Optionality for the win

Keysight’s Q2 2026

I published my in-depth report on Keysight on January 2025. You can read it below if you are a paid subscriber:

Keysight reported (once again) phenomenal earnings. The objective of this article, however, is not to pat ourselves on the back about how exceptional these were (I have already done that in prior occasions). I believe that the quality of the report is apparent just looking at the headline numbers and how these fared compared to market estimates.

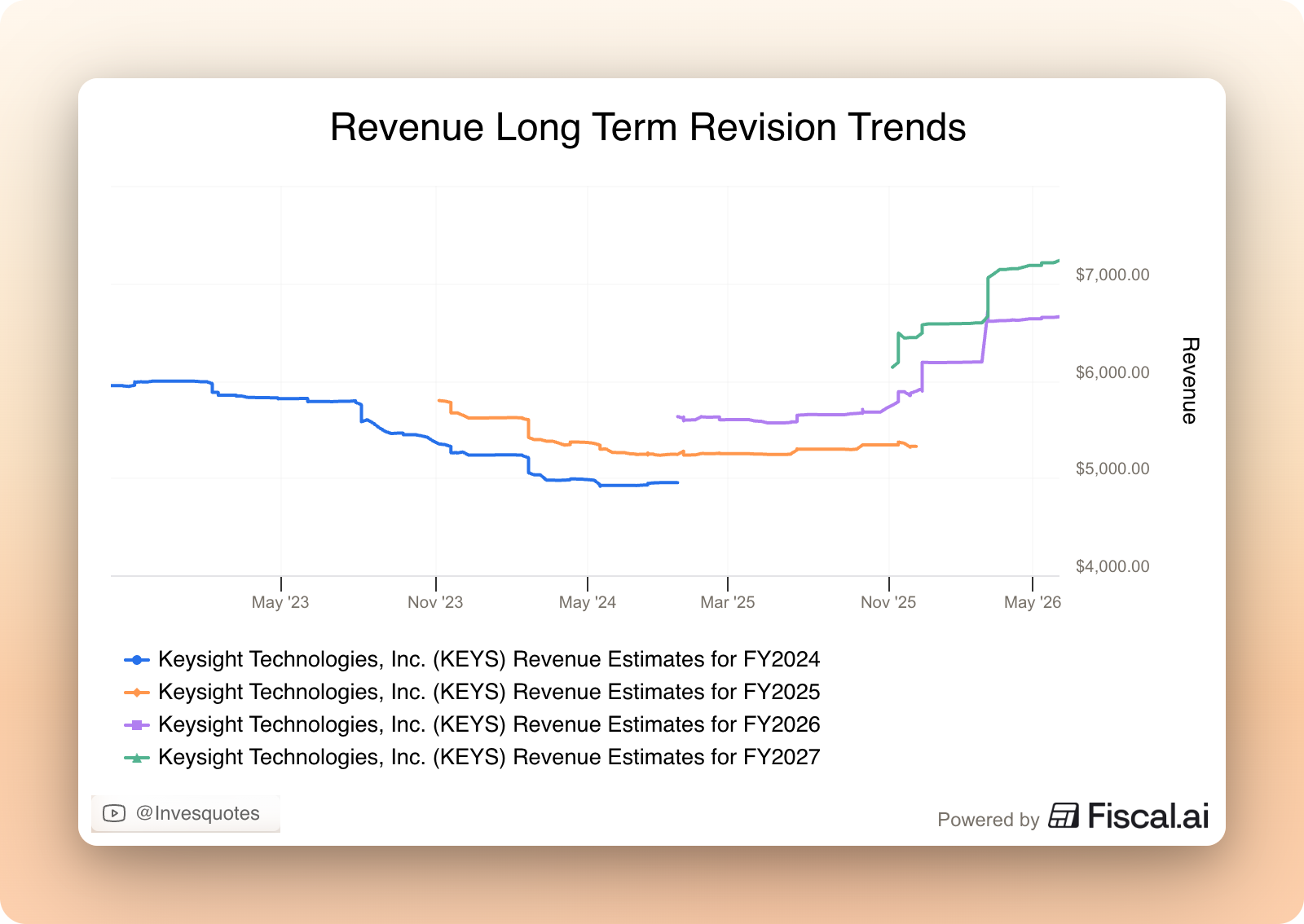

One must consider that analyst expectations have risen pretty considerably for Keysight over the past few quarters on AI-driven demand. This means that we could consider the current expectations pretty optimistic or at least updated to the current demand wave…

…which didn’t deter Keysight from beating these yet again:

Q2 revenue came in at $1.71 billion for a 0.7% beat. This was despite a $40 million revenue headwind from tariff refunds (which Keysight is likely using to pay customers back).

Q2 adjusted EPS came in at $2.67 for a 24% beat. Operating margin incrementals are incredible for Keysight and they are tough to model at these “unprecedented” revenue growth rates.

This said, the beats over already “inflated” market estimates are not what made these results impressive. Let’s take a look at orders. Despite Keysight posting 31% revenue growth in Q2 (+24% organic), management saw orders grow a whopping 56% (+48% organic). Not only are orders growing twice as fast as revenue, but management also claimed that the pace at which these orders will convert into revenue is unchanged (6 month delivery). This means that further acceleration is likely upon us.

This “sudden” AI wave has logically surfaced several concerns around sustainability and whether this is a “supercycle” that will eventually leave Keysight’s financials in dire shape once it turns around. Note that Keysight is a fixed-cost business that enjoys significant operating leverage. The company experienced operating margin incrementals of 49% in Q2, which caused an operating margin expansion of 520 basis points. There’s another side of the coin: if revenue falters going forward, decrementals are going to be significant as well. So, in short, the way up is great, but if there’s no sustainability, then the way down will be painful. There was also “good” news here (evidently one mustn’t ask a barber if he needs a haircut).

Let’s start with AI. Keysight is evidently benefiting from the AI data center buildout through its Communications Solutions segment (“CSG”). Management claimed that “momentum is accelerating” and that AI-related revenue in H1 2026 has already surpassed the levels of the entire 2025 (wow). Now, this doesn’t mean that it’s the only thing that’s working. Two examples…

Within CSG, the AI buildout is bundled in “commercial” which grew 40% YoY, BUT the aerospace, defense, and government portion of CSG also grew considerably: +24%

EISG (which also has a semi component so not entirely unrelated to AI) grew 24% YoY

The above, in my view, clearly portrays that Keysight is much more than AI. Management believes the AI trend is durable…

We look at where we stand, and we see this as a multi-year runway that’s ahead of us because of all the discussions we’re having with customers around their future plans.

…but we will only know in hindsight how durable it really is. Seeing orders growth + management qualitative comments around “accelerating momentum” surely makes it seem like a cliff is not upon us. The 6-month visibility that the order book provides led management to raise full year revenue growth expectations to “high 20s,” which honestly seems sandbagged if orders turn into revenue at the pace they expect, but that’s around a 500-800 bps raise to their expectations barely three months ago. The current AI wave (+ strong demand elsewhere) is also making management consider raising the LT growth algo of 5-7% growth:

We’ll update you on the long-term growth dynamics of the market and our ability to outperform.

To all of the above we must add potential optionality. Even though I evidently did not expect Keysight (a historically MSD/HSD grower) to be growing revenue at a 30% clip in FY 2026, the reality is that it was all part of the plan, a plan that rested on optionality.

When I released Keysight’s in-depth report, one could purchase Keysight at a reasonable valuation assuming historical growth + historical incrementals while getting the company’s vast optionality for free. The returns would’ve been fine without the optionality playing out, but in hindsight we know that some of it ended up playing out in the form of AI. Now, AI is not the only form of optionality one gets with Keysight, there are many other long-term trends like robotics, autonomous driving, quantum, satellites…Keysight is exposed to pretty much every advanced technology and therefore has latent optionality:

As we are focused on capitalizing on our early leadership in the AI data center infrastructure ecosystem, we’re equally excited by the broader set of secular growth opportunities we’re progressing, including defense technology, space, 6G, and quantum computing.

Let’s size some of the opportunities/risks. Management mentioned that AI was a $500-$600 million business for Keysight in the first half. The company generated revenue of around $3.3 billion in the first half, so despite AI’s incredible growth, it’s still around 16% of the entire company. This does seem like it’s about to become significantly larger over the coming Qs.

Now, there were other interesting nuggets around non-AI revenue sources. Let’s start with space/satellites. Space is currently less than 1% of the company’s revenue, but management believes the opportunity is significant:

We get to participate in the component part of the ecosystem and also as an expansion opportunity into the emulation side of things as things are getting more complex from a spectrum perspective. We feel very good about our early position and the growth potential looking into the future.

We’re happy to be in a position to contribute to the scaling of the constellations.

What took me by surprise, however, was quantum:

At this point, we are enabling quantum computers, more than 1k quantum computers. It’s a steady triple digit business for us.

Seems impressive that Quantum is a triple digit business (so one would suppose that $100 million+) despite the industry being still so early. Management believes the opportunity here is also significant:

We are also excited about new opportunities where you get into this hybrid compute state where you have quantum computers, you have CPUs and GPUs, really driving the next generation of computer architectures.

So, the bottom line is that…not only does the AI trend seem durable for the time being, but also that something might come in the future that will substitute AI if and when its participation in growth diminishes.