The Bottleneck is Dying. Long Live The Bottleneck.

ASML just killed the bottleneck thesis (sort of)

ASML and TSMC (two of the most relevant indicators of the health of the AI trade) reported earnings this week. I typically only write about ASML, but as I always end up reading TSMC’s call, I thought it made sense this quarter to bring a “joint” article to discuss the status of the AI trade. It’s worth noting that when I say the “status” I am evidently referring here to the supply side to a greater extent, although I will also talk about the demand side a bit (both are related, of course).

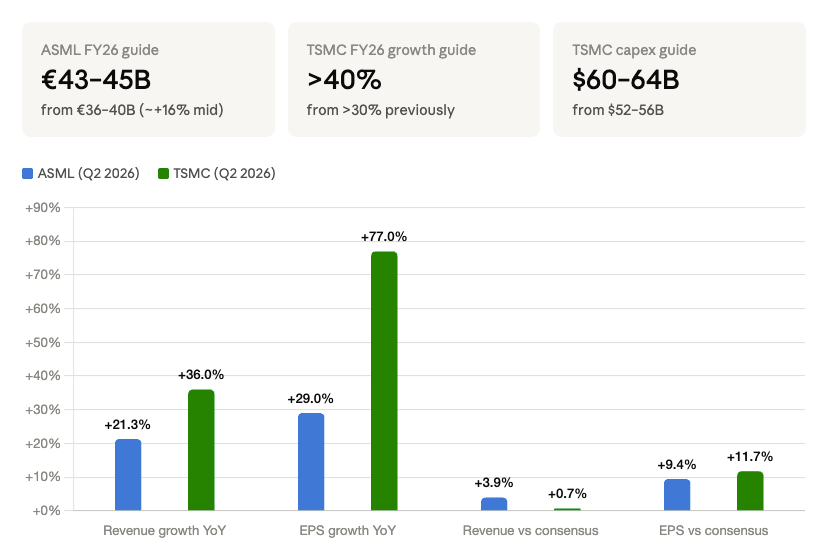

It’s no secret that both ASML and TSMC reported very strong earnings this week. Their stocks did not react as positively as many expected, which is something to consider in terms of what the market is telling investors. I believe a lot of people think that great earnings should (in 100% of the situations) result in strong stock price appreciation. This is actually not always the case, as earnings should always be considered in the context of expectations. There’s no denying that expectations for the AI complex in many cases have run up too fast and that stock prices do not always follow sell-side expectations!

Anyways, both companies significantly beat revenue and EPS expectations and considerably raised guidance.

The directional nature of their fundamentals shouldn’t surprise anyone because these companies are impacted by similar forces. TSMC sees very strong demand from its customers (companies that outsource their chip manufacturing), which translates into TSMC’s willingness to expand capacity. This capacity expansion eventually flows to the WFE (Wafer Fabrication Equipment) industry, where ASML is a strong player and has a monopoly in lithography.

I don’t think that going over all the numbers makes sense (those have been extensively shared by others by now), so I’ll focus on the qualitative aspects of the earnings with the goal of providing a differentiated POV (point of view).

Despite being moved by similar long-term forces (semiconductor demand), both companies’ short-term outperformances are driven by different things. Due to the long lead times of its equipment, ASML’s short-term beats have historically been correlated to the strength of its IBM (Installed Base Management) segment. As IBM is a high-margin segment, revenue beats driven by IBM have historically translated into EPS/profitability beats as well. IBM includes software/hardware upgrades and services conducted on the existing installed base. When capacity is tight, customers order new systems, but as these take time to make it into the installed base, customers perform upgrades on the existing installed base to improve their productivity (this is important for the capacity discussion that comes later).

It’s also worth noting that ASML’s raised guide (+16% at the midpoint) is very relevant. Management is guiding for sales of €44 billion this year, a number which should sound familiar considering that it’s the low-end of the company’s 2030 guide! This evidently has implications when thinking about the 2030 guide (discussed later on).

TSMC has more leeway to flex high demand over the short-term. For starters, the company is in many cases the beneficiary of ASML’s upgrades, which allows it to increase the number of wph (wafers per hour) relatively fast, also considering that fabs don’t typically run at 100% capacity. This gives TSMC the ability to somewhat flex capacity quickly.

Secondly (and most importantly), TSMC can flex its pricing power considerably faster due to the shorter lead times that wafers enjoy when compared to equipment lead times. A leading-edge wafer may take 3-4 months to be fully manufactured whereas ASML’s equipment typically takes 12-18 months (to which one should add when the order was made). ASML had also been historically known for not flexing its pricing power despite its monopolistic position. This is about to change.

The company had historically “priced to value,” meaning that, as systems got more productive, the company increased their ASP (Average Selling Price) to capture its fair share of value added. They’ll continue to do this in the foreseeable future BUT management also shared that they would make “exceptional” (my words) price increases to consider the current demand environment. Some rumours claim that TSMC is not happy about the price increases (neither about the price of high-NA EUV), but I’d say that it’s a bit unfair for TSMC to get upset about price hikes considering that…

TSMC is raising prices + expanding margins at an aggressive pace (are they the only ones that can get their fair share of value added? ASML seems to think “no”)

Even though TSMC was considered once the only viable EUV customer, this has since changed. The arrival of the memory players, Intel, and other potential players like Terafab and Rapidus has converted what was once a monopsony into a more fragmented customer base. This evidently means that customers must “fight” for ASML’s existing capacity

“Capacity” was probably the “star” word from TSMC’s and ASML’s earnings. We can look at this from several angles, but I believe all the angles make us arrive at the same conclusion: ASML and TSMC are likely not going to be bottlenecks for as long as many expected. Let’s start with ASML.

ASML has three main ways of increasing the industry’s capacity:

Manufacturing more systems (the most straightforward capacity lever which everyone understands)

Making new systems more productive

Upgrading the installed base (i.e., existing systems) to more productive configurations

The company is flexing the three levers in the current environment and capacity is going to come online probably at a faster pace than many expected. Let’s not forget that many investor’s supply-demand imbalance expectations came down to ASML’s extremely long lead times.

ASML announced in its Q2 earnings call aggressive capacity expansion plans over the short-term in both EUV and DUV. Management plans to raise its low-NA EUV output by 30% in 2027 and by an additional 30% in 2028 (albeit the latter is not a firm commitment but rather a forecast based on current conversations with customers). Immersion DUV is expected to experience a similar capacity increase (+30% in 2027 and +30% in 2028). An important point of this expected capacity expansion is its visibility. The order book for low-NA EUV systems (including the expected 30% increase) is full for 2027 and the company is already filling the 2028 order book.

The above translates into an expected low-NA EUV output of 110 systems in 2028, compared to the 65 expected in 2026. This is already a 70% 2-year increase in unit output, but the low-NA EUV mix will help ASML increase capacity further. ASML currently manufactures three configurations of low-NA EUV systems: “Ds”, “Es”, and “Fs”. While the mix had historically been made up of “Ds” and “Es”, it’s transitioning slowly but steadily into “Es” and “Fs” (with some analysts believing that 2028 sales will be made up of mostly “Fs.” This is important because these systems have considerably different productivity levels (in terms of wph):

Ds: 160 wph

Es: 220 wph (+40% compared to the D)

Fs: 260 wph (+18% compared to the E)

So, not only is ASML planning to increase the unit output, but the new units that are expected to come to the market will also be considerably more productive. Management sized the impact for 2027: while they expect unit output to grow 30%, they expect the unit mix to add an additional 1,500 basis points (15%) to said capacity expansion (so it’ll be closer to a 45% capacity increase). This means that we could expect wph output from new systems to roughly double in two years. Using 220 wph as the base case (ASML announced that no additional Ds would be shipped in 2027/2028), the increased unit capacity translates into a doubling of low-NA EUV wph exposures added to the industry in just two years. 65 systems in 2026 are equivalent to around 14,300 wph (based on continuous operations and assuming productivity of 220 wph), but 110 in 2028 would be equivalent to somewhere around 26,400 (assuming 240 wph).

If we take a look at the current capacity of the industry in terms of wph we can also see how material this is going to be. ASML doesn’t publish exact numbers on its installed base but we know how many EUV systems they sell over time. This, together with the fact that all systems remain in operations, means that we can approximate the low-NA EUV installed base.

Considering that ASML had shipped 190 low-NA EUV systems by Q1 2023 and adding the shipments from that date onward gets us to a cumulative installed base of roughly 290-300. These are heavily tilted toward B and C configurations which are significantly less productive than the newer systems. If we assume that the blended wph output of these systems is 180, this means that the current installed base supports around 52,000 wph. Assuming that ASML adds a cumulative 260 low-NA EUV systems in 2026 (+65), 2027 (+85), and 2028 (+110) at a blended wph of 240, we get to net wph adds of 62,000 wph. This ultimately means that wph capacity increases 120% over the next 3 years (per the estimates above).

Now, it’s important to understand that wph is not necessarily directly correlated to wafer starts. For starters, one could think that some of these systems are likely going to fall in the hands of less yield-efficient companies than TSMC. TSMC doesn’t even earn yields of 100%, so the “less experienced” players will not even get close to that number. This means that the above is a theoretical maximum. The second thing to consider is that pretty much all of the leading-edge wafers are multi-patterned and wph is a metric that explains exposures. This means that a percentage of this increased wph is absorbed by layer intensity rather than by new wafers, but it’s still considered “capacity increase” as those higher exposures should’ve been absorbed either way.

Are bottlenecks still trendy?

ASML’s and TSMC’s commentary around the most famous word in current financial markets (bottlenecks) was also interesting. Analysts asked the company whether the 85 and 110 numbers were based on their ability to supply or rather on end demand (likely expecting it to be the former!). Management unexpectedly said that the output is based on demand signals by customers and that supply could be stretched further (or at least stretching it further could be considered) if customers required it. Higher demand is not out of the question, according to ASML’s CEO Christophe Fouquet it’s actually highly possible for 2028:

I don’t think we have reached yet a stable state on what the demand will be for 2027, certainly not for 2028.

This ultimately means that ASML is expanding capacity to meet demand and therefore that it will not remain a bottleneck for long. This isn’t probably what many expected!

TSMC somewhat confirmed ASML’s words in a broader sense, claiming that they don’t expect bottlenecks across the supply chain to meet their capacity expansion goals. Capacity expansion goals which by the way are pretty aggressive…

Last time we said our Capex in the next 3 years will be significantly higher than the Capex in the past three years. The Capex in the next three years will be even more significantly higher than in the last 3 years.

TSMC is about to spend considerable amounts of capital in capacity expansion which management admitted (as obvious as it is) that it’s coming from their customers telling them how much they’ll need. I don’t believe I am saying this, but TSMC is getting “bulled up” on AI (sign of a top?):

Remember that I believe every customer tells me the truth, everyone. You put all the truths together, it’s not the truth. We have to make some of the judgement. We are checking all that to make sure that TSMC’s chip will not be put in inventory.

Next few years are going to be very good business for TSMC.

How I interpret all of the above is that the bottleneck remains memory but that many bottlenecks are getting solved sooner than many expected. Jensen Huang said a couple of months ago (on the Dwakersh Podcast) that semis would not be a long-term problem (“If I can convince TSMC, ASML will be convinced.”) but rather that the bottleneck would be power. I believe he is slowly being proven right:

We want to reindustrialize the United States. We want to bring back chip manufacturing, computer manufacturing, and packaging. We want to build new things like EVs and robots. We want to build AI factories. You can’t build any of these things without energy, and those things take a long time. More chip capacity, that’s a 2-3 year problem. More CoWoS capacity, 2-3 year problem.

I am not going to discuss the memory situation here (I’ve written other articles on the topic), but TSMC did confirm that memory pricing is destroying non-AI demand. This means that memory pricing is already impacting demand, and with increased capacity coming…

I believe memory needs will be significantly higher in the future (not only driven by digital AI but also by physical AI) but that capacity can come online faster than many expect (and I think ASML is a proof point of this). To this we must add the potential impact of any “memory enhancement” that comes the industry’s way. An event like this should not be ruled out of the question considering that memory is now the main bottleneck in AI. What this ultimately means is that the brightest minds are focused on solving the “memory problem.”

Now, the fact that TSMC and ASML are not going to be bottlenecks beyond 2028 (at least not according to their current expectations) doesn’t mean that AI will not remain in a supply-constrained environment. I potentially see two things that might invalidate the demand-supply balance:

Demand might be much more significant than customers expected in the first place. Not out of the question considering that it has happened a couple of times before

There are other bottlenecks different from TSMC and ASML (like the aforementioned memory)

The second point is likely but bottlenecks might get resolved over time. They most surely will, but if the main bottleneck according to Jensen Huang (power) doesn’t get solved, solving things downstream won’t do much to help AI growth. Interestingly, TSMC alluded to higher competition in back-end wafer manufacturing being positive because it eliminates the bottleneck for their front-end operations.

What does look likely is that the commentary claiming that the entire industry will remain significantly constrained “beyond 2030” must be revisited. It might happen, but some of the historically considered bottlenecks are bringing significant capacity online before 2030 and likely faster than many expected (humans always find a way to bypass bottlenecks).

ASML’s expected capacity expansion not only has implications for the industry but also for the company’s 2030 guide. Let’s take a closer look at this.

ASML can demolish the 2030 guide…two years in advance

Above I discussed that ASML’s management guided for €44 billion in sales this year, which is the equivalent to the low-end of its 2030 guide. The €44 billion doesn’t “include”…

The aggressive capacity expansion the company is about to undertake

The exceptional price increases the company is about to make

The increased IBM sales that come with the capacity expansion

This should have investors wondering: is the 2030 guide still valid? The quick answer that was somewhat confirmed by management during the call is that it’s not (management claimed they would revisit the 2030 guide in the next capital markets day in 2027). We can crunch some numbers to understand what ASML might achieve in 2028 and understand whether the 2030 is longer valid or whether it’s not. To do this we need several things:

An estimate on how many systems are going to be sold (primarily EUV and DUV). We got this in the Q2 earnings call

Average ASPs: we can somewhat estimate this although it’s tough to be precise because we don’t know what the exceptional price increases will be (I am not going to consider these)

IBM revenue

Metrology and Inspection system sales

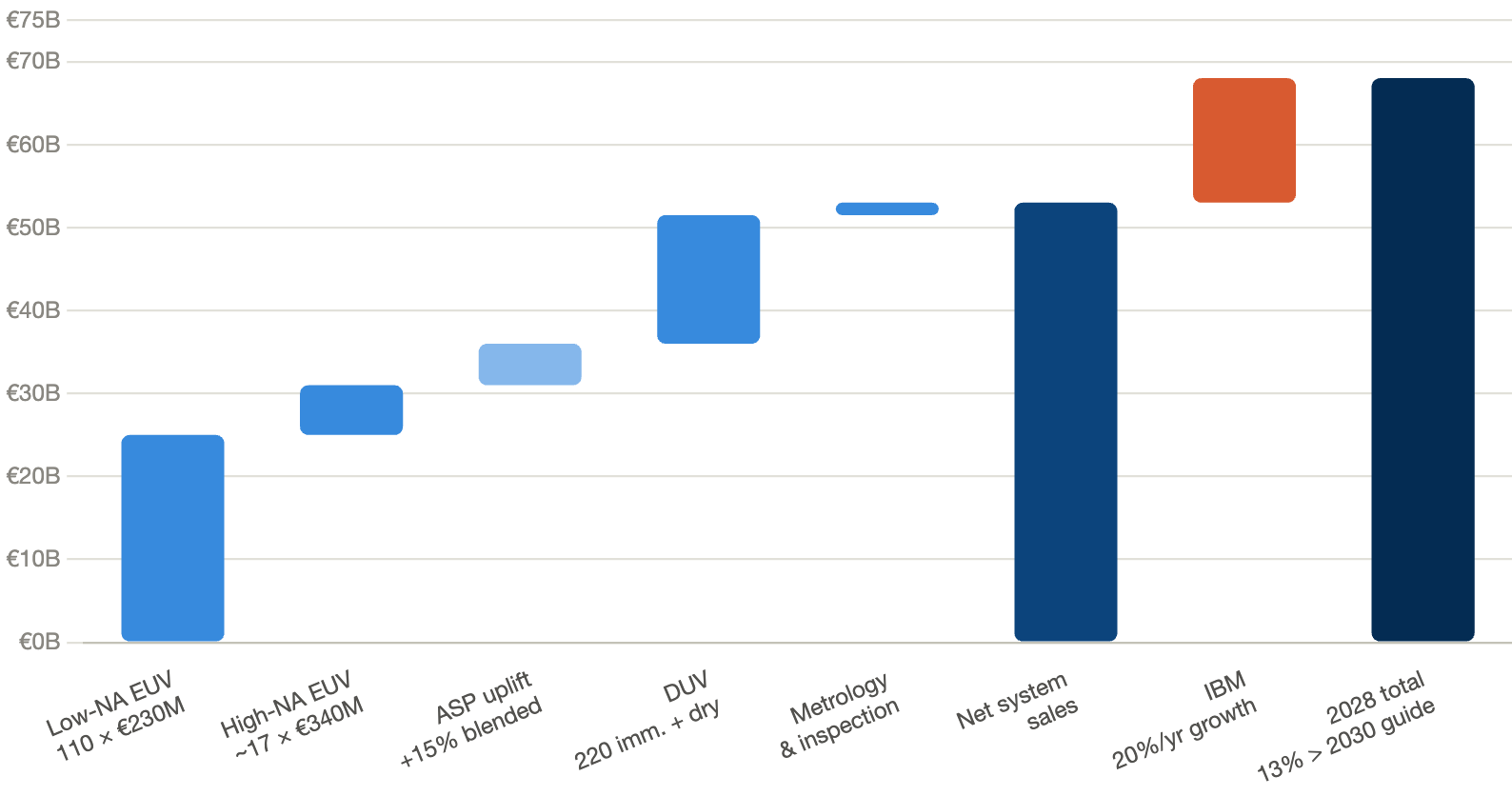

Note that this is just an estimate and that I’ll hold ASPs constant from 2025 levels (which is not a realistic expectation but will behave as a source of conservativeness). Based on 2025 numbers we have an implied ASP of roughly €230 million for low-NA EUV, €70-€75 million for immersion DUV, and €15 million for dry DUV.

Let’s start with low-NA EUV. Assuming ASML is able to ship 110 systems in 2028 at a €230 million ASP (will likely be higher), this results in around €25 billion in low-NA system sales.

In terms of high-NA EUV, management did not raise the capacity expectations so we could more or less calculate this. From management’s commentary we could imply around 15-20 high-NA EUV shipments by 2028. At an average ASP of €340 million we get somewhere around €5-7 billion in high-NA EUV revenue. This means that total EUV revenue in 2028 will be around €30-32 billion. And recall that in the case of low-NA EUV it doesn’t consider a significantly higher ASP that will most likely become a reality. If one would like to conservatively add a 15% blended ASP increase through the period, that would result in €35-€37 billion in EUV revenue in 2028.

DUV immersion capacity is also expected to grow 30% in 2027 and an additional 30% in 2028. This means that the unit output should be around 220 units in 2028. At a €70 million average ASP, this results in €16 billion in immersion DUV revenue. Dry DUV is also seeing an uptick in demand, but for conservativeness we’ll hold it constant at €2.5 billion. This means that total DUV results in €15-16 billion of revenue in 2028. Metrology and Inspection is also seeing an uptick in demand due to ASML’s holistic lithography strategy, but we’ll keep it at €1.5 billion in 2028.

All of the above means that net system sales land (with a 15% 2-year ASP increase and little growth in dry DUV and metrology & inspection) somewhere around €51-€55 billion in 2028.

Now let’s add IBM revenue. IBM sales should ramp fast for three reasons:

The installed base is going to grow significantly

It’s the first thing that customer can flex to expand capacity

EUV sales have attached a higher IBM attach rate than DUV

IBM sales are going to be around €11 billion in 2026 (considering management’s comments around 30%+ growth). If we assume IBM revenue grows 20% in both 2027 and 2028 (reasonable considering all of the above), this gets us to around €15 billion in IBM revenue in 2028. This is realistic considering that…

Management guided for €13 billion in IBM revenue on a €47 billion net system sales base for 2030. This results in a 28% attach rate, which is exactly the same as €15 billion in IBM revenue over €53 billion in net system sales.

Management has historically been conservative with IBM sales

If we add this to net system sales (€53 billion midpoint) we see that ASML could land around €68 billion in total revenue in 2028. Not only is this 13% ahead of its 2030 guide, but it’s also achieved two years earlier.

The remaining unknown is margins. Gross margins are likely going to go up in 2027 and 2028 for several reasons:

IBM revenue is growing fast and it is high margin revenue

The system mix is improving and ASML is going to flex pricing more aggressively than they expected (should drop to the bottom line)

The planned capacity expansion is based on the existing footprint (i.e., there will be considerable operating leverage)

Gross margins above 60% should not be out of the question considering this was the high end expectation for 2030 with a considerably lower level of system and IBM revenue, but I’ll anchor on this number. 60% gross margins result in gross profit of around €41 billion. With €6 billion in R&D expenses and €1.7 billion in SG&A (from management’s 2030 guide), this gets us to operating income of €33.3 billion. This means that ASML is currently trading at a 2028 EBIT multiple of 18x. If one believes that this business is worth at least 25x EBIT (not unreasonable), the potential IRR is around 17-18% (without considering share buybacks and/or dividends which should at least add 1-2% to these numbers). Honestly pretty good considering the run the company has already enjoyed.

At a 20x EBIT multiple in 2028, the IRR compresses considerably to 6% (in such a short period the multiple drives much of the IRR), but let’s not forget that I assumed little flex in terms of ASP. Now, all the forecasts above are definitely not free of risks. ASML’s 2028 orders are still not firm and demand could falter. Just as I am writing this, the new Chinese model Kimi K3 promises to bring another “Deepseek” moment to the industry as it supposedly performs better than Opus 4.8 and GPT-5.5 but at a fraction of the cost. Jevons Paradox invalidated the “Deepseek moment,” but this is just a reminder that demand and the thesis can suffer hiccups along the way.

To this we must add that the 30% capacity increase expected for 2028 is an aspiration, not a firm number (albeit ASML believes it’s actually on the low end). The good news is that it’s based on the existing footprint, meaning that ASML will most likely not have significantly unused capacity if demand ends up faltering a bit. With my fundamental expectations on ASML increasing considerably and the stock price correcting somewhat, I am starting to get interested again in a potential add. One thing is clear: I’ll maintain the position that’s left after my several trims.

Have a great day,

Leandro