The Narrative vs. The Reality

Amazon's Q1 Earnings Digest

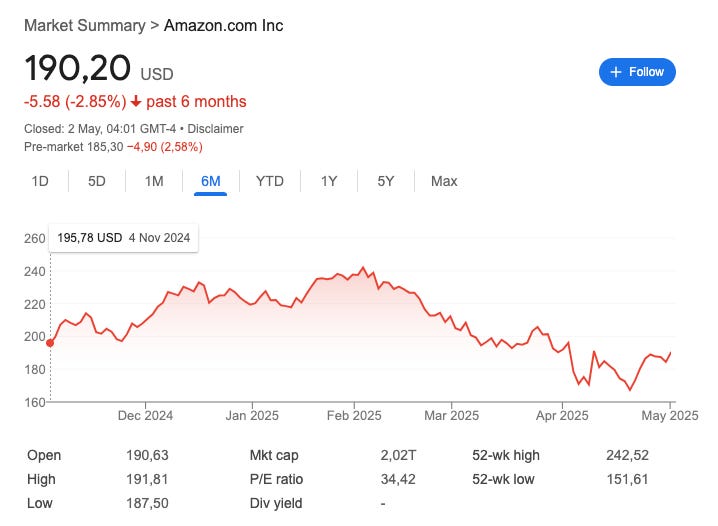

Many long-term investors claim that not many things change in a quarter and that businesses and the environment tend to change over extended periods. While I consider myself one of these long-term investors, there’s no denying that things have changed pretty fast for Amazon in just a couple of months, both for the company and the stock. Amazon’s stock was trading at $229 when it reported Q4 earnings in February, but the stock is set to open around 20% lower today, barely 3 months later. This is the first, and most evident, thing that has changed in just one quarter:

While many investors also claim that the market is acting irrationally when companies like Amazon drop 20%, it’s essential to realize that 20%+ drops don’t happen out of thin air; i.e., there’s almost always a reason for said drops. This doesn’t mean that the drop is rational; it simply means that it’s being driven by something, either a narrative or a temporary (or permanent) deterioration to the fundamentals. With Liberation Day taking place on April 2nd, Amazon’s drop in Q1 has been purely driven by two narratives. First, that tariffs will put a significant toll on the business. Secondly, that AI is a bubble and Capex investments will deliver questionable ROIC (Return on Invested Capital). Is Amazon’s drop warranted due to these narratives? That’s, among other things, what I will try to answer in this article.

Let’s start by looking at Amazon’s numbers. Here’s the summary table for the quarter:

The first highlight I like to comment on for Amazon is typically growth. Amazon delivered yet another quarter of double-digit growth (in constant currency) despite a TTM revenue base of $650 billion! Management also guided to potentially enjoying yet another quarter of double-digit growth in Q2. Many investors have gotten used to such growth rates at this scale because companies like Microsoft, Meta, Alphabet, and Amazon have spoiled them over the years. What would've happened if one had told an Amazon investor in 2015 (Amazon was growing 20% back then on a $100 billion revenue base) that the company would be growing at a double-digit clip with a $650 billion revenue base? He would’ve probably been described as completely irrational if not mindlessly stupid. Now, the fact that some companies have achieved this feat doesn’t mean we should take it as a base rate for all companies. These companies have, if anything, proven to be the exception to the norm.

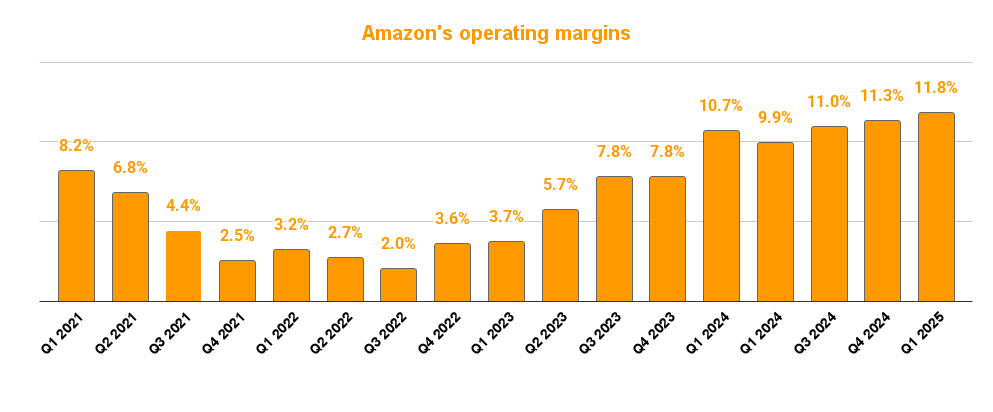

Arguably better for Amazon is the fact that it’s managing to grow at a double-digit clip while significantly expanding its margins. Q1 was yet another quarter of substantial operating leverage, with operating profits rising 20% year over year and operating margins landing at an all-time high of 11.8%:

Margins would’ve landed higher if Amazon had not recognized several one-time charges to its North America and International segments in Q1 related to tariffs. Absent these charges, operating profits would’ve been around $1 billion higher for a 12.5% operating margin. Management also noted that costs related to Kuiper are currently being expensed as incurred, but that a portion of these will be capitalized once the project gets commercialized (expected to happen later this year). This should, in theory, be a tailwind to margins, although we don’t really know the magnitude of these expenses.

Now, while all of the above is great, we shouldn’t ignore the development of AWS’ margins. Amazon reported its highest AWS margin quarter at 39.5%. While this is great, we should be aware that this level is unlikely to be normalized. Management did allude to several cost efficiency measures being implemented at AWS, but they also claimed that AWS is currently capacity-constrained and that the supply/demand imbalance should somewhat correct itself during the second half. This would potentially mean that margins go lower in the second half.

I honestly don’t know what AWS’ normalized margin will be in 5-10 years, but I think several things point to its attractiveness. The most important of these, in my view, is that the cloud market is an oligopoly made of rational competitors. I expect rationality to continue here for a very long time because the pie is large enough to accommodate the three main players (Amazon, Microsoft, and Alphabet). I’ll talk more about AWS later on.

Despite all these moving parts, Amazon’s management team believes there is still a significant margin expansion opportunity across its retail segment. While this is evidently great, we must not forget that around of 63% of Q1’s operating income came from AWS (should’ve been 59% if not for the one-time charges to retail), meaning that changes in AWS margins to the downside are expected to have a bigger impact on overall operating margins than improvements in retail margins. One thing I would highlight is that Amazon’s reliance on AWS profits has been decreasing since the height of the pandemic:

Going down further in the income statement, I recommend completely ignoring the net income and EPS figures. The reason is that Amazon recognized a one-time benefit of $3 billion from its investment in Anthropic. All in all, it was a great quarter from the income statement POV. The truth is that Liberation Day took place in Q2 when Q1 was already locked in, but I’ll refer more to tariffs later on because it’s not as bad as it seems.

Cash flows, Capex, and AI

Capex, cash flows, and AI are where most investors are focused. The main reason is that, due to AI, a lot of Big Tech is undergoing a massive capacity expansion plan. With the unknown ROI that these investments will generate going forward, many investors are concerned with the earnings quality of these companies (especially as they manage earnings by changing the useful lives of their assets). Will profits down the road justify the higher capital intensity of these businesses? Let’s first look at the numbers. Amazon underwent a significant capital expansion plan during the pandemic, primarily investing in its retail operations to gain share as the world moved online. This eventually created a myriad of inefficiencies, which have since been corrected (the company has beaten margin records in retail). Capex also started to decrease as the pandemic waned and Amazon’s cash flow ballooned thanks to higher margins combined with lower capital intensity. Investors were now happy because they saw light at the end of the tunnel and were experiencing Amazon’s potential to generate cash flows.

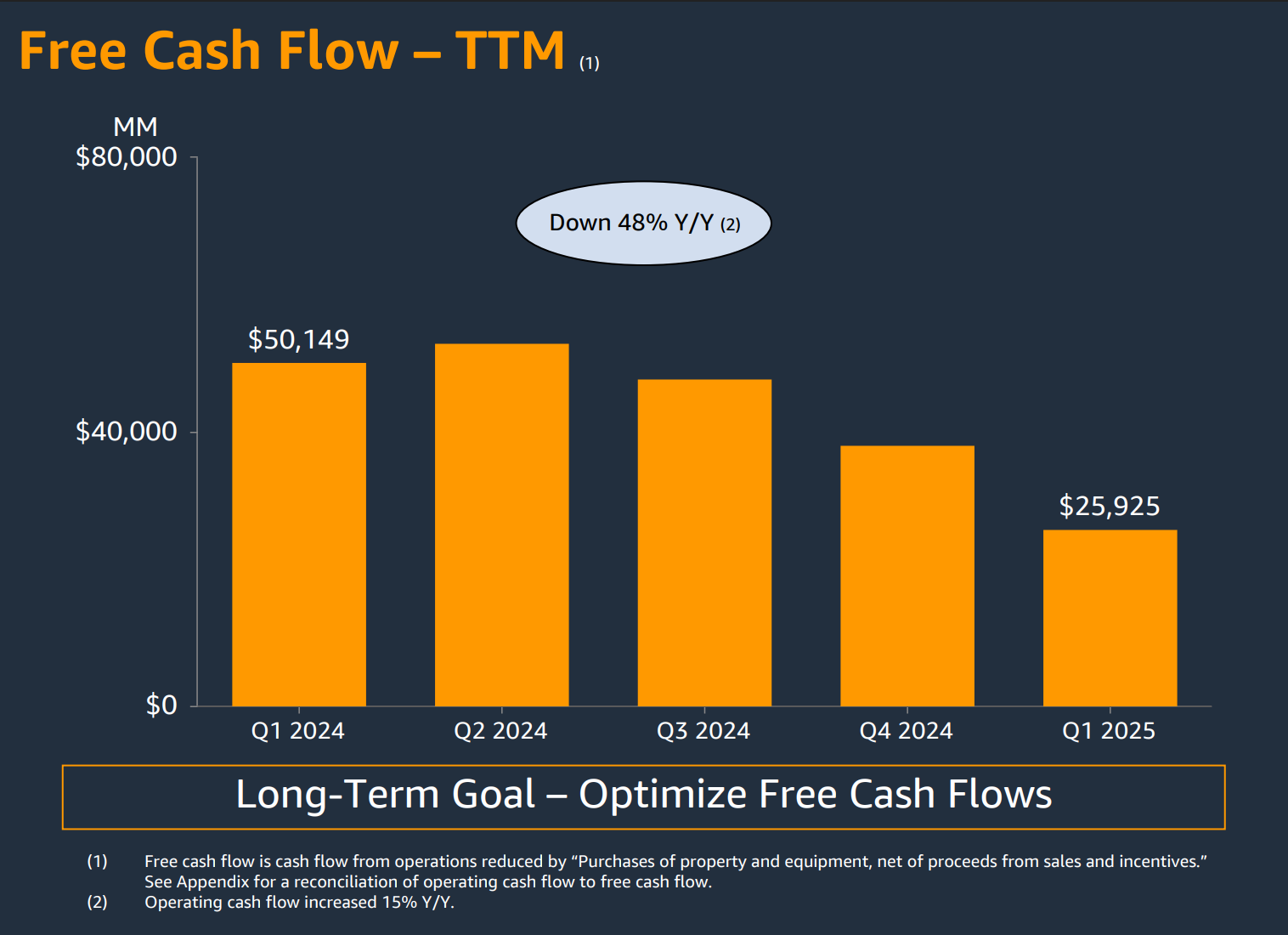

Now, in came AI. AI took the world by storm, and because many of these innovations are happening in the cloud, Amazon has begun yet another Capex cycle, this time more oriented to AWS. After peaking in Q2 2024, TTM Free Cash Flow has steadily decreased and is now at $25 billion. Free Cash flow was negative in Q1, but that’s also somewhat normal for Amazon due to seasonality:

There are reasons to be more skeptical about this capacity expansion plan than the one experienced during the pandemic. As time went by, it became evident that Amazon overshot its pandemic capacity expansion plan, but it seemed easier to believe that the excess capacity would be eventually used due to the ongoing trend in e-commerce. That said, I don’t think this was the consensus back then, as Amazon’s stock had dropped more than 50% from its highs (it was a pretty easy buy). Now there’s undeniably less visibility, and this lower visibility requires more trust in management. Management believes that AI is an opportunity like no other and that Amazon would be making a terrible mistake not investing aggressively to capture it. This optimism was evident during the call:

Our AI business has a multibillion-dollar annual revenue run rate, continues to grow triple-digit year over year, and is still in its very early days.

As fast as we actually put the capacity in, it’s being consumed.

I would say we’re not even at the second strike of the first batter of the first inning.

I think we could be doing more if we had more capacity, and I expect the capacity to ease in the coming months.

While the long-term is uncertain, short to medium-term developments seem to be proving them right: AWS is currently operating in a supply-constrained environment (which might explain what margins have done). This reflects that AI demand is growing faster than was expected and that capacity takes some time to come online. I do believe that AI is an opportunity unlike any other and I trust management’s judgement, but I am also sure that it will not be a straight line up and that there will be periods of lower demand (if this doesn’t happen, then great, but I believe it’s better to expect it will happen at some point).

AI is also driving a self-reinforcing flywheel for the cloud business. The trend of companies shifting workloads from on-premise to the cloud was unstoppable, but it is accelerating now that pretty much all AI innovation happens in the cloud. If a business is thinking of shifting to the cloud, it seems they will have to make a decision quickly if they don’t want to be left behind in an AI-driven world. It was interesting to see Andy Jassy finally change his “90% of workloads are still on-premise stat.” Amazon’s CEO claimed that 85% of this is still on-premise. Regardless of whether you believe or don’t believe this stat and think that there’s “only” 60% left, it does seem that this, together with the growth in AI, signals that the opportunity ahead for AWS is significant despite its $100 billion run rate.

Before this generation of AI, we thought AWS had the chance to ultimately be a multi-hundred-billion-dollar revenue run rate business. We now think it could be even larger.

AWS’ growth rate was impressive this quarter and remained resilient, but management even hinted at an acceleration being possible once capacity comes online. The backlog growth supports this: it grew 20% year over year and now stands at $189 billion. Faster growth should also help counter the impact of potentially diminishing margins as capacity comes online.

The topic du jour…Tariffs!

Everyone looked at Amazon like the black sheep when Liberation Day took place on April 2nd. It made sense on paper: Amazon runs retail operations and sources many of its products from China. A potential trade war between the US and China (which ended up happening) would’ve been theoretically devastating for Amazon. Reality seems to be somewhat different, though.

Management not only mentioned that tariffs are not yet having an impact but that they can make Amazon’s competitive position comparatively better and could be somewhat positive over the coming quarters. Let’s unpack this. One thing that many people seem to have ignored is that tariffs on China not only impact Amazon but all of its competitors. This means that if prices go up, they will go up across the board, and management believes Amazon is in a good place if this happens. For two main reasons…

Amazon has cheaper prices than most of its peers and has the widest product assortment

Amazon sources many products directly from China, whereas other companies might source from intermediaries who source from China. Amazon believes these businesses are comparatively worse off because the intermediary will raise prices significantly

All this said, the impact of tariffs has been muted thus far. Prices have not yet increased (management believes in some cases they will not go up much because the seller will assume the tariff) and both Amazon and its sellers have pulled forward some of their purchases. However, management said clearly that the intent is not to build up inventory. They also experienced some heightened buying in Q2, but nothing too extraordinary.

I must say I agree with management’s POV here. China tariffs are bad for everyone, but they are comparatively good for the retailers with the largest assortment at the lowest price. If we add Amazon’s scale to this, it seems evident that some sellers will be willing to assume the tariffs as long as they remain profitable. Tariffs are still TBD, but I am pretty surprised to see a muted impact thus far on the company that many thought would get completely obliterated. The second-order effect of tariffs would be a potential recession, which is evidently not great for Amazon. However, the higher mix of everyday essentials and the fact that this category continues to grow faster should help the company isolate to an extent from this scenario.

Some words on valuation

In my last Amazon earnings digest, the company was trading at $230, and I made a sensitivity exercise based on operating margin and an exit EBIT multiple. Assuming a 9% revenue CAGR over the next 5 years and 1% dilution, I got to the following expected IRRs