No signs of AI (at least not yet)

Topicus' Q4 and FY 2025

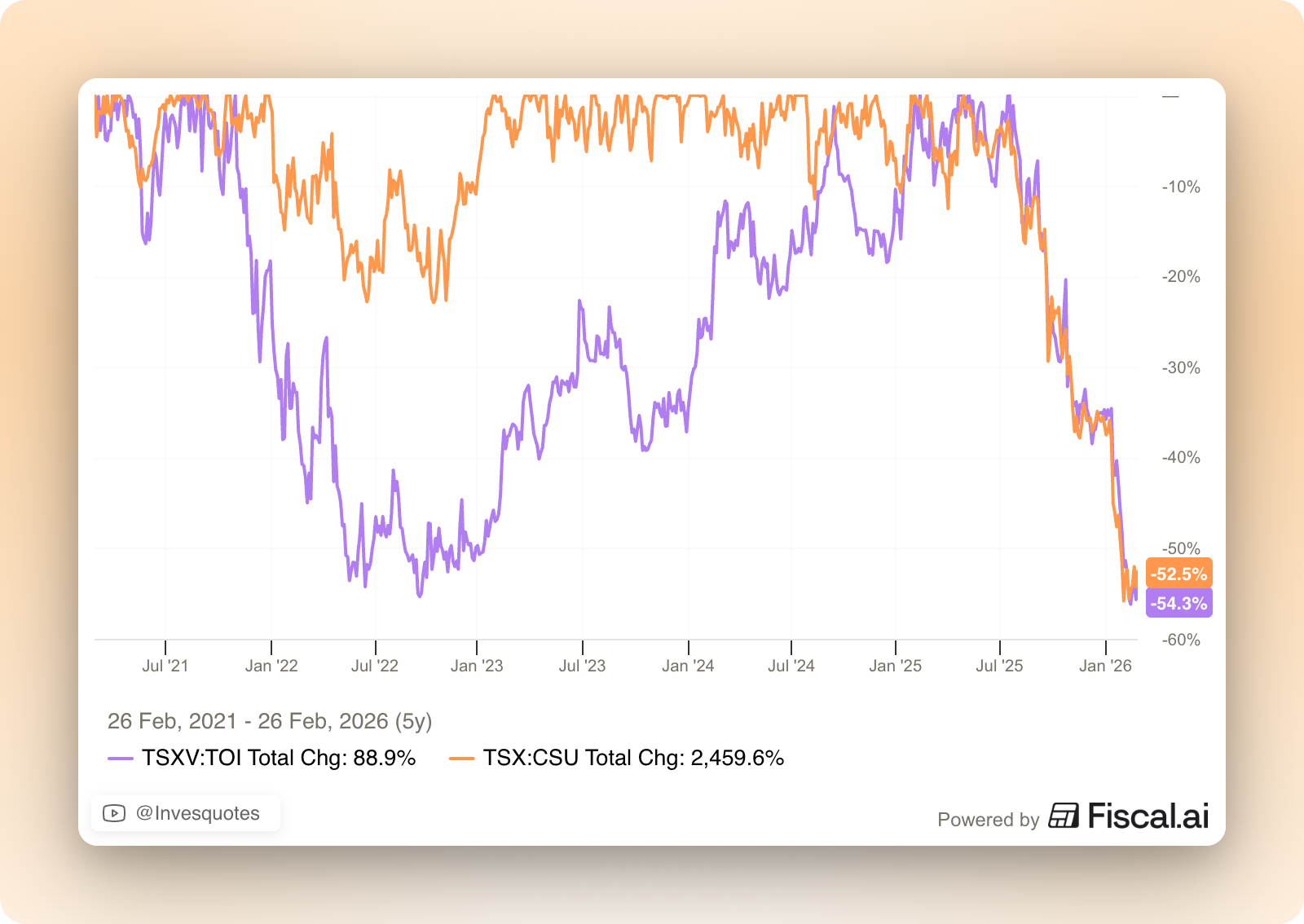

Topicus reported its Q4 and FY 2025 earnings yesterday. Earnings, both for Topicus and Constellation, are in focus not only because their stocks (Constellation in particular) are undergoing significant and unprecedented drawdowns, but because they have been caught up in all of the AI-narrative that’s impacting the software industry:

As far as I know, Topicus’ “earnings call” will most likely be bundled with Constellation’s in a couple of weeks. I’ll go over the numbers (both quarterly and yearly) in this article and will also share several interesting tidbits that might portray that Topicus is not suffering from AI (at least not yet!). I acknowledge the AI-narrative is more of a long-term one than one that would already be evident in the financials, but investors must start to monitor the leading indicators.

The numbers

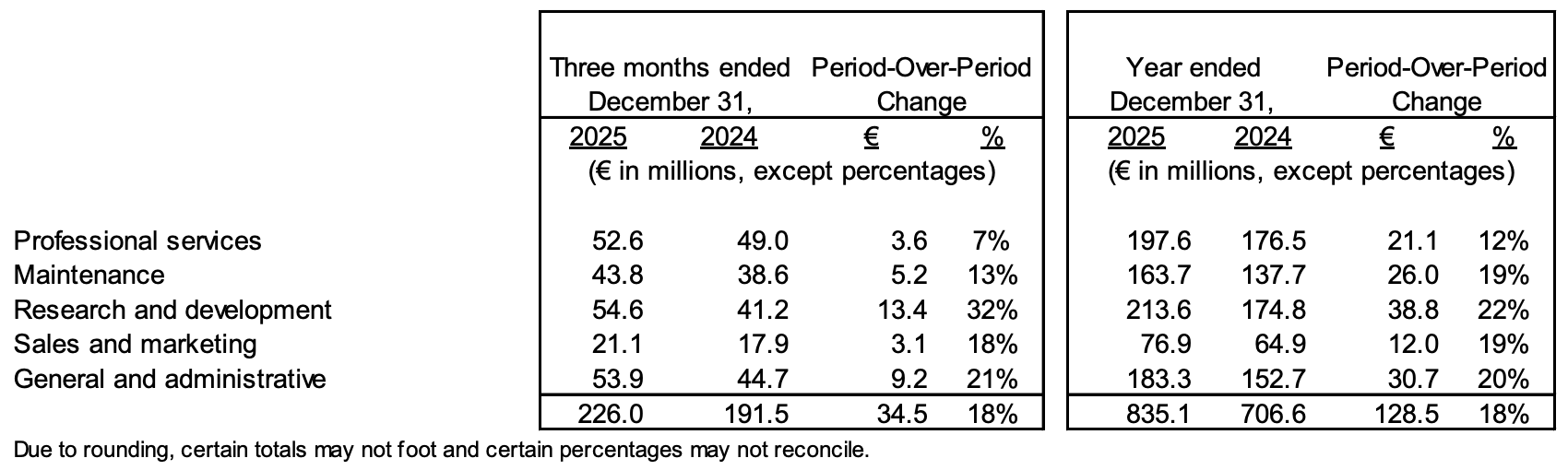

Numbers-wise, Topicus reported a very solid quarter. Revenue both in Q4 and FY 2025 grew 20% year over year. Expenses grew more on less in line with revenue during the full year and slightly ahead during the fourth quarter:

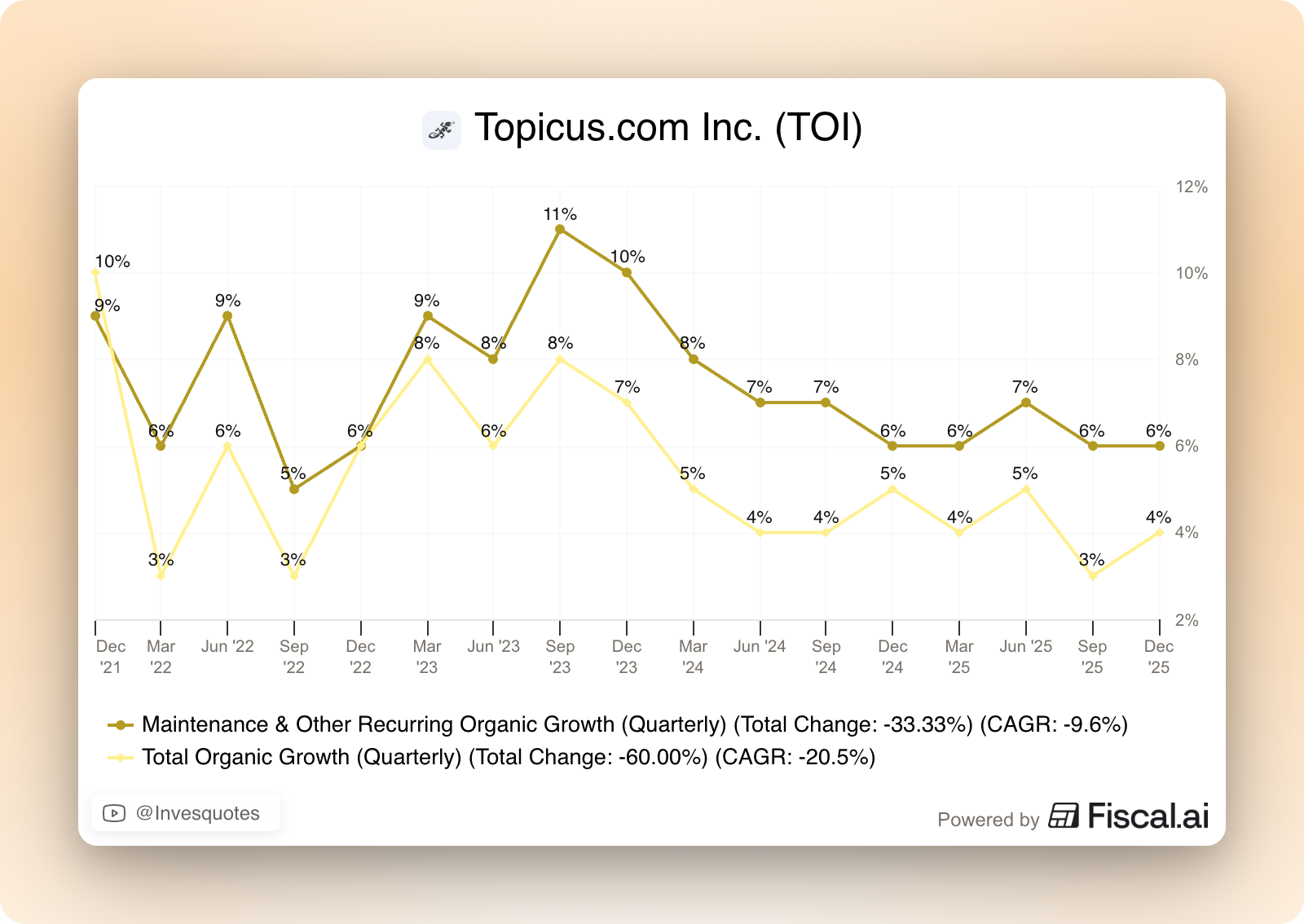

Organic growth was not mouthwatering, but not catastrophic either. Total organic growth was 4% both for the year and the quarter, but maintenance and other recurring organic growth was 6% for both periods. 6% might not sound like much, but it definitely doesn’t break the pre-AI narrative trend:

Does the above mean that Topicus is entirely safe from the AI threat? No, not really, but at least it demonstrates that, for the time being, AI is not having a significant impact (I’ll take it?).

Earnings Before Taxes grew nicely (+29% YoY) during the quarter but saw a 41% decrease during the year. The yearly number is pretty misleading because Topicus is now accounting for its Asseco investment using the equity method. This has resulted in an adjustment to the P&L that drove a non-cash expense of €221.7 million in 2025. Did you need yet another reason to not focus on the P/E (besides amortization of intangibles)? Well, here you have it.

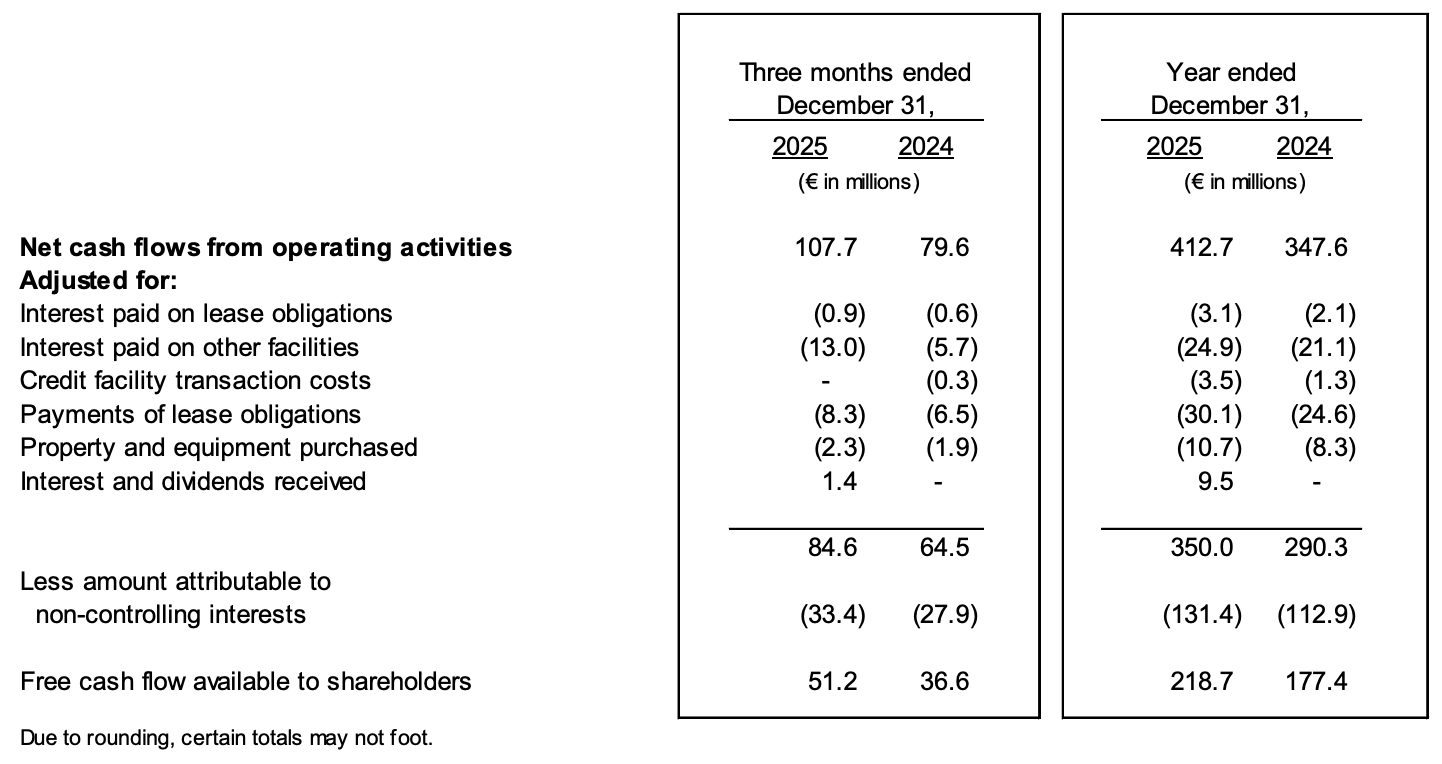

Yearly cash flows painted a different story than P&L figures. CFO grew 19% in 2025 and Free Cash Flow Available to shareholders (FCFA2S) grew 23%. Note that FCFA2S is a “cleaner” number for Topicus than it is for Constellation because there’s no IRGA (for a detailed explanation of this, read this article):

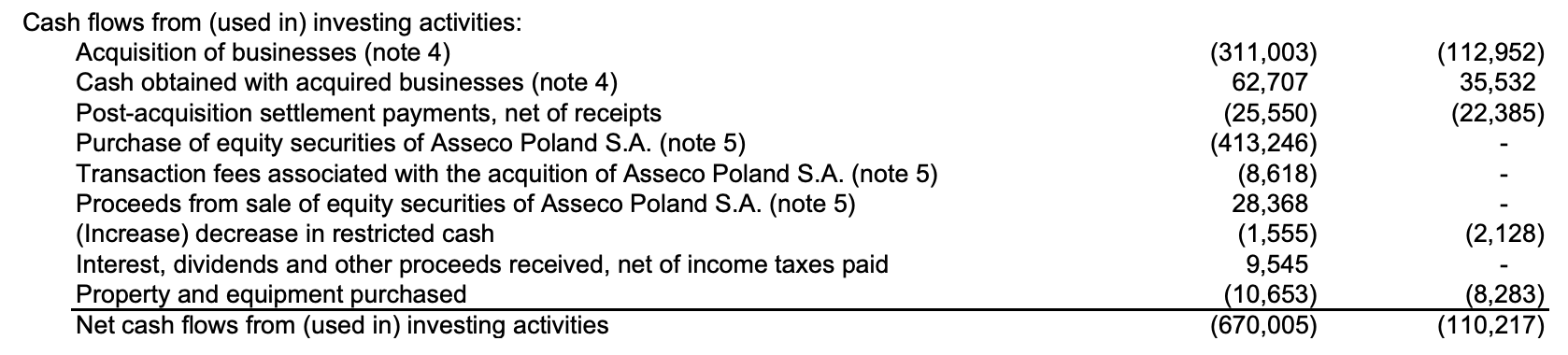

Capital deployment was undoubtedly the highlight. It was the strongest year on record for Topicus in terms of capital deployment (and by a wide margin). Between Asseco and other acquisitions, Topicus deployed €662 million of capital (net of cash acquired):

Just for context, this number last year was €77 million last year. This year’s capital deployment is equivalent to 3 times this year’s FCFA2S. It seems pretty obvious that Topicus is not short of opportunities to deploy capital (and this is the reason why I currently weigh it above CSU, among other things).

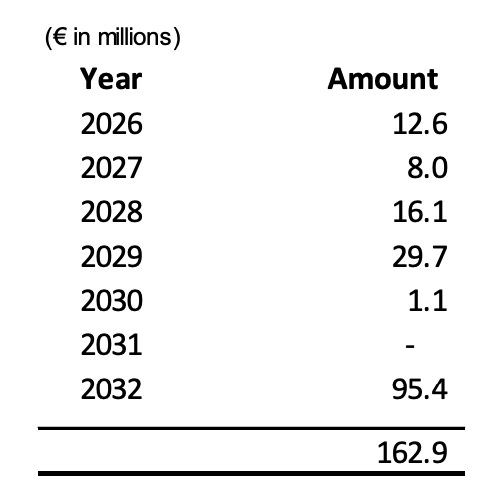

There is even more good news on the capital deployment front: there’s still significant dry powder to continue deploying capital into acquisitions. Topicus ended the year with €366 million in net debt, equivalent to a leverage ratio of 1x operating cash flow. To this we must add that debt maturity is not significant until at least 2032, meaning that Topicus can potentially lever up more to acquire companies should it need to:

This comes at a time when PE (Private Equity) might be looking for exits, which for software are unlikely to be realized at the most favorable valuations. According to Allianz, PE distributions grew significantly in 2025 but these were concentrated in large deals, “leaving the mid market stagnant.” The mid and small cap market is potentially where Topicus will benefit from, and there are reasons to believe it can’t remain stagnant for long: PE holding periods have lengthened somewhat while investor pressure to get capital back is only intensifying. All in all, it seems like an ideal environment for a company like Topicus to continue deploying capital: somewhat “desperate” sellers and no capital constraints. What’s not to like?

Now, this said, as with any diligent capital allocator, we shouldn’t count on a smooth capital deployment cycle. Topicus will deploy capital opportunistically, and this will result in lumpiness. I remember as if it were literally two years ago (oh wait, it was) that Topicus was heavily criticized for paying a special dividend when cash was accumulating on the balance sheet. How the tables have turned this year!

The AI narrative: some interesting tidbits

I evidently know that whether the AI narrative will bear fruit or not will only be apparent in hindsight. Still, I found several interesting tidbits in Topicus’ earnings that I believe are worth discussing. Let’s take a look at these.

Staff expenses show an interesting (new) trend?

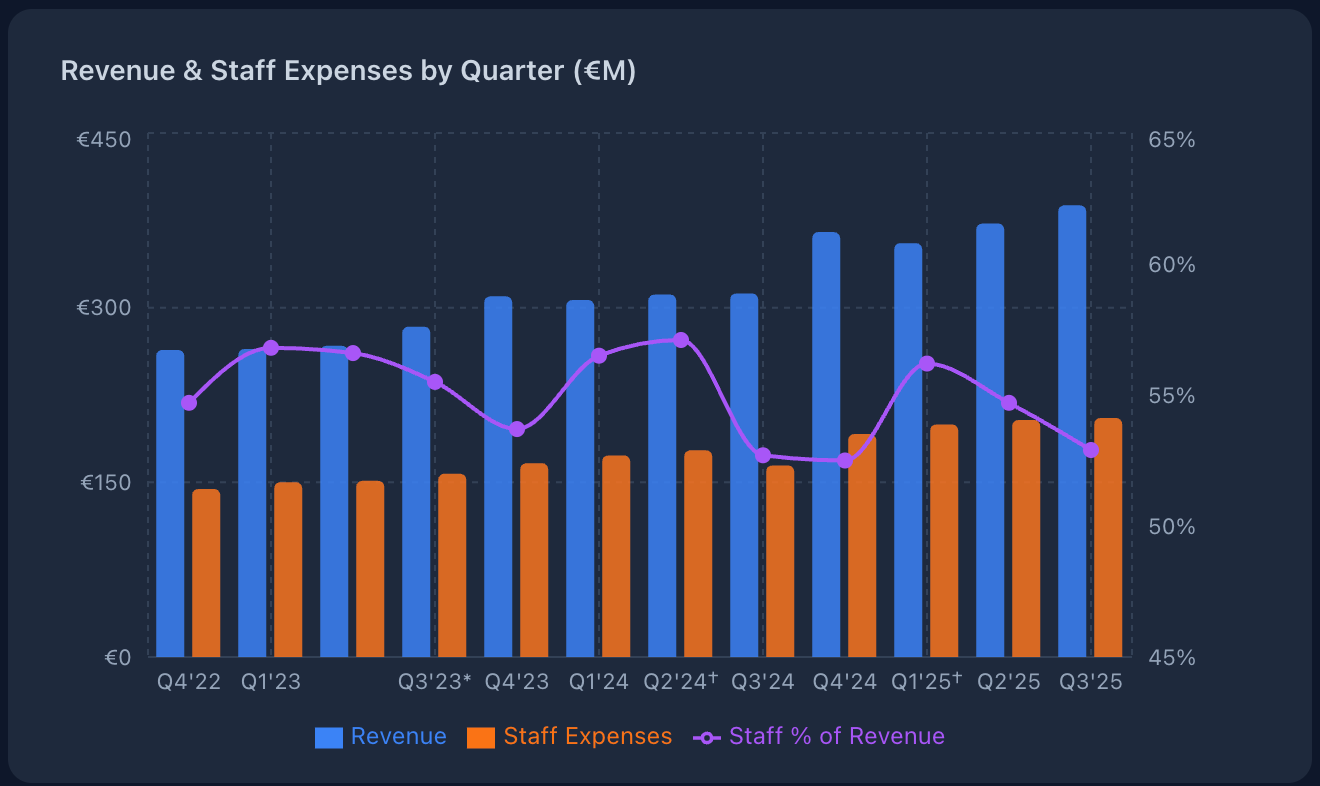

Staff expenses showed some interesting dynamics. Topicus’ revenue grew ahead of its staff expenses, but within these staff expenses, R&D staff expenses grew considerably faster than the rest:

One data point does not make a trend, but it’s nonetheless interesting that staff as a % of revenue has decreased throughout the entire year (it was even lower at 52% this Q) despite the year being a strong one in terms of capital deployment. It’s true, though, that staff expenses as a % of revenue tend to be highest in Q1 (maybe to do bonus payments), but nonetheless it’s something worth monitoring:

Acquisitions tend to come with a significant number of employees, making Topicus less (not more) efficient. So, what are some potential explanations for both numbers? Who knows, it might be related to AI. Seeing Topicus become more efficient throughout a high capital deployment phase and while significantly increasing R&D resources is pretty interesting, but I’ll leave it open to your interpretation.

Contingent considerations and impairments not showing cracks (yet)

A leading indicator that we can look at to understand whether AI is having an impact on Topicus’ business is the relationship between contingent considerations and impairments. We must be aware of certain caveats, though. For starters, contingent considerations are not applied to all acquisitions. Secondly, for the multiples that Topicus pays for its businesses, we are unlikely to see significant impairments resulting from long-term concerns (i.e., acquisitions are not as sensible to long-term outcomes).

Now, all this said, I believe it’s still positive to see that contingent considerations grew in 2025 and impairments slightly diminished. If AI is wrecking (or expected to) havoc across Topicus, I would expect to see different readings in these metrics.

Nobody knows how the future will unfold, but what one can do is objectively try to understand how AI will impact this business and find ways to monitor it to the best of our abilities.

Topicus looks pretty cheap (and what I think about the AI risk)

I lastly wanted to touch on the topic of valuation. Topicus’s stock has dropped considerably from ATHs but the business is doing as good as ever, so what happened? The first thing that happened is that the AI narrative took hold of software stocks, in some cases more warranted than others. The other thing is that Topicus was trading at a somewhat rich valuation at ATHs. But, what about now?