Full Steam Ahead

Keysight’s Q2 2025

Keysight reported great earnings this week. The company delivered a beat, beat, raise quarter despite being exposed to the Capex cycle of its customers in a turbulent macro environment. Capex is, in theory, one of the first things that businesses cut when volatility increases, but Keysight seems to be defying economic laws. This has probably something to do with the fact that Keysight is more exposed to the strategic CapEx of its customers, more than the discretionary portion of it.

The market evidently liked the results, and Keysight’s stock started the day rising significantly (it eventually gave it all up when the market started to drop):

I’ll go over three things in this article:

The numbers

The highlights from the call

The valuation (I’ll explain why I am not discussing it in detail in this article)

Without further ado, let’s start with the numbers.

The numbers

Here’s the summary table for Keysight:

The first thing I would highlight is the state of the cycle. The trough of the cycle seems to be a thing of the past; Q2 was the second consecutive growth quarter, growth is accelerating, and it’s pretty obvious the recovery is in full force:

Strength was also broad-based this quarter. CSG and EISG grew this quarter (it was EISG’s first quarter of revenue growth after 6 quarters of declines). Within CSG, both wireless and wireline grew:

If a “BUT” can be given to this release, that was the gross margin contraction. This contraction was caused entirely by a $7 million tariff impact. Without this, gross margins would’ve slightly expanded (I’ll discuss tariffs later on in more detail).

The gross margin “weakness” is also caused, to an extent, by the cycle's recovery. Keysight enjoys significant operating leverage as the cycle recovers (evident in the operating margin expansion enjoyed this quarter) because it treats many of its operating costs as fixed, but its gross margin can suffer some headwinds from mix. The underlying reason is that as customers order more equipment, the proportion of software over total sales decreases and negatively impacts margins. Software as a percentage of revenue was down 300 bps year over year and down 400 bps sequentially. Management still sees significant opportunity for software and ARR (Annual recurring revenue) to make up a more significant portion of the pie in the future, but it’s undeniable these KPIs tend to peak at cycle troughs!

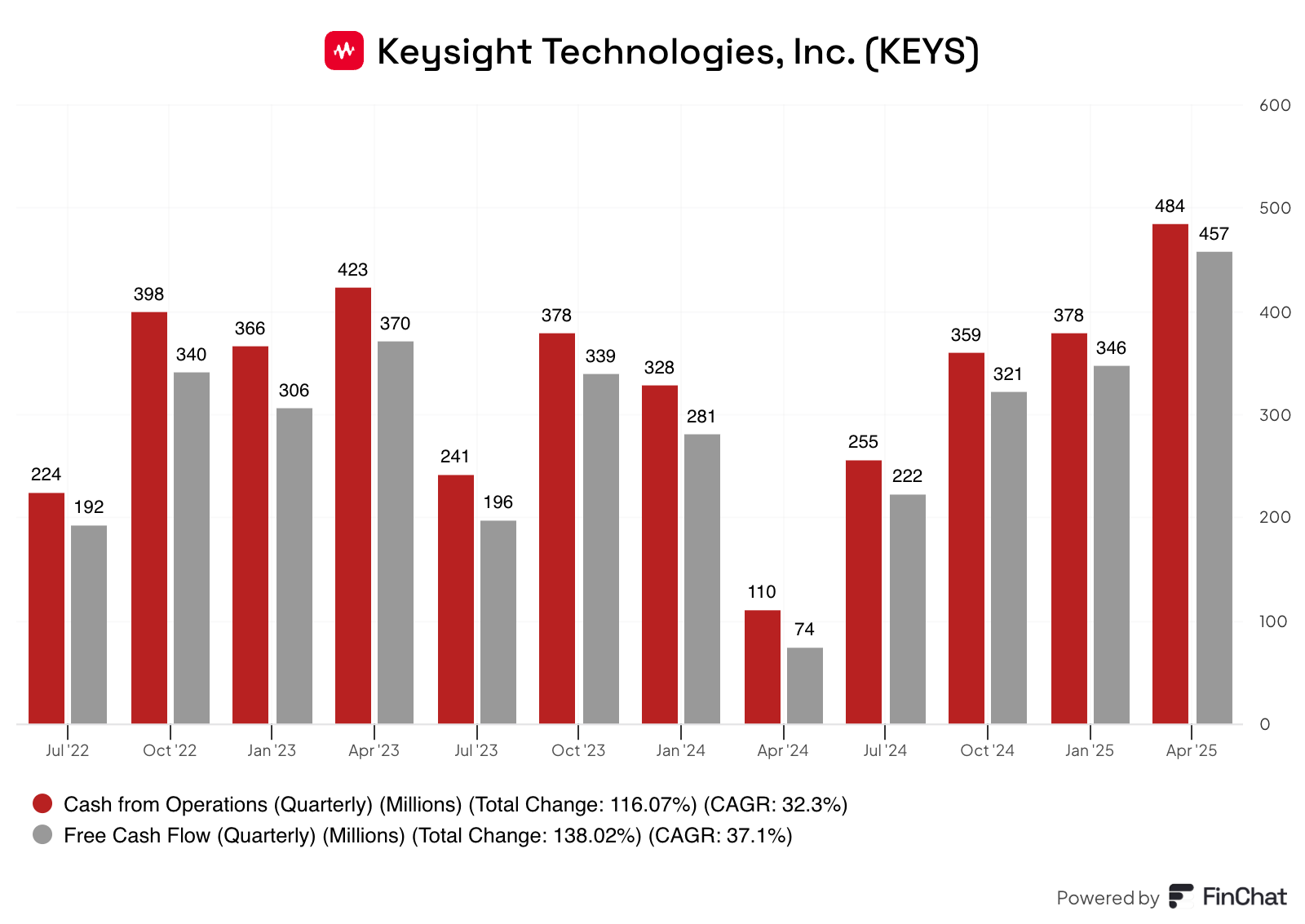

I would be careful with taking some of this quarter’s numbers at face value, namely GAAP net income and cash flows. Both rose tremendously this quarter, but for reasons we could deem non-recurring. Net income enjoyed a $112 million other income benefit (we will have to wait until the 10Q is published to know what this was exactly composed of). Regarding cash flows, Keysight enjoyed a $60 million gain on a hedging contract related to the Spirent acquisition (probably included in the $112 million shown in the income statement). This, together with favorable working capital dynamics, helped boost cash flows:

I wouldn’t consider these increases sustainable, but Keysight’s operating leverage is undeniable. GAAP operating income rose 17% on the back of a 7% revenue growth. Yet another place where operating leverage is evident is in the annual guide. Management raised the revenue guide from 5% to 6% and claimed that EPS will grow slightly ahead of 10% this year. This would not be that impressive were it not for the fact that it includes the tariff impact! We must also not forget that management tends to be pretty conservative with guidance. Just for context, Keysight beat the high-end of its EPS guidance this quarter despite tariffs being unknown at the time of setting it (tariffs ended up subtracting $0.04 in EPS in Q2). In my in-depth report, I contextualized management’s conservatism:

Since its IPO in 2014, Keysight has maintained a long track record of conservatism regarding guidance. The company has beaten its own expectations for 10 consecutive years.

Death, taxes, and Keysight’s management being conservative! Note that this guidance is purely organic and therefore doesn’t account for Spirent or any of the assets coming from Ansys/Synopsis. Should these acquisitions materialize in Q3/Q4, we should…

See higher revenue growth this year

See lower operating margins but higher gross margins

I would expect Keysight to aggressively work through operating synergies in the coming quarters, but the acquired businesses are more software-focused and therefore carry a higher gross margin than Keysight.

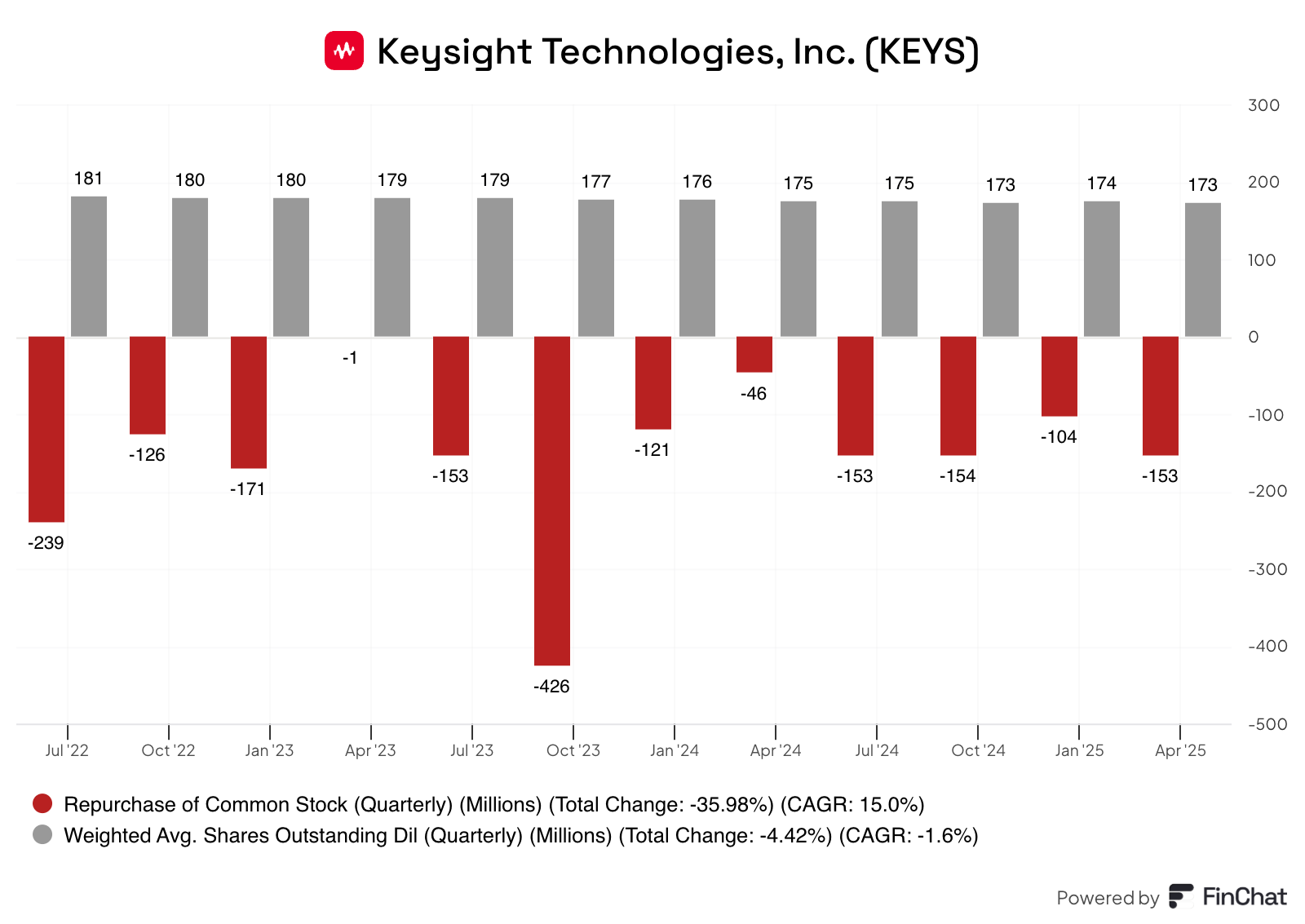

It’s also great to see Keysight generating significant sums of cash that it can later use to repurchase shares. This quarter gave a pretty good opportunity to the company to repurchase shares at attractive prices: management repurchased around $150 million at an average price of $144.

I expect share repurchases to moderate now that Keysight has to acquire Spirent and some assets from Ansys/Synopsis, but the company has a strong financial position to continue repurchasing shares even post-acquisitions. It was undeniably a strong quarter by Keysight, and hopefully just a small taste of what’s to come.

Tariffs, Defense, and a read-through for Judges?

Tariffs were probably the most discussed topic during the call (no surprises here!). Management’s commentary was actually pretty similar to that of Deere. First, the tariff impact is expected to be limited because Keysight’s supply chain is not overly exposed to China. Management diversified its supply chain away from China to Southeast Asia, and US/China flows are only 10% of the full impact for the year. The gross impact from tariffs for the full year is expected to be around $75-$100 million. Management was asked about offsets to this impact, but just like Deere, they mentioned that they will commit to the prices on their backlog. This means offsets might take some time to run through the order book. The good news is that earnings are still expected to grow north of 10% this year despite tariffs.

The Trump administration can, however, be positive for Keysight’s defense business. Management mentioned that they are seeing significant strength in their European defense business:

We saw some good order bookings with our prime contractors in the US and actually had a double-digit growth in our European business.

Keysight, however, did mention weakness in the US education funding environment, just like Danaher did a couple of weeks ago. This should theoretically not be great news for Judges Scientific, but as I discussed in my Danaher earnings digest, the impact is likely to be limited + the stock price of Judges seemed to already be pricing it in (the stock is now up 40%+ from the lows):

The negative aspect was that Danaher alluded to the academic and university environment slowing down significantly in the US due to the uncertainty surrounding funding. In a recent news of the week, I mentioned this as a potential headwind for Judges due to its exposure to universities (universities made up around 50% of Judges’ revenue in 2024). The exposure is more limited once we put it in the context of the US (note that Danaher alluded to this being a source of weakness for the US in particular). In 2024, approximately 25% of the Judges’ revenue was generated in North America. Assuming the same customer distribution in North America as elsewhere, the real exposure would be around 12% of total sales. Still high, but manageable.

Taking a look at the company’s valuation

Keysight is now trading only at a slightly higher price than when I released my in-depth report. Even though we have incrementally positive guidance, I will not revisit the valuation in depth. You can find information about the valuation in the in-depth report and last quarter’s earnings digest.

My purchase price remains the same.

Have a great week,

Leandro