Risk/Reward vs Momentum

Deere’s Q1 2026 Earnings

The developments over the course of the past three months have strengthened our belief that 2026 marks the bottom of the current cycle, as we project mid-single-digit net sales growth for the equipment operations this fiscal year.

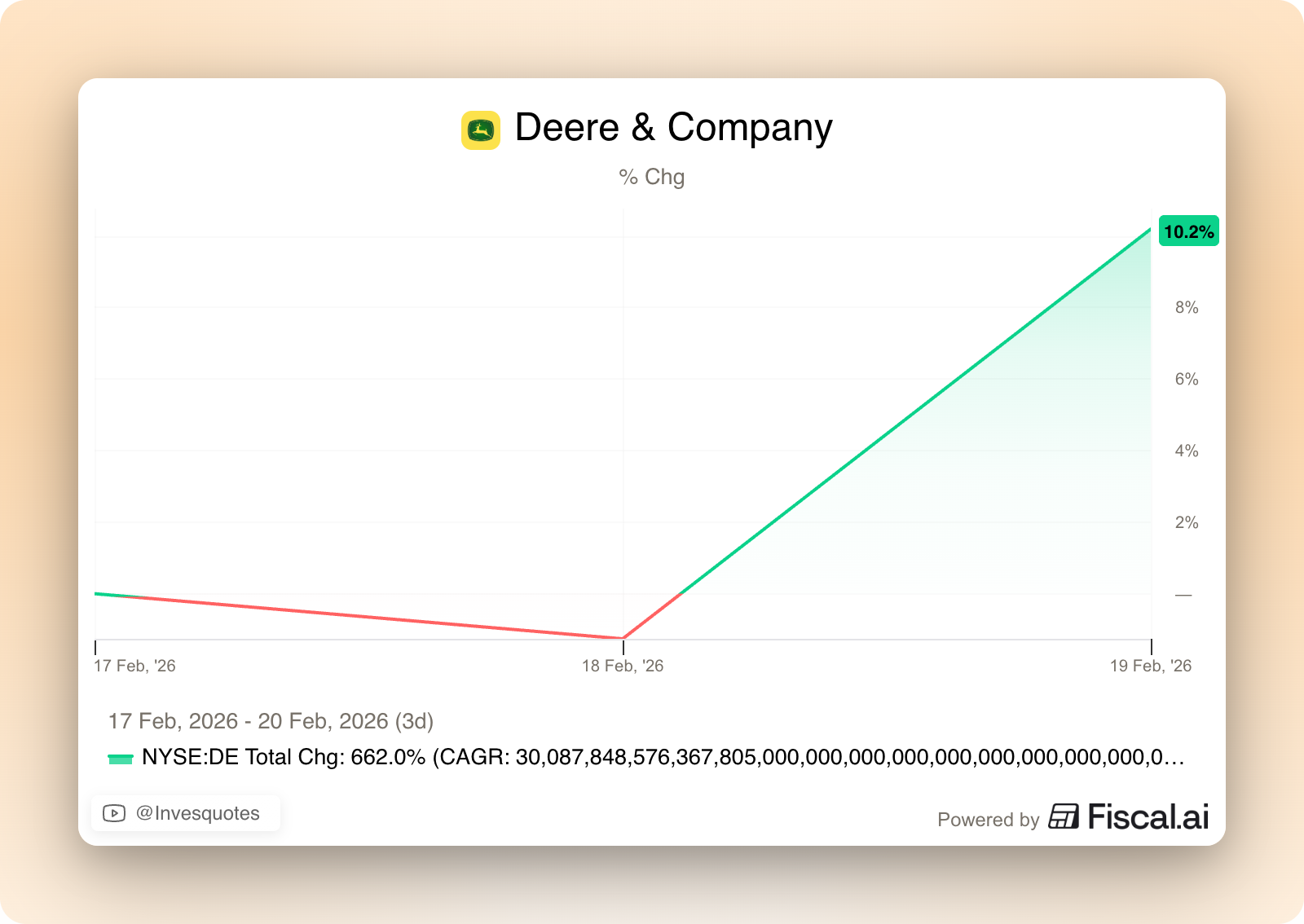

Deere reported strong Q1 2026 earnings last week. Earnings were stronger than expected and the market reacted very positively to these, sending Deere’s stock to ATHs (now up 42% for the year, yes, wow):

While I could make this article very long talking about everything the management team discussed during the call (Deere always hosts pretty long calls), I’ll try to be as brief as possible.

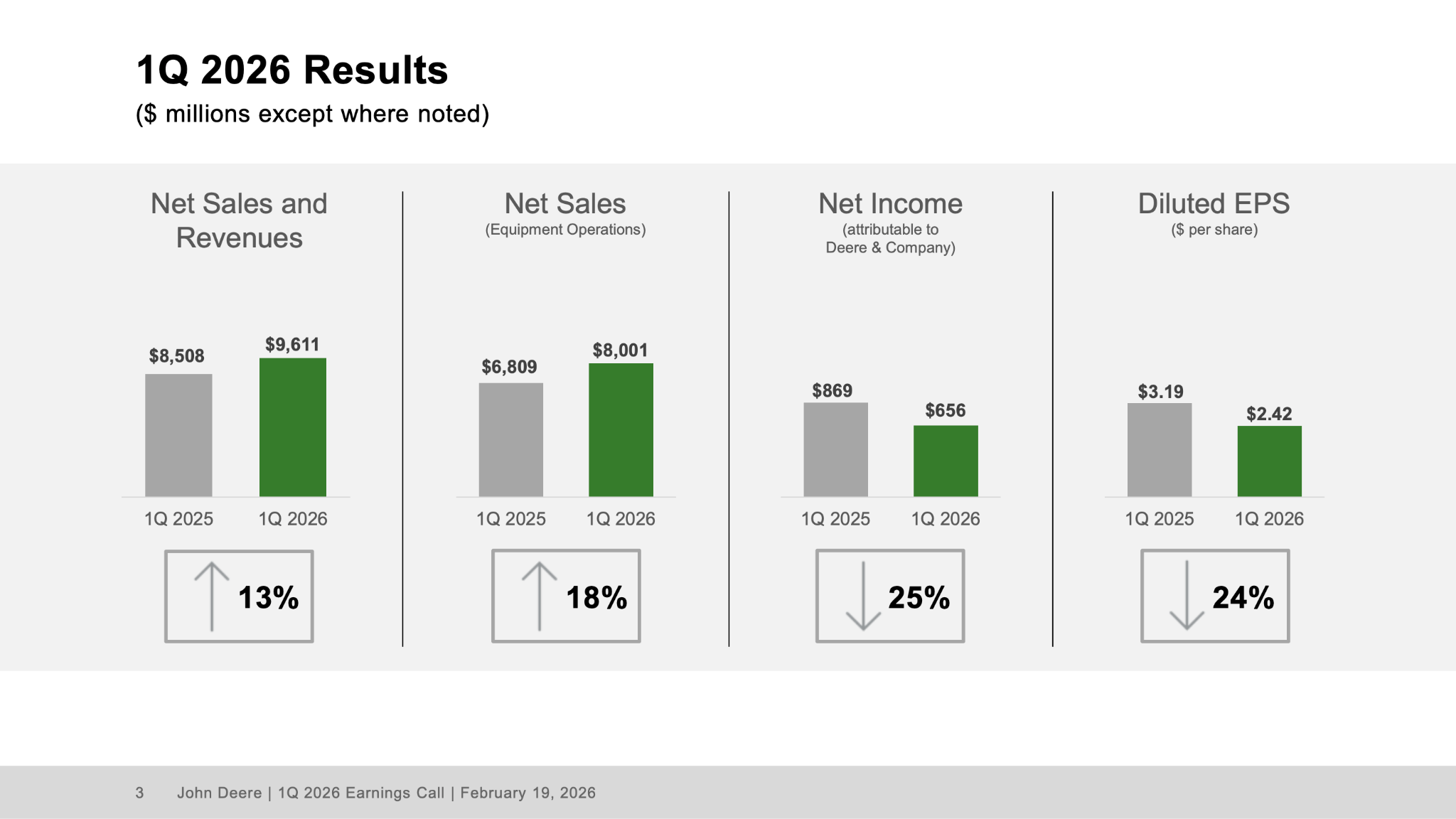

So, let’s start with Deere’s financials. Numbers came in above expectations, Deere is back to growth, and management raised the guide. What’s not to like?

Source: Deere’s Q1 2026 Earnings Presentation

Even though numbers were better than expected, they require some context. Strength was somewhat broad based across Construction (+34%) and Small Ag & Turf (+24%), but PPA (i.e., Large Ag) was a mixed bag (despite growing 3% YoY). PPA showed further signs of stabilization in the US and Canada (good news), but experienced some additional weakness in Brazil. Seeing PPA experience weakness in Brazil was somewhat of a surprise considering that the Brazilian stock market is being bid up by investors anticipating lower interest rates. Lower interest rates should (theoretically) be good for Deere as customers would be able to finance equipment purchases at a cheaper rate:

Management argued that the “weakness” stems from higher inventories and an uncertain environment:

Despite being higher than our target (inventory in Brazil), our current inventory to sales ratio for combines is still significantly lower than what we see with competitors.

Despite PPA not being back to growth in full force like the remaining segments (which also portrays that Deere is more than just Large Ag), this quarter’s performance served to reinforce management’s view that FY 2026 will mark the bottom of the large ag cycle. It also seems pretty evident that the market is now getting comfortable with this view judging by the stock’s performance. According to management, their view is supported by several green shoots:

“Our Combine Early Order Program finished better than expected, and large tractor order activity has increased.”

“Ongoing improvement in the used inventory market is providing a better environment for machine replacement, while the age of the fleet continues to grow.”

“The US fleet age is high and continues to get older as customers put more hours on their equipment. With the stabilization that we’re seeing in US ag fundamentals, along with an improving used market, our expectation is that we’ll start to see some replacement demand return.”

“Large tractor order velocity for the North American market has picked up, and our rolling order books now provide visibility into the fourth quarter.”

“We haven’t seen much replacement over the last couple of years, and you do have some folks that do need to look to replace even sort of despite what we’re seeing with ag fundamentals.”

Despite the better-than-expected performance…Deere is still below trough levels for large ag…

We’re still below trough levels for production precision ag overall, and North America below that.

Something I have discussed in prior articles is that Deere will most likely enjoy a double benefit throughout the upturn. Not only will the company benefit from higher end market demand, but might potentially from inventory build-up. The reason is that dealers have kept inventories low during the downcycle.

Our channel has consistently worked to reduce used inventory levels, and our deliberate approach to managing production and inventories set us up favorably both this year and into the next.

When I talk about Deere, I typically discuss Large Ag, but I believe we should give the Construction segment some merit this quarter. For starters, Deere now anticipates strong growth for the segment, driven among other things by AI (can Deere be considered an AI stock now?!):

Construction markets remain solid, supported by US government infrastructure spending, declining interest rates, strong rental demand, and data center construction starts.

Deere is also bringing significant innovations to market in construction. The company is launching a new excavator that (in management’s opinion) is the first differentiated product that they’ve launched in a while.

This new model gives us differentiation that we haven’t had over the past couple of years.

To this we must add the tuck-in acquisitions, like Tenna. Tenna is sort of a VMS (Vertical Market Software) for contractors to manage their jobs. Interestingly, it’s focused on mixed-fleets. I know that in the past I’ve criticized this mixed-fleet strategy claiming that it’s a sign of competitive weakness in the ag market. The reason is that farmers tend to increasingly favor single-colour fleets, whereas the landscape in construction is entirely different: mixed fleets are the norm.

Another topic worth discussing is that of tariffs (back in headlines once again…). After an unfavorable ruling from the Supreme Court, Donald Trump announced this weekend through Truth Social that the universal tariff rate would increase from 10% to 15%. Tariffs, as you might now, are a relevant cost for Deere. The company has guided for $1.2 billion in increased costs from tariffs this year, but the company is getting leaner excluding these:

Transitioning to cost management, excluding tariffs, production costs were lower year over year for all business segments in the first quarter.

This shouldn’t take us by surprise because we should already know that Deere’s margins are going to be structurally higher in the future, something with which management agrees:

As we see demand come back, I think we will see strong, strong incrementals.

We don’t know what the recent tariff tantrum will end up meaning for Deere, and although it’s likely to have an impact, I don’t think a 5% difference in the tariff rate changes the story much over the long term (especially with the cycle recovering).

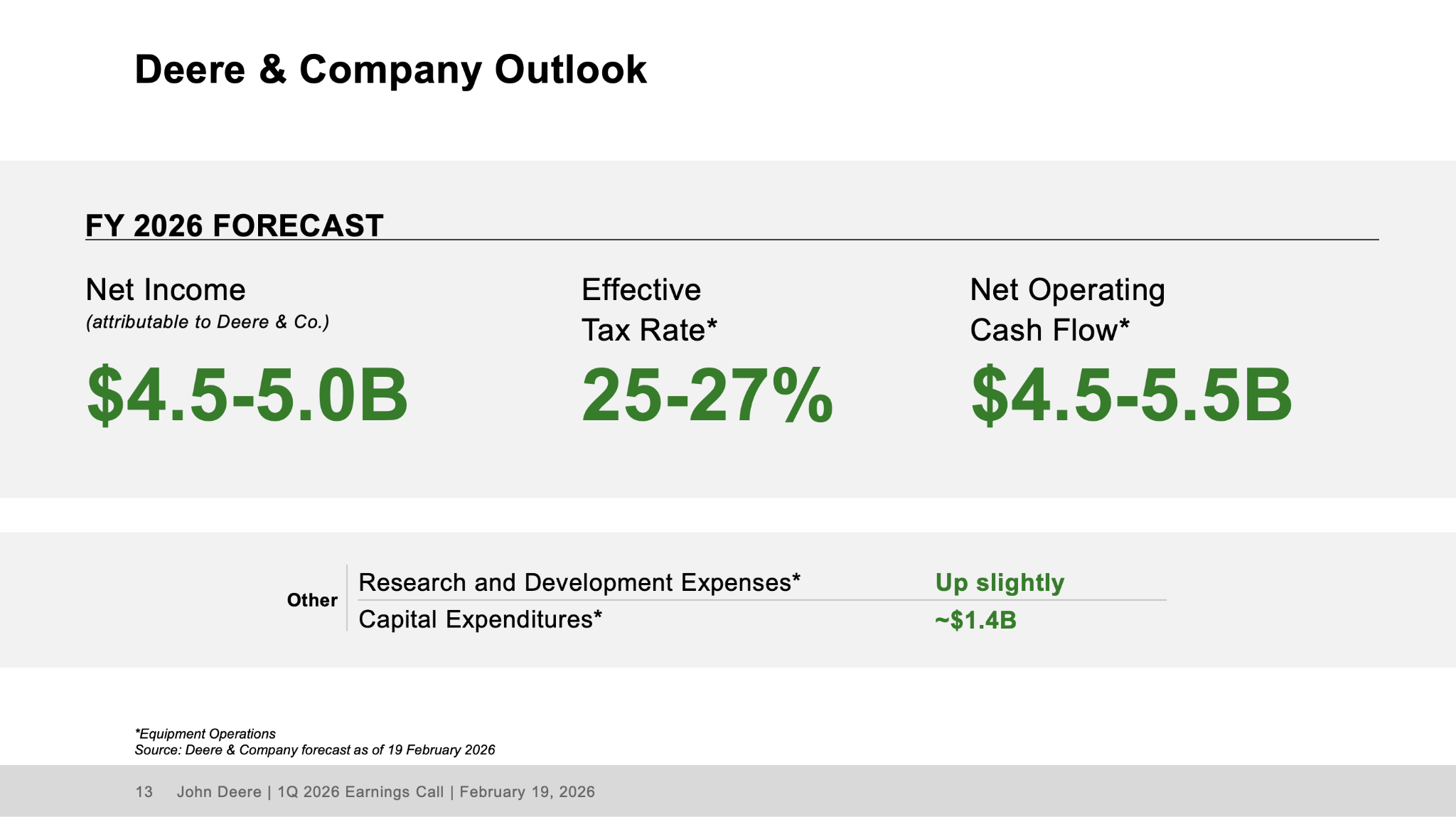

So, all in all, good earnings from Deere and great market reaction. The stock is up 40%+ this year and around 60% (29% CAGR) since I released my free in-depth report, so the question today is:

Is Deere still cheap after the run?

Let’s take a look at this.

The rest of the article is reserved for paid subscribers. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of paid subscribers today:

Is Deere still a hold after the run?

With fundamentals still not improving much (albeit likely will improve materially over the medium term), much of Deere’s stock price rise has been driven by multiple expansion. This doesn’t necessarily mean that the stock price run has been unwarranted, but we must understand (through our preferred valuation tool) whether the risk/reward is still worth it.