Interest rates, war, oil…the market doesn’t seem to care (NOTW#96)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

You’ll also get access to the 30+ page detailed report on the robotics industry.

The in-depth reports of Stevanato and Deere are also free to read to gauge the quality of the research.

Join today:

Markets were flattish/down this week despite several relevant news around two things that should theoretically matter quite a bit: interest rates and war. I’ll talk about these topics in the brief market commentary.

Without further ado, let’s get on with it.

Articles of the week

I published one article this week, an in-depth report on the robotics industry.

The Durable Winners of the Robot Age

The full PDF of this report is available (for paid subscribers) at the end of the post. There’s considerable free content as well so don’t hesitate to read.

I go over…

My framework to understand the industry

The potential opportunity

Who participates in each segment

What segments seem more appealing from the POV of a long-term investor

And much more

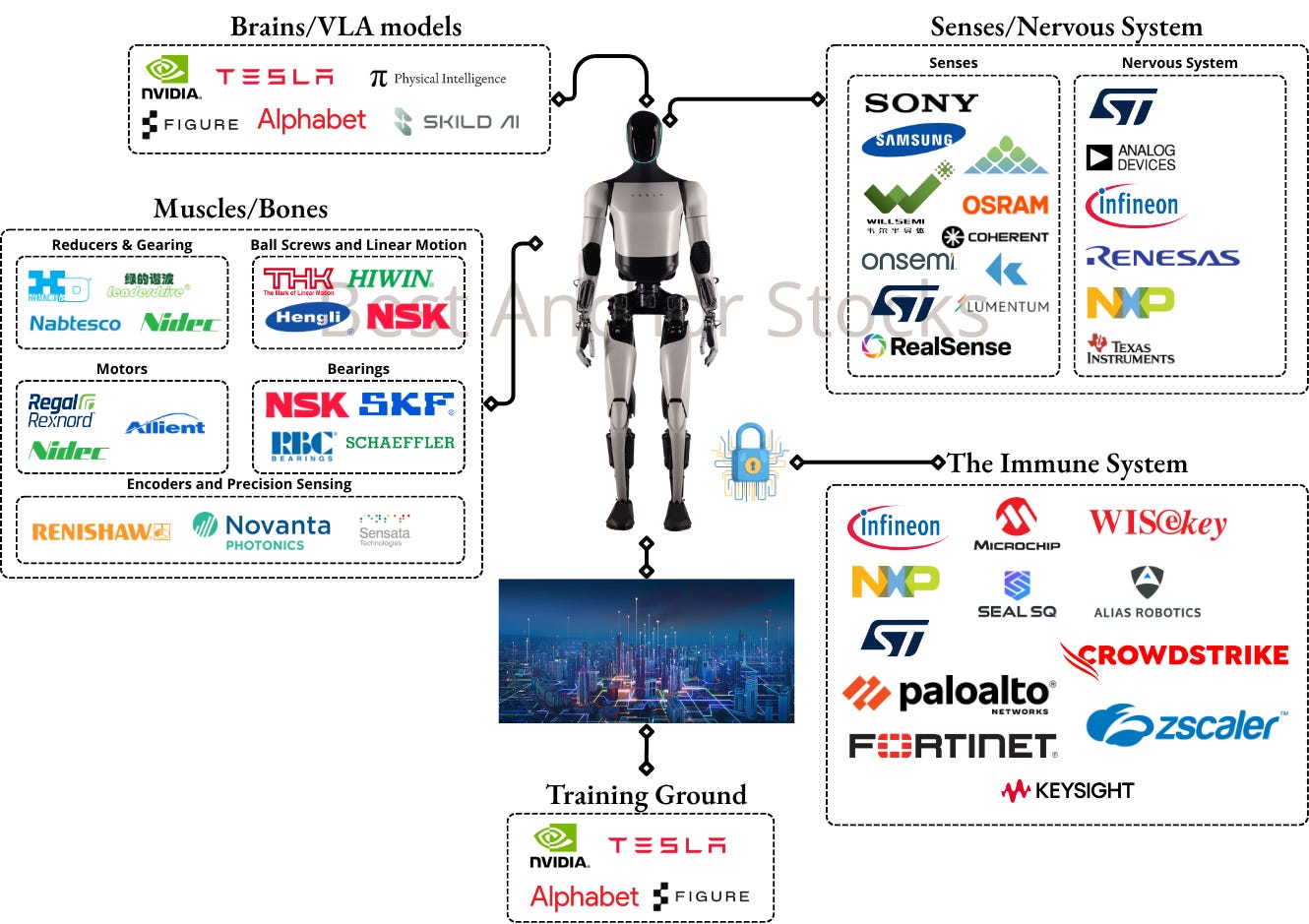

The goal is that you understand the industry well after reading the article and come out of it with a name or two that enjoys competitive advantages within the sector. Here’s the industry map:

The result of the report is that I will start a new position on Monday. I explain my reasoning in the article.

Without further ado, let’s see what the markets did this week.

Market Overview

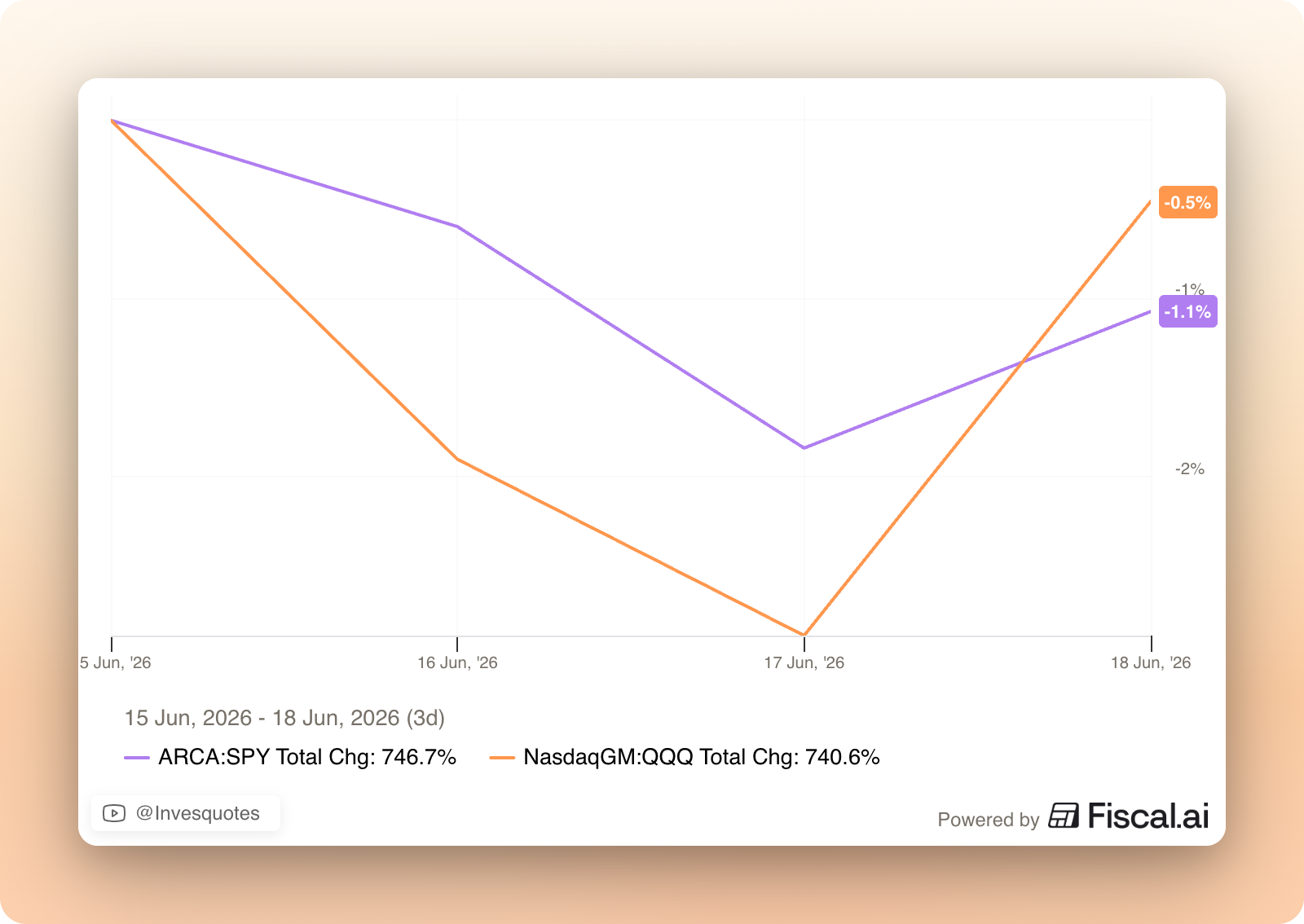

Markets were down/flattish during this short week (due to Juneteenth holiday):

It was a week in which the Fed made the headlines again (yay). New Fed Chair Kevin Warsh shared that the committee had decided to leave rates unchanged and gave a speech that the market interpreted as hawkish (i.e., theoretically not good for risk assets). 9 of the 18 members now expect rate hikes in 2026. When Trump got confronted with this, he said that “it is what it is” which is a significant departure from what he claimed when Powell wanted to raise rates! I don’t have a clue about what rates will do this year, but looking at my portfolio’s composition, I don’t think I have to worry much about 50-100 bps higher or lower interest rates.

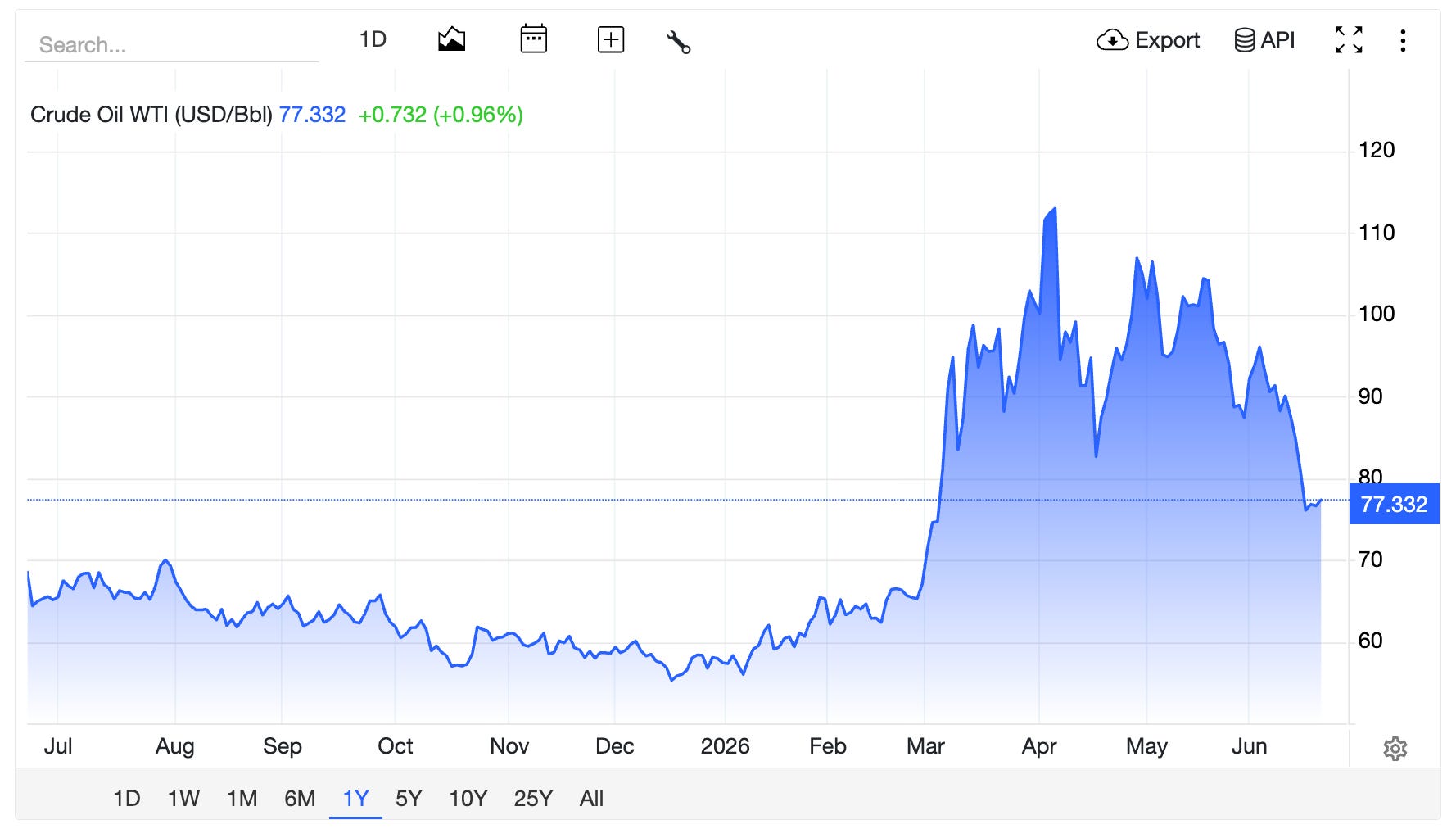

There was also news around Iran, as the US signed the official peace deal in France this week. Shortly after signing it, Israel attacked Lebanon, which resulted in yet another “closure” of the Strait of Hormuz. This evidently caused oil prices to decrease significantly:

This bodes well for inflation starting next year, but it’s also funny because many claimed that oil was unequivocally going to $140-$200 per barrel (this happened not long ago). Oil bulls and permabears were once again wrong, and while they’ll eventually be right, I believe that the timing also matters when you are going against a secular trend. This is precisely why I look to invest behind secular growing themes: it makes timing significantly less relevant! (albeit not totally unimportant).

So, plenty of relevant news this week about things that theoretically matter a lot to markets (interest rates and war) but despite all this the indices did not do anything crazy.

The industry map was mostly green this week driven by semis (as concerns over Anthropic and the US government eased):

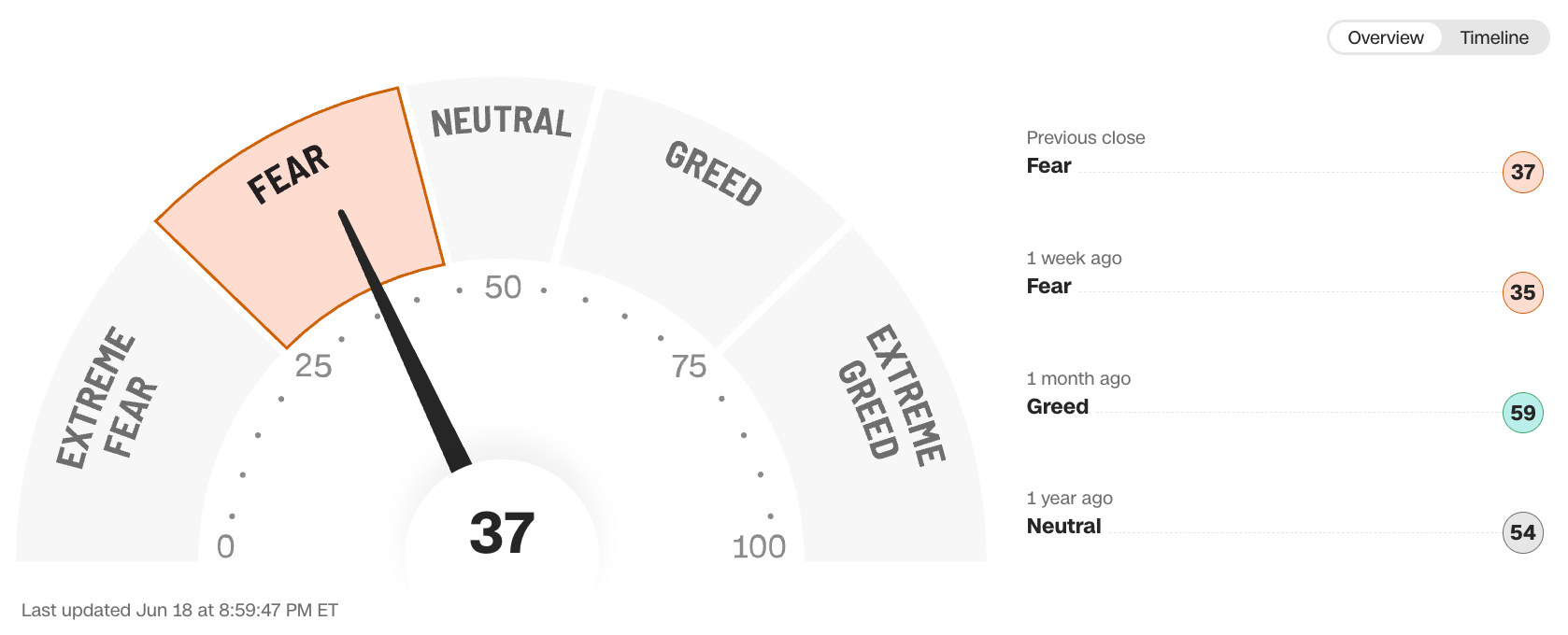

The fear and greed index remained in fear territory: