Rosebank Industries (LON:ROSE)

A “bet” on capital allocation

Rosebank Industries PLC is a story about how serendipity is a major force in investing, more so than one could ever realize. Serendipity is defined as follows:

The occurrence and development of events by chance in a happy or beneficial way.

Even though serendipity is involved in 100% of business success stories, I am specifically referring to serendipity in the context of investment discovery. So, this begs the following question: how did I end up studying Rosebank Industries (LON:ROSE)? Maybe my impression is misplaced, but I’d say Rosebank is a relatively unknown business (thus far, nobody who I’ve spoken to about the company knew about it). I got to Rosebank in an “unconventional” way, but it was honestly a way that typically happens more often than we realize.

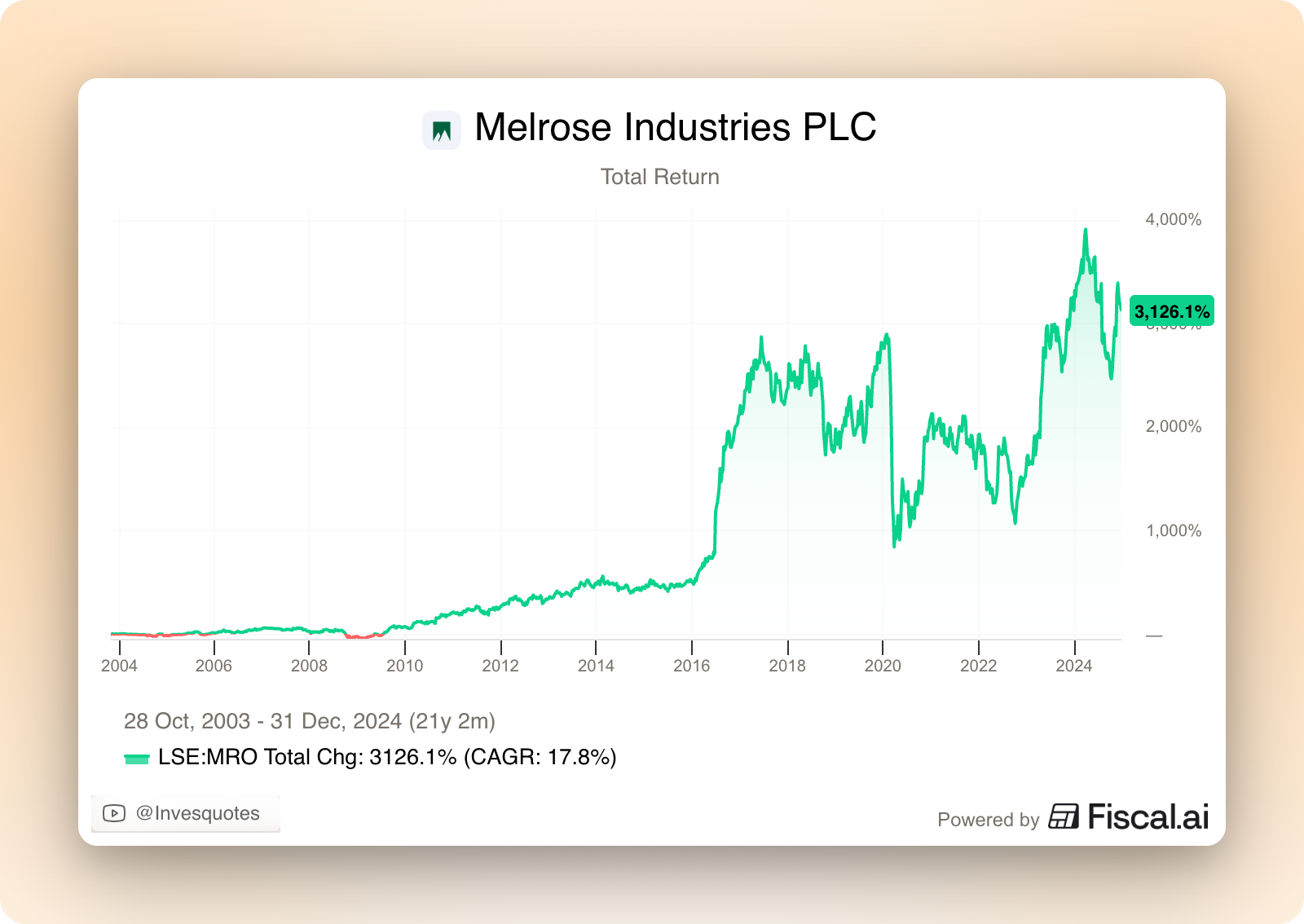

In my quest to look for appealing investments that operate in attractive industries (such as aerospace), I came across Melrose Industries (LON:MRO). Melrose Industries is a publicly traded pure-play aerospace business that looks appealing in its own right, but its history can be clearly subdivided in two phases, one of which led me to Rosebank.

Melrose was founded in 2003 by David Roper, Christopher Miller, and Simon Peckham. Even though the official slogan of Melrose’s strategy was “Buy, Improve, Sell” the reality is that this was just a “fancy” way of saying that it was a publicly-traded PE (Private Equity) vehicle. Melrose strategy was based on acquiring troubled industrial businesses, improving their operations, and selling them. The only slight difference between Melrose’s strategy and a pure-play PE strategy was arguably leverage. Melrose typically ran its acquired companies at 2x-3x leverage, which significantly trailed leverage levels set by its previous owners (who typically run them with >5x leverage). The playbook was simple yet effective:

Buy a good business for a reasonable multiple that was underperforming due to x,y,z internal reasons (i.e., find a “fixable” business)

Improve the business’ margin profile and cash conversion through operational improvements

Sell these businesses to the highest bidder 3-5 years down the line

Return capital to shareholders

Rinse and repeat

The “rinse and repeat” step is where the model differed from what we could consider a pure serial acquirer. After exiting, Melrose either deployed the funds in a new venture (if available) or returned the funds to shareholders. The strategy worked (put mildly), and both shareholders (and executives) were well off. From 2003 to 2024 (the year when Melrose’s founders departed), the stock enjoyed a total return of 3,200%, or roughly an 18% 21-year CAGR:

It’s worth noting that, besides achieving a great CAGR up until 2024, the Melrose founding team did not leave a business “starved for value”: Melrose is today a pure play aerospace business with pretty interesting future prospects (I’ll most likely write about Melrose in the coming weeks).

Despite having successfully applied its playbook since 2003, everything changed for Melrose in 2018. After having sold most of its investments (5 until that date), management set its eyes on the golden egg: GKN. GKN was a decent and (somewhat) vertically integrated automotive and aerospace business that was significantly underperforming profitability-wise. GKN was generating at the time of acquisition more than 10 billion in revenue but enjoyed slim operating margins of 6-7%. Melrose believed it would be able to significantly improve these margins and turn the business around, so they decided to pay 8.1 billion pounds, 4x Melrose’s revenue at the time.

The deal soon encountered “problems,” but these were not operational in the purest sense. They were related to GKN’s geopolitical relevance and mission-criticality. Airbus (a long standing customer of GKN) COO publicly stated that it would be “practically impossible” to award GKN new work under short-term owners. This is when Melrose’s founding team realized that, for the first time in almost 20 years, they would not be able to implement their “buy, improve, sell” strategy, at least not without encountering significant obstacles along the way. The UK government also set some limits around what could be done in terms of cost efficiency (EU-related countries are not a big fan of efficient operations, shocker).

Realizing that the GKN turnaround would only be able to be conducted by long-term owners and that this was not their expertise, the founders left Melrose in 2024 to start a new venture and Melrose became an independent pure-play aerospace business (and a relatively interesting one).