The Durable Winners of the Robot Age

The full PDF of this report is available (for paid subscribers) at the end of the post. There’s considerable free content as well so don’t hesitate to read.

Without further ado, let’s get on with it.

Many investors make the same mistake over and over again by freely interchanging growth and valuation. Even though these two variables are intrinsically related…

Growth and value are joined at the hip.

- Warren Buffett

…the reality is that it’s tough to make a valid valuation argument if growth is nonexistent. Can one do well by investing in low-growth businesses trading at apparently low valuations? The answer is evidently “yes,” but no-to-low growth comes with several drawbacks. For one, it’s incredibly difficult for management to add value when there’s no top-line expansion. Furthermore, in a world “full” of growing businesses, it’s likely challenging to ever get the market interested in a stagnant one (i.e., multiple is likely to stay lowish unless the market decides to treat it like a bond proxy).

I’ve come to this realization the hard way: by losing money on several low-growth but “resilient” businesses. These unforced errors eventually led me to set a hard rule: I will not invest in businesses with meager organic growth (defined as growth below (or too close) to GDP growth) regardless of the investment thesis. This simple rule shrinks the investable universe significantly (not many businesses are able to outpace GDP growth consistently) and increases the optical multiple one has to pay, but also significantly reduces the value trap risk.

Step 1: realize that growth is a non-negotiable variable in future value creation. Check.

Step 2: find themes or industries that enjoy secular growth to make the job easier. This article.

While you can find growth businesses pretty much across any industry, it’s much simpler to swim with the current at your back. I see a few macro trends shaping the next decade and I believe that the Best Anchor Stocks portfolio (my personal portfolio shared with subscribers) is adequately positioned across many:

Complex biologics: large, complex molecules are increasingly dominating the drug pipeline, requiring highly specialized and stringent manufacturing and administration processes. There’s significant exposure in the Best Anchor Stocks portfolio. I believe getting exposure to this theme is pretty cheap right now.

Infrastructure renewal: physical assets across the developed world have aged far past their useful lives and must be replaced. To this, we must add the exponential power grid demands driven by the AI data center buildout. Even though this has been a long-standing trend, the reality is that pace has failed to pick up. There’s light exposure in the Best Anchor Stocks portfolio.

Defense & Reshoring: in an increasingly polarized world, globalization is fracturing, forcing countries to make strategic decisions across defense and local supply chains. There’s minimal exposure to defense but a more considerable exposure to reshoring in the Best Anchor Stocks portfolio.

Semiconductors: no matter what structural trend you look at, it likely can’t function without an increasing number of semiconductor content. There’s considerable exposure in the Best Anchor Stocks portfolio.

Aging populations: the population is aging fast, straining health systems and driving massive demand for cheaper, outsourced or alternative care delivery. There’s no exposure in the Best Anchor Stocks portfolio, and I believe this trend suffers some hurdles (like regulatory pushback and strained budgets).

Specialty testing & certification: as regulations tighten and social media amplifies corporate missteps, independent certifications are becoming critical for mitigating reputational risk. There’s light exposure in the Best Anchor Stocks portfolio.

Physical AI and the rise of connected devices: crashing hardware costs and soaring computational power have made the unthinkable a reality: a world where we live and work alongside millions of autonomous, connected devices. There’s considerable exposure in the Best Anchor Stocks portfolio, but I believe this promises to be one of the main macro-trends of the coming decades.

You can agree with these to a greater or lesser extent (if you can think of any other feel free to leave it in the comments), but the reality is that these are secular themes that deserve your attention as an investor. Identifying these, however, is just one side of the coin; valuation/timing is the other. The objective of this article is to dive deep into the last of these: physical AI. I believe Physical AI will shape the next decade, riding the kind of S-curve that every investor strives to find. There’s another thing that makes it interesting: it’s vast and made up of a wide variety of niches. This means there’s potentially a lot of ways to gain exposure to the trend.

When everything clicked

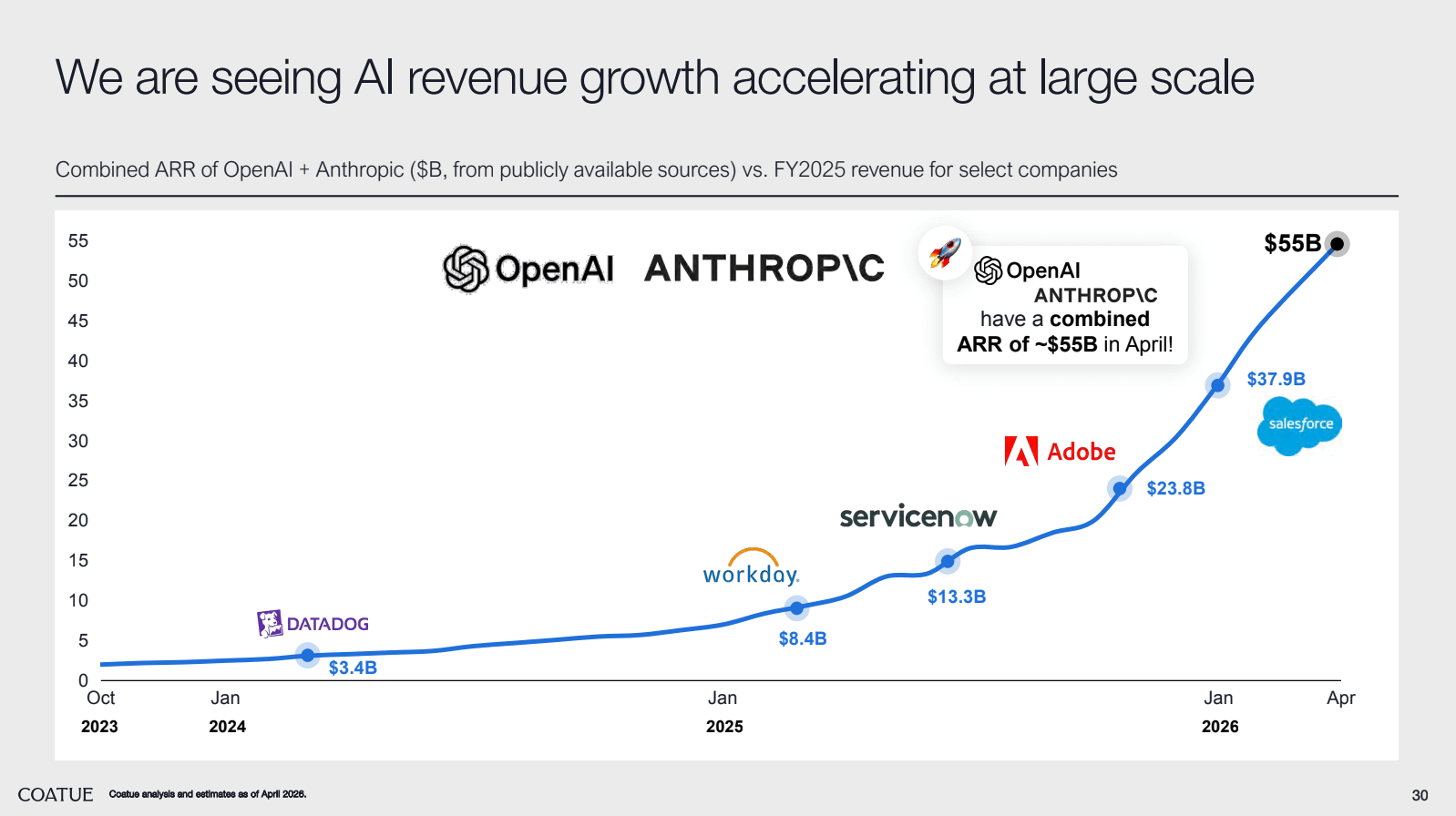

ChatGPT was not the first commercial LLM (Large Language Model) to see the light, but it was indeed the one that got the AI revolution started. OpenAI’s flagship LLM was launched in November 2022, achieved “verb” status at the speed of light, and soon became the fastest-growing consumer-facing product ever. Anthropic joined the party later and both went to defy the law of large numbers:

Source: Coatue

Not only is life “unthinkable” today without LLMs, but they’ve also enabled a whole new wave of technological frontiers. The first one is agentic AI. AI is no longer encapsulated in an LLM; it’s now able to retain context and conduct tasks in the digital world just like any person would, but faster…and cheaper (sort of)!

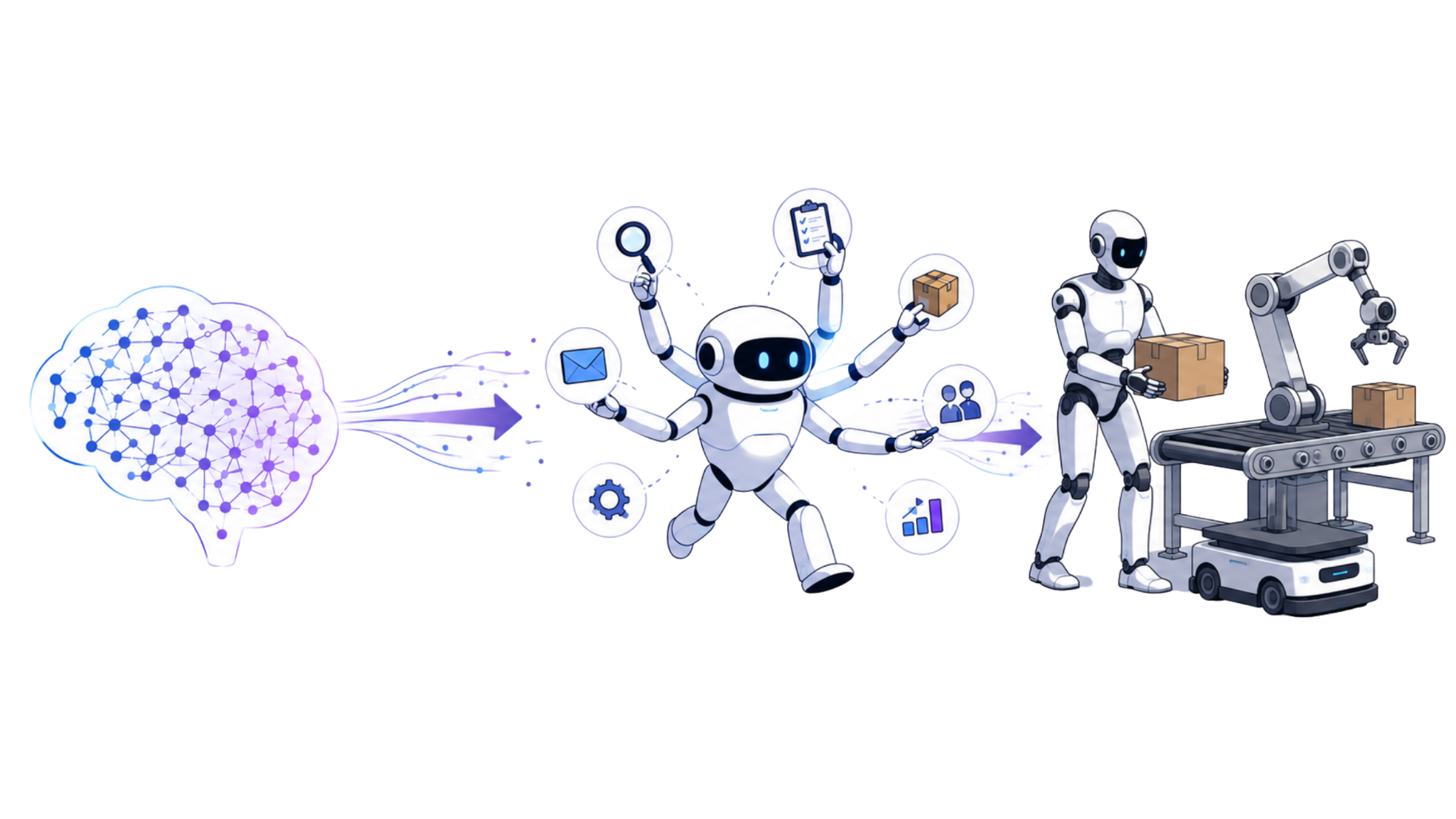

While we are still in the early innings of the agentic frontier, the next frontier is already upon us: physical AI.

The next wave of AI is physical AI. AI that understands the laws of physics. AI that can work among us. Everything is going to be robotic. All of the factories will be robotic. The factories will orchestrate robots and those robots will be building products that are robotic.

Jensen Huang, Nvidia’s CEO

So, what is physical AI and why is it “suddenly” possible? Even though the world is currently transitioning towards powerful AI digital agents that promise to substitute (or power) human labor, the crude reality is that these agents are only able to operate in digital environments where physics is not even a consideration and the cost of failure is manageable. But, what if we wanted to unleash these digital agents in the physical world? Things get a tad more complex.

From the screen to the real world

Physical AI can be understood as a digital agent that operates in the real world. This apparently minor transition changes everything and comes with a comprehensive set of risks/threats/obstacles, but also with its fair share of opportunities. We could understand Physical AI as a continuous loop of perception, interaction, and reaction.

Humanity has not suddenly woken up to physical AI; a concerted effort throughout decades has made this frontier possible. We’ve gone (in my view) through four stages:

Perception: we first needed a way to recognize and classify real-world variables. This became possible with sensors, cameras, analog chips…but this information was not entirely useful unless we were able to interpret vast amounts of heavy data and (very importantly) capture the sufficient amount of data (either real or “generated”) to mimic the real world

Generative AI: then came LLMs and with it the ability to interpret vast amounts of data (both structured and unstructured). Perception data (considering it was vast enough) was suddenly useful thanks to compute. Generative AI also came as a way of processing, synthesizing and even creating perception data (thank you, GPUs!).

Agentic AI: before being able to jump into the real world, the systems needed to be tested in the digital world so we started to find ways of automating digital tasks.

Join 1,2, and 3, and we suddenly had all the ingredients to make physical AI (stage 4) a reality. Now, physical AI comes with a pretty relevant obstacle: the tolerance for mistakes is very low. This means that the historical process of trial and error that has been so prevalent in the digital realm is no longer valid; physical AI must be almost mistake-free before making it out to the real world. So, how can we prevent these failures?

Let’s begin by taking a look at a couple of interconnected terms (I’ll talk about these throughout the report)…

Long tail problem

Data scarcity problem

Sim to real gap

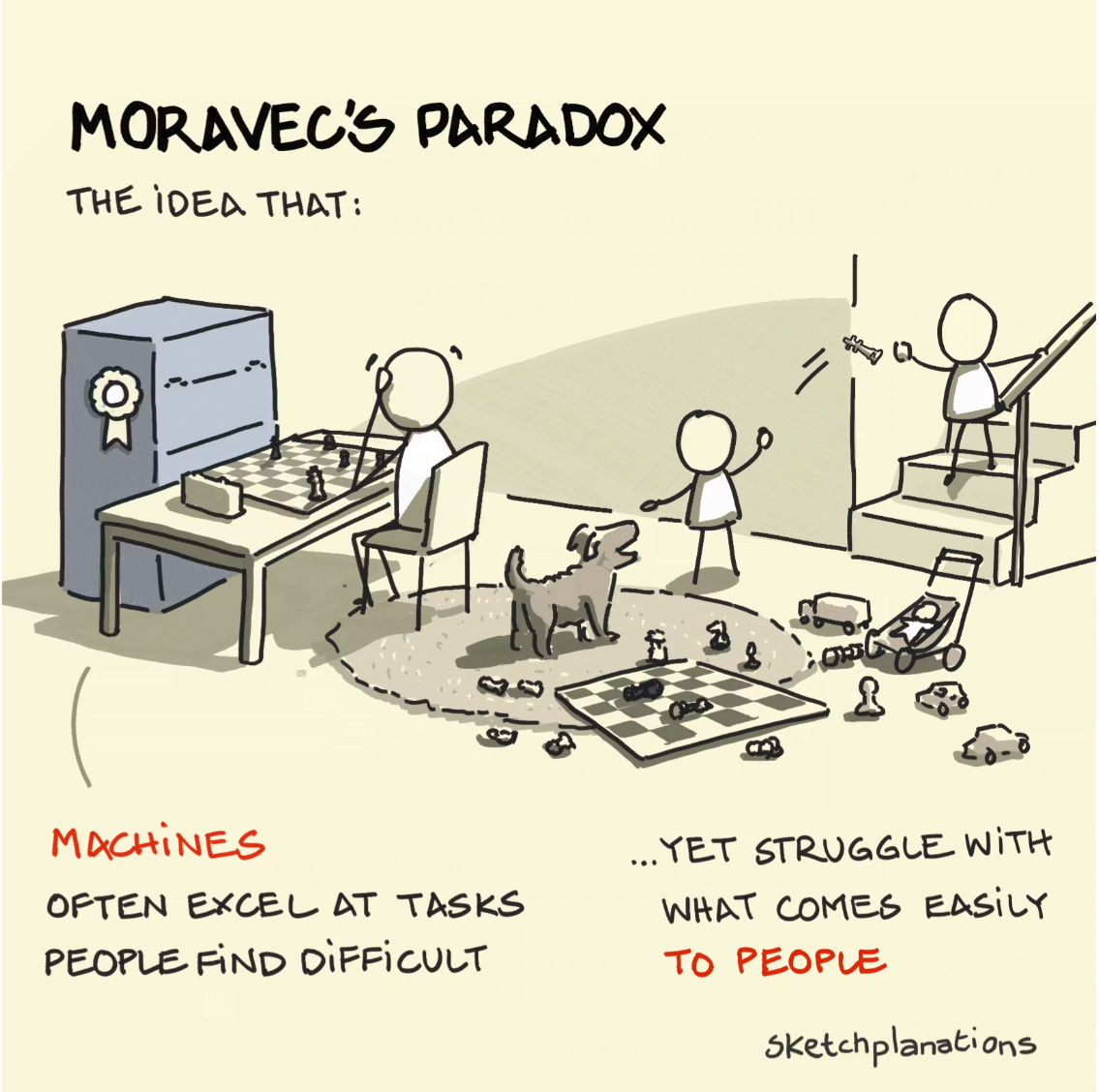

Moravec’s Paradox

Let’s start with the manifestation of the problem. Moravec’s Paradox states that what is easy for humans is tough for computers, and vice versa.

LLMs are capable of conducting tasks that would be impossible for humans, but robots have struggled to conduct apparently “easy” human tasks like walking on uneven ground. Solving Moravec’s Paradox historically proved challenging due to the data scarcity problem. We ultimately lacked physical data good and comprehensive enough to train physical AI in real-life environments where unpredictability is a given. Now, you might think that there’s enough data in the world so that a robot can learn how to move, and while this is true, there’s also a long-tail problem. What does this mean? That there’s a lot of base case data, but very little edge case data. This is acceptable in the digital era where edge cases can be solved as one goes, but not in the physical one (at least not entirely).

With little margin for error, the lack of edge-case training data could lead to disastrous consequences (even if rare). Now, hold up! The industry is slowly but steadily bypassing these limitations. Let’s understand how by comparing physical AI to a human body.

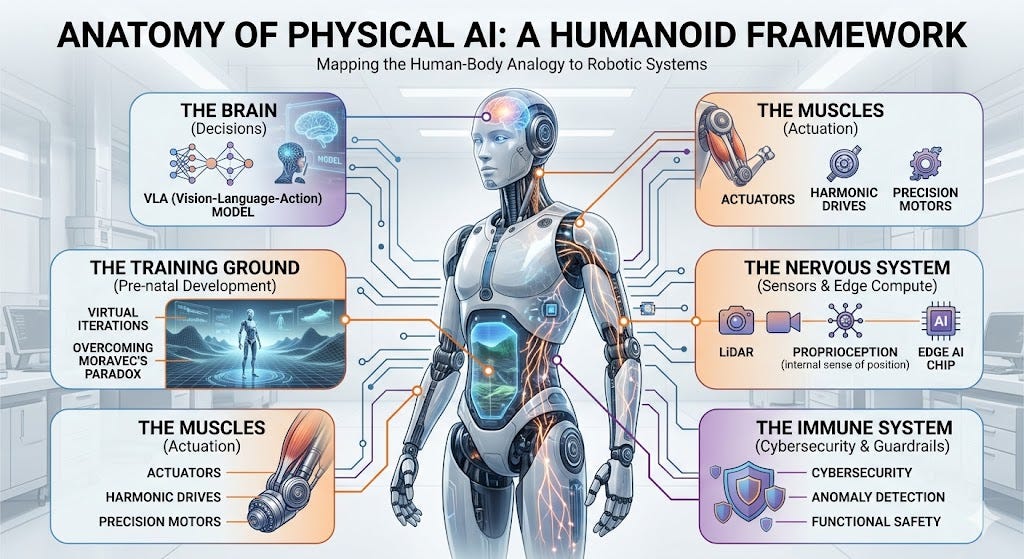

The anatomy of physical AI

Physical AI spans three main “applications,” (humanoids, industrial robots, and autonomous driving) but I am going to focus on humanoids to explain my framework. Even though these three can be considered different “applications”, physical AI systems can ultimately be understood using the same framework of perception, interaction, reaction, and reinforcement learning.

Physical AI is ultimately the fusion of digital AI (“intelligence”) with physical capabilities, and that looks a lot like us humans (sort of). I believe there are several parts to a physical AI system that can be mapped to parts of our body:

The Brains can be understood as the robot’s mind/model. This is ultimately the decision-making tool. Just like for the human brain, there are two parts to the brain: high-level thinking and low-level reflexes. Maybe System 1 and System 2 sound more familiar if you’ve read Kahneman’s ‘Thinking Fast and Slow’.

The training ground refers to the virtual worlds used to train the brains before they touch the real world. Here lies the main problem for physical AI, as discussed above. Most of the training ground (unlike for humans) could be considered “pre-natal” as these systems have to be quite polished before making it out to the real world. Humans are allowed to make some mistakes which we end up calling “experience.”

The muscles and bones refer to the hardware, the actuators, and all the physical parts that ultimately compose the humanoid’s structure.

The senses and the nervous system work hand in hand with the brain and relate to the sensors and cameras that allow the system to interact with the real world and also to “feel” what’s going on inside its body.

The immune system is what keeps the system healthy from unwanted intruders. We could understand this as cybersecurity, regulation…

So, at the end of the day, a humanoid doesn’t pretend to be much different to what a human body actually is:

Source: Made by Best Anchor Stocks with Gemini

I’ll dig a bit deeper into each to understand what companies participate and who is poised to win as the industry rides the S-curve. The best scenario would be to find a picks-and-shovels business, and luckily for us, there are a few (but not many) that are really “investable.”

What’s at stake and why now?

Before jumping into the ecosystem’s components, I believe we should try to size the opportunity. Many estimates typically treat the largest market (AVs) separately and, even though I’ll also focus majoritarily on humanoids, the AV market is expected to be huge. As one would expect, estimates vary tremendously, but many believe it’s a market worth trillions in under a decade, growing at a 20%+ CAGR from current levels. The AV opportunity is typically “analogous” to the robotaxi opportunity.

I’m also not going to spend a lot of time on industrial robots because it’s the most “mature” market and where growth is the slowest. The main reason is that a lot of industrial businesses (especially across automotive and electronics) are already significantly automated. Now, the humanoid opportunity will most likely present itself in the industrial realm, further automating human tasks in these businesses (i.e., the humanoid opportunity rests on automating more of the industrial base). For example, Texas Instruments’ CEO believes that we are not far from seeing humanoids walking around their fabs:

Now, you tell me the number of humanoids that are going to be built. Depends who you listen to, but I think we are starting to see it, and I am excited about it. I don’t think it’s as soon as people say, but I can see why humanoids, like robotics, will be one day walking around our factories, especially assembly and tests, and providing value. I’m excited about that.

Haviv Ilan, TI’s CEO, at the May 2026 Bernstein Conference

The industrial robot market is estimated to grow to around $60-70 billion by 2030, but the IFR (International Federation of Robotics) admits that this only considers robot sales and not the entire ecosystem that surrounds them. They believe that the real market might be 2x-3x larger when accounting for the entire ecosystem, so around $120-$210 billion by 2030. A pretty significant market, but nothing that should get people too excited in the trillion-dollar-industries era…

It’s also worth pointing out that several of the picks and shovels companies that sell components/ecosystems to industrial robots also participate in the other two segments, making their potential target market extremely large regardless of the “meager” growth in industrial robots.

Let’s jump now to the most speculative (but also attractive) market of them all: humanoids.

Tesla Optimus

There are several ways to arrive at market size estimates here, and these can be separated as recurring and one-time. Some size the market with this simple formula:

Humanoid robots shipped * average ASP

While this methodology can potentially lead to astronomical numbers, the reality is that it’s not a great method to size the opportunity because it severely understates it; why? Because it only captures hardware sales. Humanoids today go for upwards of $100k, but to make them accessible they’ll most likely need to come closer toward the $30-$50k area. Assuming 5-6 year replacement cycles, this market is likely going to be large, but far from the revolutionary numbers that one sees out there.

The above is the equivalent of measuring Apple’s opportunity just based on hardware sales but ignoring its services segment which is recurring and currently makes up more than 30% of total sales. As in everything in tech, the most likely scenario is the transition to a razor-razorblade model, which in the case of humanoids makes a lot of sense and leads us to the second estimation method.

The second way TAM is estimated (which also leads to a significantly larger number) is through labor/task substitution. I would consider this to be the most likely scenario because I’d imagine that the value add of a robot goes far beyond the sale of its hardware and the industry would like to take its fair share of value by transitioning towards a Robots-As-A-Service (RaaS) model. The math here is pretty straightforward (albeit the assumptions are pretty speculative):

Make assumptions around what % of labor (or what % of tasks) get substituted by robots in a reasonable timeline (will likely face some regulatory backlash)

Assume that humanoid providers keep a portion of the value add

So, for example, if a humanoid is substituting someone who made $50k a year, then maybe the humanoid provider (or the apps that sit on top) can make $20-$30k every year from that robot (+ the hardware sale). Note that these estimates might prove to be conservative considering that $50k is likely on the low end of the salary spectrum in developed economies and that humanoids would be able to run multiple shifts per day, but it’s just illustrative.

This is a win-win scenario for the humanoid ecosystem, the robot acquirer, but not for the worker (which is why politics will most likely be a relevant consideration). We could somewhat compare it to the smartphone industry: there are hardware providers who monetize the installed base by offering 1P services or acting as a toll booth on 3P services. The humanoid industry can develop in two ways which are analogous to the Apple/Android strategies (I’ll discuss it later). I don’t know how monetization will evolve in the future, but in my mind two monetization avenues make sense: subscriptions for renting the Robots plus an added service fee on top depending on the skills you want to rent (maybe these will come from external and internal providers, just like we have 1P and 3P apps on the phone).

This is evidently pure speculation, but Morgan Stanley makes the following assumptions for the humanoid industry:

13 million humanoids in 2035 (mostly in tasks in factories and warehouses)

24.4 million units by 2036

1 billion units by 2050 (10% of which are in domestic cores)

This is literally what an S-curve looks like…slowly at first, then all of a sudden. As humanoid pricing drops, one could argue that adoption will grow significantly (this is a tale as old as time in tech).

I believe the assumptions are pretty aggressive, but even if we assume that there will be “only” 10 million humanoids by 2035, at an average yearly ASP of $20k, that pencils out to a $200 billion market. Of course, if one agrees with Morgan Stanley’s 1 billion unit estimate and assumes a $20k ASP, that’s a $20 trillion market by 2050. Penciling out a given number for the industry is pretty much impossible, but many industry participants agree that it’ll be in the trillions and I see no reason why it’s not possible (careful with asking a barber if you need a haircut though):

Humanoid robots are poised to bring physical AI to the world’s largest industries, unlocking multi-trillion-dollar economic opportunities.

Physical AI will revolutionise the $50 trillion manufacturing and logistics industries

Jensen Huang, Nvidia’s CEO

I think, however, that Morgan Stanley’s estimate is tough to believe considering that the working age population across developed countries is around 1.1 billion and that the total market for labor is around $40 trillion. Do humanoids realistically capture 50% of all labor? I have my honest doubts considering that they’ll face political backlash before getting even close.

The working age population rises significantly if we include non-developed countries, but ASPs will most likely have to come down considerably for these to come into play. Now, all this said, the humanoid market today is in research-phase, so the growth opportunity is pretty large regardless of how one wants to spin this and “getting cute” about whether it’s $5 trillion or $10 trillion will probably make us miss the forest for the trees.

Now, it’s also worth noting that we should take these estimates down a notch when sizing the potential opportunity for Western producers. Morgan Stanley believes (imho, rightly so) that a significant portion (upwards of 30%) of these robots will be housed in China, which potentially means that they are out of reach for the western supply chain due to geopolitical concerns (China is, btw, already building its own ecosystem of humanoids, led by vertically-integrated humanoid producer Unitree).

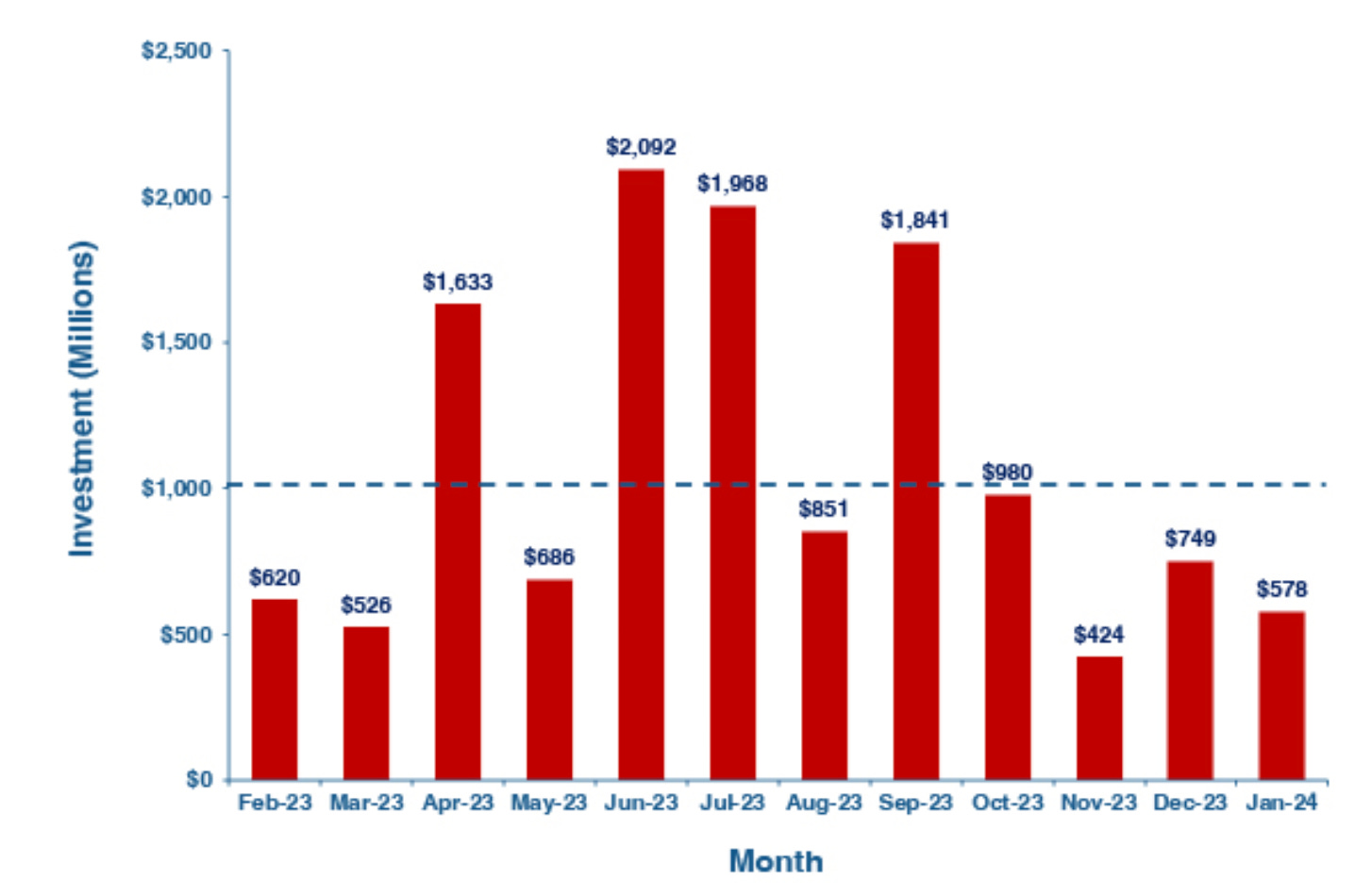

So, the market promises to be huge, but investors are not blind to the opportunity with things starting to get funded pretty aggressively and many pure-play robotics companies experiencing multiple expansion in public markets. In 2023, robotics companies raised around $13 billion:

That number (according to Dealroom) is $57 billion YTD, which annualized is around $114 billion or roughly 9x the amount barely two years ago. This shouldn’t be surprising as timelines compress. In 2023 we barely had “solved” digital AI and physical AI remained a distant dream. It’s not a dream anymore, is becoming a reality:

The ChatGPT moment for physical AI is here.

Jensen Huang at the 2026 CES Conference

Jensen tends to be early, but not wrong!

Let’s now take a more in-depth look at the ecosystem to understand how it works, who participates, and who is poised to win in this trillion dollar opportunity.

Join hundreds of paid subscribers to get access to…

Industry deep dives like the one you are currently reading

All in-depth reports (15+ companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

The Brains - The necessary inflection

The brains of a humanoid robot are the cognitive layer of physical AI. Humanoid brains were historically dominated by hard-coded rules that failed in a changing world. Physical AI required an adaptable model, so VLA (Vision-Language-Action) models became a reality. Google DeepMind released RT-2 in 2023 which formally introduced the concept of VLA: