A Credible (and Terrible) Bear Case (NOTW#83)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of subscribers today:

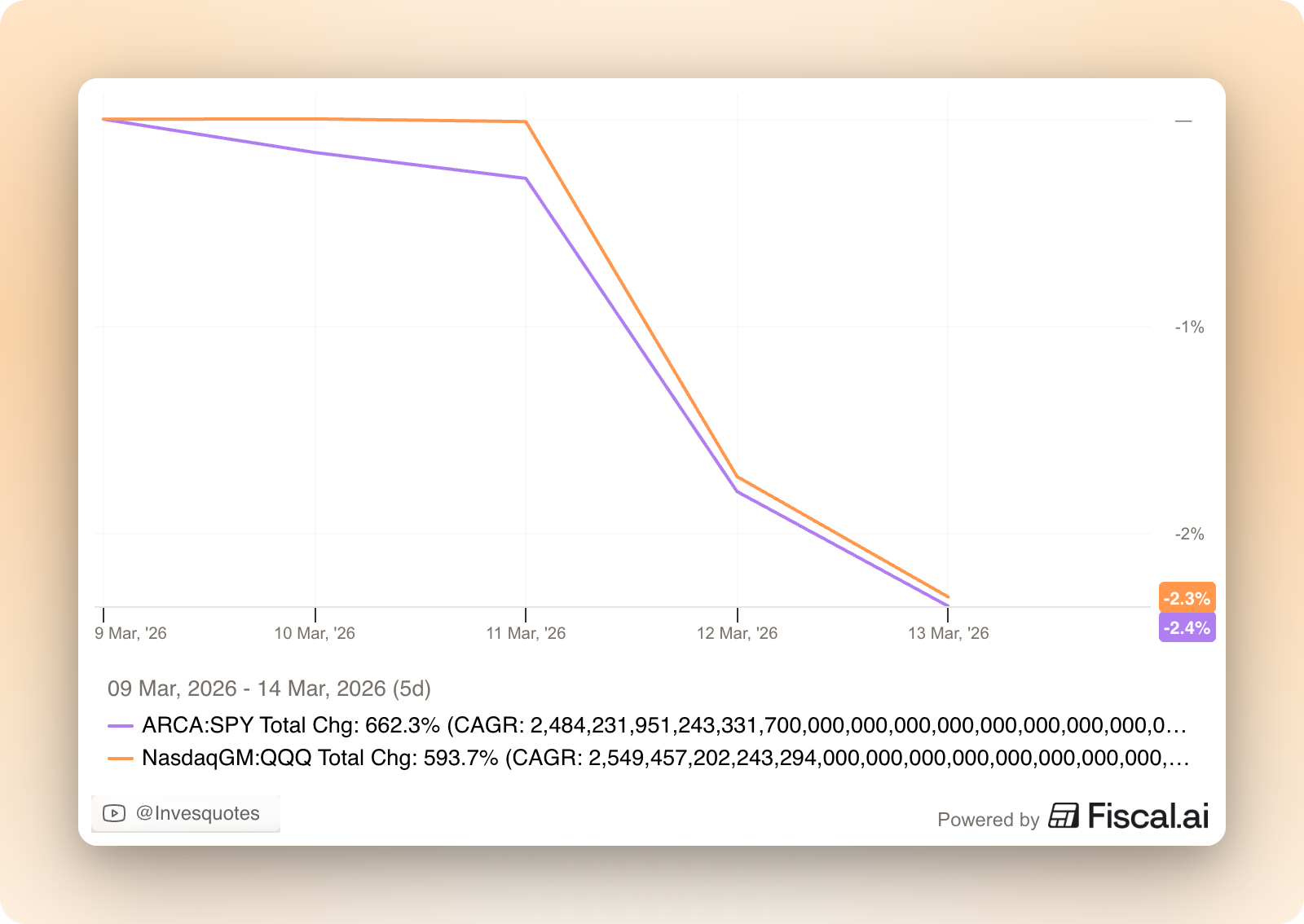

Both indices were down again this week driven by the conflict in Iran and the impact it might have on oil prices. I discuss this at length in the brief market commentary. There was also other relevant news across several portfolio companies.

Without further ado, let’s get on with it.

Articles of the week

I published two articles this week. The first one was Constellation’s earnings digest.

New Horizons

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

The company not only reported good earnings but also held its first earnings call since 2018.

The second article of the week was the earnings digest of the latest addition to my portfolio.

Fundamentals up, stock price down, expected IRR increases from 16% to 20%

A couple of months ago I added a new company to my portfolio, and the company recently reported earnings. These were (again) spectacular, but the stock price dropped for unknown reasons (as it’s also not expensive). This resulted in an increase of

The company was able to sustain its 37% 3-year CAGR and continues to gain significant share in its industry thanks to its disruptive nature.

Without further ado, let’s see what the markets did this week.

Market Overview

I am not going to discover anything new by saying that it’s a volatile market and world out there, albeit probably less than one would’ve imagined with the scale of the operation in Iran and what’s going on with energy prices. Indices were significantly down this week after being down considerably last week (the magnitude of the drop should be contextualized acknowledging these are diversified indices):

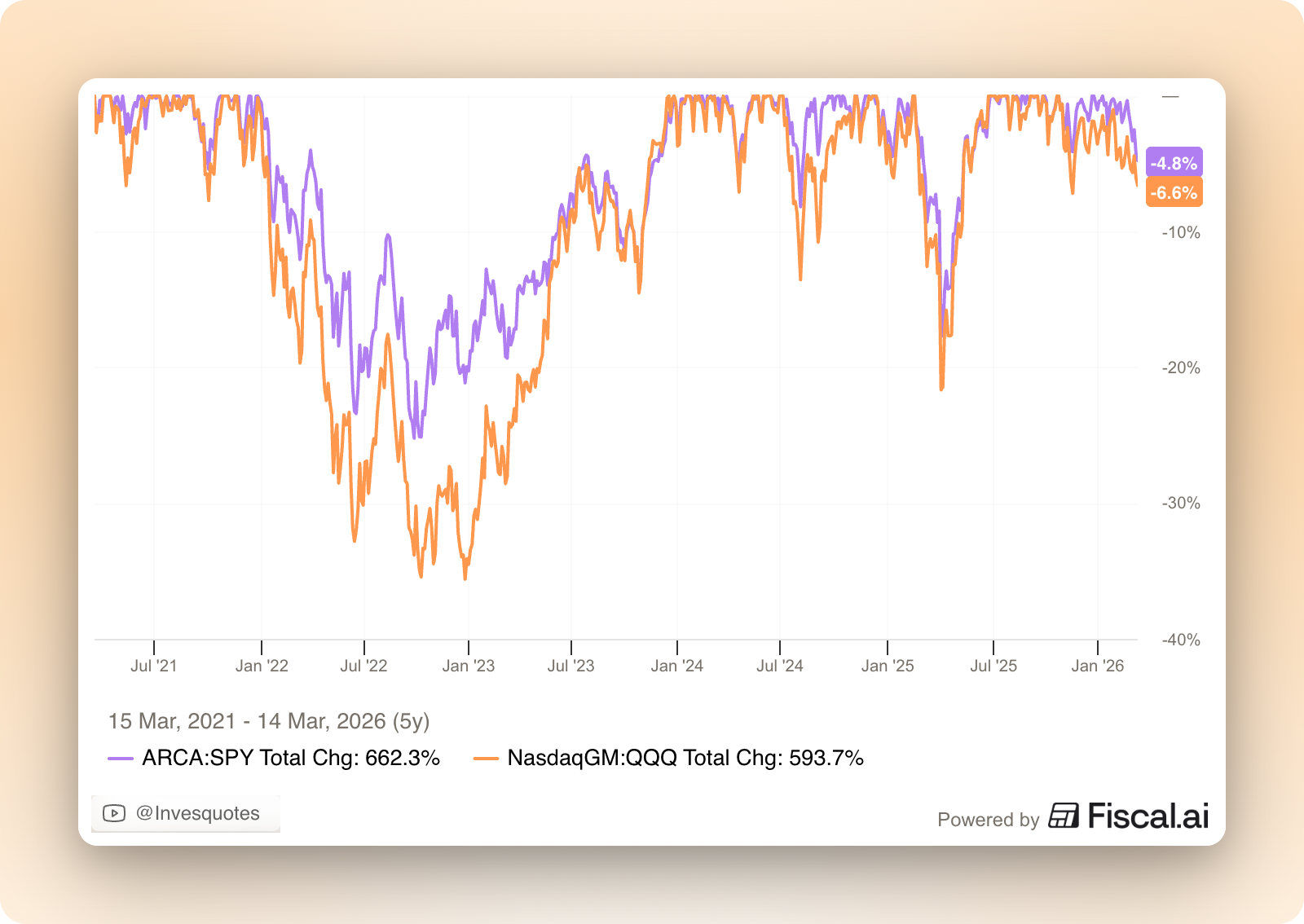

Despite these drops and the fact that there’s a full blown war in the Middle East that is causing oil prices to rise considerably, indices are “barely” 6% off highs:

Knowing what will happen from now on is pretty much impossible, but 6.6% off ATHs surely does not seem like the drop we’d have if markets expect the conflict and its impact on oil prices to be long-lasting. I believe the market is sort of cautiously pricing in that the conflict will be short-lived, maybe supported by the fact that Trump has shown a tendency to care about markets (i.e., TACO). Now, TACO gained popularity during the Tariff tantrum, but I’d say tariffs were a self-inflicted wound and therefore solvable with just a “simple” shift (I should remind you, though, that many believe that it would be a structural impact). This situation honestly seems much more complex because it involves a war and many more players, meaning that it’s probably not solely Trump’s hands, at least not to the extent all the Tariff situation was (Ps#1: I don’t consider myself an expert on geopolitics so take everything here with a grain of salt. Ps#2: I don’t think anyone is an expert on geopolitics).

The bear case here is that the conflict lasts longer than everyone expects, which creates an upward pressure on energy prices on an economy that is not precisely the strongest it has ever been. This ultimately creates a stagflationary period through which the Federal Reserve (and other Central Banks around the world) is forced to make a tough decision on interest rates. I hate to be the bearer of bad news, but this is something that could definitely happen so we shouldn’t be too surprised if it does (i.e., the probability is above 0). A “less-terrible” case is that the conflict gets resolved relatively soon but that it still has a lingering impact on energy prices (less long-lasting, though). I would imagine it’s this last case that the market is pricing in.

The bull case (or maybe the less-terrible case) is that (once again) the world adapts. Without being an energy expert I believe there are several levers to pull here. First, the Strategic Oil Reserves, both in the US and across the G-7. There have already been rumours that hundreds of millions of barrels might be released from said reserves, which would help tame the supply shock caused by the conflict. Now, this is 100% a short term solution that can’t be prolonged indefinitely.

The second lever is Saudi Arabia’s West Coast. Several sources have confirmed that tankers are now heading to the West Coast to pick up barrels, bypassing the Strait of Hormuz entirely:

Saudi Arabia apparently had built a massive pipeline to be able to transfer oil to the West Coast should they need to, and well, they need it now. This is probably not going to be a long term solution either because the capacity to ship barrels from the West Coast (around 5 million barrels per day) is considerably lower than that of the East Coast (around 20 million barrels per day), but it’s definitely better than nothing. There are also other risks in the West Coast like Somali pirates and the Bab-El-Mandeb strait which the Houthis promise to disrupt if Iran wants, but this definitely seems more manageable than mines and going against Iran’s army. We’ll see how this develops but a potentially terrible scenario here is that both of Saudi Arabia’s export routes get closed down, something that has never happened in the modern economy and which will likely put significant pressure on oil prices.

Even though I know energy “experts” will say this does nothing to reverse the situation, I believe it shows how adaptable the world (and the human being) is when they truly need it and when powerful incentives are in place. I am well aware that the bear case can play out, but we must not forget that there’s no incentive for it to play out and that political leaders will do whatever it takes to avoid a full blown crash. Modern western societies have zero capabilities to sustain suffering and we have midterms coming up. Humans can go great lengths to pursue their interests, will this time be different? Now, with this said, it would not be the first time (nor the last) that humans make a mistake that they can’t reverse, will that be a similar situation today? Only time will tell.

Trump also announced during the weekend that the US had bombed Kharg Island. He was quick to point out that only military bases had been impacted, leaving oil infrastructure “untouched.” Sentiment on X is terrible after this move and everyone is claiming that we are going to have another Global Financial Crisis, which makes me think we are actually not going to have a remotely similar situation. The bear case is always in play, but remember that just last weekend people were saying the same thing: oil above $150 and Black Monday. None of the two things ended up happening but still the same accounts that incorrectly made those forecasts are back at making them again with a high degree of confidence. It’s pretty incredible how macro bears can simultaneously have a high ego with a terrible success rate, but it happens. Of course, they will eventually be right and they will promote the hell out of the times they are right (not many). The bear case is ALWAYS scary, and I must say it does seem scarier today than what stocks are pricing in, but that doesn’t mean that it has to necessarily play out like fear mongers think it will.

The industry map was pretty much red this week:

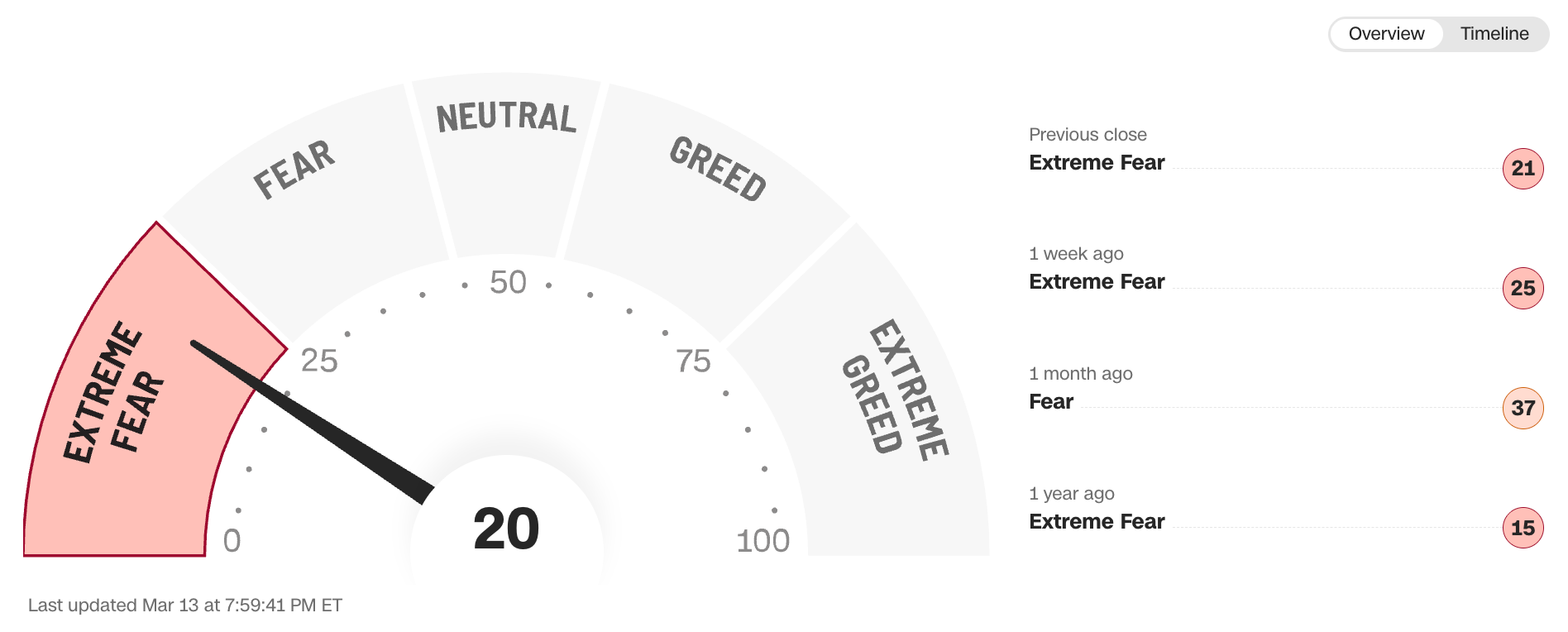

The fear and greed index worsened again and remains in fear territory:

My transactions this week

This week I added to one position which dropped considerably despite reporting outstanding earnings: