Spruce Point's Short Thesis on Intuit

One of the weakest I've ever read

Hi reader,

You might have seen that Intuit was the subject of a short report by Spruce Point last week. It was one of the weakest short reports I have ever read, but I agree with the main message: Intuit does seem expensive here, all things considered.

As you might know, I am not a huge fan (or even remotely) of shorting because it eliminates an equity investor's main advantage: having a capped downside while a potentially limitless upside (i.e., the risk-return is skewed favorably). However, I think it’s interesting to read such reports to be aware of a company's weak spots. I don’t think, however, that a 125-page report (like the one Spruce Point published) is necessary to claim that a business is expensive, and I also don’t think that shorting based solely on valuation is the most profitable shorting strategy (albeit I am not an expert in the topic). How they get to their downside scenarios and overvaluation thesis is also pretty misleading, and the comps used are more than questionable.

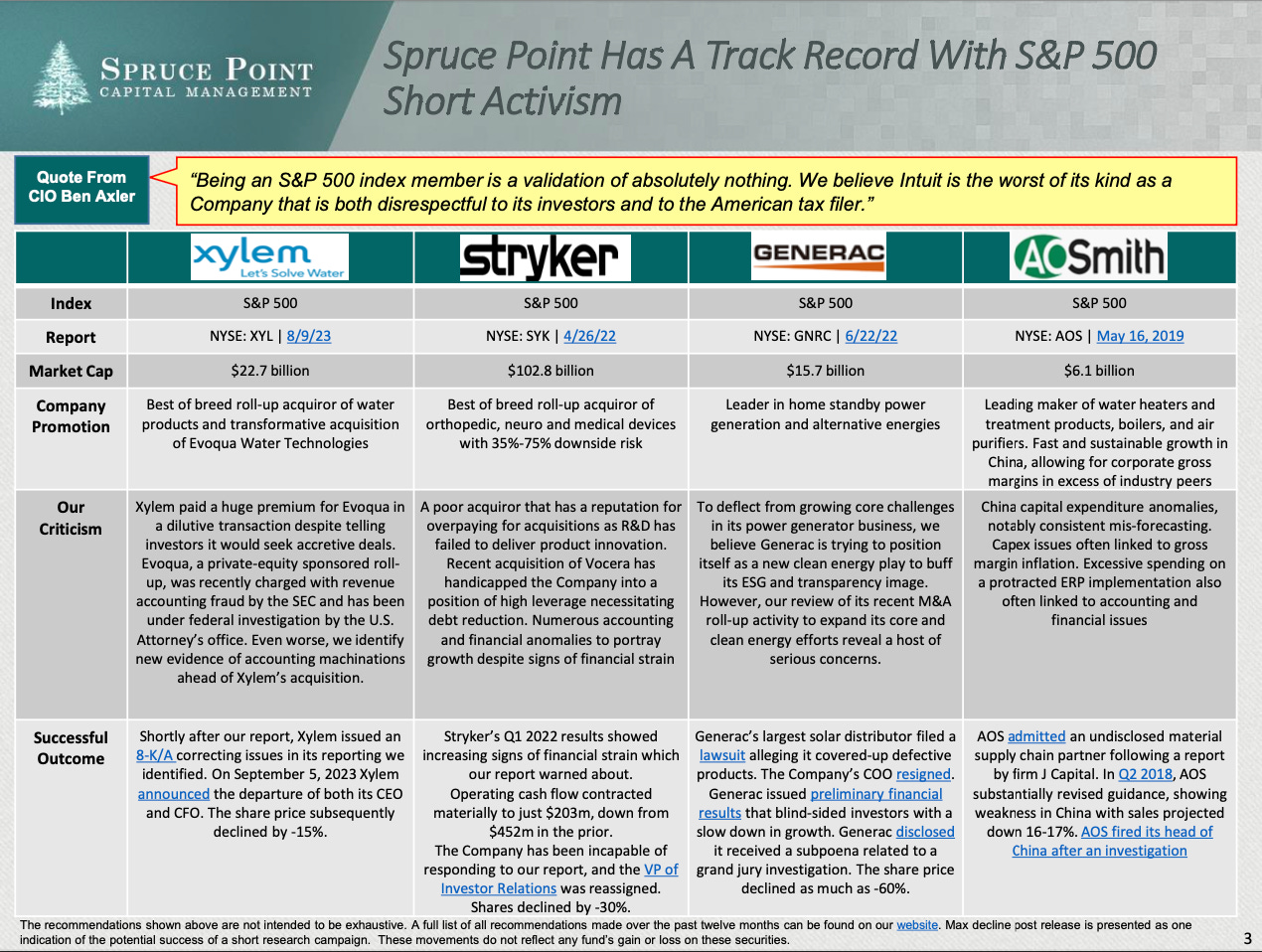

Interestingly, the report starts with Spruce Point’s track record in shorting S&P 500 companies. The company claims its track record is great, but I believe the slide used to prove this point proves the opposite. Spruce Point uses 4 companies to “defend” its track record: Xylem (XYL), Stryker (SYK), Generac (GNRC), and AO Smith (AOS):

Here’s how these companies have performed against the S&P 500 since Spruce Point’s short report:

XYL +32% vs the S&P 500’s +33%

SYK +47% vs the S&P 500’s +38%

GNRC -36% vs the S&P 500’s +46%

AOS +89% vs the S&P 500’s +100%

To this we must add the short report Spruce Point issued on XPO Logistics (one of Brad Jacob’s companies) in 2018. Brad Jacobs conducted shortly after one of the largest buybacks in the history of the company and the stock is up 400% since that report.

Rather than proving that they are good at shorting S&P 500 companies, the above slide seems to prove just the opposite, and it honestly seems ironic (I thought it was a joke at first). They claim these stocks went down briefly after the short report was published, but this shorting strategy seems more like one of market manipulation rather than one based on shorting skill. When reputation is permanently impaired, it will be tough to profit even over the short term from these short reports.

Anyways, while they do not have a great track record in shorting, I think it’s useful to go over the report (one never knows if Intuit might be the next Generac, i.e., a successful short report). I’ll touch on some points discussed in the short report to explain why I think it was a very weak report. I will then look at the valuation using methods different from those used by Spruce Point.