New Horizons

Constellation’s Q4 2025

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of subscribers today:

Constellation Software reported very good earnings today. As you may know, the company’s stock has not been immune to the SaaSpocalypse narrative, but investors’ fears should’ve been calmed a bit post-earnings. For several reasons…

There’s no noticeable impact of AI in the numbers yet

Management provided interesting (albeit qualitative and subjective) comments as to what they expect the AI impact to be

AI fears have actually enlarged Constellation’s capital deployment opportunity

The stock has recovered somewhat from the lows but still remains far away from its all-time highs:

I believe there were several interesting things in the numbers worth discussing.

A quick look at the numbers

Revenue grew at a good pace in Q4 and FY 2025 and Constellation should be now considered as an “accelerating top line.” Interestingly, the company enjoyed somewhat significant margin expansion. Expenses grew 100 bps slower than revenue in Q4 and 200 bps slower for the full year:

Source: Constellation’s Q4 MD&A

What I found particularly interesting about the margin expansion was its source. “Staff” makes a disproportionate amount of the company’s expenses, and these grew considerably slower (+11%) than revenue (+15%) for the full year:

Source: Constellation’s Q4 MD&A

The optimist in me wants to believe that the differential here was driven by increased AI efficiency. This would mean that AI is currently being accretive to the numbers (which would be somewhat of a narrative violation for many). Now, the realistic in me is aware that Constellation comes from a period of slightly slower capital deployment through which the business typically gets more efficient (either way, good news for shareholders).

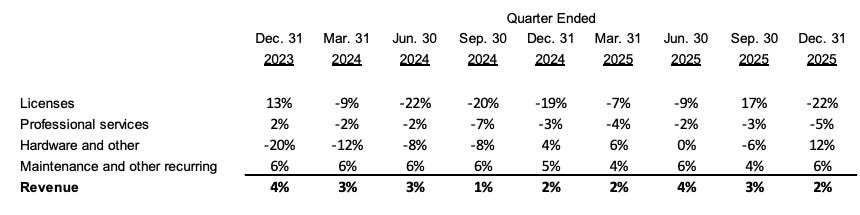

Investors probably had their eyes on organic growth to gauge the impact of AI. Organic growth (constant currency) was 2%, but organic growth (again, constant currency) in maintenance and recurring was 6%. This was in line with previous quarters:

Source: Constellation’s Q4 MD&A

Several things worth noting here. First, Mark Miller claimed during the call (first call since 2018) that AI has not driven an organic acceleration (at least not yet), but that it had not resulted in loss revenue either (i.e., it’s business at usual at Constellation for the time being):

We haven’t really seen a lot of new revenues from that, right. You know, so far. And on the contrary, we haven’t really seen loss of revenues from it. You know, at this point. So it’s been really. Really just we’re really just in the process of just bringing everybody up to speed and making sure they, they can use the tools and they know as much as they can across our, across our businesses.

I believe the organic growth in licenses (-22%) also requires some context. Constellation typically converts license contracts to maintenance and recurring contracts (spoiler alert, because they are more recurring) when it acquires companies. This means that it’s natural to see significant volatility in other items besides maintenance and recurring. So, all in all, nothing worrying on the organic growth front.

I would personally completely ignore P&L earnings and focus on cash flows. P&L earnings were negatively impacted by the IRGA revaluation charge and the reclassification of the Asseco stake. Add amortization of intangibles, and P&L earnings become entirely misleading for CSU.

Operating Cash Flow grew a whopping 24% in 2025:

Source: Constellation’s Q4 MD&A

Free Cash Flow available to shareholders was a different story; it contracted in Q4 and “only” grew 14% in FY 2025. Now, as I discussed in my article ‘Hidden Value in a Liability’, we should ignore the IRGA liability revaluation charge to correctly assess Constellation’s earnings power. The IRGA grew significantly in 2025 and pressured FCFA2S, which would’ve grown 27% YoY excluding this item, ahead of Operating Cash Flow.

All in all, the financials don’t seem to portray that this is a dying business, but in all fairness to the skeptics, the AI threat “promises” to be a long-term threat in nature rather than one of immediate disruption. FCFA2S excluding the IRGA was $2.12 billion in 2025. At Constellation’s current EV of $46 billion, the company is trading at an EV/FCF yield of 4.6% while growing cash flows above mid-teens and potentially accelerating capital deployment.

Let’s talk about this a bit more.

The spectacular capital deployment and a new lever

The main highlight (besides no noticeable AI impact) for Constellation was capital deployment. Let me briefly share some data. Constellation deployed (these are all-inclusive numbers, so CSU+TOI+LMN)…

>$2.1 billion into acquisitions and investments in FY 2025. Considering that all-inclusive FCFA2S (excluding the IRGA and before NCI) was $2.37 billion, that’s a reinvestment rate of 90%. Not too bad.

Almost $900 million into acquisitions and investments just in Q4

This good pace of capital deployment doesn’t seem to be slowing down either. The company pretty much took everyone by surprise by sharing the capital that had been deployed since the quarter’s end (31/12): $802 million. That’s $802 million deployed in just over two months, not bad.

But wait, there is more good news: Constellation’s capital deployment pipeline is becoming larger. This stems from a new strategy that the company will pursue named PMS: Permanent-Engaged Minority Shareholder. Sabre (SABR) was just the beginning of what might become a more prevalent strategy going forward:

We’re calling a permanent engaged minority shareholder strategy, or PMS. Our investment in saber is the first meaningful expression of it, and I have to thank Mark Leonard, who’s helping us with this strategy and helped us, explicitly on this particular investment. But the logic is straightforward, permanent, meaning we’re long term shareholders, long term holders, not traders, and will work to ensure these companies endure as institutions. We’re engaged, which means we care about governance, management, incentives and capital allocation and will actively work to have influence where we think it creates value for the minority. We’re not acquiring these businesses outright. We want to partner with other shareholders and we hope many of them become engaged long term holders alongside us.

I found it particularly interesting that not only has this strategy originated (or at least to an extent) from Mark Leonard himself, but that he also drove the investment in Sabre (SABR) (I wrote about Sabre last week here). Even though they mentioned that the details of the strategy will depend on every specific investment, they did more or less lay out clearly that the objective is not to buy companies outright but to collaborate alongside them to improve the business (sort of like what Topicus is doing with Asseco).

It’s worth noting that the modelling used in PMS is the same one they use for private acquisitions (meaning same hurdle rates). This means that, for Sabre, Constellation is likely targeting a 20%+ IRR and probably assuming no multiple expansion whatsoever. In my article about Sabre, I explained what the real problem with Sabre is and how the company might help fix it.

We should also be aware of the reason why management is now pursuing PMS: public markets have fiercely reacted to the AI-threat, whereas private markets have not:

And we haven’t really seen on the private side any change in pricing. So far. And competition for those businesses is still very strong. So nothing’s changed. There. There’s just been a little bit of change in pricing for publicly traded companies, as you well know. And so there might be some opportunities there.

AI and repurchases

Management was evidently asked about their thoughts on the AI threat. Even though they did not outright provide thoughts about the implications of AI in setting terminal values, I believe that the PMS strategy sort of confirms their view on the AI impact on VMS (i.e., the market might have gone too far in some cases). Mark Miller also opened the call with some thoughts on the topic:

There’s real noise in the market now about AI disrupting software businesses. And we take that very seriously. But we think we’re well positioned and although we are staying very disciplined about how we approach it, we’ve always run a learning culture at Constellation. Best practice sharing across our operating groups is one of our genuine differentiators. And I’ve seen more across portfolio collaboration around AI in the past year than on any topic in recent memory Over the past 12 to 24 months. We’ve directed our culture of best practice sharing to helping our businesses navigate the AI transition thoughtfully. We spent 2025 upskilling our development teams. Thousands of developers have built skills in AI, augmented coding across our operating groups. We’re entering 2026 with AI enabled coding becoming increasingly commonplace. The productivity returns are real, and they’re still growing as these skills embed more deeply in our business units across the world.

He believes that lower coding costs are going to eventually become table stakes as development tools get commoditized, but that there’s much more than differentiates Constellation’s software:

But I want to be direct about something, building products and features faster will not be what differentiates us long term. That capability will become widely available. It’s going to be table stakes. What will matter is what our businesses have spent many years developing. Deep vertical knowledge, a genuine understanding of customer workflows and processes that data inside their solutions, and the trusted relationships they built. I believe AI will help us do all of this better.

I found particularly interesting the comments around how AI might impact the M&A operations. Management believes this will happen through two ways:

They are now looking at the potential impact of AI on acquired companies. This is more of a qualitative assessment of potential targets

They are looking at AI tools that might help them accelerate the pipeline:

We’re also piloting AI tools to help us rank prospects by quality and readiness to transact. It’s early. And the jury is still out on whether it will prove its value over time.

This last part is (imho) very interesting because AI is all about proprietary data, and Constellation has a good chunk of that in terms of M&A. Let’s not forget the company has built a proprietary database of +1,000 acquisitions and that they’ve built the pipeline over decades. This is one place where I believe AI can be hugely accretive and in a unique way to Constellation.

I want to end this earnings recap with some thoughts on stock buybacks. There were some relevant news on this front. Constellation is now considering buybacks as a valid capital deployment option. This is a significant departure from Mark Leonard’s strategy. The only “problem” is that “they have a number,” but they are not yet hitting that number and have plenty of available opportunities elsewhere (i.e., they don’t think it’s in the best interests of shareholders to repurchase shares):

So we have created a subcommittee within the board to look at this. And there is a number. But at this point in time we believe there are ample opportunities to deploy capital as opposed to buying back our own shares. But if that were to change in the future, we’ll reassess. But at this point. We are not looking to put in place an NCIB.

Now, many people typically rush to interpret these comments as an admission that the stock is expensive. I disagree with this for a very simple reason: Constellation’s hurdle rate is likely far higher than the hurdle rate of most Constellation’s shareholders. Considering that the company targets 20%+ hurdle rates, the fact that they are not doing buybacks here probably means that they consider the IRR on Constellation’s shares to be lower than 20%, which shouldn’t necessarily make the stock expensive if your hurdle rate is lower.

Mark Miller was also asked about the differences in leadership style between him and Mark Leonard. He claimed that Mark Leonard came to VMS as an investor, whereas he came into VMS as a product developer. This is interesting because the leadership transition comes at a time when Constellation might actually need more of a product-guy at the top. Filling Mark Leonard’s shoes is probably going to be impossible, but Mark Miller seems like a good fit and it was nice to know that Mark Leonard is doing well enough as to be able to participate in Board discussions.

All in all, a good quarter from Constellation (and Topicus and Lumine).

Have a great day,

Leandro

Thanks for the discussion of the 2025 results. Very informative and well written!

Great article 👍