On The Radar #2

A recurring resources business, a nordic serial acquirer, and a testing business trading (demonstrably) cheap

Welcome to the second issue of “On The Radar.” If you want to know what this series is all about, I recommend reading the first issue where I shared a detailed explanation. In the first issue I share the following three businesses:

A troubled retailer (in essence a turnaround story)

An interesting healthcare business

An above-average aerospace business trading at a reasonable valuation

Today’s issue brings 3 companies that are significantly different to those shared in the first issue (remember that only the first one is free to read, with the remaining 2 being reserved to paid subscribers), namely…

A repair and maintenance business with more recurrence than one would suspect (albeit less than management claims)

A Nordic serial acquirer that went from favorite to hated relatively quickly

A testing business operated by a proven outsider that just revealed something interesting related to its valuation

I was going to write about another business for the third spot (a capital markets intermediary), but an interesting business that I have been following for a while reported earnings and I decided to switch it up. I will most likely write about the other business in the future.

So, without further ado, let’s jump with today’s issue!

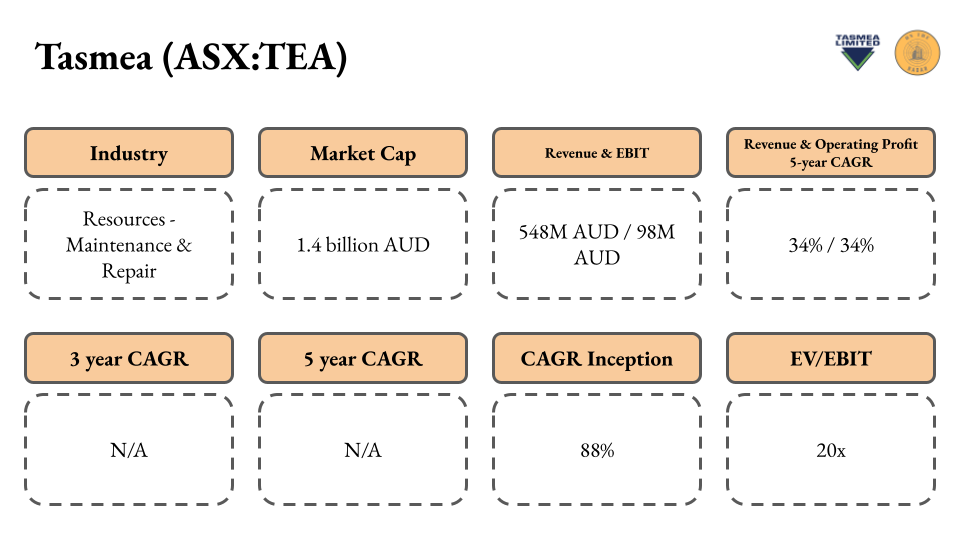

Tasmea (ASX:TEA)

Brief description of the business

Tasmea offers specialized repair and maintenance services to customers that operate primarily across the resources industries (mining, oil, energy, water…). The company operates across 4 segments (electrical, mechanical, civil, and water & fluid) and a wide variety of “brands:”

Source: Tasmea Investor Relations

The business grows both organically and inorganically (integrating specialized services businesses) and its track record is exceptional: 34% revenue CAGR since FY 2021. What Tasmea ultimately does is sell labor to keep the operations of its customers up and running.

Why it caught my attention

Tasmea caught my attention for several reasons, but the three most important ones were…

Management’s alignment with shareholders

The company’s growth opportunity (both organically and inorganically, albeit the former needs context)

The apparently undemanding valuation

Insiders own a significant chunk of the business and continue reinvesting their dividend proceeds into new shares. Simultaneously, the company’s growth doesn’t seem to be slowing down, and all while it trades at 17x pro-forma 2026 NOPAT. Now, this doesn’t seem like a bargain multiple for a services business operating in the resources industry (one could assume these industries have low organic growth and are cyclical), but its growth track record in terms of organic growth and resilience surely backs it up. I would have assumed organic growth would be much lower, and even though it’s high (the company strives for >15% organic EBIT growth), it requires context.

What I like

In no particular order, here are some things I like about Tasmea:

The business was not publicly traded during the GFC in the same shape or form as what it is today, but it seems to have grown through commodity downcycles. This portrays that the maintenance and repair services the company provides are mission-critical for its customers operations and relatively independent from commodity pricing

Management is aligned with shareholders and plans on retaining a significant stake going forward

The compensation structure is decentralized and focused on organic EBIT growth of 15%+

Tasmea’s industry is fragmented, which not only means there’s less “credible” competition to chase organic growth but that there’s also a significant inorganic opportunity

The production of many resources that Tasmea’s customers are exposed to and the electrification trend seem secular (resources are not going away anytime soon)

The company seems to be trading at a decent valuation all things considered

What gives me pause

There are a couple of things that gave me pause and that require additional research on my side: the Workpac acquisition, the fact that I don’t think the business is as recurring as many (and management) claim, and the fact that we don’t have a clear organic growth number (not saying it really matters at the current valuation). Let’s take a look at these individually.

The Workpac acquisition: Tasmea’s (and peer’s) main factor constraining growth is labor. The reason is that there’s a lack of specialized technicians, a shortage that is only compounded when the repairs and maintenance have to be conducted in remote areas (Tasmea’s bread and butter). To “solve” this problem, Tasmea diverted from its typical acquisition target and acquired Workpac, a company that focuses on “acquiring” this talent and later subcontracting it to Tasmea and its peers/customers. Management believed that insourcing this capability would result in a competitive advantage in terms of technician availability. While this makes perfect sense, the reality is that Workpac is a different beast to what Tasmea has historically acquired and operated, so it introduces execution risk, cyclicality, and less recurrence.

The recurrence of the business: management claims that, due to the mission criticality of its services and the fact that these are focused on production and not capacity expansion, makes the business pretty recurring. Management explicitly shares that 80% of the business is recurring (according to their own definition), but their definition of recurring differs from what I would consider recurring because it includes brownfield investments/upgrades. I would not say these are as recurring as the company’s maintenance activities, but it’s also true that they are driven by regulatory tailwinds (electrification). To this we must add that the inclusion of Workpac makes the business less recurring as well. I do believe it’s a decently recurring business, but not to the extent that management shares (and I believe the market is also aware of this and it’s fed into the multiple).

No clean organic growth number: even though Tasmea boasts a 15% organic EBIT growth target, the reality is that this target is inclusive of acquisition synergies. When Tasmea acquires a business, they typically use it as a platform to cross-sell the services of other subsidiaries. While this growth is definitely counted officially as “organic” the reality is that it’s dependent on a continuous stream of acquisitions. This is not a problem yet, but it might become a problem in the future and the reality is that there’s no way of knowing what true organic growth (ex-acquisitions) would be in that scenario.

What I am watching

There’s nothing too specific that I am looking for, I just need to do more research to get comfortable (or not) with the three things I shared in the “what gives me pause” section.

Let’s jump to the second business.

If you want to have exclusive access to On The Radar Issues and…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

(The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.)

Consider becoming a paid subscriber: