SpaceX (SPCX): Defying Gravity

All you need to know about the historic IPO

For those of you who don’t know, I run a podcast called +FlowKCash with my good friend Javier from Edelweiss Capital Research.

The podcast is in Spanish, but we thought it would be a great idea to translate the transcript of this week’s episode to make it available to you. The reason is that it was a special episode about Space X and what is likely to be the largest IPO in history.

In case you want to watch it overdubbed by YouTube, here it is:

We touch on several topics…

How SpaceX made it: the rockets that exploded, the contracts with NASA, Starlink…

The current segments: $19B in revenue, 10M Starlink subs, the xAI merger…

The future business: space datacenters, Mars, humanoids…

Red flags that nobody is discussing

Valuation scenarios

You should understand all that there is to know about the IPO after reading this. That’s the goal.

You can read this article for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Next up will be a comprehensive report on a macro-trend that will most likely be with use for the coming decades.

Join today:

Introduction & Contextual Framing

Javier: Today’s episode of +FlowKCash is a special about SpaceX, following its imminent IPO. We will talk about its history and the segments that compose it. In addition, we will discuss everything they want to build in the future, from data centers in space, terrestrial transport with rockets, bases on the Moon, and even a city of 1 million inhabitants on Mars. Lastly, we will look at the things that don’t smell good, the risks of investing at these valuations, and what our projections are for the future.

Leandro: Good morning to everyone and welcome to episode number 39 of +FlowKCash. Today we have a special episode. We already did a teaser last week. Today we are going to talk—well, everyone will have seen it already—but today we are going to talk about SpaceX because this is being published, if I’m not mistaken, two or three days before the IPO. I don’t know if the IPO also coincides with the start of the World Cup? In the end, it’s an important week.

Javier: Yes. No, it’s a universal moment. A universal moment.

Javier: Yes, let’s talk a bit today about everything, right? In the end, the idea is that the people who listen to the episode leave here with a reasonable idea of what SpaceX does, where it comes from, and also a bit of what we think. For now, we have the regulatory document, the S-1, which is the prospectus companies have to publish before going public. We are going to base our discussion on that, and also a bit on the history and on Elon’s vision, of course. Leandro, man, it’s very important. We are going to see that the valuation is a key point.

Javier: We are going to have a presentation for those of you listening. It’s not necessary to see it, we are simply going to have it as support, but it’s good because it gives a visual image of many things we are going to talk about: the different rockets, the numbers, and so on. Although we are going to mention everything, it also gives you an idea of how things have evolved in a visual way—really seeing what they have been achieving.

Javier: Leandro, we have to remind people of some things, right?

Leandro: Ah, yes, I had forgotten. It’s just that it’s a SpaceX special, you can’t talk about anything else.

Javier: Remember that we are recording for the second time. We are recording for the second time in the morning, and Leandro is still waking up, it seems.

Leandro: Remind people that if you like it—and I think especially this episode is a good one to share—if you think that people might be interested, because even if you aren’t very interested in investments, this episode can probably interest you. Also, if you want to become members of the channel, we have the option enabled, okay? We want to thank the two members we have. For now, they are few, but in the end, everything helps, right? We do this selflessly because Javi and I really are interested, and we like to talk about these things, but obviously right now the podcast is an expense. We are going to jump directly, Javi, if you think it’s right, into the history of the company.

Company Origins & First Principles Thinking

Javier: Come on, yes, we’ve told it a bit, right? We’re going to start with the history, how SpaceX has arrived up to here, because it’s a pretty incredible history. Moreover, it gives you a bit of context to understand the S-1 or the prospectus for the people who want to take a look at it, and the tone it has. It’s a slightly unusual prospectus, I would say.

Then, we will see what SpaceX does today, where the money comes from, and how the current businesses work. We are going to see what they want to do in the future because it’s a bit of science fiction, not suitable perhaps for cynics or non-visionaries—meaning it is not suitable for the majority of investors. But the same could have been said about SpaceX a few years ago for the people who invested in the private market at valuations that in their day seemed relatively quite crazy. Here we are today with an expected IPO at 1.75 or 2 trillion. Finally, we are going to look at some things to give a bit of criticism to Elon too, right? Some things that smell bad, without filters, and then we are going to finish by talking about the valuation, our thoughts, and there we can enter into a bit of a discussion.

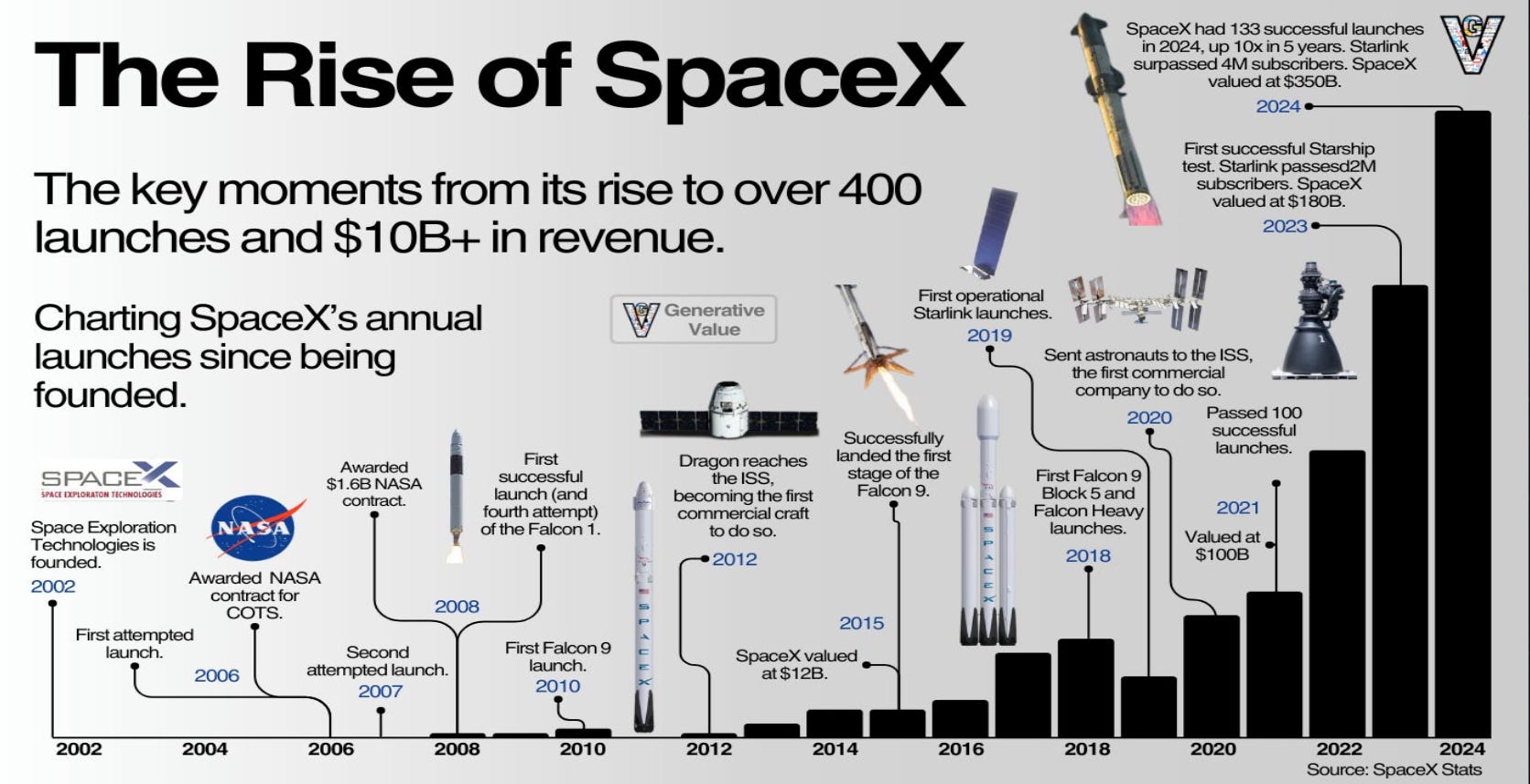

Javier: So we start with the history. This all started in 2001. Musk has just sold PayPal to eBay for 1.5 billion dollars. He is 30 years old, he obviously has more money than he can spend, and based a bit on how he had grown up reading science fiction books and his own interests, he decides that he wants to go to Mars. Not that he wants to go to Mars himself personally, although that too, but rather that he believes it’s important for humanity to be an interplanetary species. Since he is a guy who is, in the good sense of the word, a bit crazy, he starts to talk with NASA, and NASA tells him that they don’t have a budget for missions to go to Mars.

Then Elon, the way he acts, says, “Well, then I’m going to buy a Russian rocket.” He goes to Moscow, he meets with the Russians, and the Russians want to sell him a converted ICBM rocket for about 8 million, okay? Musk thinks that it’s a bit crazy, and in fact, on the third trip he makes to talk with them, they double the price to 16 million, meaning they were pulling his leg a bit. Then Elon, on the flight back on the plane, takes a napkin and starts to calculate from first principles, as he does many times, how much it can cost to build a rocket from scratch by hiring the engineers. That is basically how SpaceX is born. June 2002, initial capital, 100 million from Elon himself.

Leandro: For people who don’t know, SpaceX is Space Exploration Technologies, the official name of the company.

Javier: The thesis that Elon has at that moment is: if the cost of accessing space drops by many orders of magnitude, humanity can become multiplanetary. It’s a thesis of first principles. It’s not “the launch market is worth X billions,” it’s “the cost of steel, fuel... it’s an abstraction of the price of the rocket.” Why? Because rockets are only single-use. For example, if you make rockets reusable, then obviously the unit price of launching collapses. And if the unit price of launching collapses, then space opens up to potential new projects.

Leandro: This is, in the end, Javi, how technology works in general, and what Moore’s Law has achieved, which we’ve talked about in other episodes. In the end, if you lower the barriers to entry, markets are created that today are impossible to imagine because they are prohibitively expensive.

The 2008 Financial Crisis & Near-Bankruptcy

Javier: And obviously, all this has not been easy, nor does it continue to be easy. SpaceX, until 2008—we are talking about the financial crisis almost 20 years ago—had a pretty fucking hard time because it started at a tough time to finance a project like that.

Leandro: That’s another thing, and now we’re going to see it. It’s just that they were on the verge of going bankrupt several times. Three times.

Javier: So they start with their first rocket, which is the one they called Falcon 1, and they do three launches and three failures. The Falcon 1 exploded once from an engine failure, another time a poorly adjusted screw, etcetera. By that time, we are talking about 2008, Elon had already spent almost all his money, the engineers weren’t getting paid on time, and the company was literally on the verge of bankruptcy—add 2008 to that. Then they launch the fourth Falcon 1 rocket in September 2008 and it is successful. The rocket managed to orbit around the Earth, okay? It is the first private rocket that manages to orbit the Earth.

Weeks later—notice that we are in 2008—NASA gives SpaceX a 1.6 billion contract to supply the International Space Station. SpaceX survives, but by the skin of its teeth. This is quite important to understand the mentality that the company has. SpaceX has almost died three times, and Elon himself said that in 2008 the company had like a 10% probability of surviving. Nonetheless, it iterated, it moved fast, and they achieved it. The same has happened to him with Tesla, basically the same has happened to him with all his companies.

Leandro: Yes. I mean, in the end, companies, especially technological ones that we see today, many people look at them and take for granted how easy it is to get there. But along the way, many others have been left behind that, for X or Y, for the same reasons these have triumphed, have failed.

Javier: Yes. And we will see one day when we talk about Nvidia, which won’t be long, we will see that Nvidia was on the verge of going bankrupt a lot of times too. Great businesses have been on the verge of going bankrupt. It’s something logical, and more so when spectacular things are done like the ones these people do, right?

Disrupting Launch Costs via Falcon 9 Reusability

Javier: So, after the NASA contract came a period in which they really started to execute. Ah, by the way, I forgot to change it—for those of you who are watching this, here you can see a bit of the evolution of SpaceX as a desktop background.

In 2010 arrives the first flight of the Falcon 9, which is the rocket that changes everything. Not only was it a better rocket, it was a rocket that was designed to be reusable, and that obviously was something revolutionary. Everyone in the industry thought it was impossible to land a rocket back. There is a video of the CEO, I think it’s from Ariane, which is a European rocket company, who literally laughs at Elon and his intention to make rockets reusable—literally laughing. Well, in 2015, they are also...

Leandro: Javi, as you said before, what Elon wanted was to lower launch costs. This is obviously key, because the problem with launches into space is that when you lose the rocket, a lot of money is lost.

Javier: Of course. We are going to see a bit how the launch cost has been dropping. In fact, in 2015 they are able to land a booster for the first time on land. In 2016 they land it on a barge in the ocean, and in 2017 they reuse one of those boosters for the first time, okay?

What does this mean in numbers? Today, 84% of Falcon 9 flights reuse the booster, and the same booster flies up to 25 times. Imagine the cost reduction that generates, right? That is a bit of what we are going to see now. Reusing a rocket 25 times makes the price go from about $54,000 per kilo that you launched before with the Falcon 9 down to $2,700 with the reusable Falcon 9. We are talking about a 95% reduction, okay? To give you an idea, a duopoly that existed called United Launch Alliance, which was basically a duopoly between Boeing and Lockheed, charged between 350 and 500 million per launch. SpaceX charges 67 million for the same destination, okay? Obviously, the market has noticed this, and in 2025, for example, SpaceX did 165 launches, which is 52% of all orbital launches on the planet. One out of every two is from SpaceX today.

Leandro: Today SpaceX would be the lowest-cost producer in the industry.

Peer Analysis: SpaceX vs. RocketLab & Manned Spaceflight

Javier: Yes, there is data, for example, we haven’t talked about it yet, but you have RocketLab. It’s a much smaller company, I think it’s at a 90 billion valuation with 500 in revenue, but losing money. Nonetheless, for example, RocketLab has rockets that are much smaller, but their attraction or value proposition—they aren’t reusable yet and so on—is that their rockets have a relatively low cost, and moreover, they make it dedicated for you. That is, if any company wants to launch something, they contract directly with them. It’s not like in a shared launch capsule where there are different satellites from different companies put into the orbit that is required. These guys from RocketLab do it dedicated for you. They are much smaller rockets, but what happens with these larger rockets like SpaceX or Blue Origin or any other is that many times you have delays. If you have a problem, then it delays your entire line of clients. So it’s not specific for you, you are simply working with many more clients, right? What RocketLab does is simply give you the priority because you are the only client per rocket, so to speak, at a price, obviously, much more expensive than what you can get here, but with that added value.

Javier: While the Falcon 9 was already starting to dominate the commercial satellite market around 2020, it also launched the first manned mission of SpaceX with two NASA astronauts going to the International Space Station in a capsule designed also by SpaceX called the Dragon. Since then, basically SpaceX has been NASA’s only orbital taxi, up to nine missions that they have carried with this Crew Dragon, as they call it. I suppose many of you will have heard, in fact, that SpaceX had to go rescue two astronauts that the competition, the Boeing Starliner, left trapped in the International Space Station 9 months ago because the capsule had structural problems. It’s almost acting as a savior for the screw-ups of others. A business that emerged as a result of this quasi-monopoly that SpaceX has with the theme of launches—and which is a bit, I think, for the people who are interested and want to invest in SpaceX—the thesis is: look, having efficient rockets at the lowest production cost is a massive barrier to entry. It’s very complicated, it’s not as easy as simply generating software. It’s something very complicated to build. If this gives you a monopoly on launching into space, basically everything that happens in space goes through you.

Leandro: You are the tollbooth for journeys into space, a critical infrastructure, if the space economy really develops at some point. Then you are a tollbooth, and how much is that worth?

Javier: Well, it seems like one, almost two trillions, Leandro.

Leandro: Yes, it’s true. If I’m not mistaken, SpaceX was the first to land an orbital rocket in the year 2015, and I think in the S-1 it says that they have a 10-year advantage because it hasn’t happened again, or another company hasn’t done it until the year 2025, could it be? Or something like that I seem to remember reading.

I think there are some Chinese companies that have achieved something.

Javier: There are some. I mean, in the end, it has been a monopoly for 10 years, right? It’s true that it carries an advantage, but now it does seem that they are matching it somewhat in terms of being able to lower the launch cost.

Javier: Sure, but we are comparing—later we are going to see the different rockets—we are comparing Falcon 9 with what some Chinese companies are achieving now, or you could say Blue Origin with the New Glenn and so on, which are still a bit obviously exploded. In the end, the 10 years of advantage, you carry it anyway. The thing is that it wasn’t just that it carried 10 years of advantage, it’s that nobody had even been capable of achieving what you had done in 2015.

Starlink’s Global Dominance & Satellite Economics

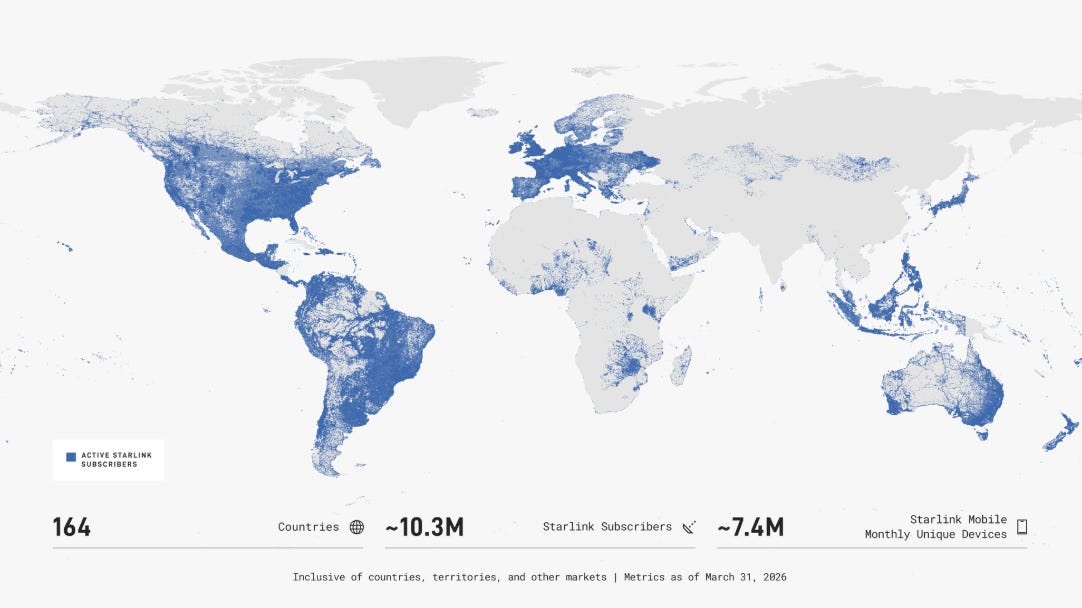

Javier: And now with the Starship, which is the last one you see there, the launch cost drops significantly. We are going to see it. It is even expected that they will be capable of lowering it even more, still. Okay, now we’ll talk. Before, I wanted to talk because it goes a bit earlier in the timeline, the theme of Starlink, which I suppose many people know, right? In the end, it’s the capacity to have internet via satellites with broadband for everyone, basically. When they launched it in 2015, the reaction of the market in general was, as always, skeptical. OneWeb had already tried it, Teledesic tried it, Iridium tried it, and all of them failed, or the use cases were relatively very niche, smaller, not something really very scalable. The difference, obviously, is that SpaceX could launch its own satellites with its own rockets for a fraction of the cost that any previous competitor had faced. That has made it so that today Starlink, or SpaceX, has 9,600 satellites in orbit, which is crazy, Leandro. Because if I tell you they have almost 10,000—they have lost some, they have launched I don’t remember if it was 12,000 or 15,000, 12,000 I would say, but they have about 10,000 satellites in orbit—what percentage do you think that is over the total of satellites in orbit around the Earth?

Leandro: Look, I don’t have the remotest idea, but I’m going to say 70% almost.

Javier: Correct.

Leandro: Oh, well look, it seems like I knew it, but I had no idea.

Javier: It’s almost 70%, it’s almost two-thirds of all the satellites there are. We talked about it in a program, in fact, now I’m going to give you a piece of data that I’m sure you do remember. It’s crazy to think that two-thirds of the satellites there are in orbit are from SpaceX and Starlink. They already have 10 million subscribers to the service and they are present in about 125 countries. The numbers, in fact, have been quite powerful. They have gone from 500 million in 2021 to 11 billion in revenue in 2025. It’s almost 22x in 4 years. Obviously, we are talking about a company that is going to come out at almost 2 trillions. 11 billion is not much, but let’s separate a bit the valuation from what they are achieving and the growth they have had with things like Starlink, okay? The theme of this that I was telling you about, let’s remember a number that we talked about when we discussed data centers in space, we mention it again because of the 10,000 they have, they have requested authorization to launch up to 1 million. 100 times more. Okay, we leave it...

Leandro: Let’s see, but if you think about it and launch costs are reduced so much, in the end, it’s just that for the same price you can launch that. This we will talk about a bit later in future projects and the things that they want to do or that they propose that they can do.

Starship Mechanics & Evolutionary Engineering

Javier: Finally, in this part of the history, is to talk about the Starship, which is the rocket that comes to change everything. Really they started to design it and build it in 2019, and basically Starship is the largest rocket ever built. It’s 120 meters in height, it can carry 150 tons to low orbit—to give you a bit of context, the Falcon 9 carries 22.

We are talking about seven times the amount, and they want to make it 100% reusable, both the booster and then what comes to be the Starship, which is the top part.

Leandro: Because on the Falcon, Javi, for now, the only thing that’s reusable is the booster but not the rocket as such, or how?

Javier: No, both parts are reusable.

Leandro: Okay, okay, okay.

Javier: In Starship they have managed to catch it. Have you seen it, surely? If someone hasn’t seen videos of how they are capable of catching the booster back to Earth, see it because the truth is that it’s spectacular. For now, the booster yes, they have recovered it. The Starship, sorry, not yet, but it’s in the project and that is the theme—as you know, these things take time.

The development of the Starship has cost 10 billion, not bad. They had 11 test flights. The first flights obviously exploded and even some on purpose. At SpaceX they say that if it doesn’t explode, you aren’t learning fast enough. What does the Starship do to the cost per kilo? If the Falcon 9 lowered the price from 54,000 to 2,700 per kilo, Starship aims to lower it to less than 100 per kilo, another factor of 27 times reduction. It’s just very crazy. For this, obviously, the Starship would have to be fully reusable. When accessing space costs you less than almost a transatlantic flight per kilo, the economy maybe reorganizes itself, right? And things that didn’t make sense to do today—we could say data centers in space, factories in microgravity, or space tourism—maybe they start to work economically. But the truth is that the Starship still hasn’t entered into service and moreover, they go with a lot of delay, like almost everything in general, so you have to take it into account too, okay?

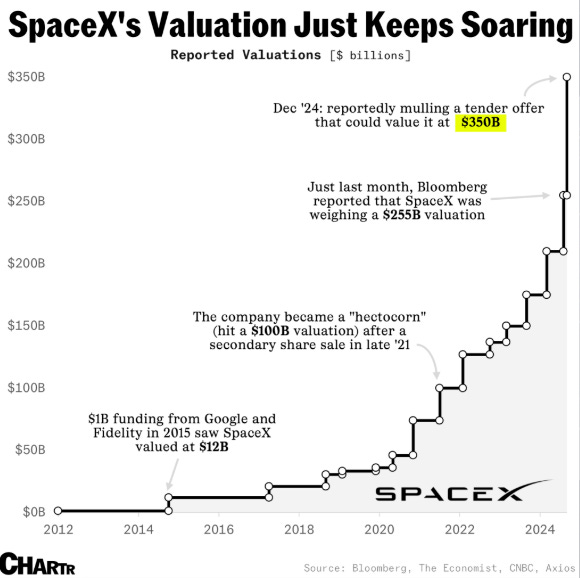

I bring you a bit, to finish with this long introduction, how the valuation of SpaceX has been changing and what financing rounds they have had.

They have raised more than 10 billion in private capital. Let’s remember that for this IPO they propose to raise between 70 and 80 billion, okay? They have done series from 2008 until a series N in 2025. They have been raising capital, as you can see there, almost always, because in the end, there’s no choice. As many of you know, their investors include everything from pension funds, like the Norwegian pension fund, to Google, among many, many others. In each round, almost the valuation has more than doubled. Always Elon said that he didn’t want to go public. I don’t know if you remember when Tesla had problems, not problems where the quote dropped and so on, and Elon always said that he proposed even taking it off the market. He didn’t want to ever take SpaceX public, and look how things have changed. It’s also true that raising 80 billion... I understand that he wouldn’t have many problems in raising them in private markets, especially now, but he has decided to take it public. I can’t tell you very well why, because I don’t know. If you want, we can discuss that.

Public vs. Private Markets & The xAI Acquisition

Leandro: Let’s see, later we can talk about it, but it’s also true that he takes it public but it continues to be a controlled company. I mean, it’s not a public launch as usual of what we are used to, I would say.

Javier: That’s true. It’s also interesting that he has changed his mind, not wanting to have it public, now taking it out. Obviously he has the power, so it matters little, quote-unquote, but you control less... well, you don’t control the valuation, that’s the truth. While in private markets, you have much more power. In the private market, he controls the valuation because you don’t see it. Well, yes you see it, but when you have to raise money you have to put a valuation. What happens is that I think the demand that has always existed in private markets has been much superior to the supply, so you can put the valuation that you want.

Leandro: Yes. And I would say that in private markets it’s much more difficult for a narrative... you have a lot of time between financing rounds, or you can dominate the narrative in a very different way than in public markets where suddenly you find yourself with a narrative against you and the price starts to react on a daily basis.

Javier: Yes. And finally, to talk about the timeline that we were mentioning, because there have been a couple of facts that don’t come out here since this only goes until 2024, but as many of you know, in recent years things have happened that are relatively important. We talk above all about xAI, which came when in 2022 Elon put the blanket over his head and bought Twitter for 44 billion. I don’t know if you remember that era, because Twitter now is part of SpaceX. We are going to tell a bit what has happened today in case there is anyone who hasn’t found out.

So, we are in 2022, Elon, to defend the capacity of people to... how do we say it? How did he mention it? Freedom of expression. Sorry, I was going to say, to defend freedom of expression, Elon decides to put 44 billion to buy Twitter and to end all the Woke ideology. Obviously, he didn’t put the 44 billion entirely himself, but he did put part, and then he raised capital and debt on the part of many investors, 44 billion. He renames Twitter to X, that surely we all know, with the idea of building a superapp in the style of WeChat. Advertising revenues collapse from 5 billion in 2021 to two in 2025, a drop of 65%. It’s very crazy.

Leandro: I must say, Javi, as a user of X, when Elon bought it, the first months you could tell a lot that the application was worsening, that was so. You noticed the change a lot. Evidently, he was also doing it with much less staff because it was like a disruptive process. He had fired a lot of people, thought it could be done with much less, and yes I must say that the application lately you notice that it’s improving quite a bit. Many people complain that the content is worse. Well, but that’s the human being. If you see the content there is in reels on Instagram, each time it’s worse or more nonsense. But it’s because of what people see, it’s not the fault of the one who puts the means of distribution.

Javier: Yes, that’s a debate that could be very long, truly, but yes, it is the fault of distribution because in the end it’s pushing those things, but it’s pushing those things because it knows that’s what keeps people in the application, it’s not doing it for any other reason.

Leandro: Yes.

Javier: So, let’s go back to the financial case. Think of the investors who put money in the purchase of Twitter—from Andreessen Horowitz to the Saudi funds, to say some—they were sitting on enormous losses. The value of Twitter as a brand had dropped completely, and Elon doesn’t like when his investors are losing money, that’s something that at least you have to give him. Then, in 2025, you already know that X or Twitter started also to develop its own language model, an LLM, and changed the name of the company from X to xAI. What Elon decides in February 2026, 6 months before the SpaceX IPO, is that SpaceX is going to acquire xAI in an operation completely with shares, valuing xAI at about 300 billion. He had bought it at 44, now it’s worth 300.

And he was valuing then SpaceX, all the part of Starlink and the rockets, at a trillion. So joint valuation 1.3 trillion, now it’s going to come out at 1.75, going up. Conclusion: the xAI investors are happy. Everyone is happy because now you are integrating vertically your artificial intelligence platform with SpaceX.

Leandro: Which there, Javi, do you think... I mean, I, for example, think of the three segments, right? Which we have already commented on a bit. We have the launch part, like the pure one of SpaceX. Then we have the communication part, which would be Starlink, and then we have xAI, the AI/X part. I understand completely the synergies between SpaceX and Starlink. In the end, this launch method is vertically integrated into the part of Starlink, but it costs me much more... I mean, evidently in the future you can see connections, because if you start to launch data centers into space, the xAI part can also be understood. I didn’t understand the rationale for the X acquisition until you told me this about the investors, which now I understand much better—I understand much better the motive for the integration of xAI inside SpaceX.

Cash Burn, Compute Infrastructure & The Anthropic Deal

Javier: Now I’m going to give you another motive. xAI was burning almost a billion a month, okay?

Leandro: Okay.

Javier: In infrastructure expenses, the compute, creating a laboratory like it can be an Open AI or an Anthropic, plus all the infrastructure layer because they have mounted Colossus, which is the largest data center in the world. That burns a lot of money and Twitter wasn’t working well—later we are going to see the numbers also of Grok and how many users it has and so on—but you were burning money, the money runs out. However, SpaceX was profitable and it generated cash. What do you do? You merge them, problem solved.

Leandro: And now we are going to see. SpaceX is profitable because of Starlink, right?

Javier: Correct, correct. Now we’ll see the numbers for each one. And what you have said, right? The potential synergies in the future. In the end, Elon has always been characterized by trying to integrate vertically and the vision he has obviously in the end is that AI is going to allow him also to iterate much faster all his designs—what we have mentioned of rockets, data centers in space, etcetera, simply holding an empire.

I think you also have to think about it from the point of view that Elon also has Tesla, because with Tesla, you are seeing Terafab. You are seeing how even arriving at the fabrication of the chips themselves... vertically integrated to the extreme, to the point that people say, “This guy is stupid.” But in the end, he can be stupid or he can be a visionary. We aren’t going to know until we see the future, but that’s another of the reasons. Right now the betting markets give, I think it’s above 70%, that Tesla and SpaceX are going to merge this year. I don’t know if it’s this year or the next, but in the next 12 months, 70%. It seems like it’s, quote-unquote, pretty clear that they are going to merge, and then you have the Holy Trinity almost mounted there. I was commenting this to you as a result of... I forgot.

Javier: No, I don’t remember. Now it doesn’t come to me, but later it will come to me I think. Later it will come to me.

So we are going to start to see now each of the current business lines to understand a bit where they come from, where they go, how it’s growing, to then understand a bit also the valuation and see if this makes sense or not, okay? So let’s start. By the way, for the people who are watching it, we have especially quite a few slides for the SpaceX part showing the differences between the Falcon 9, how the launch cost has been dropping, all that type of things that we aren’t going to comment on very in depth because we don’t have time.

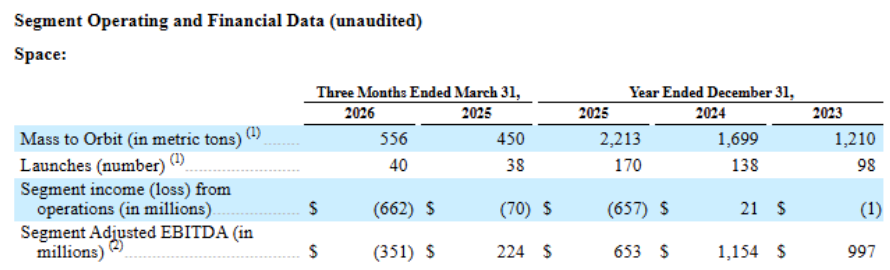

But if anyone wants, simply we are going to pass them as we talk, and if anyone wants, pause it and take a look at the data because there are interesting things simply to have a bit more knowledge, okay? And whoever is listening, it’s not necessary because they can go in to look at it later, but the important data more or less we are going to mention, right? So we have here the main numbers of the space segment, which are the launchers, basically, and we have a business as we can see it where we only have the data for 2023, 2024, 2025 and how the first quarter of 2026 evolved compared to that of 2025. They report what is the amount of kilos that have been launched into orbit, the number of launches, and what are the metrics both of revenue and of operating profit or adjusted EBITDA. You already know that EBITDA in these cases that are so capital-intensive, and on top of that adjusted, I wouldn’t take them into account to understand how the business really works, right?

There are things that draw one’s attention. Obviously, the number of launches has grown, but it’s not crazy either. We can see that in 2023 they launched 100 rockets, in 2025 170, and so far in 2026, for example, they have launched less than in 2025. The market currently is what it is, it’s not something super booming either, nor does it grow at very crazy paces. The same look at the revenue. Besides, we have to think that if SpaceX is launching Starlink without stopping, although the number of launches increases, if you launch for yourself, that doesn’t generate revenue. That’s why we see, for example, that in 2026 the revenues have dropped, for example, with respect to 2025.

Leandro: I mean, Javi, launches are counting also their own?

Javier: Sure.

Leandro: Okay. They launch their own but they don’t generate revenue. Ya, ya, ya. It seems to me the KPI is fine, but it would be better if you saw the launches that generate revenue versus those that don’t.

Javier: Well, you could say that then they generate revenue for you through Starlink, you know? So yes, yes. As you can see, the operating losses are almost the same as the revenue. You generate 600 million almost in... sorry, no, I made a mistake, it’s 600 million and in revenue, you lose more or less... 600 is basically the number. It doesn’t make sense. In the end, this is a segment that allows you to do the rest of things, at least in the Starlink part, right?

What type of launch are they doing here? In the end, commercial launches, satellites for companies, governments, telecommunications operators, you have government contracts with NASA, with the Department of Defense. The Falcon 9 continues to be the rocket that you use the most, with 165 launches in 2025. You have the Falcon Heavy, which is basically the same capsule on top but with almost three times the boosters, and the Starship, which obviously still is in the testing phase, right? It’s important to know that the most important client is the United States government, the Department of Defense, and what is the interesting thing about this business?

In the end, it’s what we commented on before, that it’s almost a tollbooth that many companies or governments or whoever have to pass through to be able to launch things outside, okay? It’s as easy as that. Obviously, when the Starship is in operation, it’s going to cannibalize the Falcon 9 too, because it’s simply going to be much cheaper. So you have to take it into account.

Without further ado, what was said, I’m passing some slides so that people see it, and here you can see the difference between the Falcon 9, Falcon Heavy, Starship, and some differences. Well, I pass them forward, okay? Whoever wants to, stop it. And above all, Leandro, when later we talk about valuation and you tell me something about whether it’s very expensive or whatever, I’m going to tell you how much this is worth because the images are spectacular. I repeat again to the people that if they haven’t seen truly how they catch the boosters and so on, it deserves to be seen, or it deserves to see a launch. Finally, to finish the space part, it’s a bit to show you... I don’t know if to say that it’s the culture of Tesla or SpaceX, or it’s a bit how Elon works, which is, I think, independently of whether you believe that his companies are overhyped or very overvalued or whatever...

Leandro: You know what happens? I think here it happens a bit—and I’m going to mention another company—what happened with let’s say with Palantir. In the end, when Palantir was, let’s say, at $10, everyone said that it was overvalued because it quoted at multiples of 60 times. Okay, people continue saying it today when it’s trading at $150 because the multiple continues to be high, but what is evident is that at $10 it wasn’t overvalued. You can’t have the two points of view because in the end, yes, the multiple continues to be high, but if you take the $10 and take today’s numbers, it wasn’t overvalued, right? Because they have grown above what everyone expected. I think that with Elon’s companies it happens a bit the same. In Tesla, many people say, “No, it’s just that it’s hyper-overvalued,” okay, but the same one who says it today was saying it 15 years ago when things are already quite different, right? So there have been advances too, and the bears from 10 years ago maybe weren’t right, which doesn’t mean that today’s aren’t right. But you also have to take it into account.

Javier: Yes. All this is quite complicated. I agree. How much is what Elon is building worth? I don’t know if it’s two trillions. It’s hard for me to see it, but maybe we are mistaken. I also would have told you 3 years ago that 300 billions was crazy.

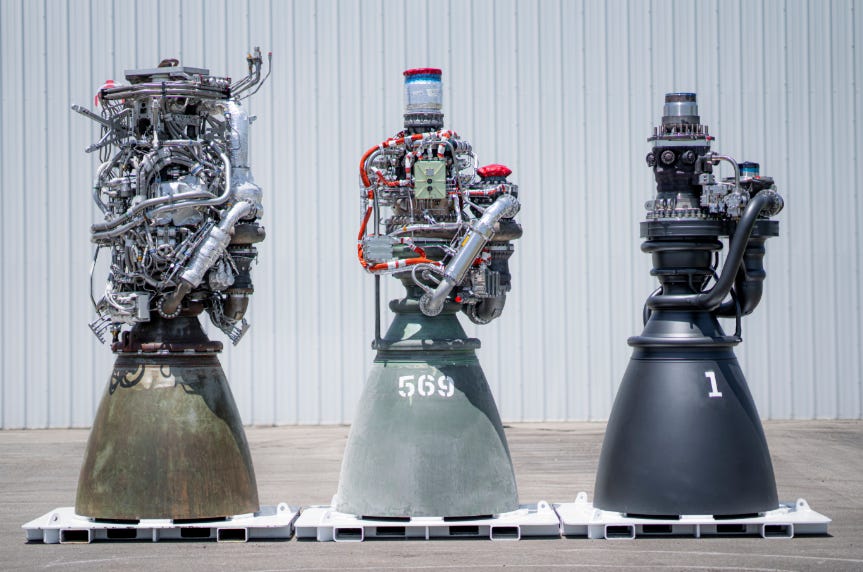

And here we are discussing if two trillions... Is the market crazy? I don’t know, but independent of that, we leave that for the end. I think that what he is achieving, what he has achieved, right? Although he has gone with many years of delay, because that is a fact, what he has achieved is incredible and that is what we are trying to tell here, and then we’ll see if the valuation makes sense or not. But this is the evolution that the Raptor engines have had, which seems to me spectacular, how they have been evolving it.

It’s very interesting to read also the biography of Elon. Have you read it, Leandro? I suppose so.

Leandro: No, no, I haven’t read it.

Javier: It’s worth it. How the guy tackles all these types of problems, or how he thinks about problems. I think these images of the three engines, the evolution, is a clear example, okay? It’s quite spectacular. I think this image is very visible, that’s why I put it in.

Come on, let’s go to the part that is a bit the crown jewel, in fact, the one that generates benefits, what is financing the rest of things, which nobody believed, but here it is. It’s that maybe what people don’t understand with Starlink is that each new generation of satellite has more capacity and you have lower cost per bit. That means that as you go replacing the constellation, the margin of the business improves automatically, and more obviously the adoption, but you don’t need to grow much to improve profitability.

Leandro: I, in this, Javi... I in this segment have my skepticism. I mean, it doesn’t seem reasonable to me, in the same way that it doesn’t seem reasonable to me to look at the losses of the space part because really many of the losses you are assuming them to generate benefits here in the Starlink part. Neither does it seem reasonable to me to take Starlink, take the profits, and say, “Look at how profitable it is.” Because in the end, you need the other part to be able to make it real.

Javier: Yes, yes, yes, yes, correct. It’s correct.

Leandro: And then also that Starlink today is a monopoly that is not going to continue being so. I mean, those are the two things that would squeak at me most about this part, but evidently from today’s numbers it seems like a very good business.

Javier: Yes. Let’s see, sure... I think you have to take both as consolidated, right? In the end, I mean, I don’t know how they will be accounting for it, I’m going to be honest, if they are putting the costs... maybe here we have the costs, they charge it to the space segment. It could be, sure, I’m not sure, so I’m not going to launch into it, but you can consider both and be able to have a better idea. Nonetheless, we can see how basically the number of Starlink subscribers has doubled. It’s also true that they have started... we told it in the case of AST, we told how Starlink was going also, which is a bit the value proposition of AST directly to the phone without need for the antenna and so on that Starlink had before, and they have collaborations with... right now I don’t remember if it was T-Mobile in the United States or which was the operator they were using to give this service, right? I am also a bit skeptical. Now the movement that Starlink is making is trying to go directly to the phone so as not to have to have all the additional hardware. It’s a different functioning, okay? And it’s still in the development process and launching the new constellation of satellites. There is a lot of stuff to disentangle there, but it’s wanting to have an approach to the business model relatively similar to the one we told in the case of AST, which was a few programs ago, okay? In case anyone wants to listen to it.

Leandro: Yes, if I’m not mistaken, Javi, Starlink is direct distribution, while AST is distribution through mobile operators, so I would understand that at first Starlink is going to have better margins for the fact of not having to pay a “commission” to anyone.

Javier: It should, yes. No, two things. Yes, Starlink originally was direct distribution, now Starlink with the directly-to-the-phone is going through T-Mobile in the United States, and it also has partnerships with... similar to AST, which I think there are many people who say, “No, it’s just that AST has directly the partners with a lot of operators.” Yes, it’s true, and in fact they form part of the shareholding, but in the case of Starlink, for example, it already has also 27 partnerships with operators, Deutsche Telekom in Europe, for example, it rings a bell that it also has it with AT&T.

Leandro: I mean, I think that here what you have to see is in the end, Starlink before was alone and now you have AST coming, you have Amazon Kuiper... in the end, more are coming and you don’t have an exclusive distribution agreement. In the end, if the technology becomes commoditized, they will use one would think the one that costs less.

Javier: It’s true that how they are approaching the problem of providing this service between AST and Starlink is different. AST are few mega-large satellites; Starlink are many satellites. To be completely sincere with you, I don’t have a clue which proposition is better. I mean, I understand that each one has its advantages, its inconveniences.

Leandro: And if we look at the future a bit, I evidently here yes that I see synergies with the Elon ecosystem because if you are building humanoids and autonomous cars, you need connectivity in any place always. So there I can see a certain synergy, right? Which in the end is part of the vertical integration that Elon looks for.

Javier: Yes, later we see it a bit in future projects, but that’s the idea, right? Well, I’m the same, passing several images. We aren’t going to enter into detail on each one of the different satellites, the different versions and how they have been improving, okay? And we are going to pass this.

Look, this is a bit the footprint they have and so on. Well, for whoever wants, let them stop it and take a look. Let’s go...

Leandro: Interesting what we commented in the episode of ASTS. We said “Hey, yes, but if the use case of this is for less developed geographies, the revenue per user is not going to be able to be very high.” And that is seen in Starlink, right? Because they have been expanding to less developed geographies, and the revenue per user has been dropping in a relatively consistent manner.

Javier: This is something that has happened in cases as simple as Spotify or Netflix. Since growth comes from emerging regions, you see that the ARPU has remained constant or has even dropped prices in developed markets. That’s simply part of how this works, okay?

Finally, the part of artificial intelligence, which as we have commented before, basically it’s three businesses in one. You have X, Twitter, with advertising, which generates about 1.8 billion a year. What we said has dropped from five since 2021. It has the subscriptions... well, no, that would be the second business, which would be X Premium and Super Grok. X has like about 4 million premium subscribers, which is not that much, I would have thought it was more, and about 900,000 subscribers to Super Grok, a month, $30 a month respectively, well, you have combined revenues that are quite modest. By comparison, ChatGPT has I don’t know if more than 15 million users, meaning quite far, right? And in fact, staying a bit behind.

And finally, you have the layer of computing infrastructure, the Colossus, that SpaceX has like 325,000 Nvidia GPUs under management, and just before the IPO—and this is quite interesting because the bulls of SpaceX took it as a super, super bullish piece of news—the fact that xAI has signed a contract with Anthropic of 1.25 billion a month to use part of the infrastructure until May 2029, okay? And people say, “Holy shit, how smart Elon, who has offered that capacity he had.”

Leandro: In the end, he has become a hyper-scaler just like that out of nowhere.

Javier: Yes. And the theme is, “Wow, what a guy, how he saw it coming, how good. These are 1.25 billion more a month. Incredible.” Sure, but what this tells you is that Grok is not working as expected. They built capacity to spare, correct? And it is detrimental to Grok and its development of artificial intelligence that it’s not going as well as they had planned. And well, I mean, so that we see how the narrative can be used in any way. If they didn’t have that capacity or because it was being used by their own business, maybe they were giving worse numbers in theme of revenue, or even yes, because maybe they go out a lot at losses, but nevertheless, the business would be going better than what maybe it’s going now. I don’t know if I’m explaining myself but...

mean, so that we think about it, 1.5 billion coming from Anthropic a month assumes about 14 billion annually, which is almost doubling the revenue that SpaceX does. Just for this, so that we are conscious of the numbers so small, quote-unquote, of which we are talking, that SpaceX is still taking in, that only... and if you put it at 3 years, well, that’s about 45 billion in 3 years, the contract, which later can be canceled along the way or whatever, but it’s quite significant if you look at the current numbers.

Financial Analysis: Consolidated Margins & Aggressive CapEx

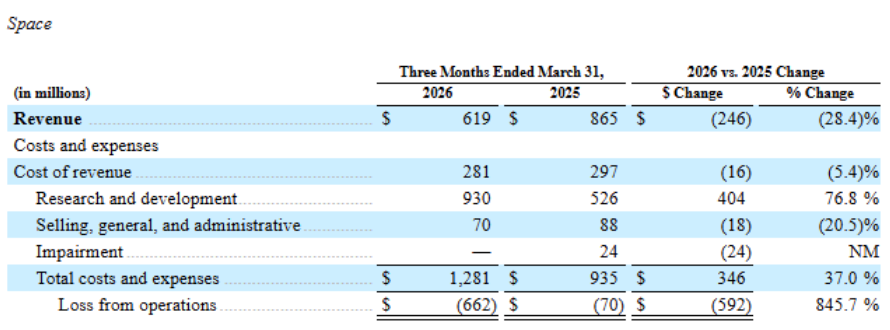

Javier: And finally, we have the consolidated numbers. What we said, last year they did 18.6 billion of revenue for some operating losses of 2.5 billion, and this is going to shoot up this year because this is not consolidated yet, xAI, which as we have seen, has some losses in the quarter of 2.5 billion.

Leandro: Well, these are the numbers for the first quarter of 2026. We see the business has grown 15%, I mean, it’s difficult to justify a multiple of 50 times revenue, I think it is if we take 20 billion depending on the valuation that comes out, but about 50 times revenues with a business growing at 15%. Obviously, who knows what is going to happen in the future and what Elon is going to manage to do if he truly lowers launch costs so much.

Javier: Well, it’s much more, right? Than 50 times they are going to do this year, they are going to do almost 40 this year or close to 40. But it’s what was said, that now you generate revenue for Anthropic because another part of your business is not going so well is positive, right? That’s why I say that the multiples, it’s relative what it means, but if you do 40 billion at 2 trillions, 50 times. Okay? And the last thing I wanted to show you was the CapEx.

Leandro: Well, the CapEx has fascinated me because in many companies you think, “Ah, look, the CapEx is...” in hyper-capital-intensive companies, the CapEx is a 20-30% of sales. How much is it for SpaceX, assuming that they are going to do about 40 billion in 2026 or 30?

In the end, it’s more than one times revenue, the CapEx, right?

Javier: No, where? Let’s see, it has 18 billion of revenue and CapEx of 20 billion in 2025. Ah, okay, yes, sorry, you’re right. Yes, correct. Crazy. Correct. And later we are going to see some very interesting things regarding CapEx, because in the launch part they are accounting for some rocket development expenses, they are passing them through the P&L as research and development expenses instead of capitalizing them, okay?

Leandro: To me, at first you tell me that way and it seems to me a more conservative accounting in the sense that you are assuming that all of it you lose and that it doesn’t report revenue to you. But maybe at this moment what they want to show is, “Hey, right now I’m losing money but I’m not spending so much on CapEx to generate future profits.”

Javier: I don’t know, it could be... you can see it both ways as you want, but yes, they have spent in the first quarter of 2026 10 billion. Annualize it, it’s almost 40 a year, which is basically what we expect them to have in revenue. We all understand now why they are raising 70-80 billion, right? Yes, it’s clear. I mean, it’s necessary.

Theoretical Markets: Satellite Scaling & Lunar Infrastructure

Javier: Come on, this we can leave it here and we are going to talk a bit, Leandro, about future business lines, what the prospectus says a bit of the things that can happen, okay? And all this, of course, it’s important to understand that the key to everything is Starship. When you are capable of carrying a cost of 1 kg of weight into space passing from $2,700 current to less than 100, that is the key to everything and that is what has to happen to start to build everything they are talking about. Because we are talking about, for example, data centers in space, which we have an episode in which we talk about that, we talk about the physics behind the opportunities, and why truly it makes sense from a point of view of first principles, if you want to say it, but also what are the risks and the difficulties of achieving it, and we have talked about it. So I would recommend that if you are interested in this part, that you go see that one because there we explain it a bit more thoroughly and it doesn’t make sense that we repeat it now.

And this is what I was telling you before too, about the petition that SpaceX has made to the FCC to reach up to 1 million satellites in space from the 10,000 current, let’s not forget. We have commented on it before, it’s Starlink. This doesn’t come out directly in the S-1 but obviously it’s one of the main reasons for which Amazon also is in this war to have capacity of connectivity from satellites to potentially control an, quote-unquote, army of humanoids, right?

Leandro: It’s the capacity of the satellites that Amazon already is putting it from this point of view. If I am capable of having a network of satellites in space, my data center clients know that there is always a backup to the connectivity problems that can happen on Earth and that it can always be operative, that in the end, the failures in data centers cost billions of dollars every time they occur.

Javier: Later it’s also important to take into account, and it’s a bit, I think, where things are going. You know that the American government has said now that it wants to have a base on the Moon. I think it’s as space starts to become a part of the critical infrastructure, be it for commercial infrastructure, the armies obviously want to have a position there, and yes that truly it could become a strategic asset to control space, quote-unquote, right? And now I’m going to give you a couple of comments in that regard. The first thing you have is the lunar base, what we have said, simply operational to extract resources, potentially water ice from the poles, produce propulsion fuel, use the Moon simply as a gas station. If you can produce fuel on the Moon with lunar resources, you can refuel spaceships without having to raise fuel from Earth, and that multiplies by a lot the operational radius that you could have in the solar system. I know that we are talking about craziness, but in Elon’s head, these aren’t crazies, these are things that are going to happen. We’ll see when, but they are things that are going to happen.

Leandro: And I must tell you that I also am convinced that they are going to happen. I mean, we don’t know when.

Javier: Yes, there is the theme of jurisdiction and property in space. There is a treaty from 1967 that says that no state can claim sovereignty over the Moon, but it doesn’t say anything about private companies, and SpaceX is on it, obviously, right? Then I suppose you have seen images also of...

Leandro: Sure, Javi, you are telling me that it’s two trillions, but you have the Moon. Maybe it’s not so bad... Moon, and the next thing, Mars... it’s not so bad, eh?

Javier: There we go, a trillion each.

Rocket Earth Travel & The Mars Colony Timeline

Javier: Also, apart from this, you have... I don’t know if you have seen they brought out in one of the last presentations like launchers from the Moon. Obviously, gravity is much lower, you have like a catapult basically and it’s capable of sending... Well, they also have in the S-1, it comes out also, journeys point-to-point on Earth with rockets. What happens if you use a rocket to go from New York to Tokio in 45 minutes? They claim that Starship can do that. Technically the numbers work at Mach 25. Obviously the initial target market would be luxury travel, high-level executives, military obviously, the Department of Defense for sure has interest in being able to move troops and equipment to the other side of the world in half an hour. In fact, there exists a program called Rocket Cargo on the part of the American army, and SpaceX is in it. And SpaceX says that for the mid-2030s it could have some route operational. We’ll see, because if they say mid-2030s, maybe it’s mid or late 2040s, but imagine boarding wherever and in half an hour being wherever, basically, because it doesn’t matter because you arrive in a moment. They are science fiction ideas, but well.

And then you have, of course, Mars, which has always been Elon’s dream and it continues being there. What the S-1 says in reality is... I don’t know if you know it, but the launch windows from Earth to Mars due to the alignment of the planets and being able to catch the correct orbits to be able to use the different orbits and be able, in fact, for it to be effective... The launch windows from Earth to Mars open only... they happen every more or less 26 months, and 2026 is one of those years in which there is a window to be able to launch to Mars, and they have as an objective to launch the first uncrewed cargo mission to Mars this 2026. It has surprised me to read it because it seems very soon, no? They talk also of the first manned mission in 2028 and an initial city for the decade of 2030. City, okay?

And in fact, Elon Musk has...

Leandro: We have to solve, Javi, we have to solve the housing problem.

Javier: Yes, Mars, there is space, and on the Moon too. In the incentives of Elon for his remuneration package, he has 15 blocks which are activated with different milestones. The last of them, for his retribution to be equivalent—because it’s also through shares and so on, but it would be the equivalent of a trillion dollars—would be to have 1 million inhabitants on Mars. It’s very crazy, it’s very crazy.

Leandro: And this, what year... in what year would it be unlocked or is it by KPI without limit of years?

Javier: I think it’s without limit of years. Another is a valuation, I don’t remember now if it was of 7.5 trillions or something like that, it has different tranches, okay? But the last would be a million of inhabitants on Mars. So that we see where the guy goes.

Leandro: In the end, if you see this, it’s evident that Elon is a small child trying to make his dream reality, and probably he has achieved it up to a point that nobody would expect that he was going to achieve it 10-20 years ago. And here we are, right? At the same time it seems like craziness, but he has also earned the right for people to believe in him, I think.

Javier: Yes, I totally agree. You also have to be very conscious that what Elon cares about is achieving this, not what the share does. The share is a means.

Leandro: Yes. The companies are a means for him to be able to finance it.

javier: Yes, and he is focused on achieving this, which is his vision of what humanity needs, and for it he goes. That’s why you have to be careful, right? And now SpaceX goes public precisely because it’s a good opportunity to raise a mountain of capital to be able to do these things.

The Tesla/SpaceX Conglomerate & The Terafab Joint Venture

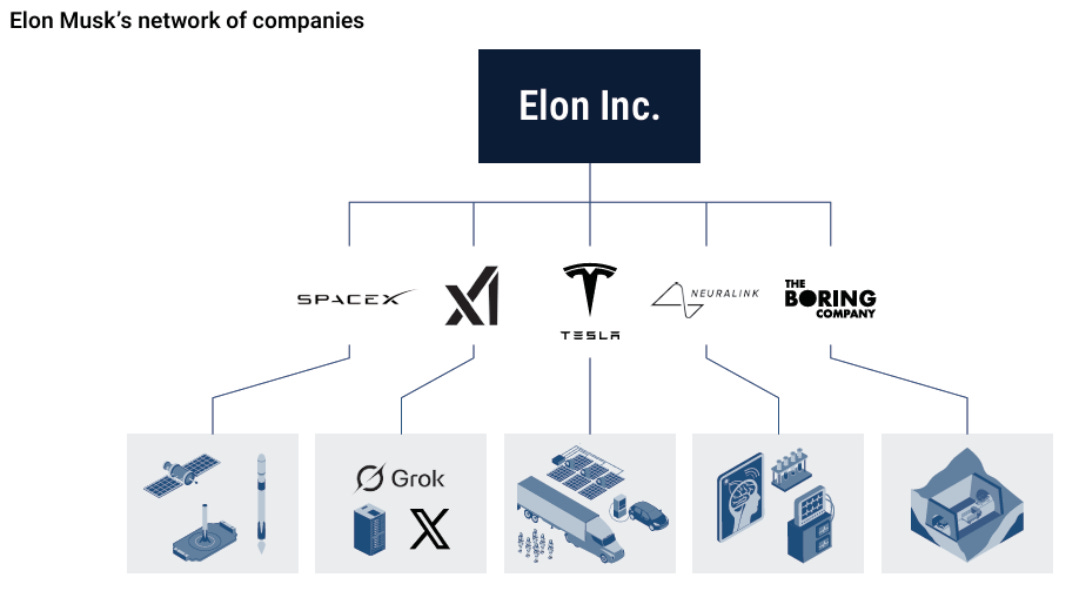

Javier: Finally, and related to the slide we have here, these are Elon’s companies:

SpaceX with xAI now together, Tesla, what we talked about before, potential to merge them both, it would make relatively quite a bit of sense. And this is also important for investors. Ah, now I remembered! Do you remember that before I told you that something I had forgotten? Now I’ll tell you. Now I have it here in the notes. So, two important things. Well, and already to also show on this slide, we have the theme of the Boring Company, which I think is not gaining much traction, but above all Neuralink. Maybe one day we have to do an episode about Neuralink, because what Elon is doing is another madness, very crazy, and they have achieved things that are spectacular already—very, very crazy at another completely different level.

Well, the case of Tesla and SpaceX and their possible union in the coming months makes a lot of sense, probably for him. In fact, it would be a way that he would be capable of having also absolute control over Tesla, doing a merger. You don’t have to discard it also in that sense, because right now he doesn’t have absolute control over Tesla. That’s why the theme of the remuneration came also, and the courts of Delaware throwing back the remuneration that the board had assigned him, and then the shareholders of Tesla to be able to have control over the company. A merger with SpaceX, given that he has a great political power in SpaceX, would be basically establishing control over the joint company. So it makes sense plus all the synergies or complementations that both can have.

And a very important thing to take into account, and what I mentioned to you before, is the theme of the Terafab that you have mentioned before yourself, and it is the new thing of Elon of wanting to be a TSMC, basically, or at least have the capacity to be vertically integrated and not depend on TSMC for the manufacture of chips. This is a joint venture, the Terafab, between SpaceX and Tesla, in which obviously already enter into conflict... you have two balance sheets, who puts the money, who has then how things are divided. Doesn’t it make sense that you merge everything so that there is no conflict of interest between the two businesses?

Leandro: In fact, I think that the fact that the possibilities of a merger have risen so much is precisely because of the Terafab—the fact that they are of the two companies and everyone has said, “Okay, well if this is the first step for everything to end up under the same roof.”

Javier: It’s just that it makes sense. That is what we have said about the capacity of control over the joint company, which right now he doesn’t have in Tesla—he has quite a bit but he doesn’t have full control. And what I wanted to mention was to all the shareholders of Tesla because I think it’s quite relevant, right? If you are a shareholder of Tesla and it’s going to merge with SpaceX, you have to consider that maybe the merger happens when SpaceX is quoting at whatever—it’s going to come out at 1.75 or at two, but it’s just that maybe in a week we are at three trillions of valuation and Tesla quotes at 1 point something, each one let them estimate what the reasonable values are for each of them. But if they merge it for you at current market prices, you have to be conscious if it interests you to be a shareholder of the conglomerate when SpaceX is valued at the valuation that it’s going to be valued at. It’s a thing also to take into account because I understand that there is a lot of people who listen to us who potentially are shareholders of Tesla and maybe see the valuation of Tesla as something reasonable and that of SpaceX not. To consider, okay?

The Cursor Acquisition & Developer Engines

Javier: The other thing is that there are thousands of things here. As you know, SpaceX or xAI have entered also into an agreement with Cursor. Cursor is an artificial intelligence code editor, to be able to acquire Cursor at a valuation of 60 billion. Already we talk here of billions as if they were peanuts, but it’s madness. Cursor basically is like the Copilot of Microsoft but for developers who know what they are doing, okay? I don’t remember what revenue Cursor had.

Okay, then, why would SpaceX want Cursor? They have arrived at an agreement in which basically SpaceX, or sorry, xAI is using Cursor. It pays Cursor I don’t know if it was a few billions a year with a penalty... with a possible payment of 10 billion if they don’t execute the purchase option at 60 billion. And at 60 billion paid in large part, I think if I remember correctly, with shares. Then, why would SpaceX want Cursor? And it is basically because if you are the provider of an infrastructure of compute for artificial intelligence, well obviously having development tools that artificial intelligence developers use...

Leandro: In the end, I think, Javi, if we think of Open AI which has Codex and in Anthropic which has Claude Code, for me those are the engines of AI right now. If you take that away from them, AI is not reporting so much to you. In the end, yes, obviously it’s a very good tool even if you don’t have the capacity to write code, but really where you are taking off is in Codex and in Code. Then, if you are Grok, the normal thing is that you want something similar for yourself.

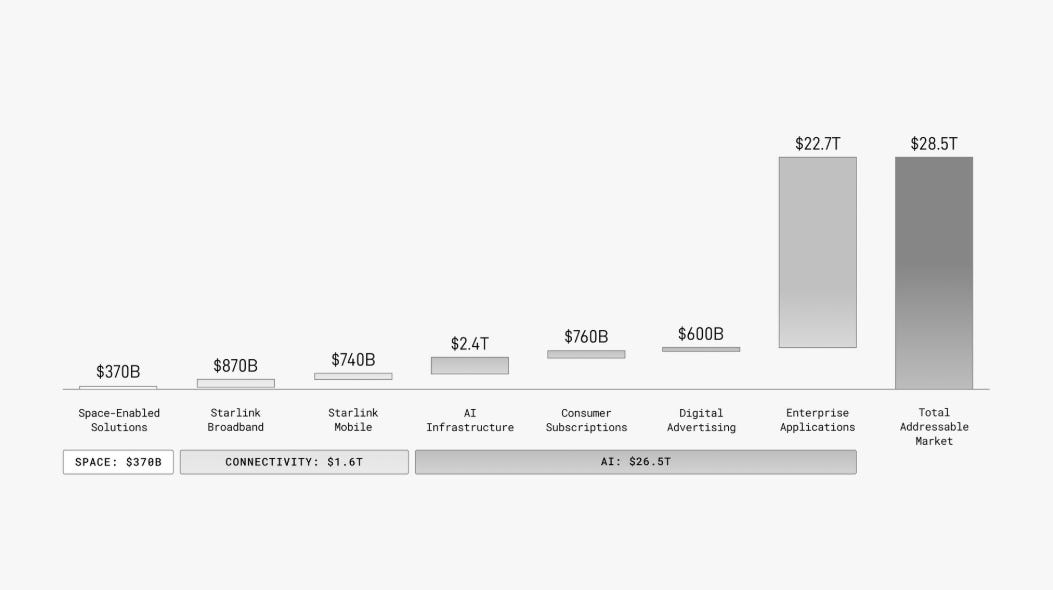

Javier: Yes. Well, I’m putting a slide here of what comes out in the S-1 of SpaceX about its TAM... so that you see it. It seems spectacular to me, and besides it has seemed very conservative to me because where is Mars?

Leandro: It seems to me evidently that it can be greater, but I don’t understand a TAM in this way. A TAM I understand it as: this is the current size and this is what I think it can grow to in the future. In the end, because the TAMs are growing, and more for a company like SpaceX, right?

Javier: I agree, the TAM should be current, and then you say that each one, but yes, simply I put it to illustrate. And as you can see, 22 trillions are from Enterprise applications.

Technical Challenges, Related Party Transactions & Cash Runways

Javier: So, I’m going to put this slide which is the last one we have to discuss the rest of things, okay? But it seems important to me so that we see where we are. We are going to talk about some things that smell bad, Leandro, okay? Some red flags. We have... I think we have mentioned almost all, but they are things that for a valuation of 2 trillions, it costs a bit. For example, we have already mentioned it: how much money is SpaceX burning annually? 9 billion in the first quarter of 2026. If things continue like this, it looks like they are going to dilute you a few times. Potentially yes.

Leandro: Yes, totally. Well, that’s one, right? You have to be conscious that the valuation in function to multiples or current fundamental realities is, quote-unquote, unreal. Simply you have to be conscious that one cannot value SpaceX—or it’s not that you can’t, but rather traditional valuation multiples cannot be taken into account to value SpaceX. It can be or not, simply it’s going to lead you to not even being able to consider it because it’s not your type of investment. Or you have to invest thinking simply that interplanetary life can generate new economies and that SpaceX can be... because it doesn’t necessarily have to be the only one, but it could be a great beneficiary of a completely new economy.

Javier: How I see it, the valuation is madness. If you take into account the current environment, yes, it’s madness. The potential market is so large that if everything goes well, the valuation could be very cheap looking at many years out too. And in the end, all the valuation... I wouldn’t say that traditional multiples can’t be used, but rather that the discounted cash flow model depends on how optimistic you are, it’s going to seem very distinct, because you are going to have very crazy growths if in the end Elon manages to make this be reality. But of course, it does seem that the current valuation leaves little margin for error for any of the big bets to fail.

Leandro: And as you have said, besides, another of the risks is that this all depends on Starship. Then in the end, you have there a point of failure. If it works all well, it unlocks many things; if not, it blocks many more things for you than unlocking.

Javier: I would say that Starship seems like it’s going to work because already it is launched, it works. Let’s see what it takes because as always, all this is very complicated engineering, but I think it will end up happening in the next few years. Then, does a demand exist to send such an amount of assets into space? That is what you have to see, right? And then if launching something is difficult, mounting a base on the Moon is much more difficult, and mounting a whole ecosystem up there is extremely hard.

Leandro: Yes. And it’s going to take many years. Then you also have to think that right now the company doesn’t generate cash. It has quite a bit of debt if we consider the revenues and not the valuation. The thing is if at some point the capital market drains a bit, you are in a tough spot because in the end, your engine for creating cash, which is Starlink, is going to have competition in the coming years. So let’s see how it maintains the rhythm of cash generation, right? In the end, it can be that temporarily the objectives are met but they take too long to be met in relation to the liquidity that you have. Evidently, he is Elon and I don’t think he has problems raising money in the capital market, but you never know. In the end, everything can go crooked.

Javier: It’s a very important point because SpaceX has 29 billion in debt that matures in 3 years. Obviously, they are going to raise 70-80 billion now, but of course they are going to burn also 40 or 50, we don’t know. So what Leandro mentioned, there can be a moment in which the capital market really dries up, and it can happen. One would always say that he’s going to be capable of raising because of what he has achieved already—he has demonstrated many things—so he is going to be capable of raising, but we’ll see at what valuations. What I do believe is that it’s very, very probable that there will be a lot of volatility and that in one or two years you are capable of buying SpaceX at another valuation very different from today’s. That would be my bet, very different.

Leandro: You mean 10 trillions, no?

Javier: Yes, and at 500 billions too. Maybe I’m mistaken, but we’ll see, right?

Leandro: These things portray why in investing you always have to do the work before the opportunity arrives. You look at SpaceX at 2 trillions, you can’t make sense of the valuation, well, there is a lot of volatility in the market. I think people aren’t conscious that if they took their portfolio and calculated the dispersion between the maximum and the minimum of the companies in their portfolio, they would be amazed at how shares move within the same year. There can be differentials for companies capitalizing more than half a trillion in the 50 to 60% every year, it’s madness, it’s madness.

Javier: We have commented already before the accounting note about research and development versus CapEx and so on. Another thing, you have to be conscious that not everything Musk touches works. We have, for example, the case of Twitter. It hasn’t worked well, despite the fact that later Elon reinvented himself a bit with the part of artificial intelligence and so on, but Twitter as such, he took it and as a business it still hasn’t taken off, so to speak. You could understand that Twitter was a whim that went wrong. These are whims that some can go out well, and many are going out well, but it can also be a whim that Elon gets infatuated with something that ends up going out poorly simply because he would like to have it.

Then there is some note, for example, related party transactions, which means transactions with interested persons of the company, okay? You have, for example, that SpaceX has bought 130 million in Tesla Cybertrucks, 500 million in Tesla Megapacks, 500 million in Tesla data bought by xAI to train Grok, sorry. Let’s see, it’s a billion and a half... that’s why we say that probably the merger between Tesla and SpaceX ends up happening because this has no... Then you have to be conscious that the fusion of SpaceX with xAI was a bailout, a very, very clear bailout, and also a capacity to put cash flow to be able to invest. You have to be conscious that this type of things can happen with Elon and can continue happening. Maybe investors in SpaceX, if Elon, for example, hadn’t merged xAI diluting the investors of SpaceX, and SpaceX went public, maybe the profitability of the investors of SpaceX would have been much higher than what it is now with xAI, potentially. Then you have to be conscious also that Elon with his universe of companies is going to do and undo a bit at his will. Later, the AI of SpaceX, Grok, has a very, very limited traction, and it is a constant expense of cash too. What is going to be the profitability of those investments? We’ll see. The bulls will say that now giving it to Anthropic is a master movement.

IPO Structures: Float Dynamics, Lockups & Index Rules

Javier: Well, what we commented on before, only 3.3% of the float is going to come out in the IPO, it’s very, very little. There are different lockups, periods in which the investors who are inside cannot sell. Elon has a year, I think, but there are other investors who have 180 days, there are different blocks.

Leandro: Isn’t it that this is going to be madness, the final lock-up?

Javier: Yes, it can be. Depending on where the price of the share is too, we’ll see, right?

The 5% of the shares go to employees and friends, families without lockup, and that means that from day 1 of the IPO there are people with shares who can sell, okay? You have to be conscious of what that 3.3% of the float means. It’s that if there is a demand of about 50-75 billion waiting, competing for that float of 50-75 billion of shares available, the price really can go to any place in the first days. But I expect to see it at three trillions. My bet is that it’s going to go to 3 trillions at some point in the coming days, and when the lockups expire between one year and 2 years, even some more I think, the float is going to multiply too.

By the way, another of the things we haven’t commented on is the change in the conditions that the indices have to be able to buy shares of SpaceX. Normally you had to wait a few months for an index to participate, these companies or a new IPO in the index. This has been changed so that indices can buy SpaceX in the days following the IPO.

Leandro: I thought you couldn’t enter into an index being a controlled company up to a point, but that can be in some European indices or something like that.

Javier: It can be. And in general, the Americans go by the float—meaning capitalization by float—but the specifications have been changed a bit to make room for SpaceX. It is what it is, okay?

Leandro: Let’s see, yes it’s true that as an index, neither can you ignore a company that has 2 trillions of capitalization because then it’s not representative of the market that is out there. That’s so. They are 2 trillions, it’s one of the largest companies in the world.

Multi-Decade Modeling Constraints & Key Man Risk

Javier: Then you have to be conscious of things like, for example, we have talked about data centers in space as a future business, but if you do a bit of mathematics, we have 10,000 active satellites and SpaceX says that it wants to reach 1 million. That requires launching obviously 990,000 additional satellites. The Falcon 9 carries about 60 Starlink satellites per launch of the small ones. With 165 launches a year, which is more or less what it’s doing, those are about 10,000 new satellites a year. To reach 1 million you need 100 years. With Starship, obviously, the cadence and the payload increase dramatically, but even so, you require launches of Starship, hundreds of launches of Starship a year sustained during a decade to reach the million this that we talk about, okay? Obviously, maybe the million, whatever.

What I am claiming is that you don’t know if the Starship 3 is going to come out within 10 years that accelerates it for you in a considerable way. You have no idea. But we are talking about decades in general in all these things, which you have to be conscious of. And if in a year what you say, the stock varies 50-60%, imagine in a decade. Be conscious. The risk of Elon, it’s not necessary even to mention it, right? I don’t even know what to say. Obviously, SpaceX has an incredible amount of engineers who surely are very good, but if something happens to Elon, we don’t know if the thing is worth the same.

Leandro: I would say that you also have to take into account that many of those engineers are there because Elon is there, because they share his vision and share the way in which he does things. If Elon is not there, many of your best engineers probably won’t be there either.

Javier: And well, Leandro, I don’t know, do you have any more things to comment regarding the red flags? Not red flags, but comments like that?

Leandro: Let’s see, I think the business right now is what it is and as we have commented, it cannot be valued with the eyes of the present and the past. Here you have to be a visionary to try to make the valuation make sense, and it can make sense if you make your estimations out to the future. But evidently if you give someone these financial statements without giving them context about Elon and about his vision, they wouldn’t pay 2 trillions. I am pretty sure about this, but of course, the business of investment is about buying profits, future cash flows, not those that are in a regulatory document.

Javier: Yesterday I listened to Ron Baron—Baron Capital, a giant fund in the United States. Ron Baron invested in SpaceX many years ago. I think he is going to buy... how much was it? A billion or something like that that he was going to participate... meaning being already an investor, he was going to buy a billion or more additional in the IPO at IPO prices, and he came out speaking. Basically there is a video on Twitter of half an hour in which Ron Baron comes out speaking and he comments a bit how Elon is and the reason that he gives to be able to invest and believe himself that the valuation is correct, for what gives you permission to participate.

Regarding the valuation, I think we have already mentioned a lot, each one has to think if it makes sense or not. And maybe if you look 30 years out, as always it matters little one trillion than two, almost, but if you don’t want to see your portfolio in 4 years... maybe in 4 years it doesn’t work well. It’s very difficult.

Emotional Capacity & Navigating Drawdowns (The Amazon Paradigm)

Leandro: I think here, Javi, enters the never-ending problem. In the end you see companies that you say, “Okay, the opportunity is enormous,” they seem expensive to you, and you say, “Well, but I prefer to wait for it to be a more reasonable valuation.” That moment may not arrive and then you stay with the face of a fool, quote-unquote. But yes it can arrive, which doesn’t mean that it’ll end up in a different place over the long term. Many people say, “No, but it matters little because then the long term you are going to end up winning.” You say, “Yes, but you have to face a drawdown...” that people say it very lightly, you have to face a 60% drawdown to know what it feels like to be in one, and then it’s not so easy. Many people when they say, “No, if you had invested in Amazon in ‘97 now you would have made 100x times whatever, okay?” Yes, but would you have held through a -90% drawdown in the dot-com bubble? Well, probably not. How many investors held from ‘97 until today Amazon? Well, probably very few. How many investors held Amazon buying it when the valuation was destroyed? Well, probably many more. I mean, in the end, I think you also have to take into account that not only is what is going to happen in the long term, but what is going to facilitate me carrying something in the long term in my portfolio, and for that conviction evidently helps.

Javier: I don’t know if it was in the interview with Ron Baron or I have seen it in some tweet from some famous investor, they mention that buying SpaceX now in the IPO is like having bought Google or Meta in their IPOs, okay? You have to be conscious. Meta came out at 100 billions and Meta, that same first year, I think it went on to a 60% drawdown. What I want to say is that one thing has nothing to do with the other, and you have to be conscious and you have to be careful because….

Leandro: Meta from May to September has a 51% drawdown after the IPO. Well, that in 5 months. The same can happen here, and it doesn’t mean that in the long term it can’t make sense. Who knows, we aren’t saying that it’s going to have it, we don’t know, each one has to... and I don’t think you have to enter into the game of, “No, but it’s just that if you are long-term, that has to matter little to you.” Each one has to know themselves and be conscious of how they manage the emotions of a significant drop. And it’s not enough to have read things about significant drops, you have to feel them. Because evidently when Meta did a minus 50 after going public, probably the narrative wasn’t the best. Then you have to take those things into account and you don’t have to let yourself be carried away also by simplistic arguments of “2 trillions is madness, you have to be an asshole to invest in this.” The two things.

The law of large numbers has been demonstrated to be a fallacy. 10 years ago someone would have said that a trillion was impossible for it to grow more, and we have Nvidia at 5 trillions. You have to be conscious which are the companies that really are capitalizing much more the advent of artificial intelligence, which are the companies that really can implement in their business models artificial intelligence much faster than any small company, etcetera. You have to be careful with simplistic narratives in general.

Industry Shifts: Value Substitution & ASML Unmapped Ocean Logic