Markets back to regular programming (NOTW#87)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

Markets went back to their regular programming this week (I’ll explain what I mean in the market commentary). The conflict in Iran seems to be finally winding down, and markets are enjoying it. In the company-specific news section I share news about three portfolio companies:

A notable insider purchase

The resolution of a risk

Great context on heightened Capex investments

Without further ado, let’s get on with it.

Articles of the week

I published one article this week, the first edition of a brand new Best Anchor Stocks series: On the Radar.

I recommend reading that article to understand what the new series is all about, but in short, the goal is to share three interesting companies every week, explaining what I liked about them and why they might potentially make it into the portfolio (or not) upon further research. This week’s article features:

A struggling retailer (turnaround story)

An interesting healthcare business

An exciting aerospace company with somewhat complex accounting

Interestingly, the third company has led me into another company that might end up profiled in the second edition of On The Radar.

More to come in two weeks!

Market Overview

In last week’s NOTW, I wrote that Iran and Trump (or the US, for that matter) had hinted at negotiations to wind down the conflict in the Middle East. This week we got some more (good) news about the topic: a ceasefire was announced (and later breached apparently by both Israel and Iran). Markets reacted positively to the continuous stream of good news (it doesn’t always work this way, though):

Many argue that even if the conflict ends today (which doesn’t seem to be the case), there will be mid and longer term repercussions for the global economy. The argument goes as follows: a lot of energy infrastructure has been destroyed and it’s still uncertain if Iran will have a say on who goes through the Strait of Hormuz. While I do agree with this, it’s also true that markets tend to bottom not when we are out of danger, but when things start to incrementally get better (which undoubtedly seems to be the case here).

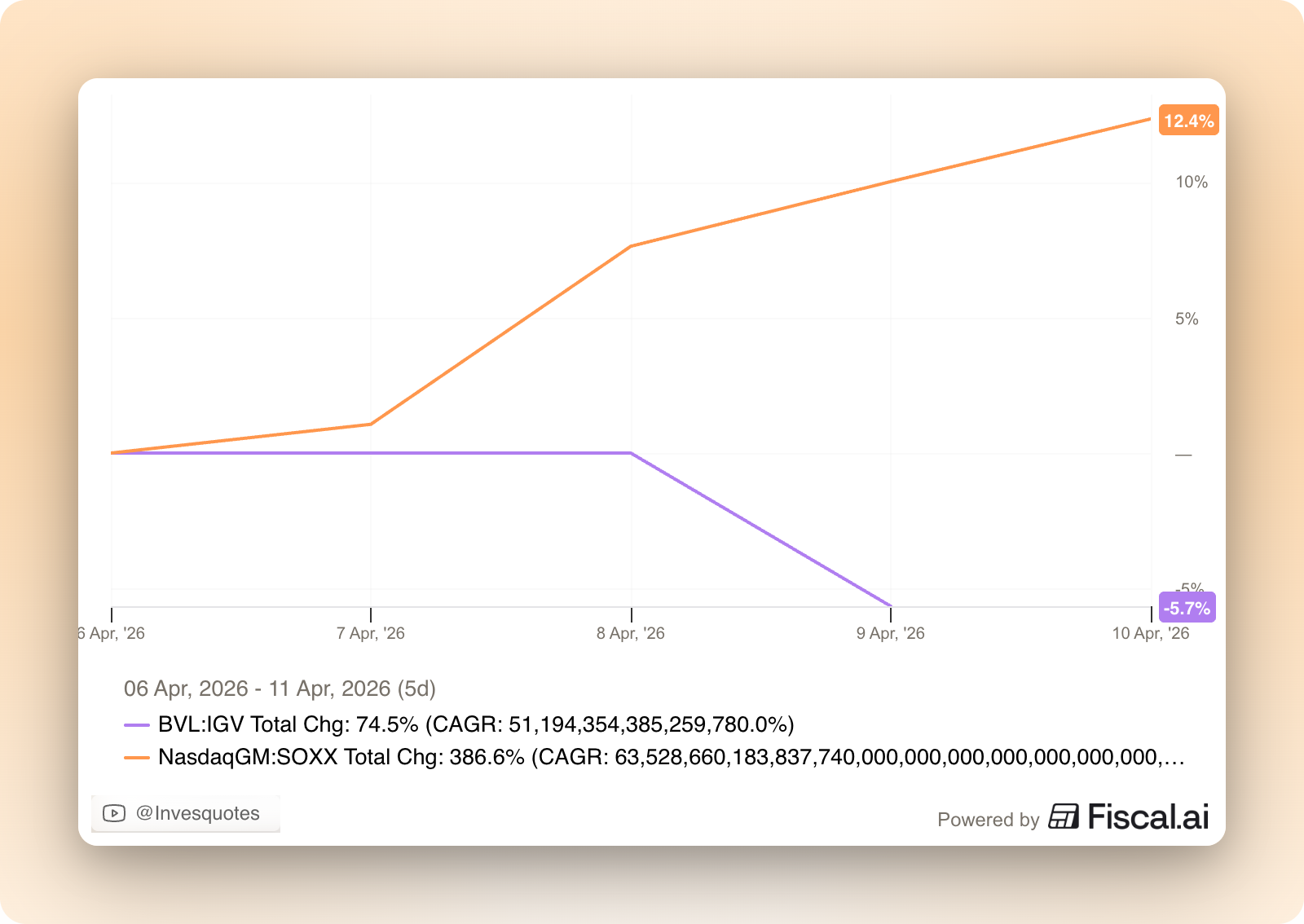

With the conflict now in the “rearview mirror”, markets went back to their regular programming: buying everything that has to do with AI, and selling pretty much the rest. Software probably deserves a special mention. The industry had had a rather peaceful conflict as the market forgot about AI, but things went back to “normal” this week. The IGV (software ETF) was down considerably, while the SOXX (semiconductor ETF) was up considerably. Takeaway? Investors continue to buy AI and sell short the AI “counterparties:”

Two beliefs can be held simultaneously in the software/AI debate. First, that AI is 100% going to render many software businesses obsolete. Second, that AI is not going to render all software businesses obsolete and many will even benefit from AI. With the market believing that AI will pretty much render all software businesses obsolete, there’s likely an opportunity to make money throughout this sell off (I own two software businesses which I evidently believe are in the latter camp).

Now, all this said, there are also very lazy “bull” arguments out there that definitely don’t help the cause. The first one is that AI will help create much more software at a lower cost and that, therefore, the software industry will thrive. I think the main flaw of this thought process is that it ignores the economics…are software businesses going to be able to generate the same historical returns in this scenario? I believe this is where the focus should be and I am not necessarily claiming that the answer is “no.”

Momentum (like it or not) is a very strong factor, and it’s a pretty easy tell where momentum currently lies (hint: it’s not in software). Even though being on the wrong side of momentum sucks, I must say that things can change pretty fast and one can find themselves on the right side of momentum when they least expect it to. We’ll see what happens here but some (not all) software businesses do seem to be pretty beaten down. Others are astonishingly still expensive after the massive drawdown, which makes me think: “what the hell was the market thinking about here?”

The industry map was coherent with what I just discussed, pretty much everything that “smelled” software was down this week:

The development of the healthcare industry continues to be interesting: despite apparently being an AI beneficiary (in most cases) and top lines slowly but steadily accelerating, it remains a laggard.

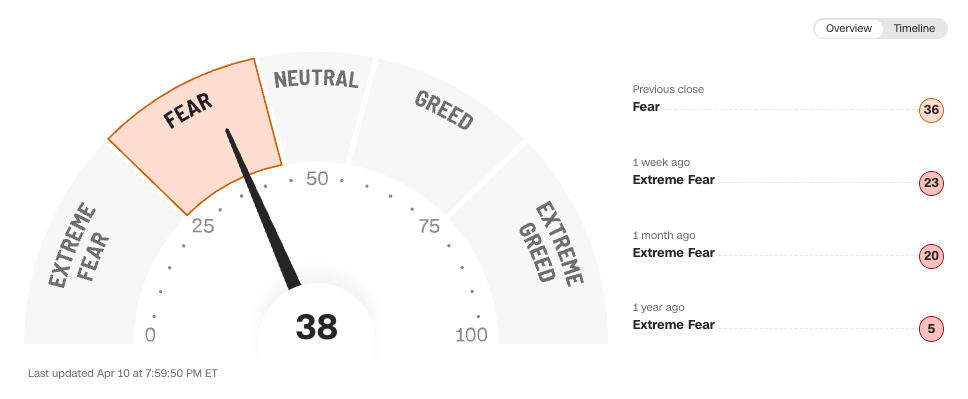

The fear and greed index improved notably with the “resolution” of the conflict: