The consequences of vertigo

Stevanato's Q1 2026

Something “weird” happened in the month leading up to Stevanato’s earnings: Stevanato’s stock had risen significantly after pretty strong earnings from WST, ATR, LLY, and NVO (with all claiming strength across their injectables franchises). Even though the stock had (and still has) been punished to stupid levels due to the oral GLP-1 narrative, there’s no denying that the run-up before earnings likely elevated implied expectations (at least I know it did for me):

Seeing stocks rise so much into earnings in such a short period of time is not something I particularly like because I feel it messes up my expectations. It worked this way: I was pretty uncomfortable coming into earnings.

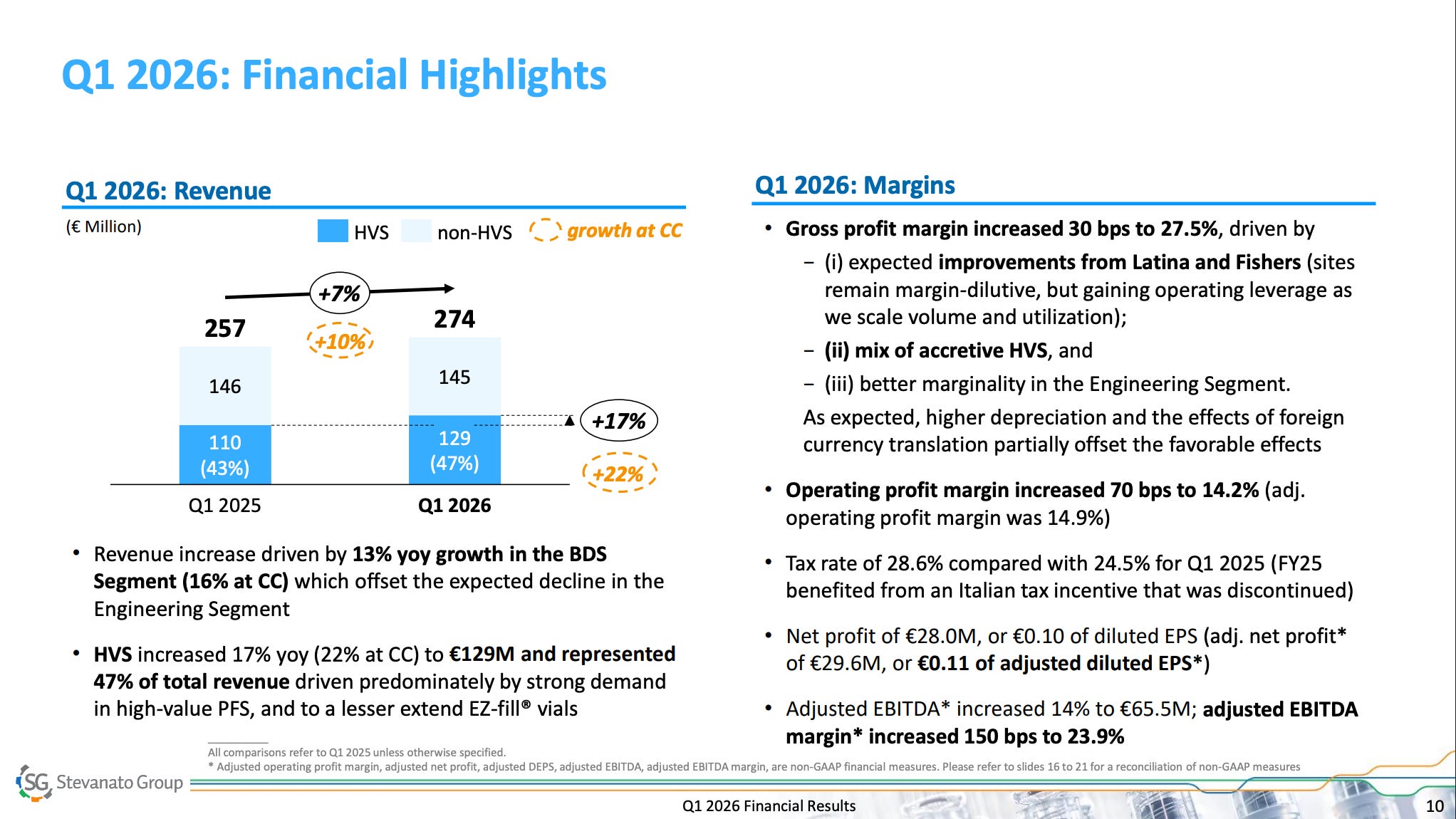

Stevanato reported pretty good earnings all things considered. The main highlight was that total revenue (+10% YoY in CC) and BDS revenue currency (+16% YoY in CC) both accelerated 300 bps sequentially (and this was on top of a pretty strong Q4 2025). I would’ve considered this spectacular if the stock had not run up into earnings (still do), but seeing management not raise guidance (with companies like WST and LLY doing so due to strength in injectables) left me a bit disappointed (maybe wrongly so). This shouldn’t have caught me by surprise considering that it’s Q1 and that Stevanato’s management is not precisely known for being overly optimistic!

Overall, the quarter played out as expected: very strong growth in BDS driven by HVS (+22% YoY at CC) and a very weak engineering segment (-31% YoY):

My hunch is that Stevanato could be growing faster should its capacity be aligned with current demand. First, Latina and Fishers continue to ramp up, with the bulk of capacity probably coming online late 2026/early 2027. Secondly and, interestingly, management shared that they’ve requalified an RTU vial line into an RTU cartridge line to align with demand. The line is expected to go live in at the end of Q2:

We are growing in vials. We are growing more rapidly in sterile cartridges where we have less capacity. That is why we decided to switch the line from vials to cartridges.

This (imho) implies two things:

More capacity is coming online late 2026 / early 2027 (Latina and Fishers)

The current capacity doesn’t seem to be aligned with current demand and Stevanato is working on this (but it’s probably impacting growth)

While point #1 would not necessarily result in higher revenue over the short term, I do think that #2 would result in faster immediate revenue growth. I mean what Stevanato is basically saying is that they can’t satisfy current demand (not future projections). In short: demand > supply. Good news to see Stevanato take proactive measures to address this.

I believe there were three main “lowlights” in the release. The first one was (as always and expected) engineering. Engineering revenue dropped 31%, although the bright spot was that margins which improved quite considerably. Seems like engineering can’t get much worse, but one never knows.

The second lowlight could be found in BDS margins. Despite management claiming that margins came in line with their expectations, BDS gross margins dropped a whopping 300 bps. Margins still improved at the consolidated level, but this is not what one would expect with 15%+ revenue growth. Anyhow, management explained the BDS margin drop as follows:

These positive trends were offset by several factors. As expected, the biggest factor was higher depreciation related to the ramp up in Fishers and Latina. As we bring more manufacturing capacity into commercial service. Second. The headwind from foreign currency. Third, in the first quarter of last year, the segment benefited from an accretive pilot project. Out of our Technology Excellence Center in Italy. Project was for an industry-leading customer for large batch, not for human use, fill and finish services. The success of 2025 project led us to relaunch this as a new service offering to meet market needs. Last, the impact of tariffs, some of which are expected to be recovered in future periods. As a result, gross profit margin decreased by 300 basis points to 28.3% for the first quarter of 2026.

So, recapping, the drop in BDS margins came from higher depreciation, FX, a one-time project included in Q1 2025, and tariffs. We don’t know (neither quantitatively nor qualitatively) what the impact of each component was. The one that seems most interesting is the pilot project (management discussed these a while ago in a press release). If we look at Q1 2025 we can see that Stevanato indeed experienced stronger-than-usual margin expansion a year ago: BDS gross margin expanded 420 bps on an 11% revenue growth. This projects (even though accretive to growth and margins) do seem to introduce some sort of lumpiness that the market did not expect. In fairness, management did not promote that strong margins in Q1 2025 were aided by said projects, which makes today’s admission come along as an “excuse.”

The third “lowlight” or actually not a lowlight but something that the market might have not liked was non-GLP1 growth. Even though several data points have “derisked” somewhat the oral thesis (LLY and NVO claiming strength in injectables and market expansion from orals, strong injectable earnings from WST, ATR, etc), it’s pretty evident that the market/analysts continue focused on STVN’s GLP-1 exposure. Management started disclosing its exposure in Q4 2025, claiming 19-20% exposure back then. Exposure this quarter was 21-22%, meaning that GLP-1 revenue “took” share of the overall company. They said the following about the non-GLP1 business:

Beyond. GLP-1s, we are seeing growing demand for cartridges for use with other biologics like monoclonal antibodies. Historically, cartridge volumes were primarily spread across a handful of large players. But today, market demand is extending into many other traditional large pharma and emerging biotech players, driven by biologics.

GLP-1s represented in Q1 between 21 and 22% of our revenue. It means that we grew compared with the same period last year. Slightly more than 20%. The non-GLP-1 biologics went up mid-single digits, 6%, to be more precise.

While 6% is somewhat in-line with what I estimated last quarter…

GLP-1 revenue grew 50% (!) in 2025 and despite the market being worried that the pill would result in a complete drop-off in terms of GLP-1 revenue, management confirmed that guidance includes mid-teens growth for GLP-1 revenue in 2026. This number is important for two reasons. First, it allows us to triangulate how much the non-GLP-1 business is expected to grow in 2026. If GLP-1 revenue is 20% of 2025 total company revenue, that means that it’ll add 340 basis points to Stevanato’s consolidated organic growth (20%*17%). Knowing that Stevanato guided for 9% organic growth (midpoint) for 2026, we can infer that the remaining 80% of the company is expected to grow 7% in 2026. This is despite the expected revenue decrease (MSD to HSD) of the engineering segment.

…it was probably not enough for a market that still believes that GLP-1s are not as sustainable as Stevanato believes. Management actually shared something regarding the durability of GLP-1s and the oral “risk”: the pipeline is active and orals are tracking their expectations:

While the vast majority of our revenue came from players with commercial assets, it also includes revenue from customers with assets in clinical phase. So we see a longer tailwind as the market continues to evolve.

Expect that the market will continue to evolve, but we still see 70% of the market opportunities in injectables and orals at 30%. This is consistent with what we hear out of many industry experts, peers as well as our customers. I think with the recent data behind us on some of the new orals that have been out, the. Commentary has lent itself much more to market expansion rather than cannibalization of the injectable market. You know those early signs. Certainly the very vast majority of those oral patients are new starts.

All in all and despite the TEC pilot project lumpiness, it was a good quarter for Stevanato. The stock is down 5% today as we speak, but it was considerably up over the last month (I still believe it remains significantly undervalued) and I don’t think this changes much of the thesis. I do believe communication could’ve been better (i.e., preparing the market for the gross margin lumpiness) and the call overall was uninspiring. One could clearly tell that Franco did not attend (due to temporary illness), but the good news is that Stevanato has three investor conferences coming up in which we’ll probably get more details.

Have a great day,

Leandro

I used to be a professional services engineer in the software sector. My assumption is that "engineering" services are mostly done in advance of other revenue activities. I.e. you hire Engineering to lay out a factory floor and then you buy the machines and run them for ten years.

So, Engineering revenue today is an important predictor of future ongoing revenue. If Engineering is down 31%, that's not good.