Texas Instruments’ Q2 2024: The Turning Point (?) And A Special Event

Hi reader,

Texas Instruments reported earnings two weeks ago and the market was pretty much indifferent to these. However, the stock has dropped almost 10% over the past few weeks, possibly fueled by a broad-based market drop and, more specifically, by the selloff across semiconductor stocks. Funnily enough, Texas Instruments’ stock has proved quite resilient against the Nasdaq and the SOXX (a semiconductor ETF) over the last month:

Texas Instruments is now outperforming both ETFs year to date, which seemed impossible some months ago. There's not much we can read into here, so let’s look at the company’s earnings. Earnings were fine, and they came with a rather unusual announcement.

Another highlight was that Haviv Ilan, the company’s CEO, joined the earnings call. Seeing the CEO present in the earnings call is normal for many companies, but it’s not for Texas Instruments. Historically, only Dave Pahl (IR Head) and Rafael Lizardi (Chief Financial Officer) used to join these. From now on, Haviv Ilan will join too.

I’ll share almost the entire article for free, except the valuation section which will disclose what I feel is an attractive buying point for Texas Instruments. That section will be reserved for paid subscribers.

The summary table and some comments

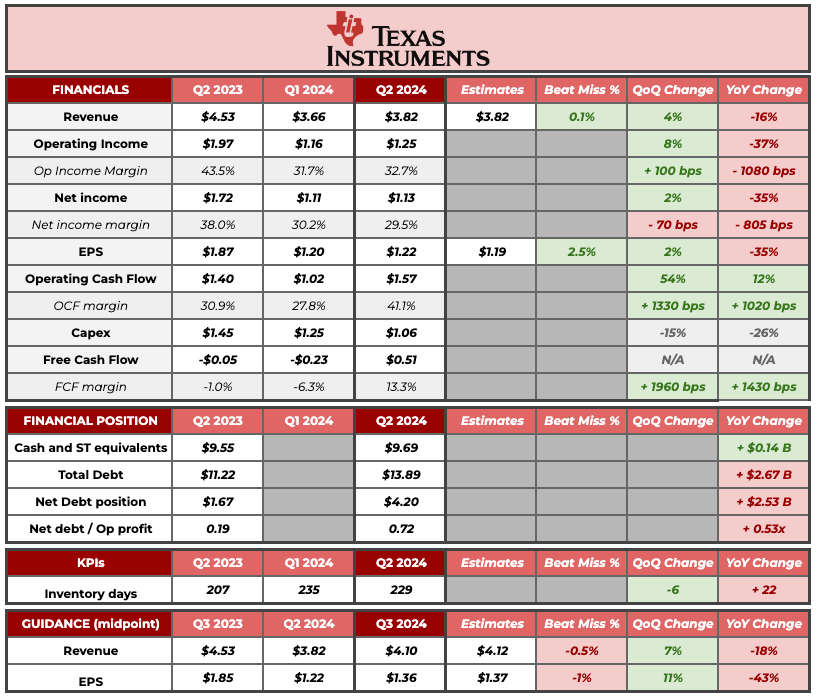

Here’s the Texas Instruments summary table with the most relevant financials and KPIs. Note that I also include the prior quarter to account for the company’s cyclicality:

Some comments…

The cycle seems to be turning around slowly but steadily, although we must account for cyclicality. Q2 tends to be a stronger quarter than Q1, and Q3 tends to be stronger than Q2. This means that the sequential improvements might be caused to a greater or lesser extent by normal seasonality rather than a cycle recovery.

The state of the end markets makes me believe that Texas Instruments might be suffering a maybe less pronounced downcycle but a more prolonged one. The reason has been alluded to by management several times: the asynchronous nature of this cycle. For example, all end markets grew sequentially except automotive and industrial, the two markets that have been strong in the past while the others were doing poorly. This divergence has helped mitigate the cycle somewhat, but it’s also making it more challenging to come out of the woods.

I’ve mentioned several times that Texas Instruments’ operates a fixed-cost model in which operating leverage and deleverage are the norm. This is evident if we look at the operating leverage the company experienced with meager top-line sequential growth. Seeing operating profit up 8% on a 4% revenue increase is a good indication of what will happen when revenue fully recovers. This is also why Texas Instruments tends to trade at optically high multiples during downturns.

Besides the inherent operating leverage in the model, gross margin also benefited from a higher percentage of internal manufacturing done in 300 mm wafers. I discussed several times throughout my article series this margin expansion opportunity, which could potentially act as an accelerant of the operating leverage once we come out of the cycle.

The growth in net income was lower than the growth in operating income because the interest expense grew sequentially and grew 48% year over year. There’s no denying that Texas Instruments’ financial position has worsened over the past year, but note that the company’s leverage is still under 1x despite the downcycle. Maybe the company was under-leveraged coming into the downcycle, but this has undoubtedly served it well in being able to invest countercyclically. Despite its massive investments, the company could pay its entire debt with cash on hand and with less than one year of operating profit.

Texas Instruments is a company that can take pretty high leverage due to its unit economics. Despite the violent operating deleverage and inventory buildup, it managed to post an operating margin of almost 33% in Q2. Very few companies can post these numbers when facing so many headwinds.

The company experienced a significant improvement in Operating Cash Flow. Operating Cash Flow grew 54% sequentially and 12% year over year. The main reason behind the improvement came from lower inventory, or better said, from inventory growing at a slower clip. Inventory days declined sequentially and its year-over-year growth moderated quite significantly. It’s outstanding to see Operating Cash Flow at a 40%+ margin despite inventory days running so high and the company being on a downcycle.

As you might know, management continues to invest significantly into the business, so Capex remains high (although it decreased sequentially). The lower sequential Capex, the improved operating cash flow and the inflows related to the Chips Act (around $312 million this quarter), allowed the company to post a Free Cash Flow inflow of $500 million. Management mentioned they still maintain the same Capex guidance despite this sequential drop but also mentioned that they expect to receive an additional $200 million in Q3 and a total of $1 billion in 2024 related to the Chips Act. These pending inflows are one of the reasons why Free Cash Flows and the company’s financial position have been misleading for a while.

As you can see in the table above, the company guided for sequential growth of 7% at the midpoint. We need to contextualize it, though. The first thing we must consider is that the guidance range is wide, meaning there’s quite a bit of uncertainty baked into these numbers. We should also remember that management tends to be somewhat conservative (i.e., they tend to underpromise and overdeliver). The second thing we should take into account is seasonality. As discussed above, Q3 tends to be stronger than Q2, so the improvement might be just a case of normal seasonality.

Qualitative highlights and lowlights

The most important highlight of the release was that the company will host a special off-cycle Capital Management Call on August 20th to share a framework for different revenue and FCF scenarios. It’s unusual to see Texas Instruments do this, but it’s most likely motivated by the recent activist. Anyway, more information is always good, not bad, so it’ll be interesting to see what management thinks about the future.

The other highlights were related primarily to geopolitics. First, analysts asked again how the company is doing in China, and it’s doing fine: “It was a good quarter for our China business. Our China headquarters business grew sequentially at about 20% versus the first quarter. The market is more competitive in China, but we can compete and we can win business in very attractive margins.”

The other side of the coin from the geopolitical situation is that customers increasingly value the company’s strategy: “Every time there is some news out there, you know, we are seeing more interest. Our discussions with our customers are providing us more opportunities to win positions in future platforms.”

The rest of the article is reserved for paid subscribers. Thanks for reading!