When Money Sleeps

Some thoughts about dead money

This article is free to read, although I would like to ask you a favor: that you share Best Anchor Stocks with people you think might be interested in my work.

This is something that should not take you much effort and is very important for me to continue growing Best Anchor Stocks.

Thank you very much and I hope you enjoy the article!

Hi reader,

If you’ve been investing for a while, you’ve probably come against the expression “dead money” more than once. This is a fairly common expression in the investment world and one that has probably caused some harm to the long-term performance of many investors. The “dead money” expression is mainly driven by the mantra that investors should be right at precisely the right time. I wanted to share some thoughts about it in this article.

First things first: what does the “dead money” expression describe? Dead money is Wall Street’s most feared expression (not really, but surely up there) and it defines a situation in which an investment does “nothing” for a long period due to the absence of any given catalyst. In simple terms, dead money defines a situation where a stock is flat for an extended period.

There are many examples of dead money charts in financial markets (especially after the pandemic boom and bust), several of which lay in my portfolio. Deere might be a good example here. The company’s stock has been pretty much flat for the great part of the last three years. We can see something similar with Zoetis. The stocks of these two companies have been pretty much flat since 2021 despite both indices advancing significantly since then:

What’s interesting about Deere and Zoetis is that both have been dead money for different reasons (more on this later).

As you might have (rightly) imagined, most investors try to avoid dead money situations, not only because they don’t provide good direct returns but because they carry an indirect blow to returns in the form of opportunity cost. Money invested in a dead money situation is money that can’t be reinvested elsewhere, and the impact of this opportunity cost, while apparently “invisible,” becomes pretty apparent if we crunch some numbers.

Imagine you had invested in a stock that does nothing for the next 5 years, a period through which the market compounds at an 8% clip. In year 5, you’d look at your investment thinking it’s been a bad investment, but hey…”at least I’ve not lost money” (I am ignoring inflation here). However, the reality is that you’ve indeed lost money (or better said, not made it) by not investing in the market (or any other investment that worked). In this scenario, an index fund would’ve yielded a total return of 47%.

With this concept of opportunity cost in mind, why Wall Street (and investors in general) try to avoid dead money situations starts to make more sense. Everything seems fairly logical until here, but there’s a problem: avoiding dead money situations relies on two premises that are unlikely to be true in real life:

Investors are good at timing inflection points

It’s the short-term return that matters most

Let me discuss both briefly. The first premise is actually much more complex than it sounds. The reason is that not only will an investor need to time inflection point in the business cycle (i.e., financials) but also in the stock market (i.e., expectations and market mood). Both of these are related, but to time both inflection points accurately, an investor must estimate the market’s mood (which seems tough), which tends to change before the inflection is apparent in the financials. This is why sometimes it’s hard to fathom why a stock is going up after reporting poor earnings; expectations and the market’s mood matter dearly (especially over the short term).

While there are no reliable statistics, I believe it’s reasonable to assume that investors (on average) are not good at timing inflection points, and if they do get it right from time to time, it’s unlikely to be a sustainable winning strategy. A counter argument here would be that you can wait until the inflection is evident in the financials and still do well. While this makes sense, I believe it’s a strategy that not many can implement due to fears of being “late to the party.” Inflection situations also tend to unravel relatively fast, too. This applies to both individual stocks and the market as a whole, with JP Morgan estimating that if you miss the best days, your returns suffer significantly:

A common counterargument to this chart would be that you could do far better than being fully invested by avoiding the worst days. While this is mathematically correct, I don’t see why an investor can avoid the worst days if they cannot correctly forecast the best days (forecasting works both ways).

The second premise refers to most investors' (and the market’s) obsession with short-term returns. Most try to avoid dead money situations because they fear its impact on their next year’s return. This, again, is numerically correct, but it’s tough to apply and shouldn’t matter for a long-term investor. If one believes a company will be worth double in 5 years (for a 15% CAGR), the timing of this CAGR “does not really matter” so long as it is achieved in the specified time frame.

What I am trying to say here is that it’s numerically the same over a 5-year period for an investor to make their money at a 15% per year rhythm or by achieving a 100% return in the last year. The ideal scenario in the latter is obviously investing the money elsewhere for four years and then owning the company in the fifth year, but again, the roadblock here is that it assumes that we can time inflection points.

While I wrote before that the timing of the return “does not really matter,” this is far from true for individual and professional investors, although for different reasons. As you might well know, professional investors are sucked into a pretty nasty tug-of-war between long-term returns and growth in AUM (Assets Under Management). While some professional investors understand the strategy to outperform markets over the long term, most get caught up in the industry’s incentive structure and end up doing things that allow them to increase AUM but that might penalize their long-term returns. One such thing is an obsession with catalysts (“tell me why this is going up over the next 12 months”). Most professional investors simply can’t be left holding a stock that does nothing for a year or a couple of years. This is, ironically, what creates dead money situations and opportunities for individual investors (more on this later).

This is a limitation that individual investors don’t suffer (as they set their own incentives), but individual investors are not insulated from the perils of dead money situations. The main problem for individual investors is that it’s psychologically very challenging to hold something that goes nowhere for a prolonged period. One might start questioning their thesis, and it’s undoubtedly a conviction tester. Achieving long-term gains is not easy for this exact reason: a very long time of constant news inflows coupled with a flat or slightly declining stock price.

There are many examples of this dynamic in the market because pretty much all long-term winners have gone through such a period. The most famous example is probably Microsoft (MSFT), which was dead money for over a decade, between 2002 (the lows of the dot-com bubble) and 2013/2014. Imagine making close to 0% returns over a decade only to see your money more than 10-bag in the following 10 years:

An investor would have achieved a 14% total return CAGR holding Microsoft from 2002 to today, but I am inclined to believe not many investors would’ve been able to hold through a dead money decade.

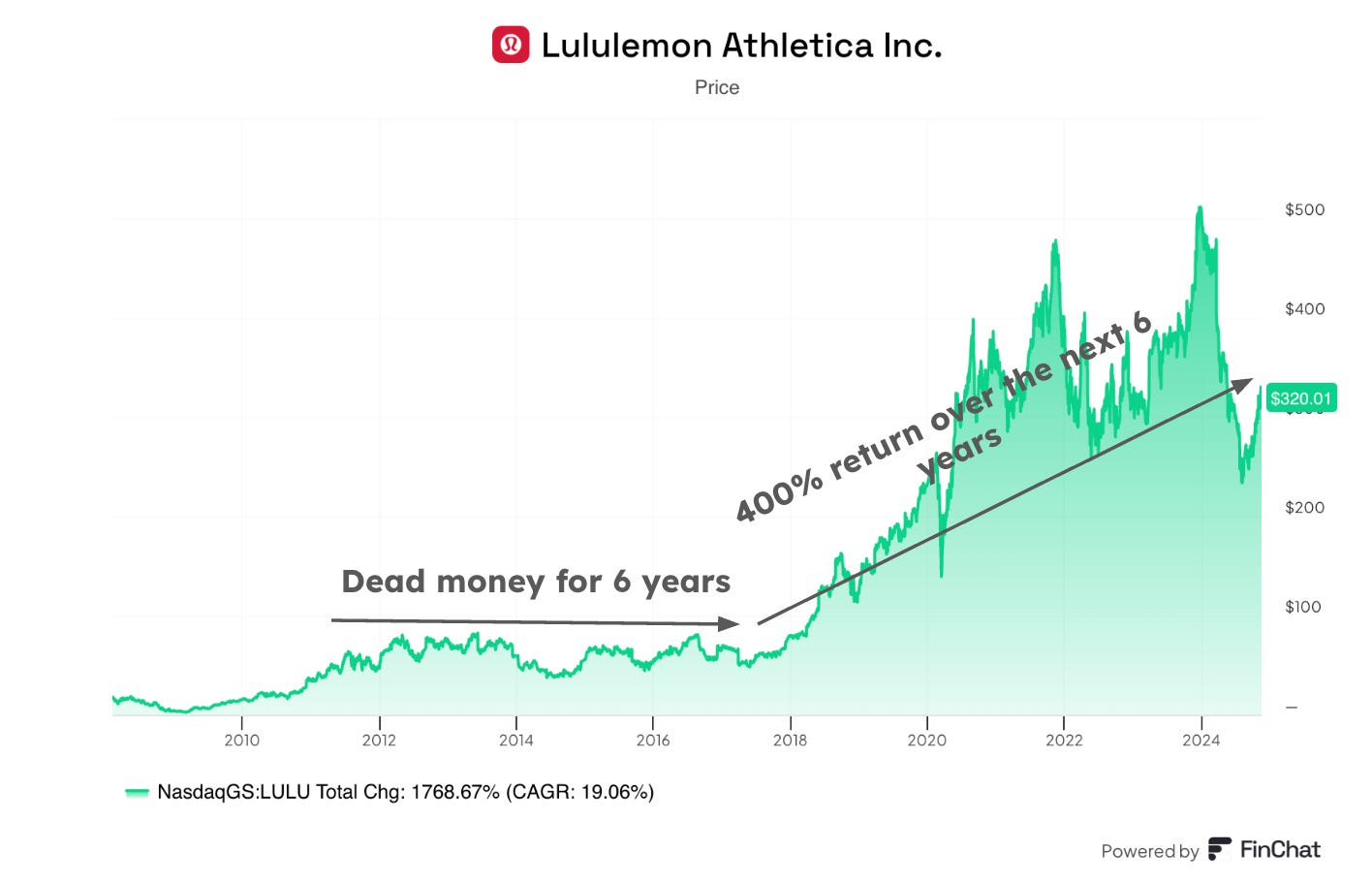

Microsoft is probably the best-known and most extreme example, but it’s not the only one. Take Lululemon (LULU). Lululemon was dead money from 2011 to 2017, only to deliver a 400% return over the next 6 years (2018 - 2024):

I could go on and on with more examples, but what I am trying to portray here is that pretty much all companies are subject to dead money periods, which is why holding positions long-term is very tough (nobody said compounding would be easy). Humans are inherently attracted to activity, but there are periods in the stock market where basically nothing happens for a given company.

What causes dead money periods?

I started this article by discussing two companies in my portfolio (Zoetis and Deere) that fall into the “dead money bucket.” Interestingly, both companies fall into this bucket for different reasons (albeit both are related). It’s my impression that two situations can give rise to dead money periods:

A company entering temporary headwinds at the start of the period

A stretched valuation at the start of the period

As valuations are intrinsically linked to expected business performance (maybe not precisely but directionally), both situations tend to be pretty related.

In both cases (mostly when the company is a proven long-term secular winner), the market will not penalize the stock too much but will let the cycle play out, or the financials catch up with the valuation. Deere and Zoetis are good examples of both. Deere is currently in an agricultural downcycle, but its stock has not moved much. One of the reasons might be that the company is improving its margin profile through the cycle, but if we look back, we can see that Deere’s stock behaved similarly in the last agricultural downcycle. It was flat for four years and started climbing up once the cycle inflected:

As for Zoetis, the company came out of the pandemic with a stretched valuation because the pandemic greatly accelerated its business. The market, which tends to be subject to recency bias, thought this growth would be sustainable. It wasn’t, but Zoetis has continued doing just fine after a short period of muted growth coming out of the pandemic while its valuation has contacted. EPS has grown at an 8% CAGR since 2021, whereas the P/E multiple has contracted at a 16% CAGR:

As you can see, both Zoetis and Deere might have been dead money for different reasons, but they are both two sides of the same coin: the relationship between fundamentals and valuation. It’s an investor’s job to understand whether the dead money situation is secular or temporary.

Dead money as a source of opportunity

Professional investors and some individual investors fear dead money because they are obsessed with next year’s performance. This, in my opinion, is great for those investors who are more long-term-oriented. Investors included in the latter group tend to be more grounded and acknowledge that they cannot time inflection points. The former group tends to believe they can indeed time the inflection point and maximize their returns.

Dead money can be a source of opportunity for long-term-oriented investors because there will be a time when many investors will eventually give up. This moment will probably coincide with professional investors unwilling to touch these stocks until they “start moving.” This might lead to depressed valuations and opportunities for those willing to hold such stocks even if they don’t move for a while.

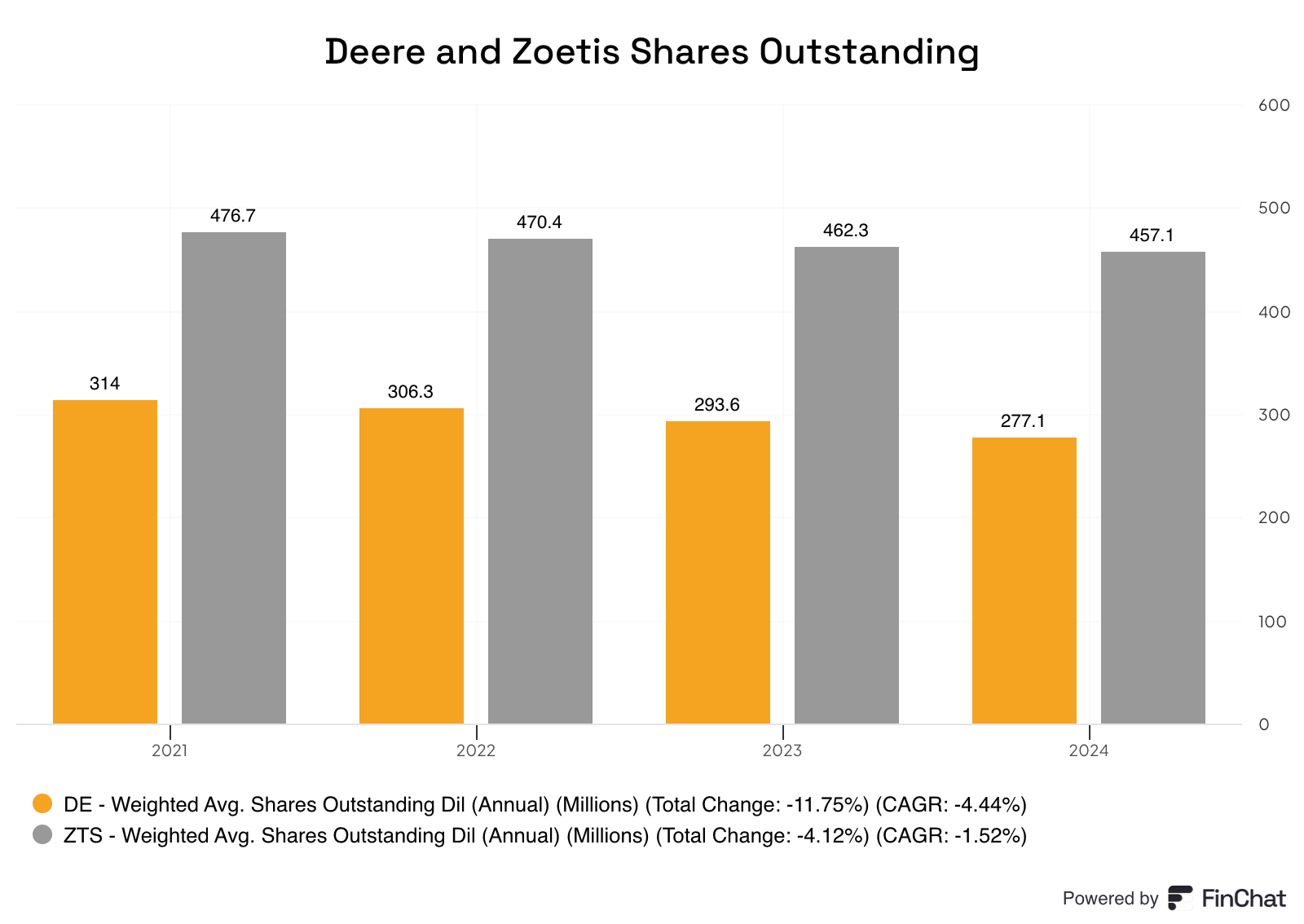

It also spells opportunity for companies that buy back stock. Assuming the company continues to generate Free Cash Flow during a challenging period, it can repurchase its shares at more favorable valuations, which will play an essential role in making the recovery quite violent (when it happens). Uncoincidentally, both Zoetis and Deere are good examples here, as they’ve retired shares over their respective dead money periods:

I once detested cyclical companies, even if they were secular over the long term. I have changed my mind, and now I believe these companies tend to offer the best opportunities due to a combination of good long-term prospects and reasonable valuations from time to time (when everyone is waiting for the inflection point). Of course, you need to get the cycle directionally right over the long term!

Dead money is not necessarily dead money if one optimizes their purchases

Another assumption behind the “dead money” situation is that an investor buys at the beginning of the period and does not make further additions. If an investor satisfies the following…

Has excess cash to deploy every month

Knows what the company is worth

…they can make what appears to be a dead money investment quite profitable. An example I’d like to share here is Adobe (ADBE). I purchased my first Adobe shares on the 24th of March 2022, when the stock was trading at around $460. I kept adding to my position, being more aggressive when it was cheap. Even though the stock is up around 20% from my first purchase, my position is actually up 50%. This strategy is one that Turtle Creek (a Canadian fund with a great track record) likes to discuss: holding period optimization. It’s true, though, that they also sell to optimize their holding periods. I rarely sell because, unlike Turtle Creek, I have to pay taxes every time I do so.

Dead money periods can be great for accumulating a position while one patiently waits for the inflection.

In the meantime, keep growing!