Still (!) no signs of AI disruption (+valuation update)

Topicus' Q1 Earnings

Topicus reported overall strong Q1 earnings, although there were also some “lowlights”. The market continues worried about the impact of AI on the business, but I would go as far as saying that some of Topicus’ lowlights portray that the narrative might have gone too far (I’ll explain why later).

Without further ado, let’s jump right into the numbers.

The numbers

Topicus’ revenue accelerated to 23% YoY in Q1, and interestingly this acceleration came with significant EBITA margin expansion (expenses grew 20% YoY):

This is what I wrote in last quarter’s article:

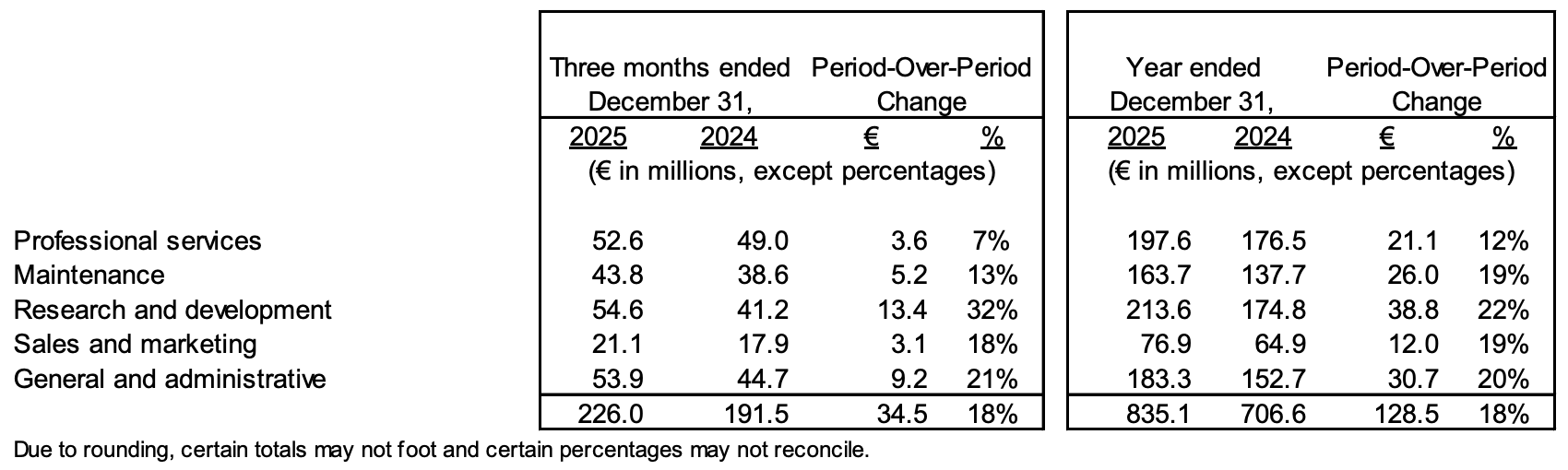

Staff expenses showed some interesting dynamics. Topicus’ revenue grew ahead of its staff expenses, but within these staff expenses, R&D staff expenses grew considerably faster than the rest:

Source: Topicus’ MD&A

One data point does not make a trend, but it’s nonetheless interesting that staff as a % of revenue has decreased throughout the entire year (it was even lower at 52% this Q) despite the year being a strong one in terms of capital deployment.

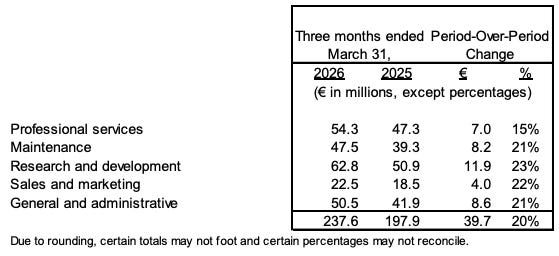

Something similar could be said this quarter. Staff expenses grew again slower than revenue, but R&D staff expenses grew at a similar pace than revenue:

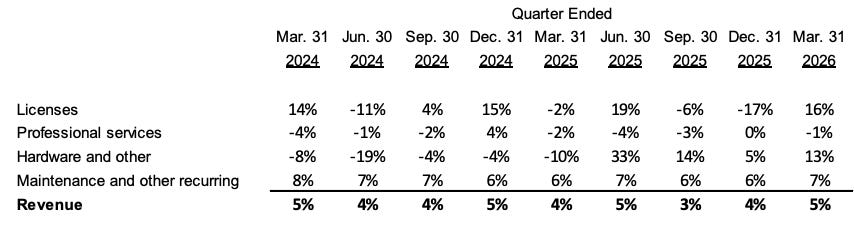

Just like one data point does not make a trend, two data points don’t make a trend either. Nevertheless, it’s interesting to see Topicus become more efficient in terms of labor without cutting on R&D staff (maybe an AI-narrative violation, who knows). Organic growth also continued to discredit the AI narrative. Both consolidated and maintenance and recurring organic growth accelerated in Q1:

The same way that I don’t believe that this acceleration entirely discredits the AI narrative, I must say that not giving fuel to the bears seems like a good-enough outcome at current valuations. One could claim that the AI impact will be felt in the future, but the reality that bears can’t ignore is that Topicus has grown maintenance and recurring revenue at >6% rates for over two years now. The AI narrative is one that will take some time to dissipate but at least investors can find “comfort” knowing that bears will have to continue to look ahead.

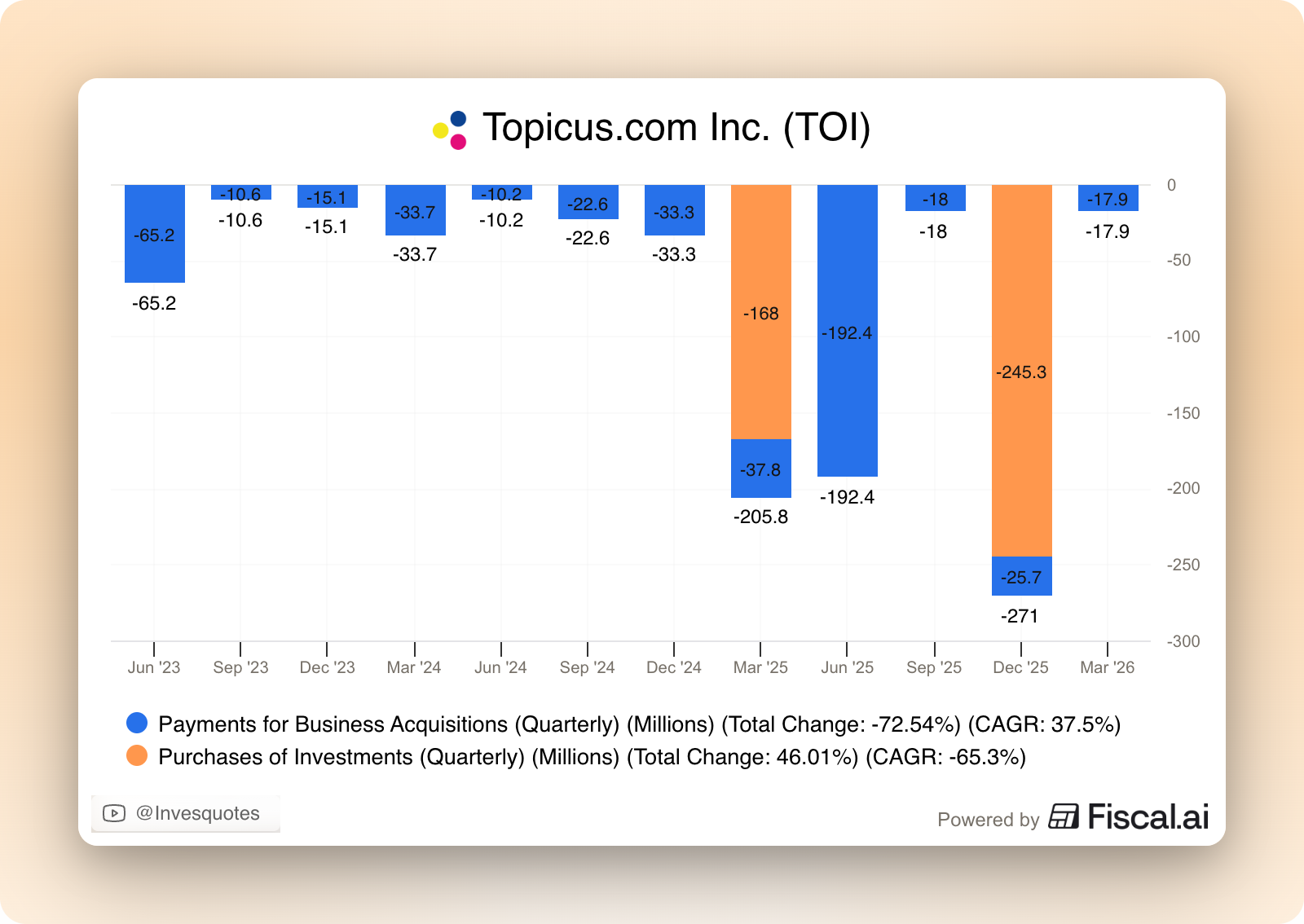

Another thing that makes me want to think that the AI narrative has probably been a tad exaggerated is capital deployment. Topicus’ capital deployment was relatively weak in Q1 (and so far in Q2):

While the evident reaction would be one of worry (as Topicus is a serial acquirer), I don’t think that the above is coherent with the fact that VMS businesses are getting disrupted. First things first, capital deployment at Topicus has historically been lumpy and cyclical (as it should be), so one shouldn’t read too much into the trend in any given quarter. I mean, this was precisely the “bear” POV in 2024, but then Topicus delivered an absolute stunner of a 2025 in terms of capital deployment.

Secondly, I don’t think that holding the view that AI is disrupting VMS businesses is coherent with the thought that this capital deployment level is structural. Should AI be disrupting VMS businesses, we would most likely see more appealing valuations in private markets (they’ve had time to adjust by now) and stronger capital deployment from Topicus.

What seems evident is that there’s a disconnect between public and private market valuations, so who is right? We’ll only know the answer in hindsight and we might just need time for the narrative to shift, but there’s no denying that something doesn’t add up (in the meantime both Topicus and CSU through PEMS are trying to take advantage of the “arbitrage”). Topicus’ has suffered the multiple compression caused by the AI-narrative, but its M&A activities have not risen to structurally elevated level (which means the targets have not received the cut). Weird, but things may change throughout the year and we’ll most likely get more details next week during CSU’s call.

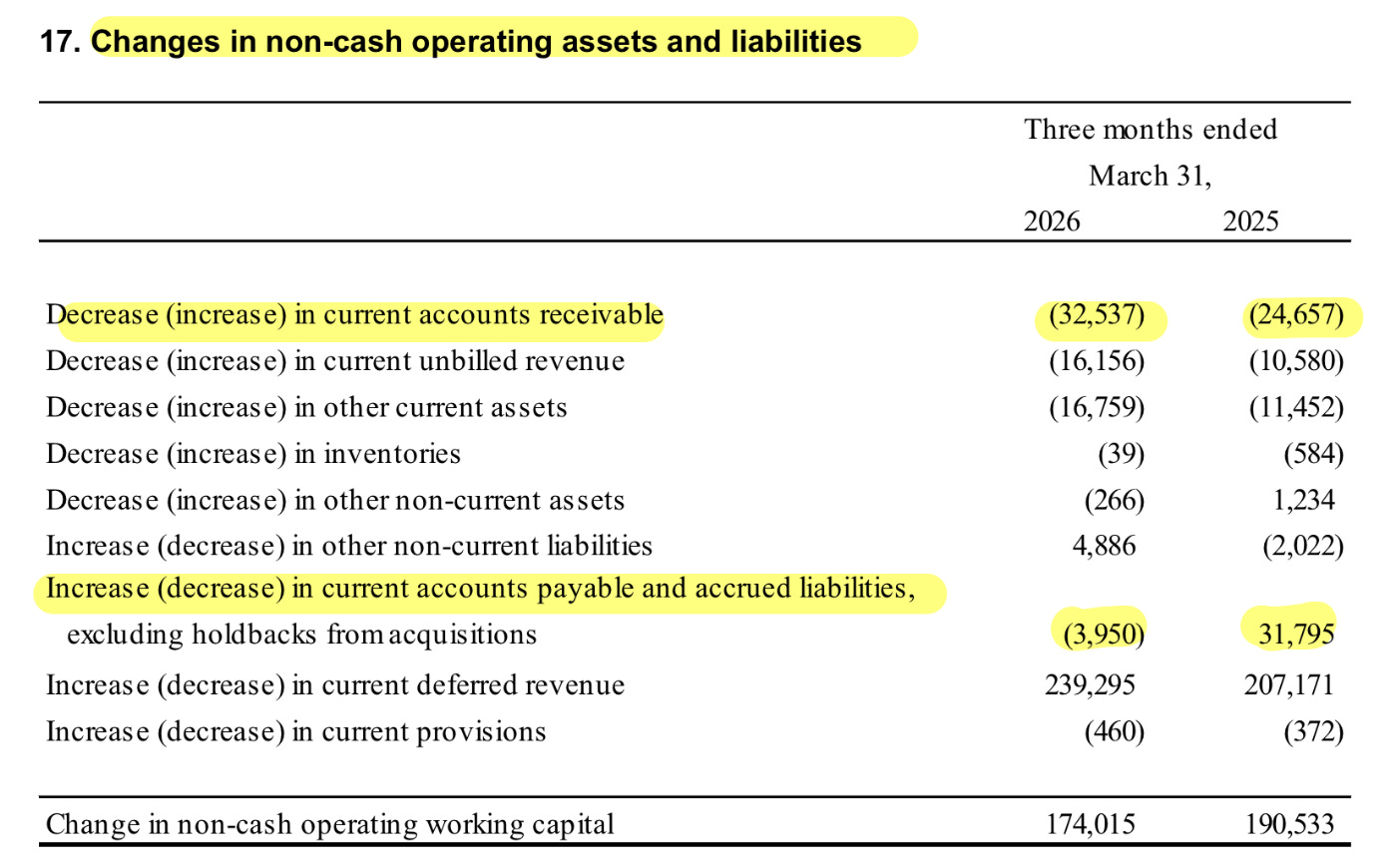

The other “lowlight” of the release could be found in cash flows. Despite strong revenue and EBITA growth, cash flows stayed somewhat flat: +3% in cash flow from operations and +2% in free cash flow. This “poor” performance could be attributed to two things:

Operating net working capital was not as much of a benefit in Q1 2026 as in the comparable period (Q1 2025)

Cash taxes rose

The slimmer benefit from non-cash operating working capital was driven by a 32% increase in accounts receivable and a shift from a benefit of 32 million euros in accounts payable to a headwind of 4 million euros:

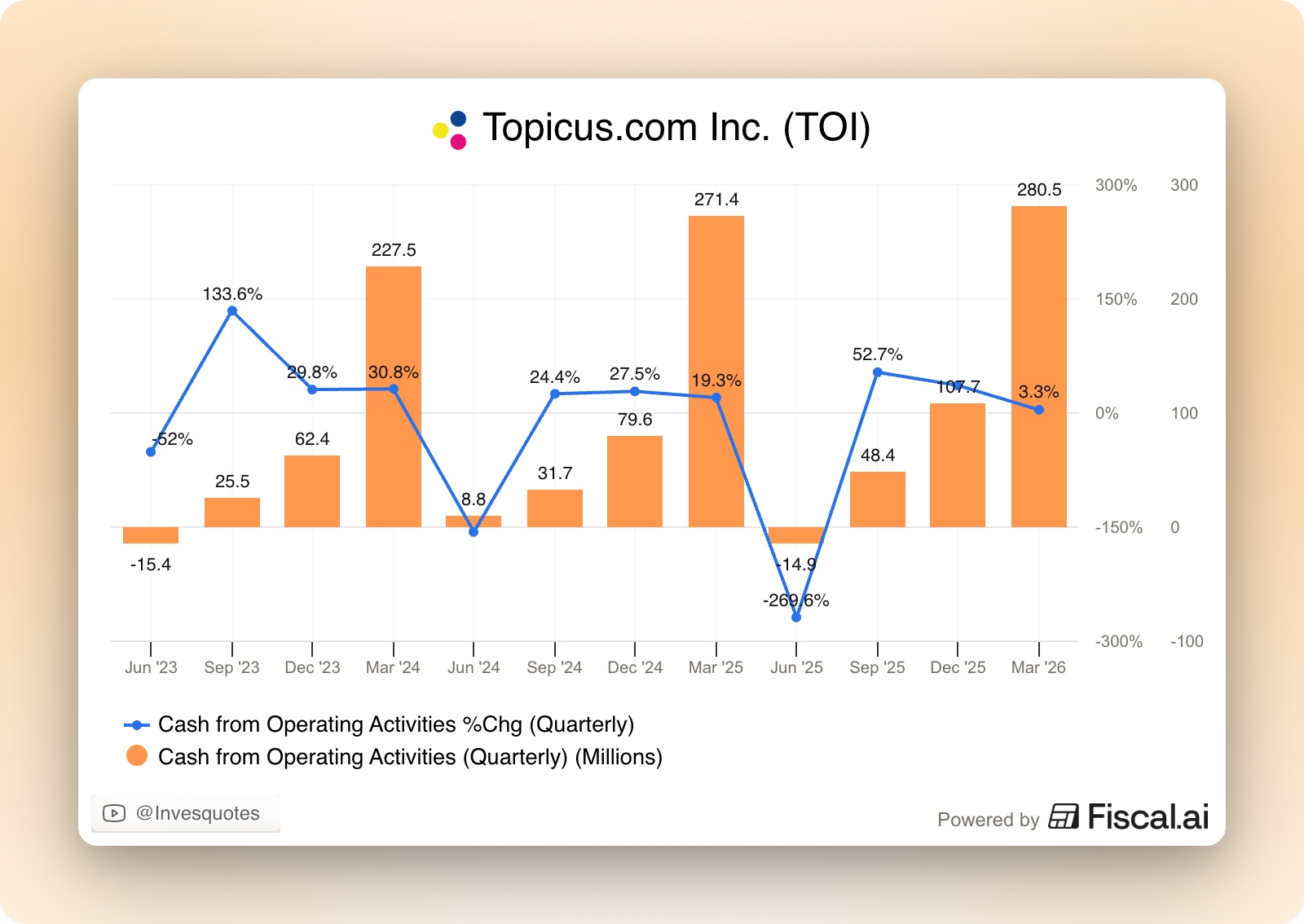

I don’t view any of these as worrying for a very simple reason: it has happened before and it was a nothing burger. Topicus’ cash flow generation is inherently cyclical and cash conversion was stronger than usual in Q2 and Q3 last year:

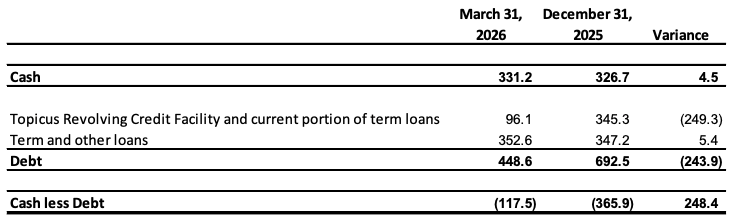

The (still) decent cash generation combined with the lower-than-usual capital deployment allowed Topicus to pay-off a portion of its credit facility. This caused net debt to decrease by almost €250 million:

Let’s assume the company can lever itself to 2x operating cash flow should it need to (a very reasonable leverage level for a business of these characteristics). TTM operating cash flow is 422 million euros, so the company has dry powder of around 850 million euros to conduct acquisition. Subtract 117 million euros (the current net debt) from this amount and you get to around 730 million euros. Bottom line? Topicus has a lot of dry powder to conduct acquisitions over the coming months should opportunities present themselves (I hope they do).

Now, with all this in mind, let’s take a look at the valuation.

Topicus’ valuation

It’s no secret that Topicus’ stock has dropped significantly from ATHs, purely driven by multiple compression. Now, this by itself doesn’t mean the stock is cheap, but let’s take a closer look.