NOTW #6: Factor Rotation And Why It's Noise For Long-Term Investors

Hi reader,

Both indices were down over the last two weeks, the Nasdaq significantly more than the S&P 500. I discuss what most people are attributing this “poor” performance to and share why I don’t think it’s really relevant for long-term investors. If anything, I’d go as far as to say that it might even be positive.

Before jumping into the market overview, let me share this week’s articles.

Articles of the week

I published two articles this week, one for free and another one for paid subscribers. In the free article I explained why I sold Five Below and the lessons learned from that investment.

Why I Am Selling Five Below

Hi reader, Five Below (one of the positions in my portfolio) shared pretty important news yesterday, which not only had implications for its financials but also the investment thesis as such. The most…

I obviously think the stock is less risky after the drop, but there’s no denying that the thesis has changed. Five Below is now more of a turnaround story than a growth story, and I think I should move along.

The second article of the week (exclusive for paid subscribers) was ASML’s earnings digest. The company reported great earnings, but the stock reacted badly due to rumors of more restrictive export restrictions to China (yes, again).

ASML's Q2 2024: Orders, China, and High-NA EUV

Hi reader and welcome back to another post, ASML reported its Q2 earnings this week on Wednesday and they were good despite the market’s reaction… The truth is that the stock probably reacted the way it did due to reasons different than earnings,

If you want to have access to all the content, don’t hesitate to upgrade your subscription:

Market overview

The indices were significantly down over the last two weeks, especially the Nasdaq, which was down more than 4%:

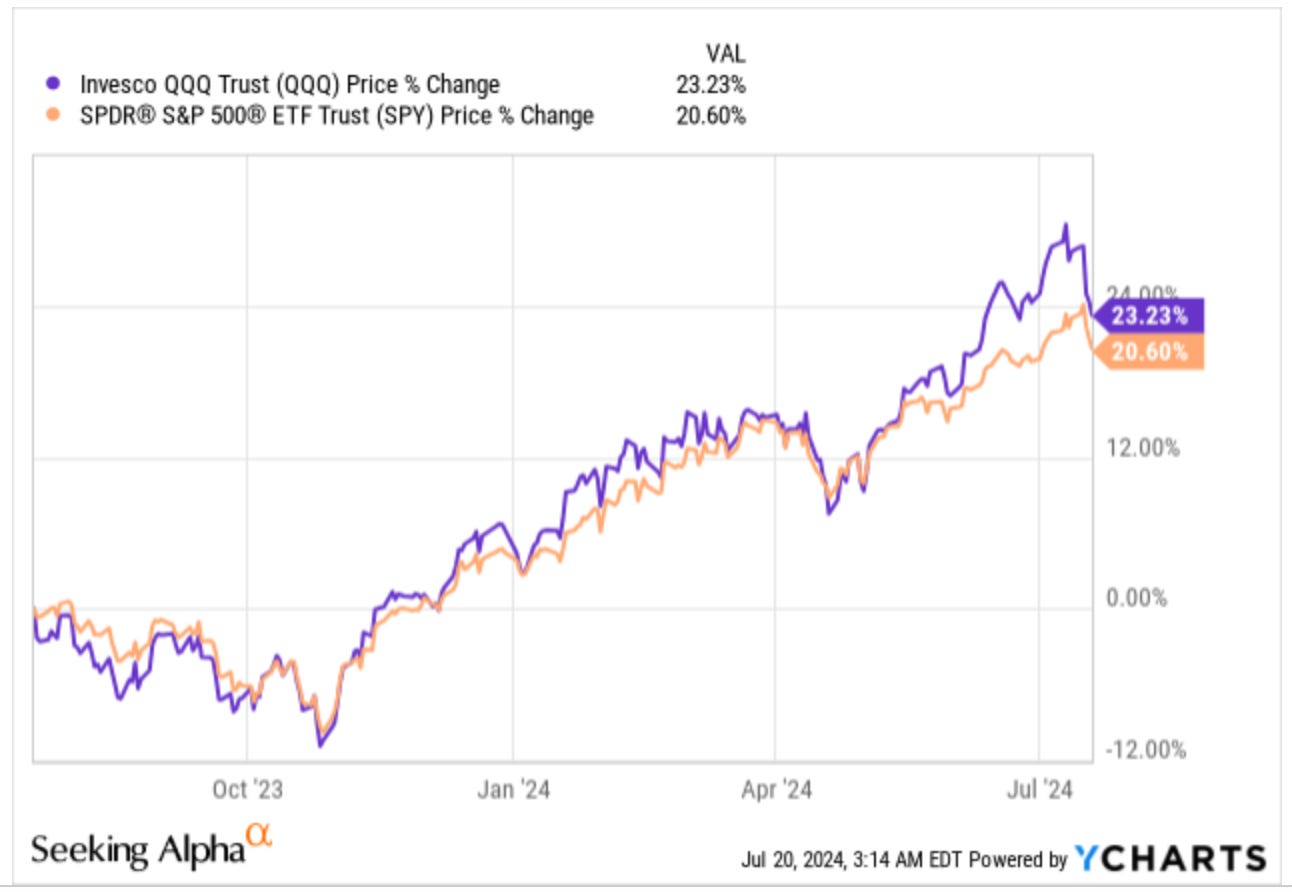

I don’t know the reason behind these drops, but it might just be a correction after their great performance over the last months. Let’s not forget that if we zoom out we can see the Nasdaq is still up a whopping 23% over the past year and 16% year to date:

Some people are trying to explain the Nasdaq's decrease and its divergence from the S&P 500 with something known as factor rotation. According to these people, big technology companies are falling out of favor with investors, who, in turn, are allocating their money to other sectors. There’s no denying that this seems indeed the case when one looks at the performance of the different sectors over the last couple of weeks.

This said, I don’t think factor rotations should matter much for long-term investors, although there’s no denying that these periods can offer interesting opportunities to add to existing positions. It shouldn’t matter much for long-term investors because Free Cash Flow per Share growth doesn’t really care about factor rotation. This metric will most likely move stocks over the long run, irrespective of the factor rotations along the way. There seems to be an ongoing obsession with many market participants who want to always be on the “right” side of the market. This strategy appears somewhat delusional, but it’s great for those investors who don’t care about always being right as long as they are more right than wrong over the long term. The ability to withstand being wrong is a great trait, and it’s not present in the average investor.

I wish I could tell you that I know for sure that a factor rotation is taking place and that we must go all in small and mid-caps because they are going to start to beat everything that’s out there, but the reality is that I have no clue. I do know, though, that factor rotations can potentially create opportunities to add to great companies at attractive prices.

By the way, I would always caution against the predictive power of something in financial markets when practically everyone thinks it’ll happen. I mean, many people believed that Nvidia was overvalued a year ago (the rest is history), and many have been claiming for three years that a recession would eventually come (the rest is also history, but they’ll eventually be right).

One of the most challenging parts about financial markets is that investors are constantly “thrown” hundreds (if not thousands) of irrelevant data points every day with the only goal of distracting them from what really matters. If you have conviction about a company growing its earnings power over the long term, it’s unlikely that factor rotations, recessions, and the like will matter much. We have to see the bright spot, though: this noise creates opportunities that those with conviction can act on. Short-term prices move based on demand (as supply is somewhat fixed), and demand is almost entirely emotional. So when someone tells you that the market is always purely rational, I’d take the under on that one.

The obsession of most market participants with winning at all times and the impossibility of doing so is probably the main reason for this irrationality. In short, even the best businesses go through periods when not many people want to own them until “skies are clearer.” The only problem with this strategy is that when “skies are clear,” the stock price would probably already be breaching ATHs (all-time highs).

Consistent with the factor rotation theory, most technology-related sectors were down this week, whereas the rest of the market was green. This also explains the significant divergence between the Nasdaq’s and the S&P 500’s returns…

The fear and greed index remained in neutral territory: