NOTW #14: An Individual Investor’s Take On Opportunity Cost

Don’t forget that Best Anchor Stocks has a partnership with Finchat (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

Hi reader,

Indices were somewhat up this week, although their performance over the last couple of months is leading to some (unfounded) frustration across investors. I tie this frustration to the concept of opportunity cost and why individual investors should see this topic differently than professional investors (and why this is their main advantage).

Without further ado, let’s get on with it.

Articles of the week

I published one article this week, my answer to Spruce Point’s Short Report on Intuit.

I thought it was a weak report showing Spruce Point doesn’t understand Intuit. I do agree, however, with the main conclusion of the report, which is that the stock does not seem cheap here.

Next week, I’ll publish two articles (maybe three, depending on how things go). I will unveil a new feature for Best Anchor Stocks’ paid subscribers, which should help directly answer the question, “What companies do you feel are good buys today?” The second article will discuss one of the main flaws of the indices and how we can take advantage of them. I will write the third article highlighting Intuit’s recent investor day if I have time.

Market Overview

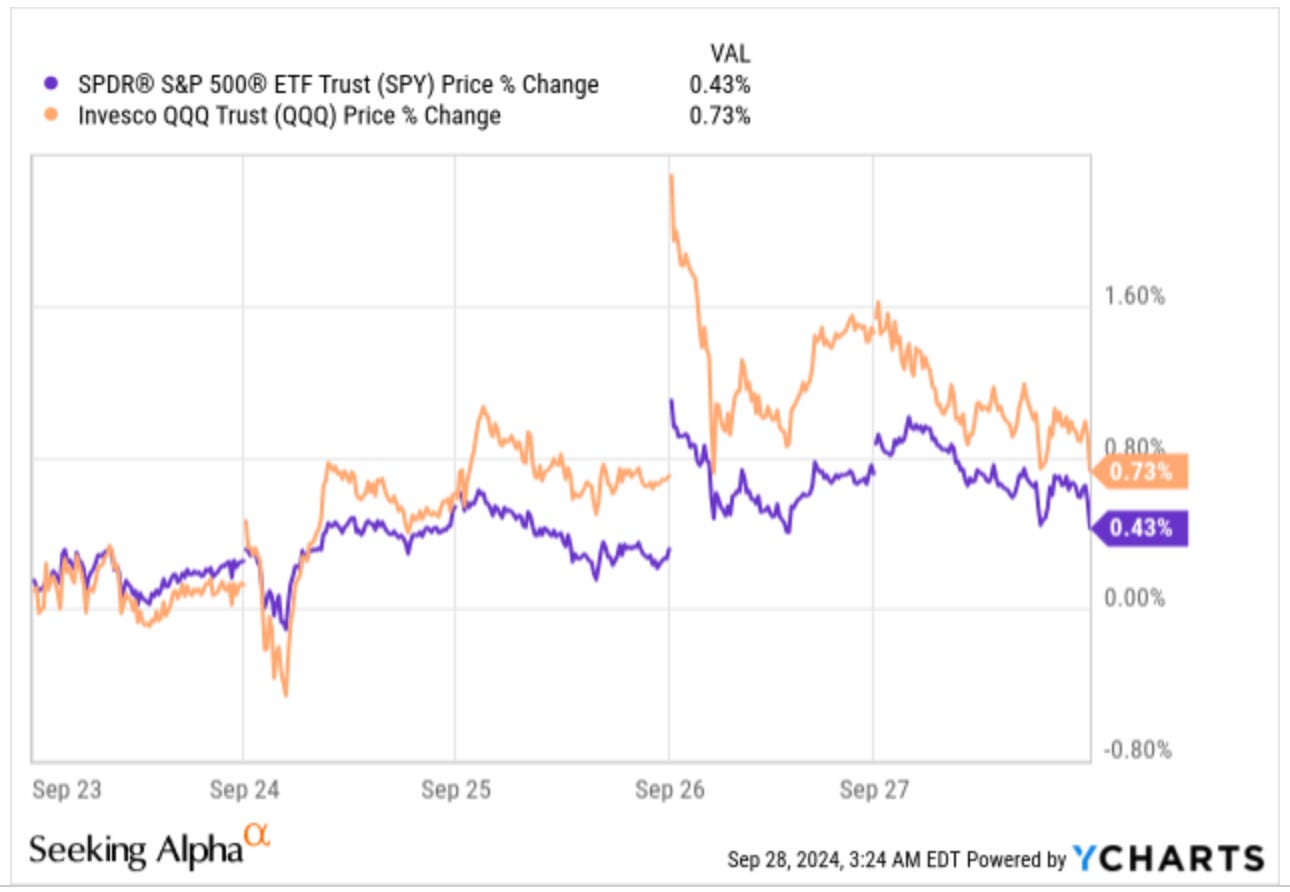

Indices were somewhat up this week, but not without significant volatility. The Nasdaq rose 0.7%, whereas the S&P 500 rose 0.4%:

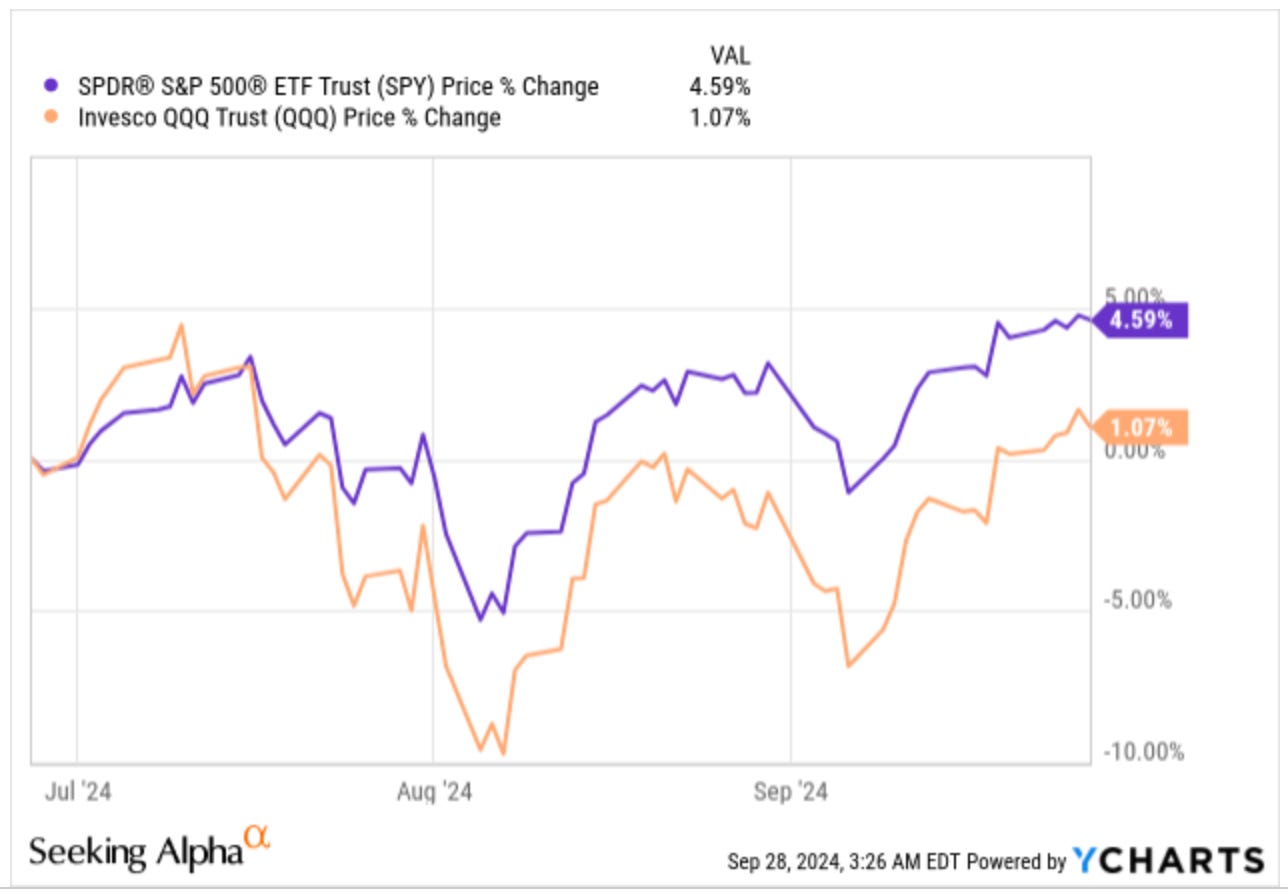

If we zoom out, we can see that indices have been “chopping wood” for the last 3 months or so despite both being up. The S&P 500 rose more than 4% over that period, whereas the Nasdaq rose 1%. It has been undoubtedly a “roller-coaster” despite the positive performance:

This behavior has frustrated many investors, which is quite surprising considering that both indices are up considerably year to date. Maybe people think that indices can only go up (recency bias), and while not many people are thinking about a potential crash or correction, this is precisely the time when we should be preparing for one (fyi, I am not calling one!). If one starts preparing (psychologically) for a crash when it’s already here, then there’s a high probability they will act in an irrational manner. The interesting thing about the stock market is that risk is the highest when it appears the lowest (i.e., when it has gone up considerably), but it’s the lowest when it appears the highest (i.e., when it has gone down considerably). That’s probably what makes investing challenging; you must swim against the current when it gets extreme.

People always want to hold the companies that are going up, which leads to markets being driven by the momentum factor. While the momentum strategy sounds very profitable at first sight, it’s not only very tough to implement but also pretty risky because the more things go up, the riskier they become (all else things equal, of course). The momentum strategy has gained popularity mainly because investors (professionals) hate opportunity cost, mostly because it’s a “real” cost that shows up in performance statements. The reason is straightforward: it’s not the same to make a 100% return over 5 years rather than over 7 years; the CAGR in the second case is lower than in the first, and oh boy, do professional investors care about CAGR! I’ve always thought that one of the advantages of being an individual investor (and therefore not being exposed to the industry’s incentive structure) is the ability to take on opportunity cost if one believes the risk of permanent capital loss is limited.

There are many companies that most professional investors will not be willing to hold at times despite their quality (this applies to entire industries as well). These tend to have some characteristics in common:

They are somewhat cyclical (which doesn’t mean that they can’t be secular over the long term)

They are going through a significant capacity expansion phase

They are currently facing temporary headwinds, maybe created by the pandemic’s stocking/destocking issues

These characteristics tend to put downward pressure on the stock because nobody wants to be left “holding the bad.” This situation, in my opinion, creates significant opportunities for individual investors. If one recognizes the value in such opportunities, they shouldn’t worry too much about when the recovery will come so long as they believe there’s a high probability that it’ll eventually come. The reason is that if many investors are aware of the headwinds, it’s likely that these will probably be priced in (to an extent), meaning that the risk of permanent capital loss is limited (if and only if the recovery eventually comes). It’s simply a matter of acknowledging that timing the exact recovery is almost impossible and therefore one should be willing to take on some opportunity cost if the value is there. Like most things in investing, there’s a trade-off.

Recall that one of the advantages of any individual investor is not needing to justify their performance or compare it to any index in a given period. Taking on opportunity costs might create some periods of underperformance, but it might also significantly diminish the risk of permanent capital loss. What seems clear is that it will be tough to find a good investment when everybody thinks it's a great company and the future is rosy. It happens rarely, but there are moments when few are willing to hold a quality company when things turn south (even if temporarily). One of the reasons might be what I have discussed above (nobody is willing to hold an underperformer), and another reason might be related to optically high valuation multiples created by temporarily depressed earnings. This leads to the classic comment of…

It’s down 30% and it’s still trading insanely expensive!

This is undoubtedly sometimes true, but in most cases, it misses normalized earnings.

I would also like to discuss the topic of China, and whether it’s the next multiyear opportunity, but I have absolutely no idea, so I’ll leave that to the Teppers and Burrys of the world.

The industry map was mixed, with semiconductors being the exception across tech-world. The reason might be related to Micron’s earnings, which portrayed that the industry is not doomed (at least for now) and that semiconductors will be required in increasing amounts in the future:

The fear and greed index remained in greed territory:

The rest of the content where I provide my transaction activity and the news of the week for the company’s in my portfolio, is reserved for paid subscribers. You can read all the deep dives I’ve released to date in this link.