Somebody's Wrong About Memory (NOTW#97)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

You’ll also get access to the 30+ page detailed report on the robotics industry.

The in-depth reports of Stevanato and Deere are also free to read to gauge the quality of the research.

Join today:

Both indices were down considerably this week despite (or maybe because) very strong Micron earnings. I go over all the memory debates in the market commentary despite many people believing that you can’t have an opinion if you don’t own these companies or if you are not going to feed their confirmation bias.

Without further ado, let’s get on with it.

SOON: The next in-depth report

I have just started working on the next detailed report. I can’t say with 100% confidence that the company will make it into the portfolio, but I’m 95% sure it will.

This is a set-up I have been looking for for quite a while (unsuccessfully until now!). It’s a software company that owns proprietary data that is mission critical for its customers. This means that AI is not a risk but a significant tailwind for the business. Now, what makes the setup interesting is that the company has been thrown out by the market with the SaaS narrative, meaning the risk/reward has become pretty appealing. Interestingly, the company is not well known across the investor community.

I won’t say anything else until I publish the report, which I expect to publish soon (for paid subscribers).

Articles of the week

I published one article this week: the fifth edition of “On The Radar.”

I profiled three interesting businesses:

A company that participates in the injectables supply chain with a pretty solid competitive position and great growth prospects

A software business that acts as the system of record in its industry and that owns proprietary data

A distributor with a great track record in a secularly-growing industry that has entered other attractive and high-growth markets

Without further ado, let’s see what the markets did this week.

Market Overview

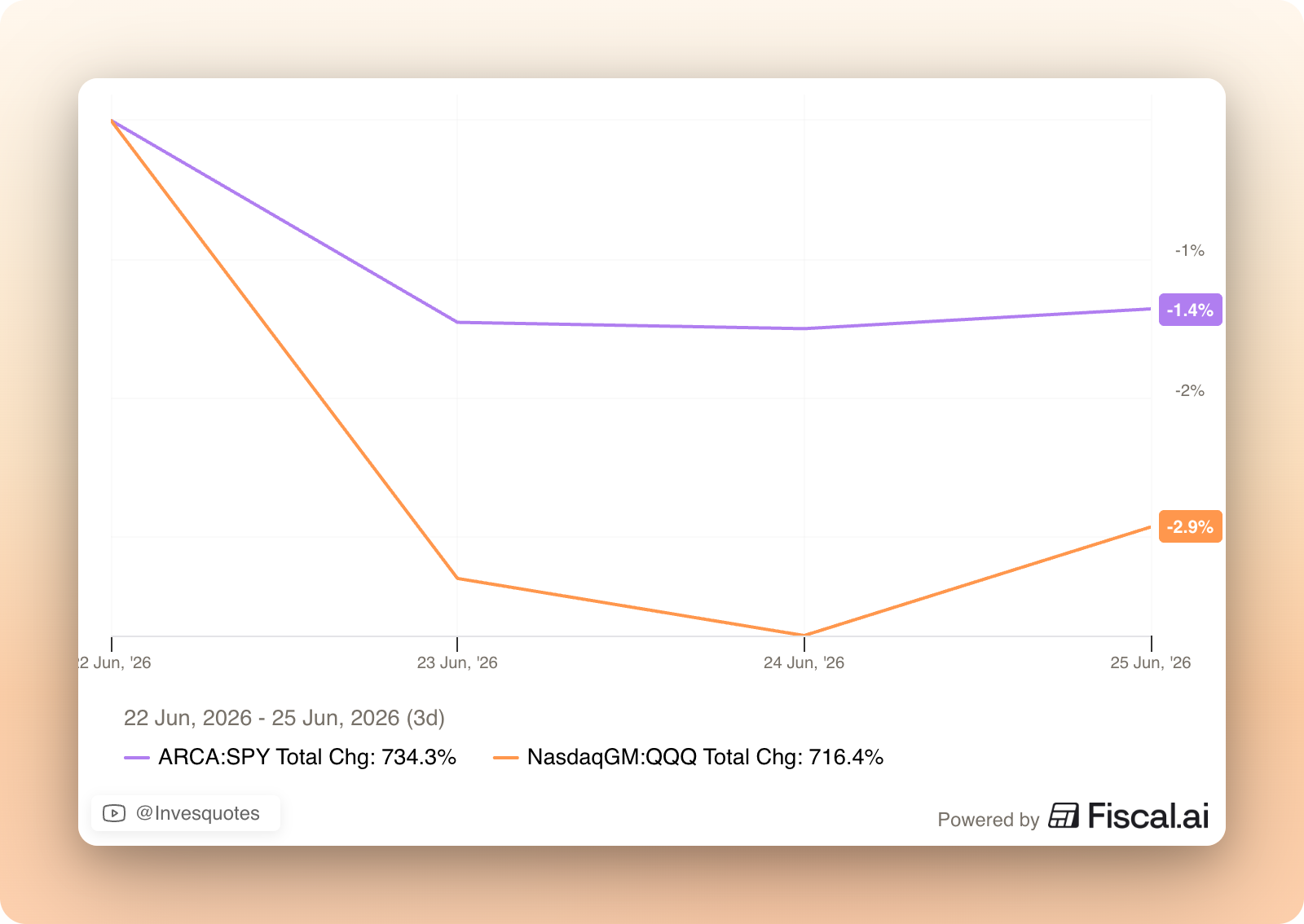

It was a very interesting week in the market. The spotlight was on Micron’s earnings on Wednesday, with everyone wondering if the AI trade was alive and well. The S&P and the Nasdaq both dropped considerably this week:

I believe that the memory situation deserves a word or two (although memory permabulls believe you can’t have an opinion if you are not invested in these businesses). So, let me first provide some context. Memory companies (Samsung, SK Hynix, and Micron) had been underinvesting in capacity for a long time because memory chip prices were low (it has historically been considered a commodity). This changed with AI, when the memory needs increased exponentially all of a sudden. With supply taking several years to come online and demand surging to unprecedented levels, memory companies are once again experiencing a supply/demand imbalance, but one that goes in their favor. What has this resulted in? Extreme pricing moves to the upside. Just for context, Micron’s gross margin has gone from the 40% range and from the company losing money operationally to 86% gross margins and 80% EBIT margins. Wow. So, in essence, memory companies have become a pretty relevant bottleneck to the AI buildout and they are surely monetizing their status.

I want to share some thoughts here. The first one that comes to mind is the market’s dilemma. While bottleneck-related stocks have been doing great lately as margins surge on the back of price increases, the stocks of hyperscalers have not done so well due to fears of them earning a subpar ROIC on their Capex. This is pretty interesting because both can’t be true at the same time. I mean, bottlenecks can’t be sustainable while hyperscalers earn a subpar ROIC on their investments because the latter will most likely pull back spending if they continue getting squeezed. So, either the ROIC that the hyperscalers earn is considerably higher than what many believe (which I must say looks likely) or the bottlenecks are not going to last long. We can even see a situation where ROIC is fine but bottlenecks don’t last for other reasons.

Regardless of whether hyperscalers are earning a decent ROIC or not, I believe that bottlenecks are (by definition) not sustainable. Or at least, they’ve not been historically, driven by the forces of capitalism and human ingenuity. Betting that a bottleneck is sustainable is betting against humanity finding a way through, which is not a bet that I would take. Interestingly, many people seem to believe that the only way that the memory bottleneck fades is if memory players expand capacity, which will take several years to arrive. Now, while this is the most likely scenario, the reality is that there are other potential scenarios worth considering, mostly revolving around politics.

Two interesting things happened this week:

Apple raised prices of certain products (not the iPhone) due to rising memory chip costs

Microsoft did the same with the Xbox

Nobody really cares about the second (who buys an Xbox anyways?) but I believe that it was a significant event because it was Satya Nadella who sent out the message. Satya is unlikely to care at this point about Xbox profitability, but he surely knows that surfacing a price hike on a consumer-facing product is likely to raise politician eyebrows. Then we got the Apple news. According to the Financial Times, Apple is lobbying the government to be able to buy DRAM from CXMT, a black-listed Chinese supplier:

I have no clue whether the company will be successful in its efforts (maybe not), but this is one of many levers that all the companies impacted by the surge in memory prices (many of which are pretty powerful) will pursue to try to bring prices down. It’s interesting because many people believe that Micron should price gouge their customers because, when they were in a downcycle, providers such as Apple were taking advantage of memory overcapacity to buy at depressed prices. So, the first thing that appears to be evident is that customer relationships between memory players and their most important customers are not the best. This is not good over the long term however you want to spin it and there’s a reason why companies like ASML and TSMC don’t price gouge their customers (and it’s not because they can’t!).

The second thing that I would say is that…if memory players are “price gouging” customers today, it seems pretty evident that their management teams believe they are still selling a commodity. If the industry had completely transformed itself and was not a commodity, then I’d imagine that memory players would be incentivized to cultivate good long term customer relationships and not make as most money as possible in a short period of time. I believe that when demand and supply balances out again (no clue if it will be demand coming down or supply coming up, or both), memory players are likely in for a rough surprise. I have no clue about when this happens, though.

While everyone is talking about supply, there are also certain things happening on the demand side. OpenAI claimed this week that the government would decide who gets access to its new models. Several months ago, I claimed that not many people were considering political issues on the demand side, and we are increasingly seeing the government meddle with the demand side. Will the government try to influence the supply side as well? Many claim today that this would be stupid and that it’s not happening, but the reality is that actions from the Pentagon might make it appear likely that it’s under consideration. Significantly higher memory prices can potentially impact the economy in two ways:

Higher inflation: this is what Microsoft and Apple are trying to surface

Lower GDP growth as the AI buildout cools down: this is what the market is implying will happen if hyperscaler ROIC is sub-par

The industry map was mixed this week, with semis/tech doing poorly and defensive industries like healthcare doing pretty well:

The XLV (healthcare ETF) has run up significantly from the lows and I believe it has significant room to run (my portfolio is positioned accordingly):

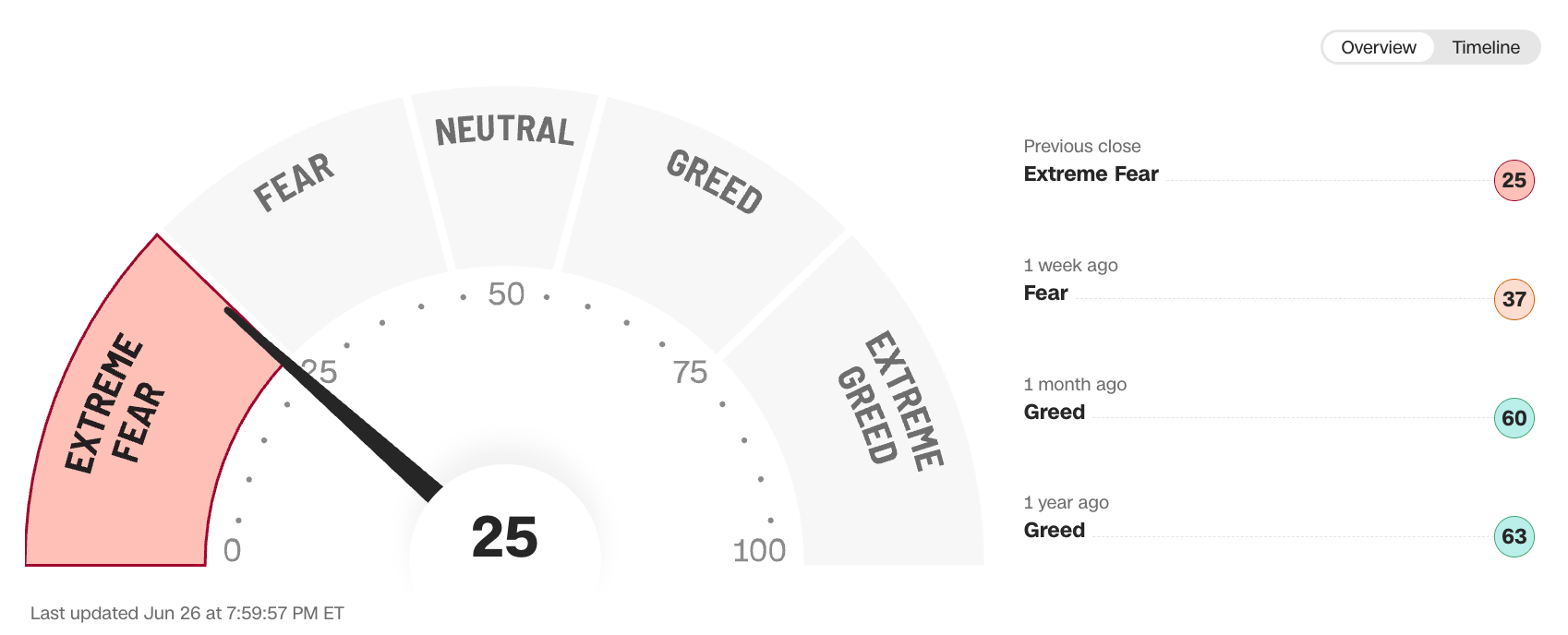

The fear and greed index dropped to extreme fear territory:

My new position

I started a new position this week. The rationale for starting the position was discussed in my recent robotics report.

Here it is: