMG owns and operates several leading online marketplaces in Switzerland (the company’s name seems quite appropriate). The company owns…

The two leading real estate marketplaces: Homegate and InnoScout24

The leading automotive resale platforms: AutoScout24, MotoScout24, and Car For You

Several leading C2C goods resale platforms: Ricardo, tutti, and anibis

The business model of online marketplaces (also known as classifieds) is pretty straightforward: two users transact, and the marketplace operator (in this case SMG) takes a cut of the transaction and offers other services to the buyers and sellers.

SMG was born pretty much “overnight” in 2021 through a joint venture that seems almost impossible to think of now (were the regulators sleeping at the wheel?). Prior to 2021, Switzerland’s Classifieds Industry was dominated by several players, namely…

TX Group: owned Homegate, Ricardo, Tutti, and Car For You

Ringier and Die Mobiliar: jointly owned Scout24

These businesses were good businesses in their own right, but knowing that the Classifieds market tends to exhibit winner-take-all dynamics, the three parties decided to contact General Atlantic (a PE firm) to merge both platforms with the goal of making them more efficient and dominant. The result was a Swiss monopoly: SMG.

Why it caught my attention

The business caught my attention primarily because classifieds are very attractive businesses that exhibit winner-take-all dynamics thanks to network effects. If the “supply” is using a given marketplace, then it’s highly likely that the “demand” is also going to be using that marketplace. More supply brings more demand and viceversa, which feeds into a network effect that creates formidable entry barriers.

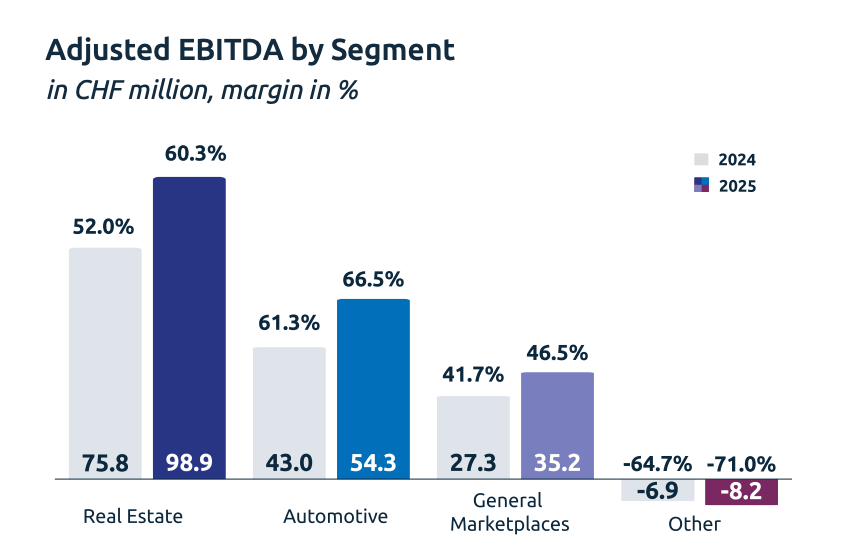

What’s more intriguing/exciting about this story is the huge margin differential that exists between SMG and its peers. Classified businesses in other countries exhibit very high margins. The reason is that, once the infrastructure is in place and the network effect reduces customer acquisition costs, revenue growth falls pretty much in its entirety to the bottom line. Many of these businesses have shown that EBITDA margins in the 60%-70% range are not out of the question, but SMG reported an Adjusted EBITDA margin of 54% in FY 2025. This means there’s a long margin expansion runway (and all while the company continues to grow its top line in the double digits!).

The belief that 60%-70% margins are “doable” also feeds into management’s medium-term growth algorithm:

Mid‑term guidance communicated at IPO confirmed: Revenue growth in the low 10% range and Adjusted EBITDA margins in the low‑to‑mid‑60% range.

The fact that is doable is also already apparent in the company’s own numbers, with Real Estate and Automotive already performing above the 60% mark:

Source: SMG Annual Report

The company is currently trading at around 17x 2025 Adjusted EBITDA and 21x reported EBITDA, which doesn’t seem expensive for a business expected to grow its top line low double digits and with (potentially) 1,000 bps in margin expansion ahead.

What I like

I believe that what I like has already been encompassed above, but let me summarize it here:

It’s a good, defensible, business that enjoys “monopoly” status and where a good chunk of the EBITDA growth will come from the margin expanding to “industry norms”

Management is focused on the margin expansion opportunity but the business continues to grow at a good pace (I’d imagine that taking significant price)

The valuation appears attractive

Now, there are also several things that I don’t like as much.

What gives me pause

There are mainly three things that I worry about, two of which are related. Let’s start with the ones that are related: regulatory pushback and organic opportunity.

Even though the regulator allowed the merger to pass (incredible), SMG is already facing some pushback around its dominant position. The company announced in January that it had reached an “amicable” agreement with the Swiss Price Watchdog:

SMG Swiss Marketplace Group has reached an amicable agreement with the Price Supervisor regarding Ricardo and SMG Real Estate. As a result, the Price Supervisor is discontinuing its informal investigations in both fields. This provides SMG with legal certainty in this regard for the next three years.

While this is good news “for the next three years” the reality is that the regulator is already keeping an eye here and this can potentially constrain the organic growth opportunity. The good thing about owning classifieds is that one is likely to be protected from external competition. The bad news about owning classifieds is that expanding abroad is very challenging because there’s likely established classifieds elsewhere. This means that once you become dominant the opportunity basically becomes one of cross-sell and price hikes.

The other thing that “worries” me is the IPO hangover. The first lock-up has already expired (March 2026) but there’s another one coming up in September so we’ll have to see how the shares react to that.

What I am watching

I have to gain more clarity into the regulatory aspect here. The reality is that every good “monopoly” is likely to face regulator/political scrutiny, but that in and of itself is a great indicator of how dominant a business is.

Let’s go with out next business.