The stock is down 40%, the Business Isn’t

Is Hermes finally attractive?

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of subscribers today:

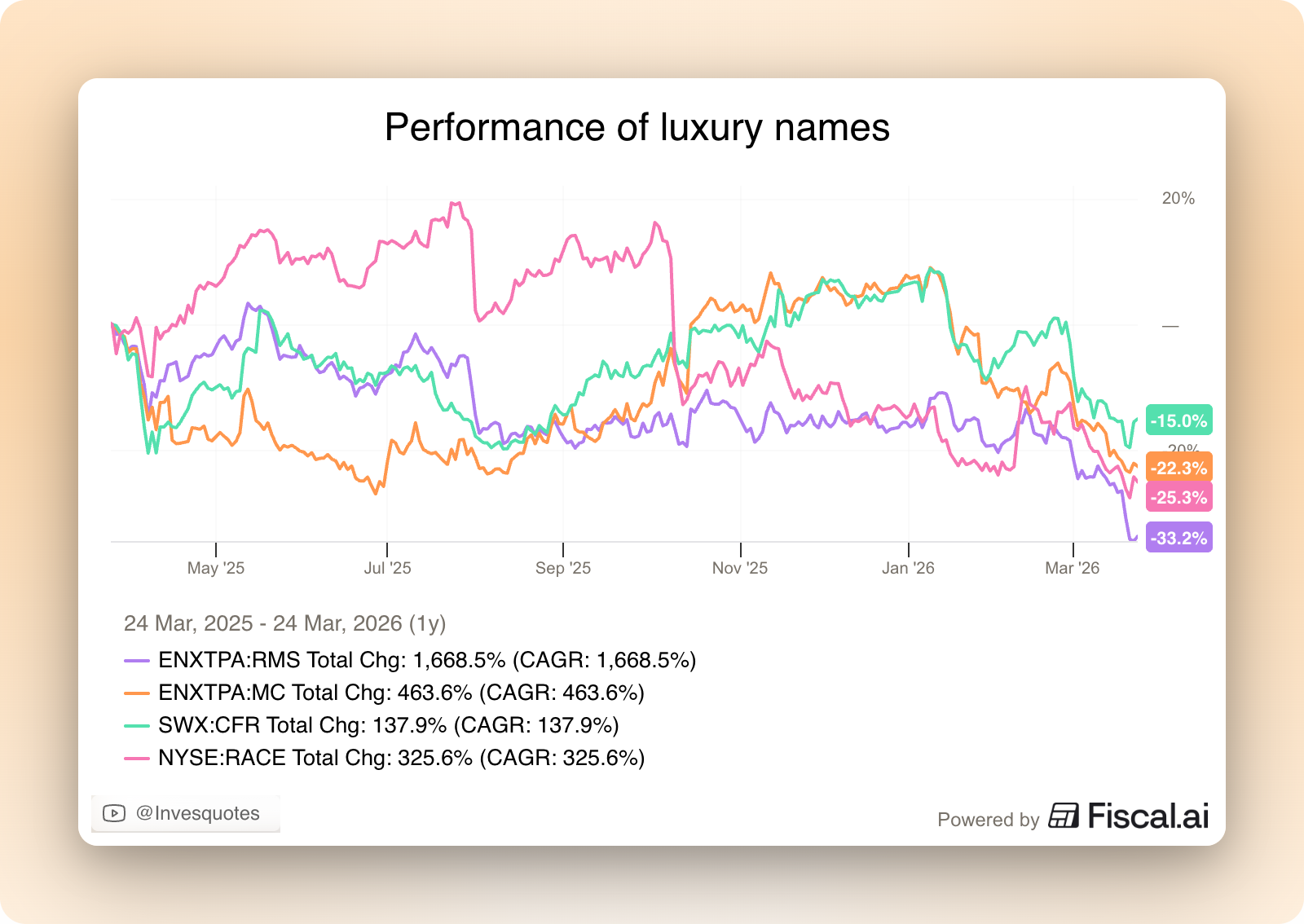

You may or may not have realized that the stocks of many luxury companies have performed poorly over the last few months/years. Even though I don’t believe that bundling all luxury companies together makes sense, the chart below portrays that the “broad” luxury sector has seen better days:

Three things (in my view) explain why the stocks of these companies have languished over the past couple of years. Let’s go over these briefly.

The luxury sector was irrationally valued at the pandemic peak (can’t blame it, though). The reason is pretty straightforward: the population’s purchasing power was not severely impacted during the pandemic, but they faced significant constraints in terms of where they could spend this money. A lot of people who were unable to spend their money on experiences decided to spend it on hard and soft luxury goods, making these companies appear as “hyper growth” businesses. The argument today seems to be quite the opposite; many believe that experiences are a secular headwind for many luxury companies (something I’ll discuss in more detail later). So, point #1: Valuations were inflated to start with.

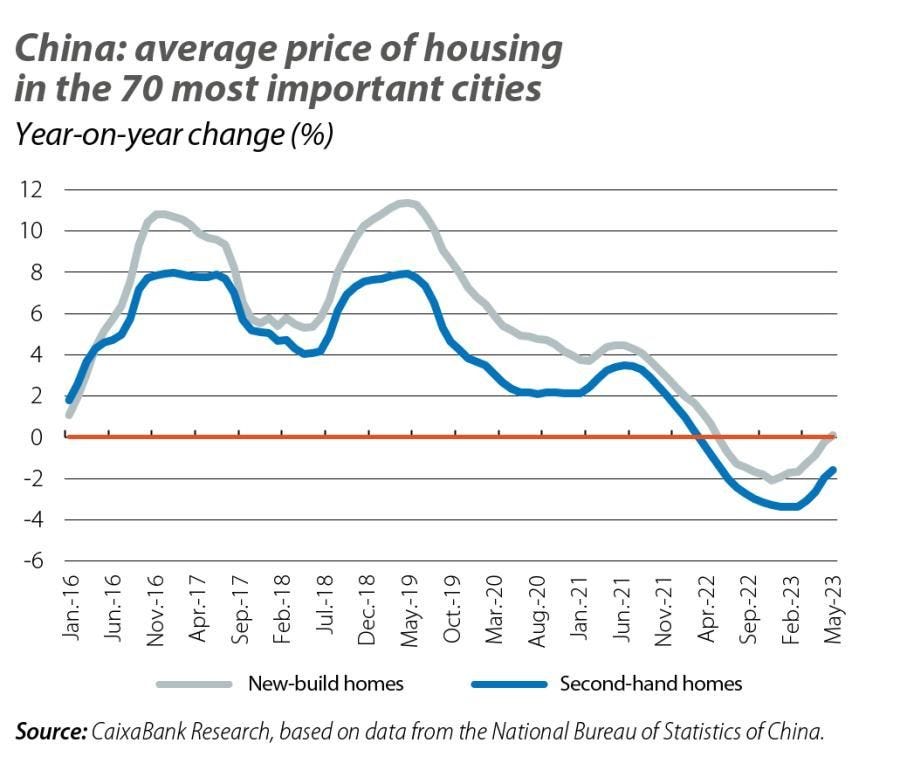

Valuations were not the only thing that were inflated, though; so were fundamentals (in most cases). Most of the luxury industry experienced a post-pandemic hangover which coincided with weakness in China (a key marker for the industry). Luxury sales in China are typically linked to real estate values, which did not do great after the pandemic. Real estate values across the major Chinese cities entered contraction territory in 2022/2023:

The good news is that China seems to be recovering somewhat. Deutsche Bank recently published that, after a weak 2025, the luxury industry in China might be on the verge of regaining its footing:

Lastly (and very recent), the conflict in Iran. The Middle East has become a high growth geography for many luxury companies and we all know that it has been severely impacted by the recent conflict. Although I acknowledge this will most likely have an impact on luxury spending in the region over the short to medium term, I don’t view it as a terminal risk for Hermes (or for any luxury company).

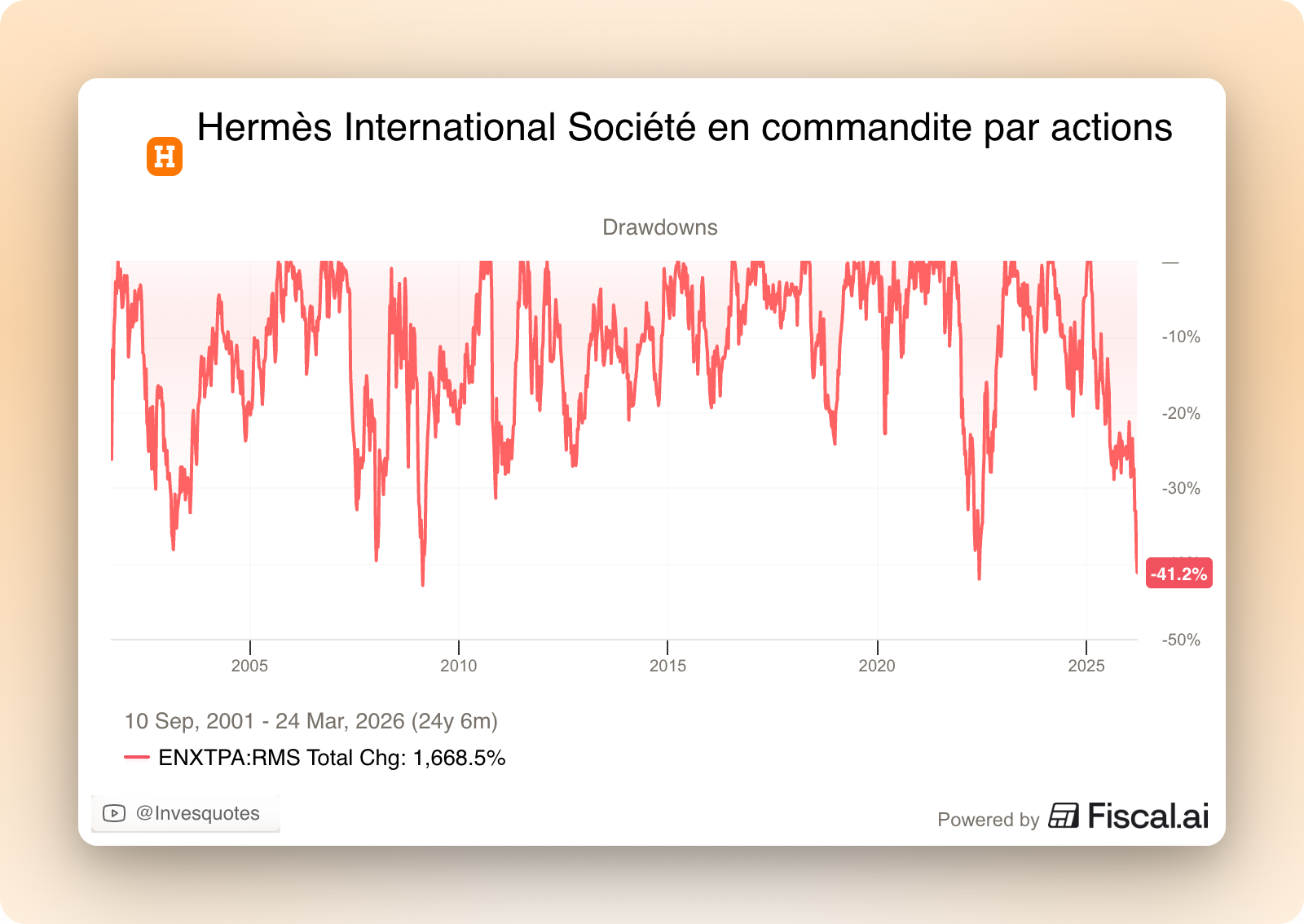

These three things have pretty much created a “perfect storm” for the luxury industry. Hermes’ stock is now in a >40% drawdown, a rare feat in its history as a publicly traded company:

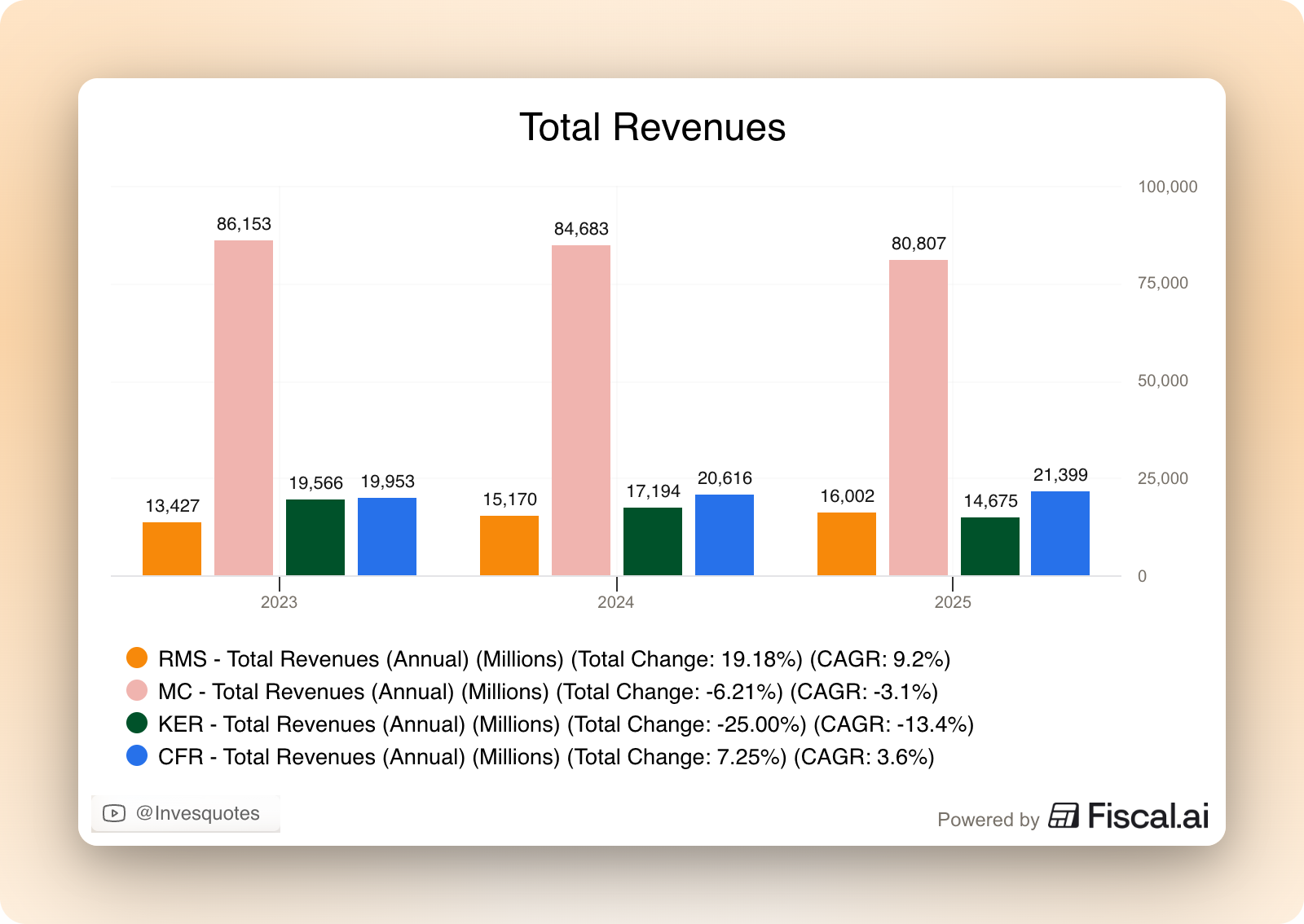

The interesting thing is that Hermes has continued compounding at a very good pace despite the noise (something that its peers can’t say). It’s in “perfect storm” periods like these when Hermes demonstrates that it doesn’t have many peers. Just for context, Hermes has grown its revenue at a +9% CAGR since 2023, whereas Richemont (the second fastest-growing company in the peer group) has grown its top line at a meager 3% CAGR. Other companies like Kering and LVMH have experienced revenue contraction over this period:

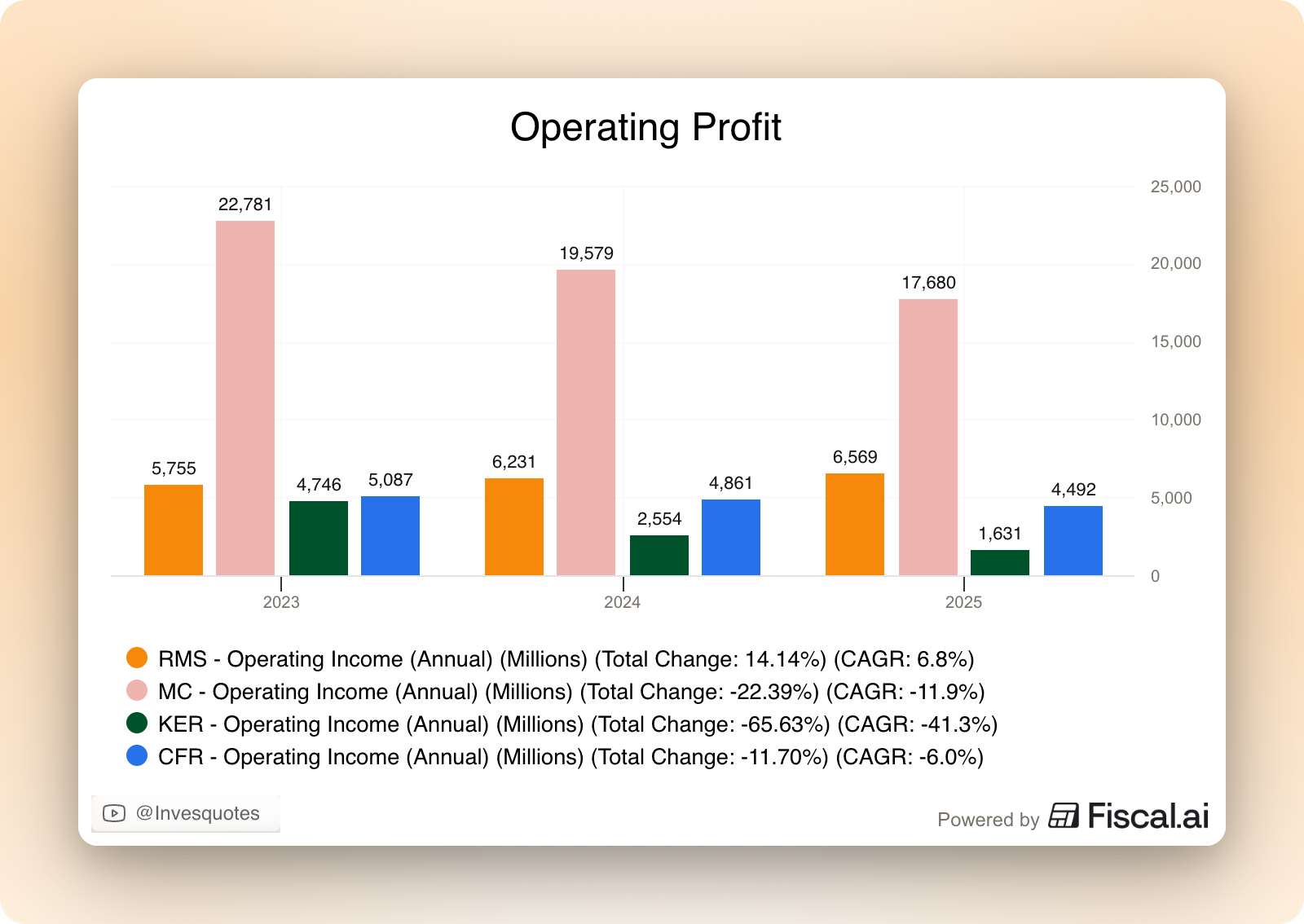

This resilience is greatly amplified when looking at operating profits. Margins have contracted across the board (including those of Hermes), but Hermes has managed to CAGR its operating profit at a 6% clip through the period. The rest of the peer group has seen operating profits contract, in some cases quite significantly:

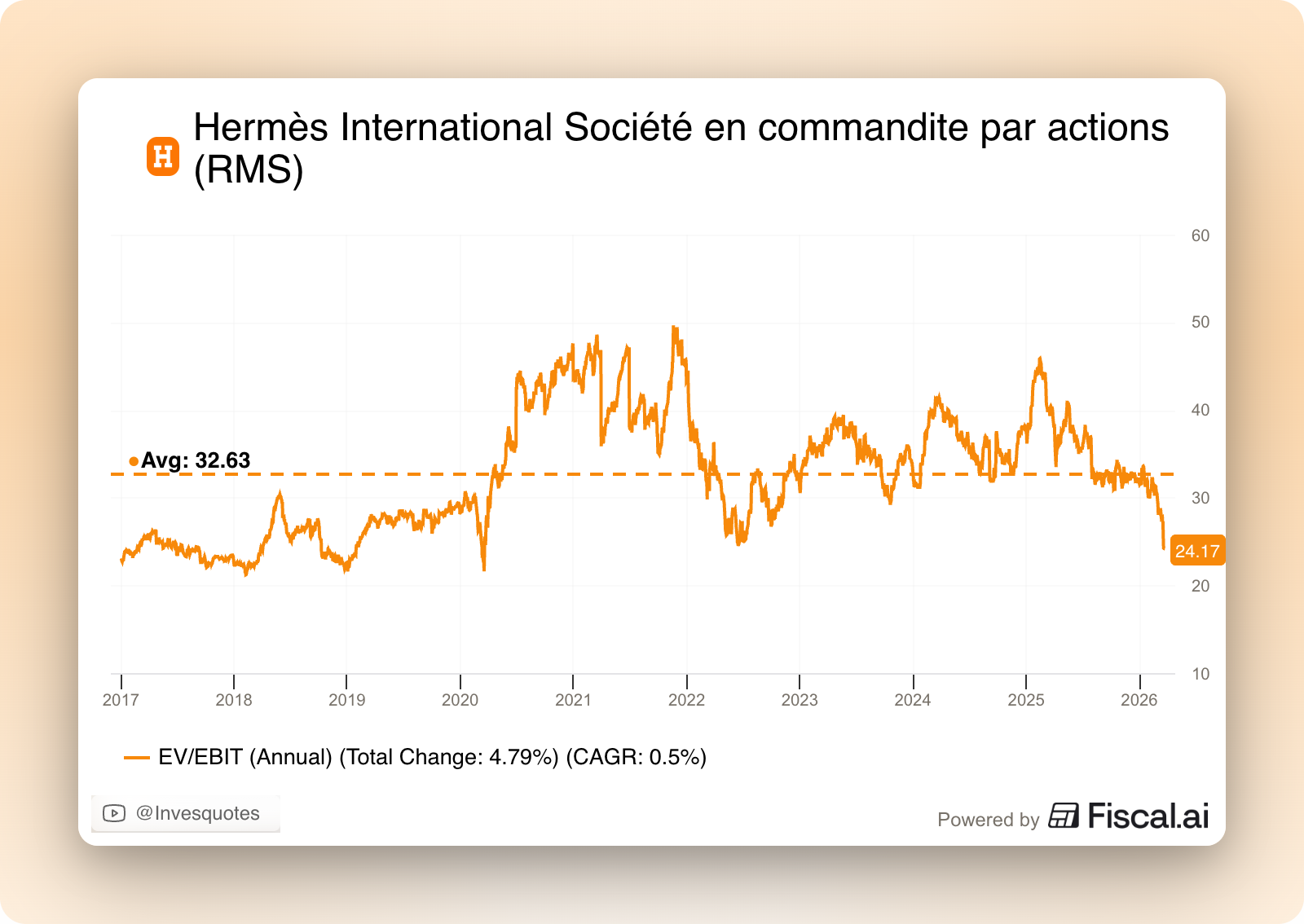

This continuous compounding (even if at a slower pace) combined with the stock price’s poor performance has led Hermes to trade at one of the lowest valuation multiples in a very long time. The company’s EV/EBIT multiple now lies significantly below its 10-year average, although this average is likely inflated due to the pandemic:

All this said and despite the 40% drop from ATHs, a 24x EV/EBIT multiple does not seem like a bargain. I’d argue, though, that multiples need some context:

Hermes’ market cap multiples are pretty misleading due to the company’s pristine balance sheet. There’s no special dividend coming this year, but the company is known for paying them in the past

Earnings are not normalized due to several one-time impacts (primarily related to tax, so this shouldn’t impact EBIT) and frontloaded investments into leather workshops

Hermes is a “special” company in terms of durability and predictability, two variables that determine how we should interpret its multiples

To understand what Hermes does and what makes the company special you can read my in-depth report on the company (I won’t go over it here again).

The good thing about Hermes is that its in-depth report is unlikely to become obsolete anytime soon.

The goal of this article is two fold. I’ll go over what many consider to be the main bear case (experiences secularly gaining share from personal luxury goods) and I’ll later go over the valuation (both through multiples and through a DCF).

Let’s begin with the former.

Experiences gaining share from personal luxury goods, existential to the story?

The most common bear case that I have read for Hermes goes along the following lines:

Luxury buyers have had enough of hard goods and will now pursue luxury experiences.

This is theoretically bad for Hermes because the company is not really into experiences and derives close to 100% of its profits from the sale of hard/soft luxury goods (aka: personal luxury goods). Now, the first thing we should strive to understand is whether this is true. Well, in the absence of perfect data, it does seem true that experiences are winning wallet share from hard/soft goods.

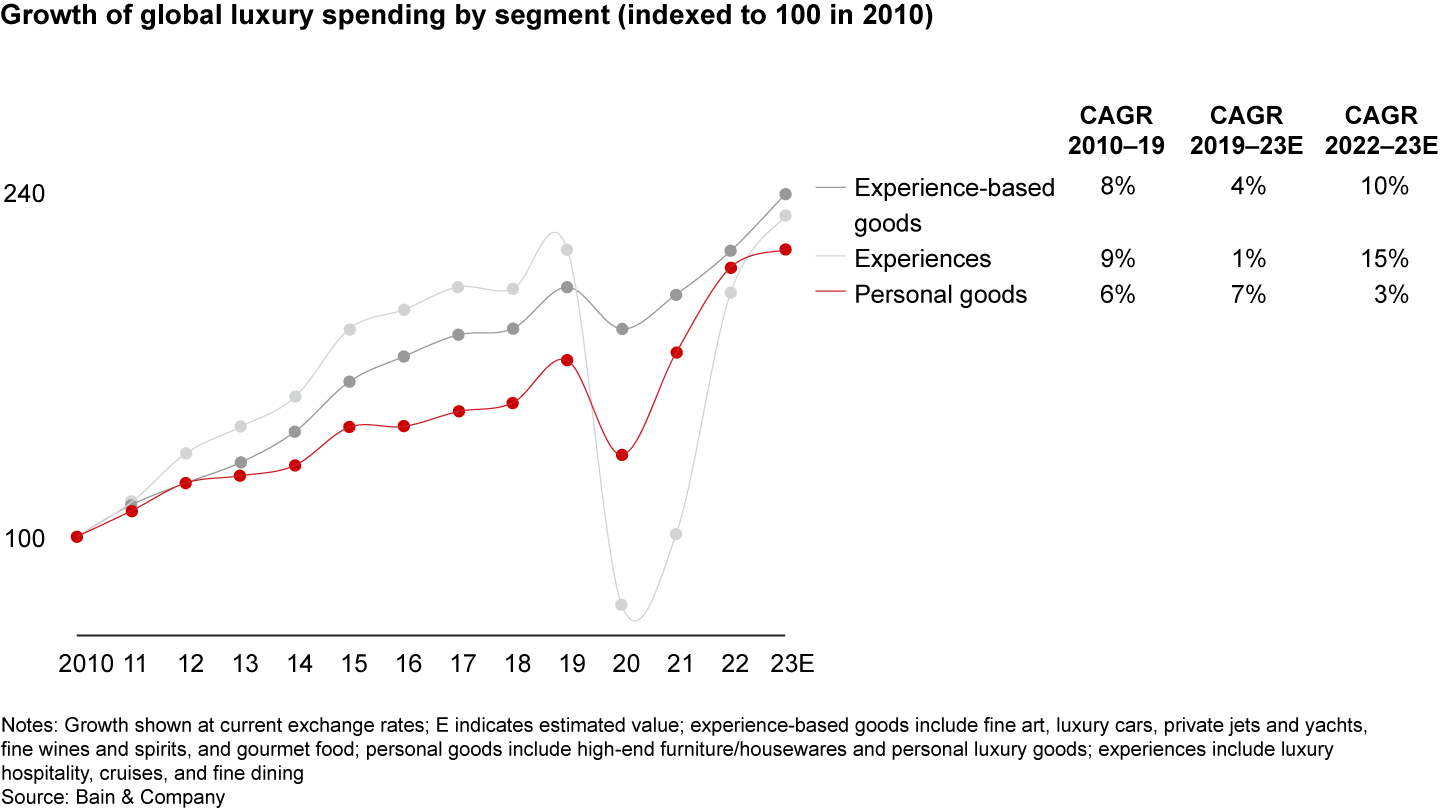

Bain & Company and Altagama claimed in their 2024 industry report that spending on experiences was pretty much the only growing segment across the luxury industry:

The overall luxury market tracked by Bain & Company comprises nine segments: luxury cars, personal luxury goods, luxury hospitality, fine wines and spirits, gourmet food and fine dining, high-end furniture and housewares, fine art, private jets and yachts, and luxury cruises. Luxury cars, luxury hospitality, and personal luxury goods together account for 80% of the total market. Overall, we estimate that in 2024 the luxury market’s retail sales value remained relatively flat at €1.48 trillion, with the final total likely to fall between a 1% decline and a 1% increase over 2023 at constant exchange rates. Only four luxury segments grew in 2024, all linked to experiences.

Bank of America also believes this shift is taking place and has credit and debit card data to back it up:

Consumers have also been foregoing luxury goods spending in favor of luxury services. Spending on high-end hotels has outpaced luxury retail spending across all generations, though with older generations outperforming younger cohorts.

Even though the transition to experiences has enjoyed its fair share of cycles in the past, the shift also seems structural. It’s not the first time that experiences momentarily gain share of hard/soft goods only to give back a good portion of these in the coming years, but the long-term trend appears evident:

Now, I don’t view this as an existential bear case for Hermes, for several reasons. First, personal luxury goods are unlikely to go anywhere even if they continue losing share to experiences in the coming years. The bottom line is that Hermes is likely to continue gaining share of a growing market (even if it’s not the fastest growing market). The fact that experiences will most likely gain share from PLG (Personal Luxury Goods) doesn’t mean that the latter will contract. Several industry sources size the PLG market at roughly $400 billion and forecast a CAGR of 4% up until 2030.

Hermes generated revenue of around $19 billion in 2025, meaning the company holds a sub-5% market share (note that the definition of PLG is critical here, and Hermes is likely to hold a more significant share in high-end PLG). Even if the company’s share gains stagnate (unlikely), Hermes could potentially grow at a MSD clip over the coming years despite the “experiences” headwind. Now, nothing indicates that Hermes should stop gaining share of the PLG market. The company has far outpaced PLG industry growth in the past and one could argue that the future is one with fewer credible competitors. Many companies have failed to “respect” the luxury strategy (I am looking at you, Gucci, Balenciaga…) and have therefore fallen to the bottom of the luxury pyramid. It’s interesting because Hermes’ management also believes that the downfall of many luxury companies has made them a beneficiary of what they term the “flight to quality:”

There’s a drop in the footfall of especially aspirational clients, which are particularly hard hit. Now, it’s true that the stock exchange and the real estate has a huge impact on our Chinese clients. Now, our Chinese clients are also extremely sophisticated. They’ve learned very quickly. From what I understand, they are currently looking for high-quality products, which is good for us. They don’t necessarily want a logo to be affixed to what they buy. There is this change, which we believe is underway and is positive for us.

All this said, the main “flaw” I see in the experiences bear case is the misconception of what Hermes sells. Hermes does not sell PLG, Hermes sells its brand through the sale of PLG. The company has been extremely successful in the past exporting the brand to different categories. Hermes started with leather for horse accessories, but quickly diversified into a wide variety of segments:

Source: Hermes

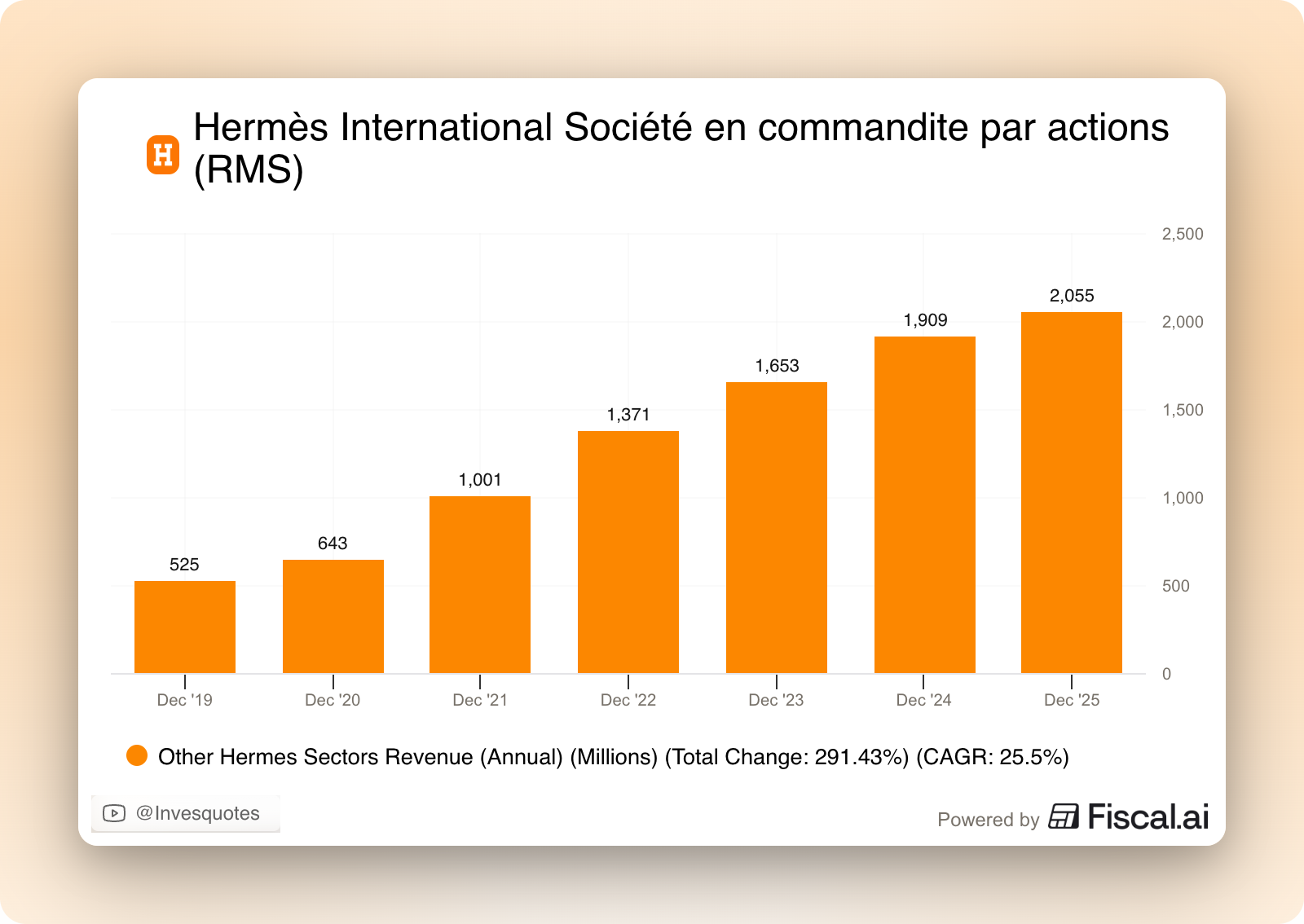

The size of its leather franchise still dwarfs other métiers, but Hermes’ other sectors have compounded revenue at a 25% CAGR over the last 7 years and now make up 13% of total revenue:

Many believe that the brand would not be “exportable” to experiences, but there’s no reason to believe Hermes could not be successful in experiences should it need to. Two reasons underpin this belief. First, Hermes has done it before. Secondly and probably more importantly: many other luxury brands have successfully undergone the transition. LVMH’s CEO, Bernard Arnault, began the transition in 2019 after acquiring Belmond:

The future of luxury will not only be in luxury goods, as it’s been for many years, but also in luxury experiences, and we want to be in both segments.

Experiences have grown fast at LVMH but are still far from becoming a significant profit driver, which somewhat demonstrates that PLGs are still the behemoth that is unlikely to fade away anytime soon. Hermes is historically known for being much more measured with “techtonic” shifts, maybe because the company rarely does M&A and builds (almost) everything organically. Now, despite Hermes having the optionality, it’s important to understand that…

Hermes doesn’t need to go into experiences to remain successful and relevant

Management has shown a preference to stay within hard/soft goods

What’s kind of ironic is that one could attribute Hermes’ success in PLG precisely to its focus. While many luxury houses pivoted to experiences and rushed to capture the aspirational luxury buyer, Hermes remained loyal to its belief that the product is the experience, therefore avoiding spreading itself too thin. This focus has probably been the route cause of the continuous share gains, which are unlikely to end anytime soon. So, no, I don’t really think that the shift to experiences is an existential threat to Hermes’ business. Not only can the company pivot if needed, but it basically doesn’t need it as it gains share in a PLG market that continues to grow at a decent pace.

Unquestionable quality, but is Hermes cheap today?

There are two ways of looking at Hermes’ valuation (or that of any company): through multiples and through a DCF. Even though both should yield equivalent results when done coherently, I believe a DCF is a much more appropriate way of valuing Hermes. The reason is that the durability and predictability of this business makes the multiple an ill-suited metric.