Interest Rates, Asymmetry, and Nintendo's Valuation (NOTW#48)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

The market was pretty much flat in this shorter-than-usual week. I discuss the Fed’s decision and delve into a topic that I believe you may be interested in. In case you're not aware, I have a community on WhatsApp for like-minded investors. It’s pretty active, and the topics discussed tend to be engaging and interesting. If you want to join, you can do so by clicking this link or scanning the following QR code:

Without further ado, let’s get on with it.

Articles of the week

I published one article this week: Adobe’s earnings digest. The company experienced (again) a poor market reaction after reporting a beat, beat, raise quarter. One can only wonder what would’ve happened had the quarter been bad! As I discussed in that article, I believe sentiment is currently quite negative and will likely take some time to improve. The good news is that Adobe still has more than $10 billion outstanding in its share repurchase program and is generating record amounts of cash, so we can expect continued buybacks at what I believe is a favorable price.

“We are retooling the business for AI-driven growth.”

Adobe’s shares dropped considerably on Friday despite the company reporting a beat-beat-raise quarter on Thursday:

I have also begun exploring an industry that feels attractive and is currently unfavored by the market, although I am still in the early stages of my research. I am looking into two companies in this industry, one of which complies with the following:

Grew its revs at a 12.5% CAGR from 1988 to 2007 and is expecting the same CAGR over the next three years

Has a pretty low market share and is taking market share consistently through a differentiated approach

The founder is still involved and owns 15% of the business

Exposed to several secular growth trends, even though it operates in a "boring" industry

Stock is down almost 50% from highs, and mgmt is stepping into buybacks

The stock has CAGRd at a 17.8% clip since 1988

I don’t know where this research will take me, but it’ll likely lead me to writing about these companies or the industry, even if I decide not to include any in my portfolio.

Market Overview

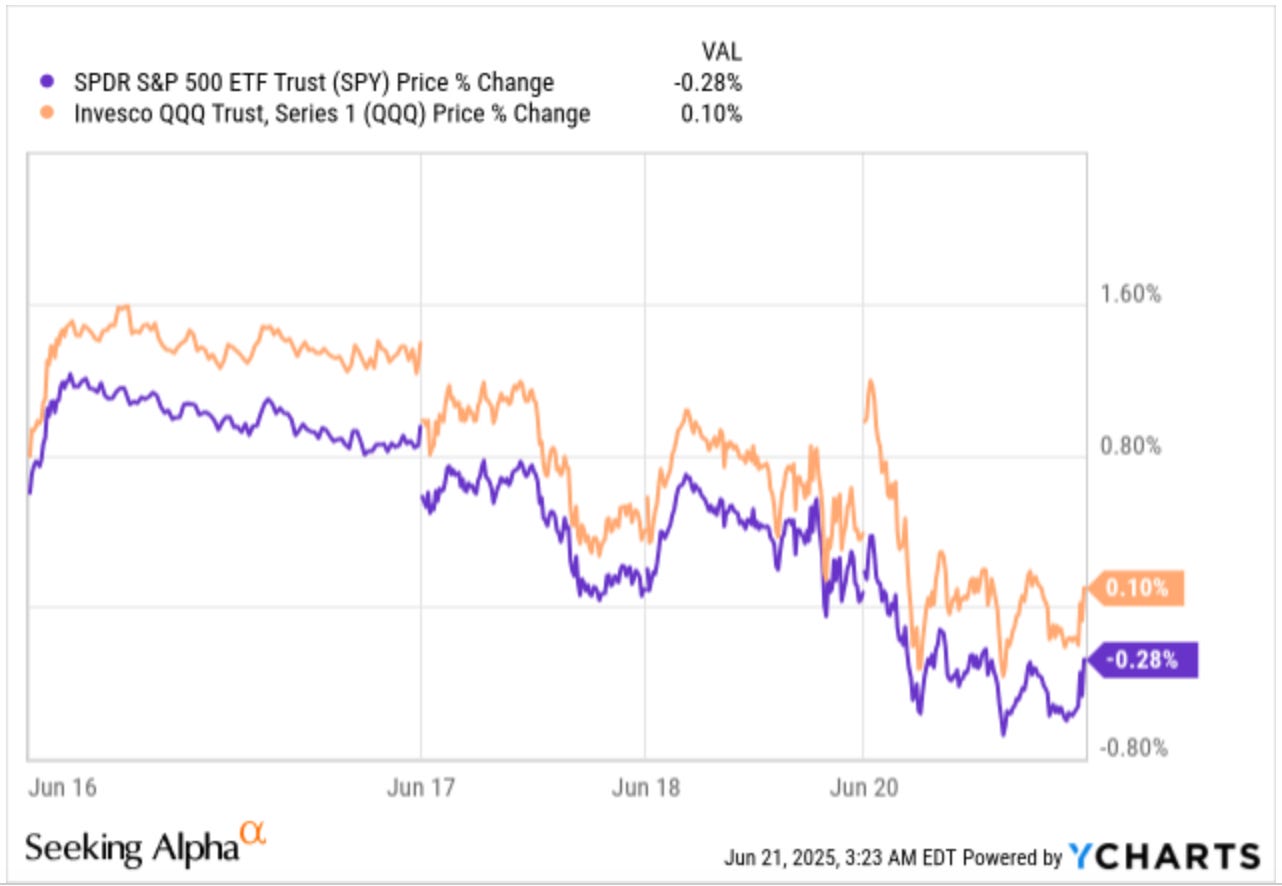

The indices started the week strong but lost a good deal of this strength towards the end of the week to finish flat:

It was a shorter week than usual in the stock market due to Juneteenth, which is a federal holiday that commemorates the end of slavery in the US. Despite it being a short week, we got a new interest rate decision by the Federal Reserve. They decided to keep rates steady, as they saw no signs that indicated they should lower them. I don’t give this decision too much thought, but I imagine Trump is furious, considering he has been advocating for lower rates even before he became President.

I obviously believe interest rates are a key variable for investors, for a couple of reasons. First, they determine the opportunity cost of risky assets, which plays a significant role in determining the overall level of valuation multiples. Secondly, because they directly impact the economy; they not only affect the valuation multiples of stocks but also the profits of the underlying companies. When borrowing money becomes more expensive, it should be somewhat expected to see a lower economic activity. What’s impressive about the US thus far is that, despite rising interest rates, the economy has done much better than many expected.

I was discussing something with some members of my WhatsApp community this week that I thought would be a good idea to bring here. I wrote the following, which I ended up also posting on X:

The ideal scenario is to find heavily skewed risk/reward situations (duh!)

These seldom come, but when they do, one has to take advantage of them. Takes a lot of willpower to say “no” to pretty much everything else

I feel that companies like Nintendo, Deere, and Stevanato have not long ago fit this description and it will be evident in 5 years (or so I hope so)

Whereas the notion of looking for heavily skewed risk/reward opportunities might be completely logical (who doesn’t want to get paid more for taking on the same risk?), I believe its applicability is not so easy, for several reasons. First, these opportunities are challenging to find because, although it can be inefficient, the market is a well-oiled machine in valuing businesses. This means that coming up against one of these will probably require saying “no” to many apparent opportunities that many investors would categorize as “good enough.” While this sounds easy, it’s pretty easy to fall into the sunk cost fallacy and end up taking action on our research, even though we don’t deeply believe that it will pay off.

The other reason it’s tough to apply is that (most) humans are naturally inclined to be optimists and therefore tend to focus on the upside, disregarding the downside. This, while it can be a great investment opportunity, doesn’t qualify as a “heavily skewed risk/reward.” I have fallen prey to this mistake before, and things can get very nasty when things don’t turn out as expected.

Three companies in my portfolio that I believe satisfy this criterion are Deere, Stevanato, and Nintendo. Let’s talk about the latter, right now my largest position, up 75% from my cost basis for a 27% CAGR (if you want to know what I think about Nintendo’s current valuation, give this article a look). Nintendo’s ADR was trading at around $9-$10 barely two years ago. While many will point out that the launch of the SW2 was a detail we did not know about back then, this is not remotely true, as it was fairly obvious that there would be hardware continuity (there were many signs along the way).

At $9-$10, Nintendo had little downside and a lot of upside (hindsight bias, I know). Was there a bear thesis? For sure, but at that price, it seemed like investors were already hedged to a great extent from the bear thesis. Nintendo is guiding for 300 billion yen in profit this year, despite what seem to be very conservative sales numbers. At $9, Nintendo was trading at roughly 18x 2025 EPS estimates, with 2025 being just the first year of arguably what will be the most successful launch in console history.

Just for context, should Nintendo achieve peak SW1 earnings (which seems likely judging how the launch of the SW2 is going), the stock is currently trading at a peak FCF yield of 6% (the company generated $5.4 billion in cash flow in 2021 and its current EV is $87 billion) despite its business model now being inherently more recurring. This doesn’t appear to be a company that is “extremely expensive,” as some people claim just based on its recent stock price run. This is also what makes holding these skewed risk/reward opportunities challenging: at some point, they will run hard and remain undervalued, with practically everyone believing they are grossly overvalued.

Investors are typically geared towards being active, but good investing is about little activity. And with this I don’t mean that investors should be bored. I believe an investor should always be on the lookout for these types of opportunities, but they must also be well aware that they will seldom end up in a transaction. And that’s hard!

The industry map was also mixed, with some exceptions:

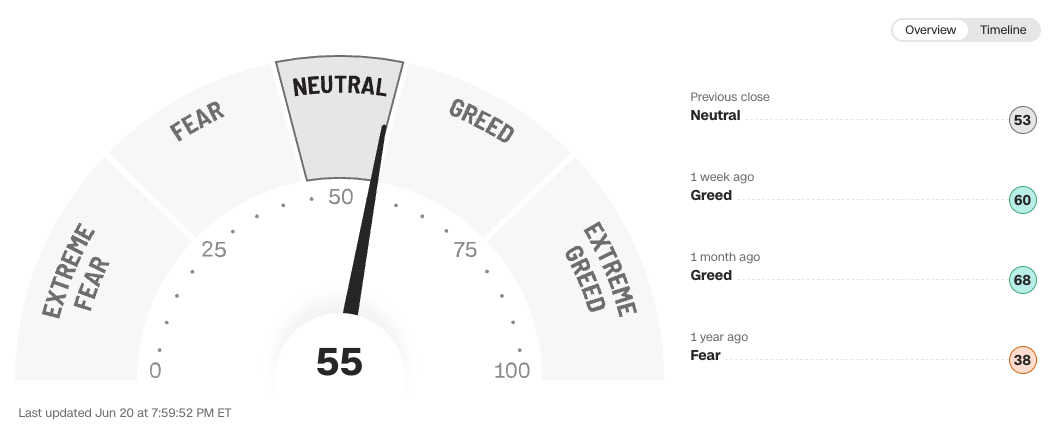

The fear and greed index retraced and is now in Neutral territory: