A broadening bull market without Nvidia? (NOTW#92)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

Both indices were up again this week, with tech leading the way. One thing I found interesting is that the bull market seems to be finally broadening out. Will it last? We’ll see. I also discuss Nvidia’s case in the brief market commentary.

Without further ado, let’s get on with it.

The new in-depth report

I didn’t publish a NOTW last weekend, but I did publish my new in-depth report on Eurofins Scientific (EPA:ERF) last Thursday:

The report is available to paid subscribers and goes over the following:

Section 1: What Eurofins does

Section 2: The growth levers and the lost credibility

Section 3: The transformation (?) of the financials

Section 4: Management, Incentives, & Capital Allocation

Section 5: The valuation

Eurofins is one of those companies that fits my investment mold to perfection: outsider/founder led, ignored by the market, and in a defensible industry offering pretty appealing returns. I share my model in the report and explain why I believe the company is positioned to deliver a 15% IRR over the next 5 years.

A webinar next week

Next week I will be hosting a webinar to discuss some changes I’ve made to the spreadsheets that paid subscribers have access to. I have built a new IRR vs Risk Score grid that should help frame the portfolio management decisions I make. I’ll share more details during the webinar and I’ll also…

Give a brief presentation on Eurofins

Answer all the questions you have

I’ll share more details with paid subscribers this week and will provide some means so you can ask your questions. The webinar will most likely take place Wednesday or Thursday.

Articles of the week

I published two articles this week. The first one was the 3rd edition of “On The Radar,” in which I shared three companies I have recently come across and which I believe are interesting:

A company that owns several monopolies that benefit from network effects (no, it’s not Meta)

A platform company currently viewed by the market as an AI loser (I don’t think the market is right on this one)

A network equipment business run by what I would consider a very unconventional outsider

The first one is shared for free with the remaining two being reserved for paid subscribers.

The second article of the week was Keysight’s earnings digest. The company reported again spectacular earnings driven by AI, but Keysight is much more than AI. I explain why in the article.

Without further ado, let’s see what the markets did this week.

Market Overview

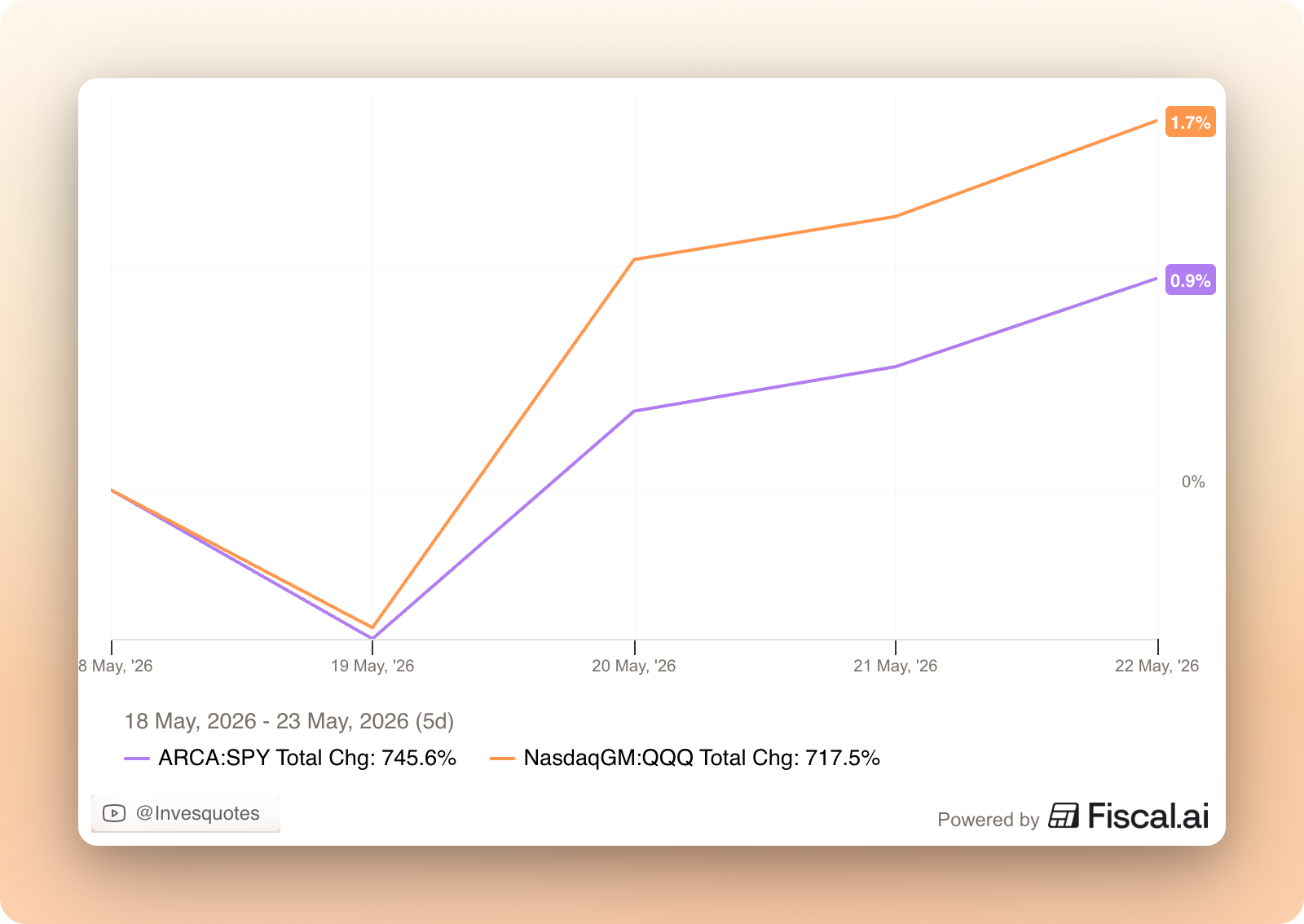

Both indices were up again this week, with the Nasdaq leading the way once again:

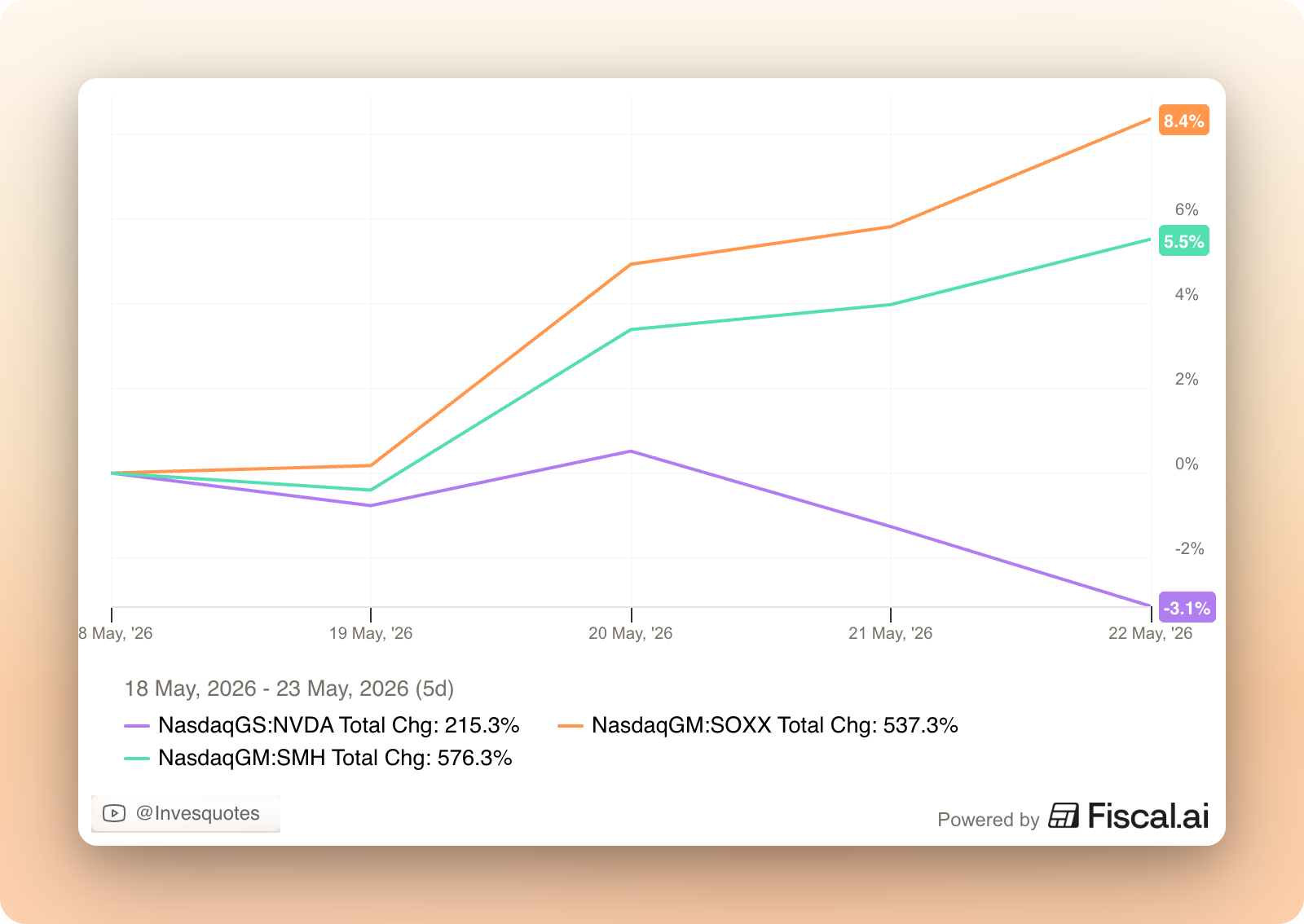

All eyes were on Nvidia’s earnings this week. Investors were wondering whether the company would report a spectacular quarter to keep the AI trend going, or if it would report a “disappointing” quarter that suddenly stopped the AI trade. Well, the outcome was probably not what many expected. Despite reporting a spectacular quarter once again, Nvidia’s stock dropped more than 3% during the week, but the SMH/SOXX did well overall (strange?):

Is Nvidia, the king of AI, being left behind in the AI trade? If we look a bit further out, we can see that this seems to be indeed the case. After doing considerably better than the semis industry, Nvidia has underperformed pretty significantly the semiconductor indices over the 1Y and shorter time frames:

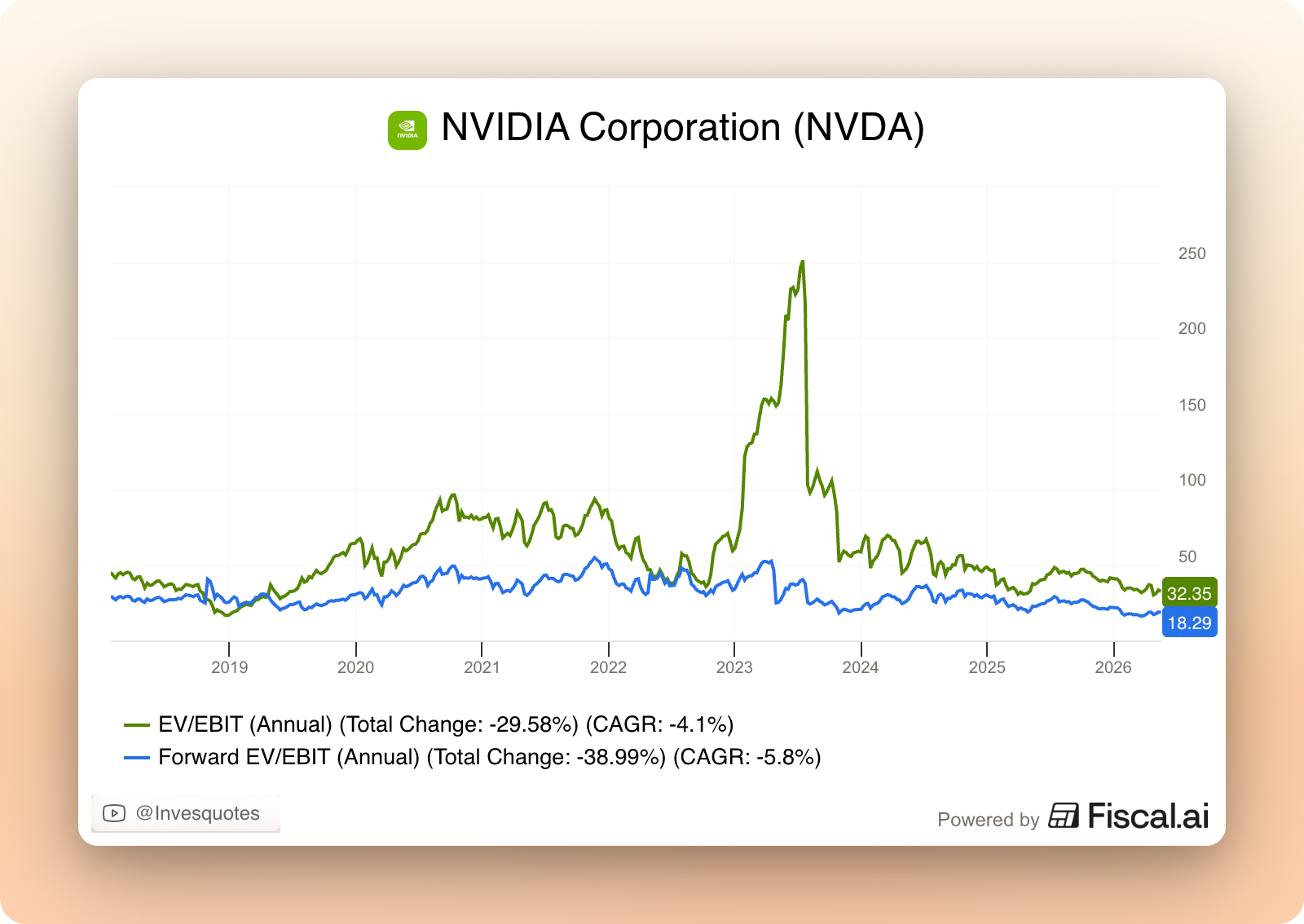

This is pretty amazing especially when considering the spectacular earnings that Nvidia has been posting lately. This hasn’t stopped the stock from not doing much since November 2025, but of course, the spectacular earnings together with the company’s spectacular performance has led to significant multiple compression. Nvidia has a LTM EV/EBIT multiple of 32x, but because the company is growing EBIT at a 147% clip, its forward EV/EBIT multiple is just 18x:

One can have several concerns regarding Nvidia (margins, growth sustainability…) but it seems undeniable that if the growth is sustainable or simply compresses to a more moderate clip, the shares are cheap. I’ve been reading more about Nvidia, its physical AI strategy and how it’s building ecosystems (which positively impacts other companies in the portfolio) and I am liking what I see (and importantly, also learning a lot of things that could lead me to other interesting companies).

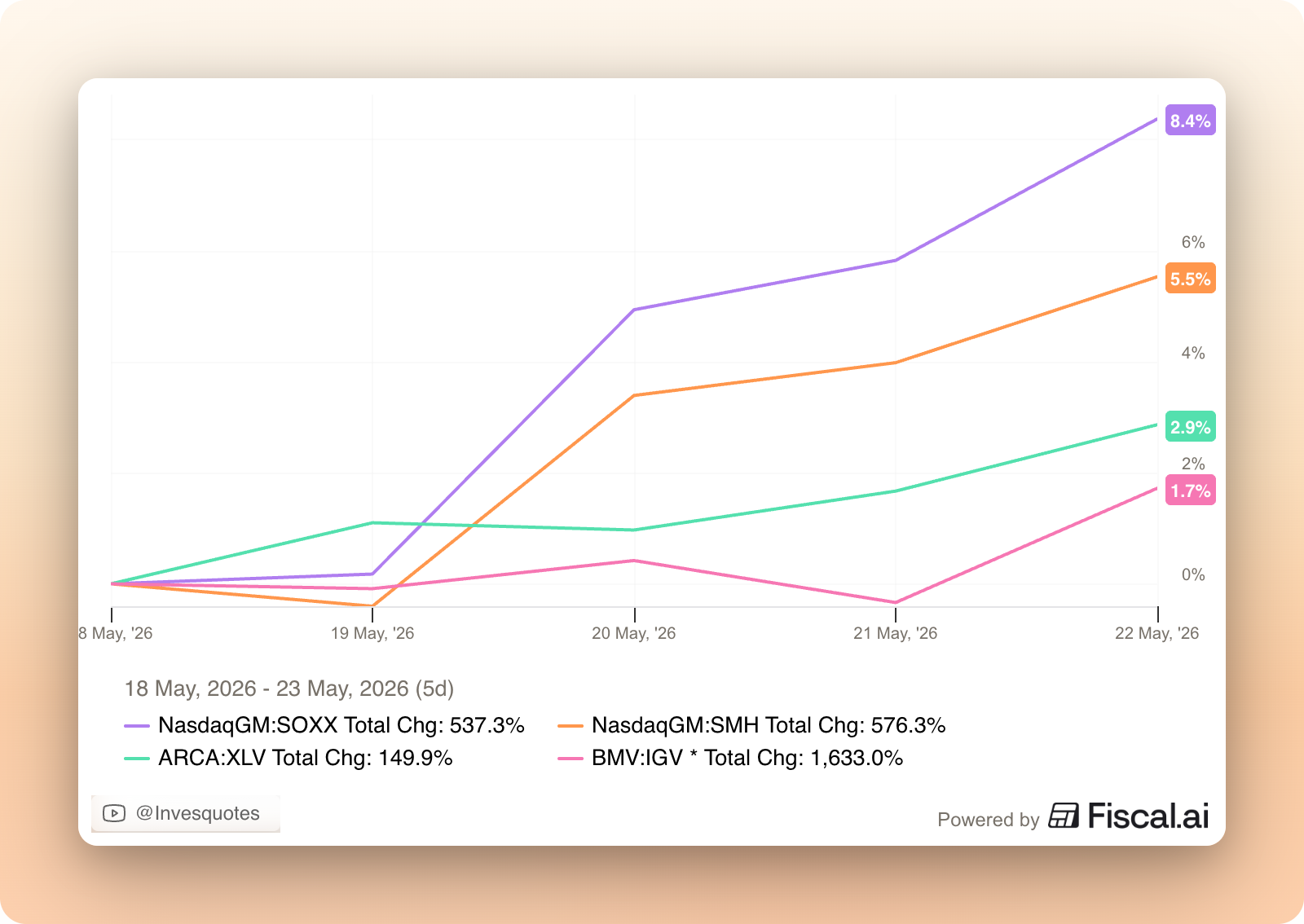

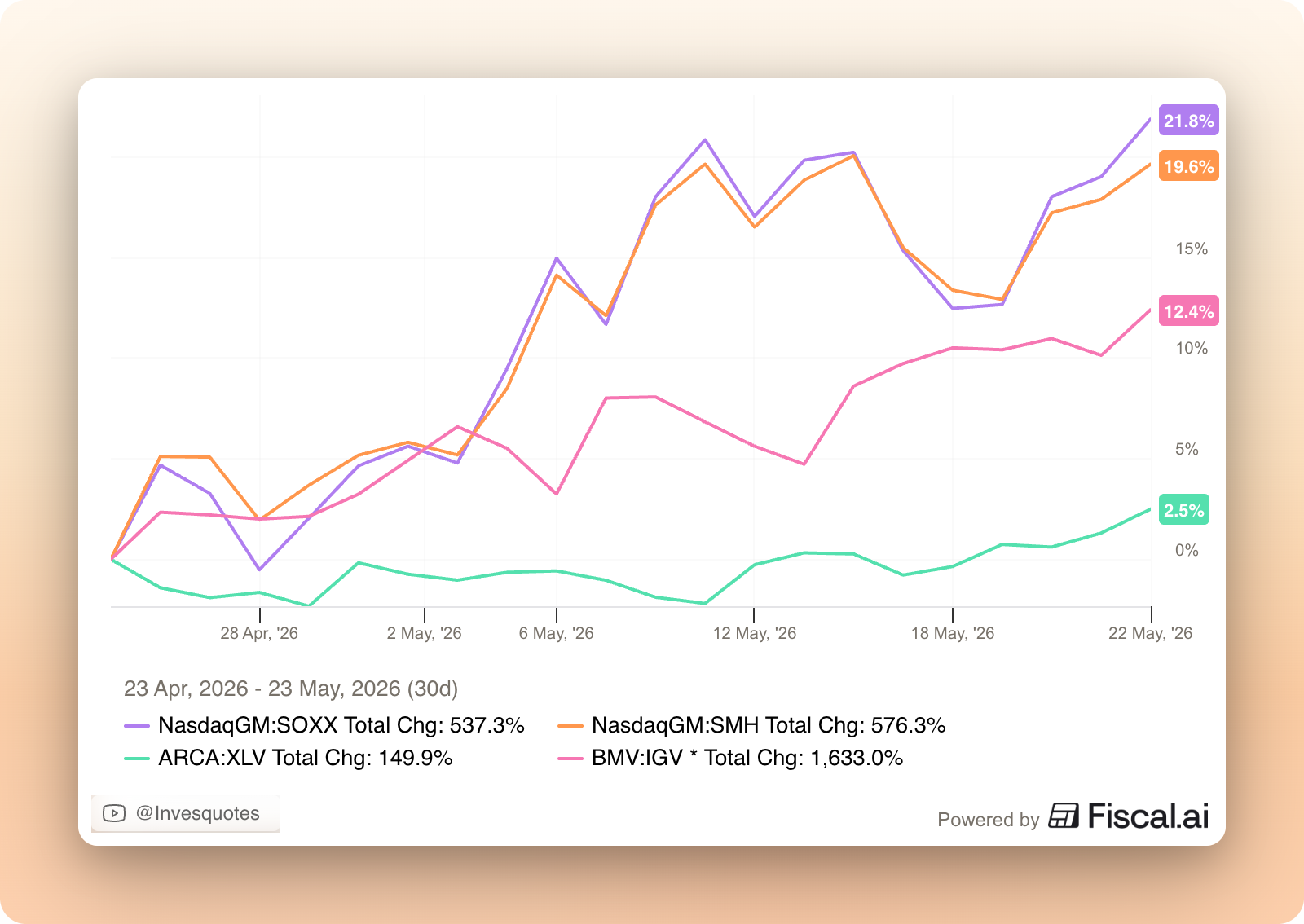

Now, the fact that the AI trend continues to be alive doesn’t mean that there can’t be a “rotation” outside of semis/tech to other sectors. One thing that continues to surprise me is that we are jointly seeing semis/tech go up along with other sectors that have historically been the other side of the coin. This is evident in the 5-day chart…

…but also if we go a bit further out:

So, semis continue leading, but it seems like the bull market is broadening and that investors are starting to believe that several industries can do well at the same time. We’ll see how this ages!

The industry map was pretty much green this week with some exceptions:

Source: Finviz

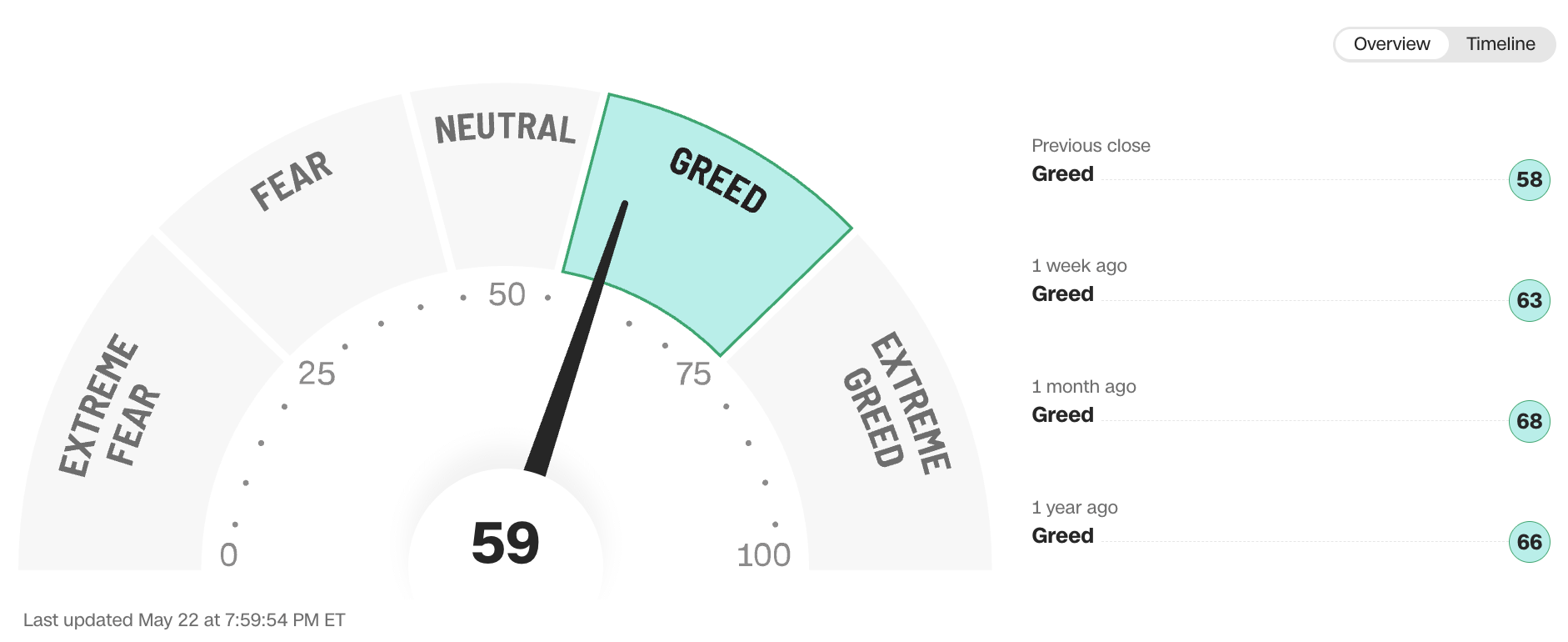

The fear and greed index remained in greed territory:

Source: CNN

I trimmed one position this week

This week I trimmed one of my positions for the third time. The company is outstanding but has skyrocketed driven by the AI trade and I don’t view the risk/reward as enticing as it was in the past.

I still hold it and it has been a great investment, delivering a 120% return in less than a year and a half for an 80% CAGR: