Momentum (and why it hurts) (NOTW#89)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

It was an interesting week in the markets as momentum continued to drive certain pockets of the market. I explain what I mean by this and give some thoughts about it in the market commentary. It was also an intense week content-wise.

Without further ado, let’s get on with it.

Articles of the week

I published several articles this week. The first one was an article on a fairly unknown company, Rosebank Industries.

Rosebank Industries (LON:ROSE)

Rosebank Industries PLC is a story about how serendipity is a major force in investing, more so than one could ever realize. Serendipity is defined as follows:

I explained where the company comes from (key to understand where it’s going), what it does, the investment thesis, and the valuation. It’s a pretty interesting business with a proven “track record” despite being newly formed.

The second article of the week was Danaher’s earnings digest.

Constructive but not there yet

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

The stock fell after reporting what appeared to be “meh” earnings.

The third article of the week was the second edition of “On The Radar.”

On The Radar #2

Welcome to the second issue of “On The Radar.” If you want to know what this series is all about, I recommend reading the first issue where I shared a detailed explanation. In the first issue I share the following three businesses:

I profile three interesting businesses, one in the resources industry, a nordic serial acquirer, and a testing business that I have started to look more in-depth (as it looks pretty interesting, it’s cheap, and run by an outsider).

Finally, the fourth article of the week was Medpace’s earnings digest.

Understanding Medpace’s business

(Medpace is a company I profiled in May of 2025. You can read the in-depth report here)

The stock dropped significantly again after a very strong earnings report (it’s been two times in a row that this has happened). I try to explain why many misunderstand Medpace’s leading indicators.

Without further ado, let’s see what the markets did this week.

Market Overview

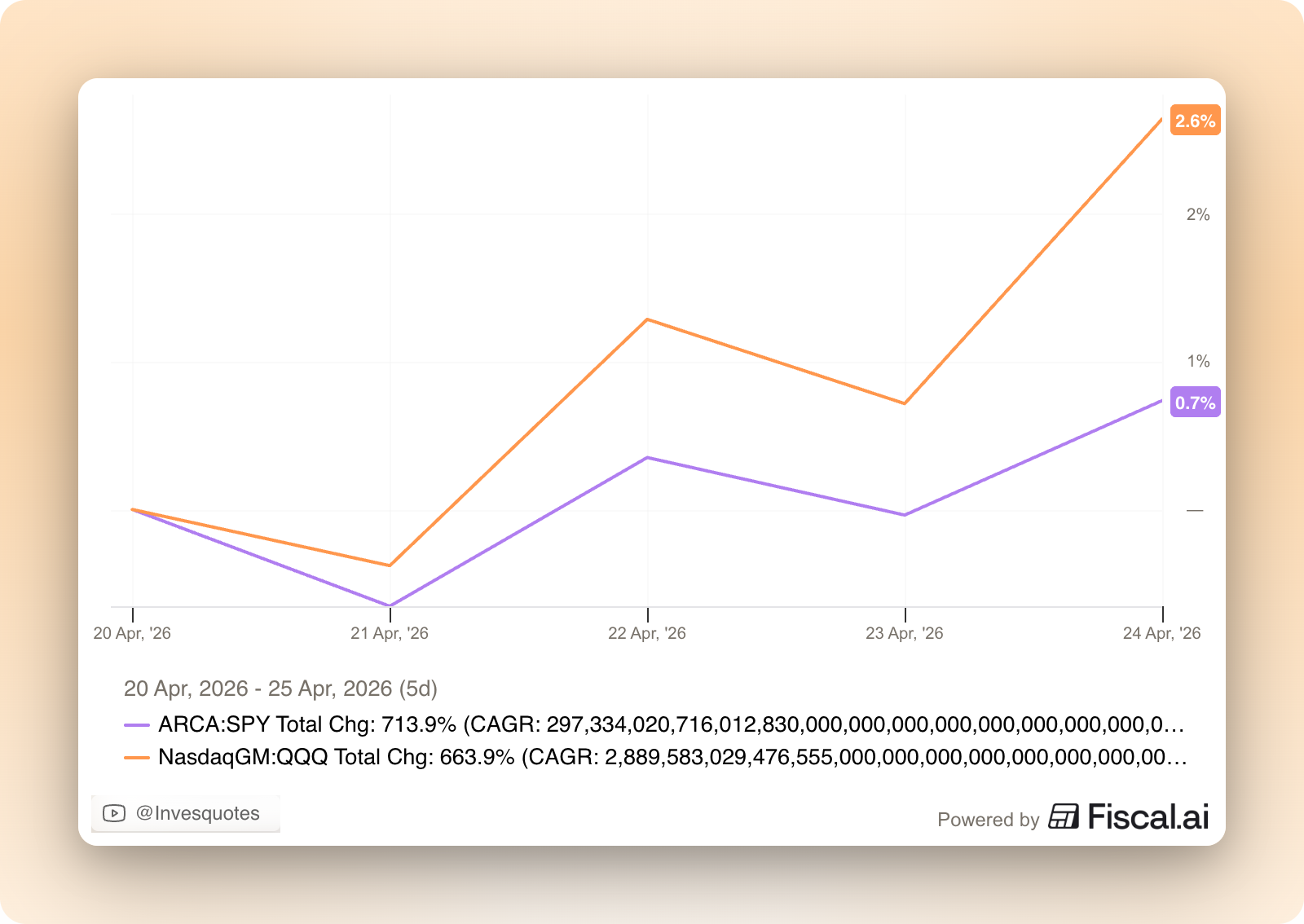

Both indices were up this week, but just like last week, the performance divergence between the Nasdaq and the S&P 500 was stark:

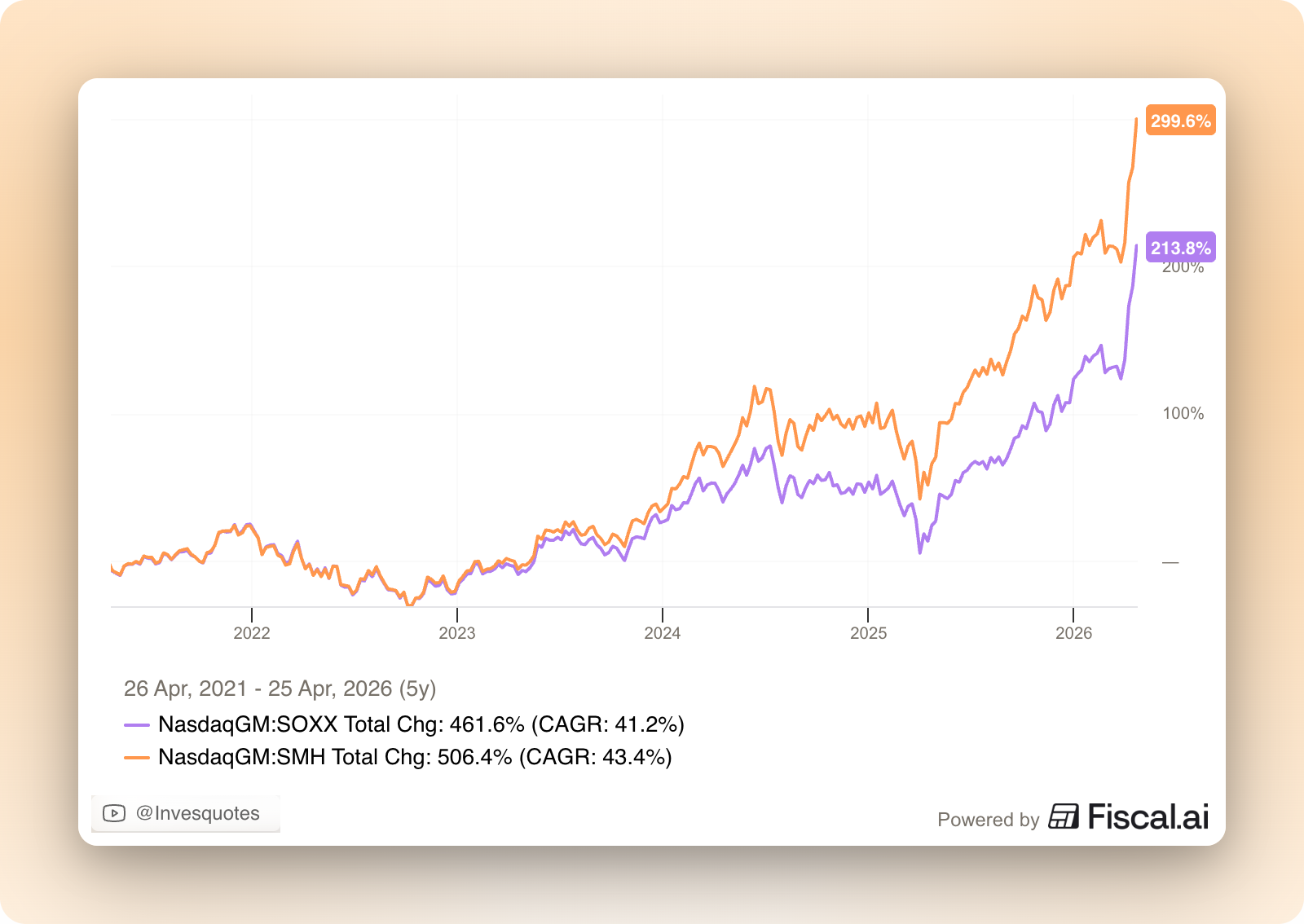

The reason behind this divergence is that the AI trade continues to work wonderfully. Many AI-related companies (you can pretty much choose any subsector you want) are at or close to ATHs. Take a look at where the SOXX and the SMH (semiconductor indices) are trading at and what they’ve done over the past couple of weeks. Amazing:

Now, despite semiconductors being a great industry (because it is) and despite AI being a high-growth technological disruption (because it is), many are starting to wonder whether the rally has gone too far. The reality, though, is that nobody knows the future and there are many scenarios in which one could imagine that semis and AI-related companies are appropriately priced here, despite the run. We shouldn’t ignore that Anthropic/OpenAI etc are the fastest-growing businesses in history, and whether you believe that these businesses have defensible (or not) competitive advantages (we’ll only know in hindsight), that kind of growth is arguably valuable.

Another thing to consider is that of momentum. Momentum is a factor that has been working great for a pretty long time. It simply refers to “buying what’s working” and “selling what’s not,” pretty much without needing to have an opinion on fundamentals and/or valuation (momentum is purely based on past price performance). Take a look at the performance of the SPMO (the S&P 500 index with a momentum skew) compared to the “normal” S&P 500:

The SPMO rebalances the S&P 500 constituents every 6 months according to a momentum score based on the price action over the past 12 months. It has gone vertical over the past few weeks, which pretty much demonstrates that the current rally is being driven by things that enjoy momentum (i.e., what has been working). We have other ways to know whether momentum is driving the markets currently. I found this post interesting:

I’ve run a backtest (thank you Claude and Python) on my portfolio to see how it would’ve performed if I had applied the SPMO strategy to my portfolio, and the results are unsurprising: if I would’ve rebalanced my portfolio every 6 months according to a momentum score, the results would’ve been better. Now, two things are worth noting:

This exercise ignores transaction costs and taxes, which I would imagine would be material with two yearly rebalances

It’s evident that it would result in better performance because I know for a fact that the momentum factor has worked, but what if it suddenly stops working?

The reality is, though, that I have a hard time chasing momentum. In fact, I have a hard time remaining invested in something just because it’s benefiting from momentum. Keysight Technologies (KEYS) is a good example. When Keysight reported very strong earnings a couple of months ago, shares rose 20% to fresh ATHs. The stock was up 100% in around a year, and imho did not offer an appealing risk-reward anymore. It had become a large position in my portfolio so I decided to trim half of it at $298. I also trimmed my position three months earlier at $211. You see where this is going, right? I trimmed against momentum in the semi/AI industry, and that did not play out well, as the shares are trading today at $346 (hey, at least I still hold a smaller position):

Trimming against momentum sucks, but honestly not doing so feels even worse (even though I’ve been wrong before). The other thing you can do to benefit from momentum is to buy all the best performing stocks. Now, this is something that I also don’t feel comfortable with, and not because I believe that something that has performed well has necessarily to do bad, but because I feel that there are very interesting things in the other side of momentum (the negative one, I mean).

Momentum can be great when it’s working in your favor, but it can be terrible when it’s working against you. Common sense would say that if there are flows going into everything that’s working (i.e., that the momentum factor is alive and well) then flows are likely coming out of what’s not working (i.e., the other side of momentum). This, in my view, creates inefficiencies in both sides of the market.

I personally feel better buying in the second pond even if it doesn’t feel great over the short to medium term. One thing worth considering is that, as momentum is purely based on stock prices which sometimes don’t even move with fundamentals, it can change on a dime. You might go from being in the wrong side of momentum to being in the right side relatively quickly, with the cause being a change in the stock price. The price to pay for being early is “opportunity cost” and the pain of being in the wrong side.

Wow, that was a pretty long way of saying that I am not invested in most things that are going vertical (unfortunately).

The industry map was coherent with what I have just discussed: many AI related industries were up significantly, but outside of that the market was meh:

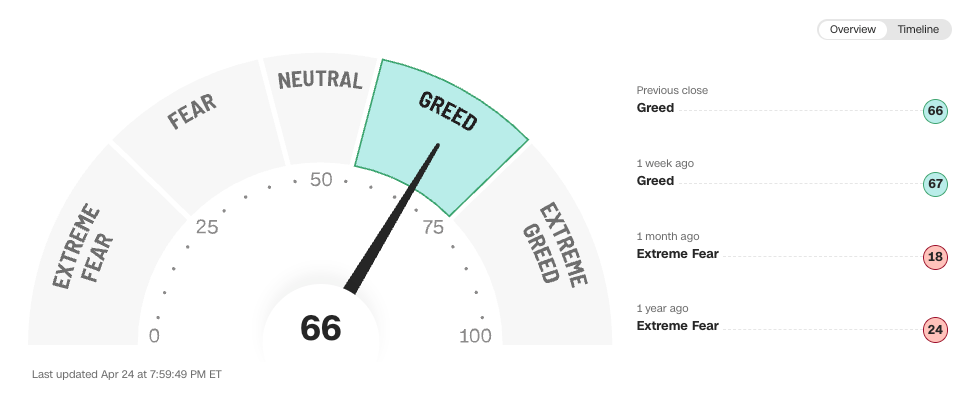

The fear and greed index remained in greed territory:

My additions this week

After a month or so of nothing moving much in the portfolio, I added to one of my positions this week. I feel that the company is posed to deliver (at least) a 15% CAGR going forward and it has been a while since the company has been in cheap territory (according to my estimates):